Gary Yeowell/DigitalVision via Getty Images

Investment Rundown

The rail industry can be quite difficult to invest in. I often think it's a very good reflection of how an economy does, if there is high activity the economy is most likely doing good, and vice versa. With Trinity Industries, Inc. (NYSE:TRN) you are getting a slightly differentiated rail company. TRN is more focused on railcar leasing rather than solely on transporting goods. In the last quarterly report by the company, the revenues increased substantially as TRN recovered its top line. A 65% increase YoY sent the share price up significantly, but it never really seems to amount to anything concrete, at least not in the short term. The stock price continues to bounce around in the same kind of range between $20 and $28. With a 20x FWD p/e though I think we are lacking a little bit of margin of safety here to make for a buy. The company trades at a premium to the rest of the sector, and well, to be frank, I would rather see a p/e closer to 17 to make a buy. In the short term, this means that the stock price would have to fall to the $20 range before I would be a buyer. This might mean that a sell rating is in order, but I would counter with that the dividend yield here is substantial enough that holding shares provides plenty of value. As the saying goes, "The market can remain irrational longer than you can remain rational". I mention this because selling out of a position might just lead to missed gains should the stock price soar if earnings continue to impress. As I begin covering TRN I will do so by rating it a hold.

Company Segments

TRN is a key player in the North American rail transportation sector, delivering a range of products and services through its TrinityRail division. The company is divided into two segments: the Railcar Leasing and Management Services Group, and the Rail Products Group. Within the Railcar Leasing and Management Services Group, TRN leases freight and tank railcars, oversees and administers railcar leases for external investors, and offers comprehensive fleet maintenance and management services. The Rail Products Group complements these services which has provided TRN with a quite strong market presence and something which has driven revenues and earnings higher during the years.

Market Overview (Investor Presentation)

The rail market is recovering in the US according to TRN and I think two major tailwinds for this over the next couple of decades will be the reshoring of manufacturing and deglobalization. These two major trends are present in a lot of countries around the globe. Factories and manufacturing facilities rely on railways to transport a lot of goods. In 2023 the railway industry accounted for over 40% of the long-distance freight volume of all the goods transported in the US. It also showcases the massive market that TRN is a part of. For TRN specifically some of the positive trends have been a steady climb in the fleet utilization rate, indicating good demand is persistent.

TRN has been quite strong in the M&A market and last year in March they acquired RSI Logistics for $70 million. This seems to have been somewhat fueled by debt as the long-term position has risen and debts issued have ticked up recently too. This is one of the concerns I have with TRN right now. The company needs to grow organically rather than just with debt. the cash position is over $100 million and by the end of FY2022, cash was $77 million. This would have completed the acquisition without the need for higher debt levels. I include this in the article since I want to highlight that TRN is making moves to expand its market footprint, but it may not be done in the best way, or at least the way that I would have preferred to see it done. Holding off on raising the dividends even higher might be a better move, and divert more of those earnings toward M&A activity.

