mixmotive

S&P Global Inc. (NYSE:SPGI) is set to report its FY23 results at the beginning of February, in a print that should mark the turning point for the financial information services empire.

Following two years of macro uncertainty which led to a depressed debt market, lower index-linked assets, and prolonged sale cycles, S&P's businesses are all set to experience tailwinds in 2024.

Coming in with a reasonable valuation and conservative consensus expectations, I believe S&P Global is due for a beat on revenues, EPS, and guidance, which will set the stage for a market-beating 2024.

Let's dive in.

Brief Business Overview

I've covered S&P in several articles in the past, outlining its segments and post-merger financials, and the temporary headwinds it experienced.

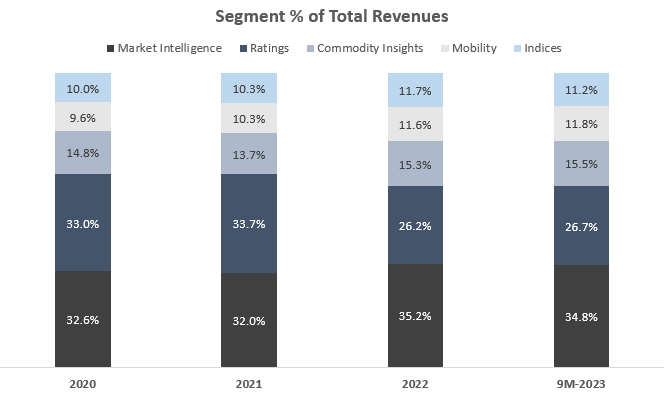

S&P Global operates under five reportable segments: Market Intelligence, Ratings, Commodity Insights, Mobility, and Indices.

Created and calculated by the author using data from S&P Global financial reports

Although it is mostly known for the ratings business, we can see that S&P Global generates 65-75% of its revenues from other activities, which primarily include its proprietary indexes, and financial-related software solutions for market intelligence, commodities, and mobility.

The Last Two Years

Since completing the $44 billion acquisition of IHS Markit in 2022, the company experienced several headwinds.

In its software businesses, which mostly cater to enterprises, the deteriorating economic environment resulted in longer and tougher sales cycles, although high demand in the automotive industry and volatile commodity markets offset these tailwinds in the Commodity and Mobility segments.

In the Indices segment, declining AUMs linked to the company's indexes weighed on results.

And, the Ratings segment, which is the largest contributor to the company's profits, experienced a sharp decline due to muted debt activity. Normally, the segment contributes approximately 34% of total sales and 45% of operating total profit, whereas in 2022-2023, it dropped to 27% and 33%, respectively.

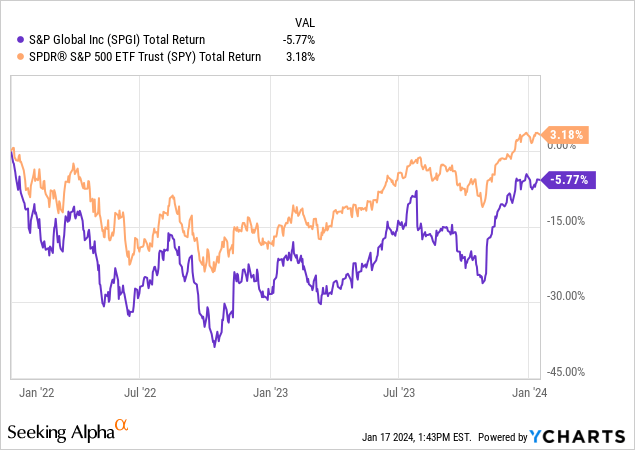

As we can see, the company's headwinds resulted in almost a 9% underperformance compared to the S&P 500 over the past two years, with SPGI still trading below its 2021 highs.

Such periods lead some investors to the perception of S&P as a cyclical company, although I believe they are missing the forest for the trees. While occasional cycles of tougher macroeconomic environment lead to temporary headwinds, global debt, and equity has been growing sequentially for more than 100 years.

In essence, S&P Global is a leverage play on global GDP growth, as the company captures more and more value over time.

Considering the strong moat across every line of its business, its strong balance sheet, and prudent management, investors shouldn't ask themselves whether or not S&P will be able to withstand these headwinds. Rather, they should ask themselves when will the headwinds turn into tailwinds, in the form of easy comparisons and a more efficient operation.

And the answer, in my view, is 2024.

The Game of Comparisons

Eventually, stock price follows earnings growth. That is one of the most important observations made by Peter Lynch and other world-renowned investors.

That means, in a weird way, that a so-called bad year could become the most significant tailwind for the year that follows. Just ask Alphabet Inc. (GOOG, GOOGL), Meta Platforms, Inc. (META), and other 2023 stars which drove huge outperformance as their earnings recovered from the 2022 trough.

For S&P Global, the last two years were quite bad. Looking at pro forma numbers, revenue declined by 4% in 2022 and is expected to grow by 5% in 2023. Net income declined by over 33% in 2022 and is expected to remain flat in 2023 (on a GAAP basis).

However, that is to be expected during a down cycle in the Ratings business, which was essentially the sole driver for the earnings decline, as all the other segments saw profits grow in both 2022 and 2023.