Earnings Highlights

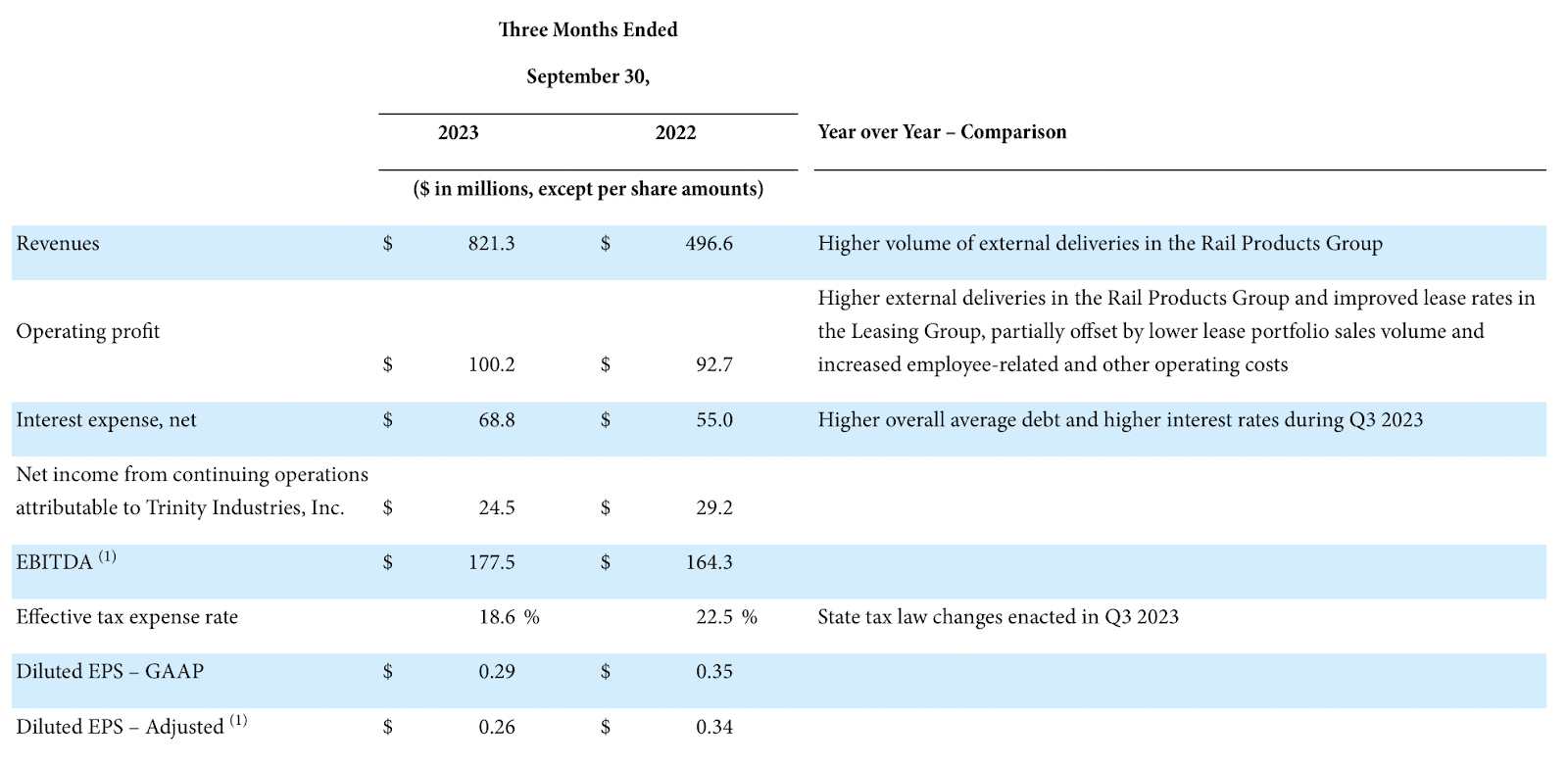

Income Statement (Earnings Report)

Let's take a look at the last report by the company, which I found to be very strong. There were clear improvements in the top line, as it rose by 65% YoY to $821 million. The report came out on November 2 and resulted in the share price quickly rising from $20.7 to nearly $24 per share. It has since its recent high retracted somewhat but not enough that I think it represents a buy. In the third quarter, TRN managed to deliver 4325 railcars and got an additional 3200 on order. The guidance for FY2023 now sits at 45 000 railcars in total which is at the upper end of the previous guidance the company provided in its Q4 FY2022 report. Over the past 12 months, the revenues for TRN have been steadily rising. Back in Q4 FY2022 revenues were $591 million and in fact the revenues have seen consistent QoQ growth all the way back since Q2 FY2022, growing from $416 million to $821 million in the last quarter. This trend I do think will continue, although perhaps not as consistent, more important will be to see a YoY growth instead. Some seasonality does exist which has to be accounted for. For example, the fourth quarter has been hit with weather difficulties, disrupting delivery capabilities somewhat, but also that activity in the sector and new orders are not commonly placed at this time. TRN's net income has since Q1 of FY2023 been trending up from its low of $4.4 million. I do think with stabilizing and possibly declining interest rates the NI for TRN will continue climbing higher even if the revenues plateau somewhat.

Orders (Earnings Report)

Since TRN derives its revenues from delivering a product like railcars, it needs to constantly have a steady supply of demand here to grow the earnings potential. One of my worries is that although the recovery seems to be under way as the last report showed, it's not happening fast enough and 2024 and 2025 may put TRN under pressure. The image above showcases the total orders declining significantly YoY. In 2022 Q3 it amounted to 19 500 in total, but has decreased to 3 200. This does include a long-term agreement of 15,000 railcars from previously. But even removing that it represents a YoY decline. I think the higher interest rates have something to do with this, as it has slowed down capital movement in the industry, as companies hold back on hefty investments, which were far more prevalent during 2021 and 2022. With rates set to decline though in 2024, it bodes well for future demand but the impact might not be noticed until 2025 for TRN. This means that the share price might continue to tick down until the trend reverses.

Valuation (Seeking Alpha)

On a valuation basis, I think TRN represents too little value currently. The company has an FWD p/e of 20.5, an 8.7% premium to the industrial sector. With some of the potential setbacks that could happen to TRN, I would want a better margin of safety. A 15% discount to the sector based on earnings I think is fair to require here. This would mean a p/e of 17 here. Estimates seem to suggest a strong recovery in 2024 for the bottom line, but I would be more pessimistic as the debt accumulation will still put a lot of pressure on the bottom line even if rates decline slightly. I think the analyst's estimates are based on a strong recovery in the rail industry, but I think you have to remember that a lot of companies are coming off a period of both layoffs and high-interest expense payments. The first thing to do won't be to fill up their order books instantly. Within TRN it would have to very rapidly raise its margins in order to support that sort of EPS increase YoY. Materials costs have risen in recent years and that won't go down quickly either I think, this will all trickle down to affect the future EPS, which is why I am perhaps less optimistic compared to the analyst estimates of the EPS the coming few years. I have TRN as a hold but my price target for them in the short term will be in the lower $20s preferably under $21 to get me that margin of safety given the risks with the business.