If Ratings return to normality in 2024, S&P's earnings are going to experience a sharp recovery, which will mark the beginning of the next sequential growth period for the company.

Will Ratings Return To Normality In 2024?

Well, normality might be too much to ask amid an election year, growing geopolitical tensions, and an uncertain rate/inflation environment. That being said, we're already witnessing a significant pickup in debt issuance, as well as the easy comparison effect on results.

In Q3'23, the Ratings business grew sales by 20.3%, and the segment's adjusted EBIT increased by 21.8%, both significantly accelerating from the second quarter.

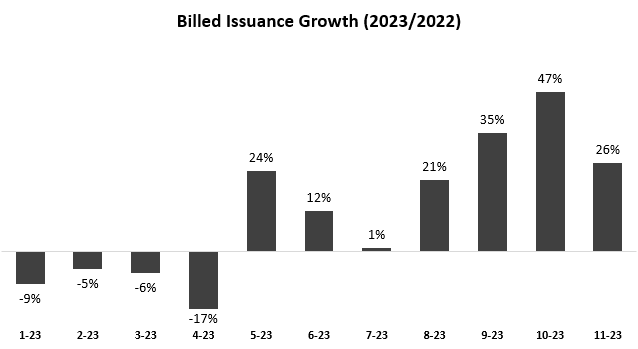

Created by the author based on S&P Global publications; Billed Issuance = Total par value of issuance billed by S&P Global Ratings.

Looking at billed issuance, for the last four monthly publications, S&P Global reported issuance growth north of 20%, which is another sign the recovery has already begun.

Plenty of companies stretched out their debt refinancing hoping for a more favorable market, and management has been consistent with saying that the most important driver for refinance isn't lower rates, but more certainty.

While the current macro environment remains challenging, and the public markets are still quite volatile, most companies are already done with their efficiency/defensive phase and are ready to invest in growth. In addition, some financing needs are becoming a necessity, and cannot be postponed anymore.

With that in mind, I'm expecting great results in the Ratings segment for the fourth quarter, as well as better-than-expected guidance for FY2024.

Other Tailwinds To Consider

Being the number one headwind, the recovery of the Ratings segment is unquestionably the most important factor. With that said, there's plenty to be optimistic about across other parts of the business as well.

First of all, the Indices business, which generates more than 60% of its sales from asset-linked fees, is set to begin 2024 with a much higher asset base compared to 2022.

Due to the averaging effect of AUM on fees, a favorable base to begin the year is hugely important. In Q3'23, the company reported a total of $2.85 trillion in assets under management linked to its indexes, a 21% increase Y/Y. The S&P 500 is up an additional 10% since, so I'm expecting continued growth in Q4.

Secondly, in the software businesses, management stated that the longer sales cycles result in larger deals and continued volatility should help drive growth across the product line.

Lastly, the implementation of IHS Markit continues, and 2024 will mark the first full year of cost synergies, which ended the third quarter at a $588 million run rate, which is 98% of management's target. That, as well as higher revenue synergies and lower deal-related and implementation-related costs, should all drive higher margins and growth in 2024.

Valuation

Let's keep things simple.

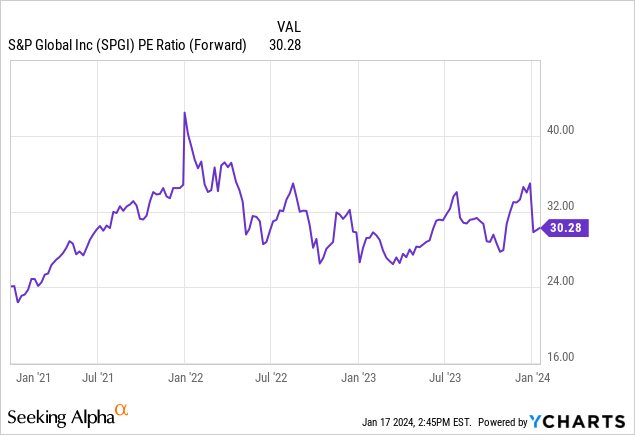

S&P is trading at a 30x multiple over the consensus 2024 EPS, which is in line with its historical average. However, I believe that there's still significant upside.

Based on all the tailwinds I listed, I believe current consensus estimates are too low. I expect that even a small recovery in ratings, combined with a higher AUM baseline, and full-year contribution of cost synergies will result in much more than the current 7% revenue growth and 2% margin expansion Wall Street conservatively projects. In fact, I'm expecting the initial guidance will come higher than that.

As the company leaves its 2022-2023 headwinds behind, I estimate it'll go back to its normal steady-state double-digit EPS growth for the foreseeable future, and a slightly below-average valuation provides an attractive enough entry point, considering the quality of S&P Global.

Conclusion

S&P Global had a rough couple of years, defined by macro uncertainty and a prolonged implementation process of its mega acquisition.

In 2024, I'm expecting most of the headwinds to transform into tailwinds, as S&P Global comes into the year as a more efficient company.

While the macro environment is far from perfect, debt activity is already high, and linked AUM is approaching all-time highs.

I estimate 2024 will mark the end of this down cycle for this long-term compounder, and reiterate S&P Global as a Buy.