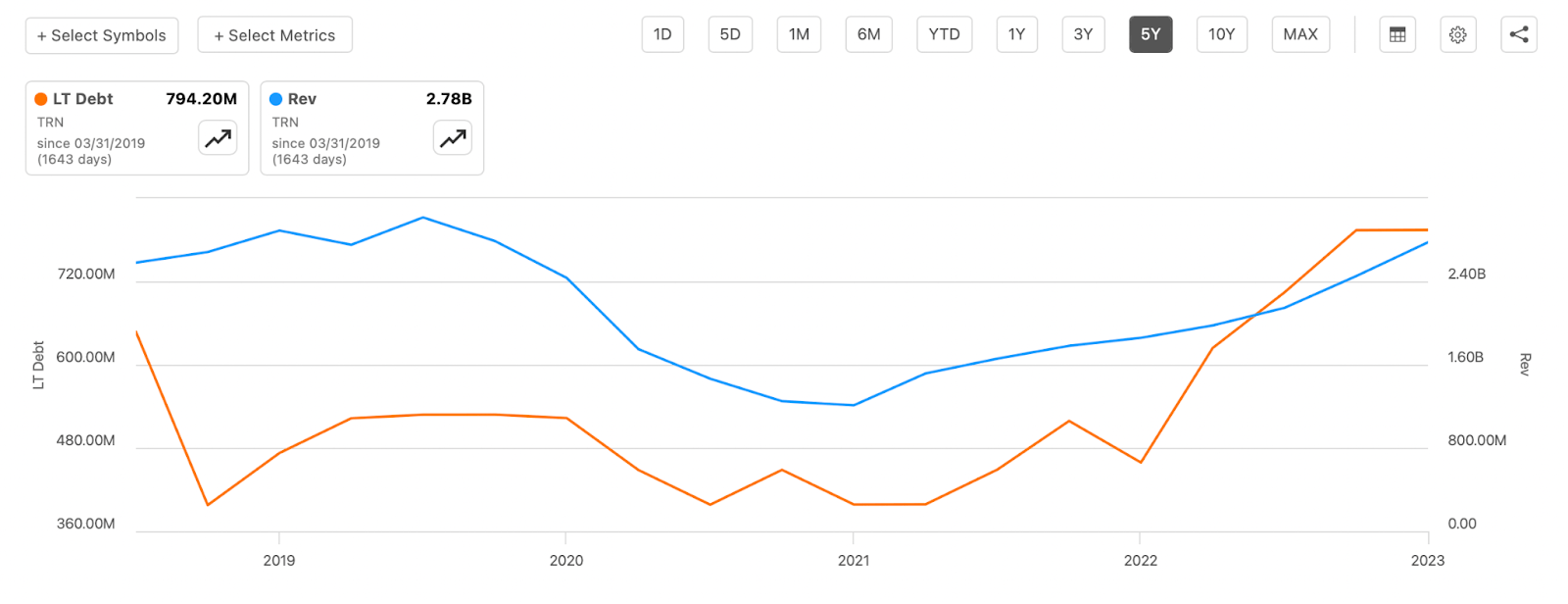

Debt Profile (10Q)

When assessing the debt profile a little closer for TRN it's visible that there is a decent chunk of debt maturing in 2024, $399 million to be precise. This can't be covered by cash, as it's at $105 million right now. TTM NI of $74 million is also not sufficient enough to cover this amount, which brings into question how TRN will go about covering it. My worry is share dilution which would lessen the value of the stock price. In total, the company's debts are at $5.7 billion, and whilst it seems to have aided a growing top line it has also meant that in times of higher interest rates, the bottom line has taken a hit. Growth here over time has been quite inconsistent.

Going forward I think TRN will be diverting more capital towards paying down debt and possibly reducing the amount of shares they are buying back. If they continue down the road of taking on debt to fuel debt and then get hit with another period of high interest rates they will have their hands tied behind their back as a significant amount of operating income will go to interest expenses instead. I do think 2024 will be a year of slight consolidation for the company as it improves its financial standing. It's sort of a wait-and-see period now I feel like and that ties into why I have them as a hold rather than a buy.

Risks

An area of risk regarding TRN revolves around its current debt levels. The company appears to be supporting its growth through debt accumulation, a strategy that, while effective in recent years, may not be sustainable in the long run. Overreliance on debt without concurrent evidence of robust organic growth could expose TRN to potential disruption from larger competitors. This scenario might leave TRN burdened with high debt levels and diminishing cash flows. If TRN struggles to demonstrate commendable organic growth, it could lead to a need for even lower valuations, presenting a short-term risk for investors.

Debt & Revenues (Seeking Alpha)

The chart above here I think shows very well how the last few years debt levels have ticked up very high. It might have been at the right time as the industry is recovering, but TRN needs to rearrange its capital priorities now and put more on debt repayments rather than value increases for shareholders like dividend raises or buybacks. I think it poses a short-term risk more than anything.

Apart from the debt levels of the company, I do think the valuation poses a risk to investors. Trading above sector average multiples like both p/e and EV/sales on an FWD basis does mean that in broader market sell-offs the stock price for TRN could fall faster and harder than others trading at lower multiples. Materials costs have also risen in the US and seeing as TRN uses a lot of steel to manufacture their products, that being railcars among others will be impacted by this. The war in Ukraine helped spur prices up for steel very quickly, they have since settled but I think further volatility could occur, and impact the short-term EPS of TRN, possibly leading to a lower multiple being applied.

Final Words

The rail industry is significant in the US as nearly 30% of all goods transported go by rail. This leaves TRN with a big market to service as railcars depreciate over time and constantly need to be replenished for big companies to continue to operate. My worry with TRN is that the growth has been fueled by debts and even if rates decline, TRN will be stuck with a high level of interest expenses to pay down, limiting its M&A possibilities. Given that I want at least a 15% margin of safety, leaving me with a short-term price target of $20.5 for TRN. Holding shares still makes sense though I think as the dividend is high enough to price enough value, along with aggressive share buyback practices by TRN management. For instance, shares have declined an average of 7% going back to 2019 when it was 125 million outstanding, now under 82 million. Over time it seems to have led to a less liquid balance sheet with low cash levels and higher debt instead, a move I don't personally like seeing, even if it does benefit shareholders in the short - medium term. Over the long-term, it could add more risk instead. In conclusion, though, a hold is my rating for TRN.