SOPA Images/LightRocket via Getty Images![]()

Business Model

DLocal Limited (NASDAQ:DLO) is an online cross-border payment experience in emerging markets. Through one API (Application Programming Interface) one technology platform enables global enterprise merchants to get paid (Pay-In) and to make payments (Pay-Out) online in safety. DLocal operates conversion rates, reduced friction, and enhanced fraud prevention, which enables us to serve nearly 2 billion potential combined internet customers in the countries we serve. Its cloud-based platform can power both cross-border and local-to-local transactions in 40 countries, and using over 900 local payments methods.

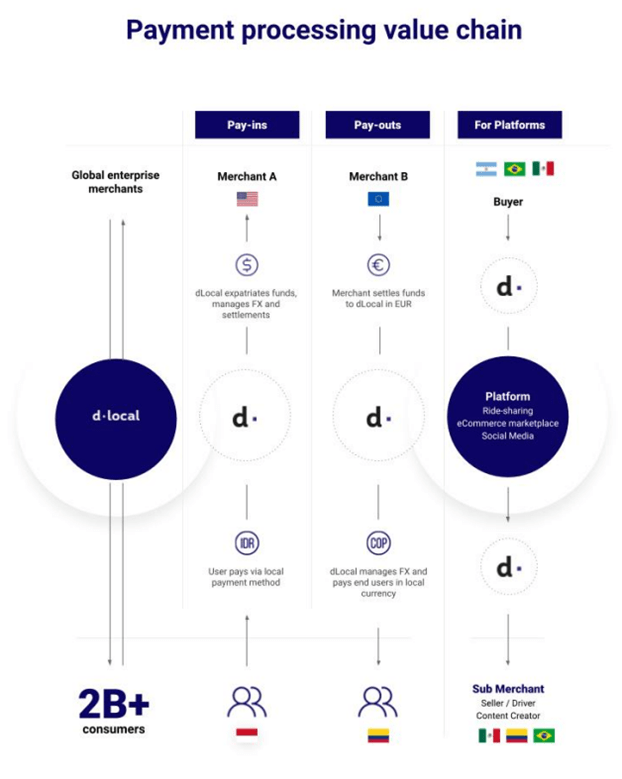

Payment Processing Value Chain (DLocal presentation)

DLocal prides itself on a powerful business model built on rigorous vetting of industry giants. This lengthy process ensures direct relationships with merchants: no intermediaries, only one API and a contract for access to DLocal's full suite of solutions across its extensive network. This frictionless approach, along with economies of scale, makes each additional deal highly profitable for DLocal, solidifying its competitive advantage and high barrier to entry.

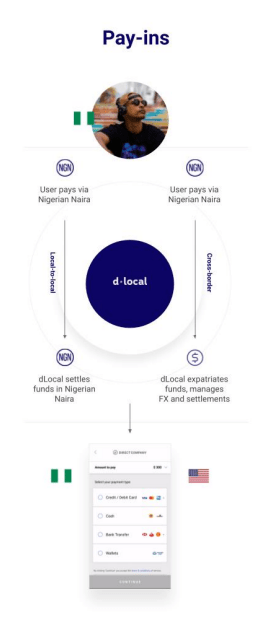

Pay-In

Pay-ins (DLocal presentation)

Pay-in - Enables global merchant's payment methods, including national and local cards, debit cards, bank transfers, e-wallet, and cash payments. This allows customers to pay for their online purchases using their preferred methods, allowing global merchants to target large users all over the world. It's a trust that delivers higher conversion rates and lower friction for our merchants. Mainly global and regional competitor payment.

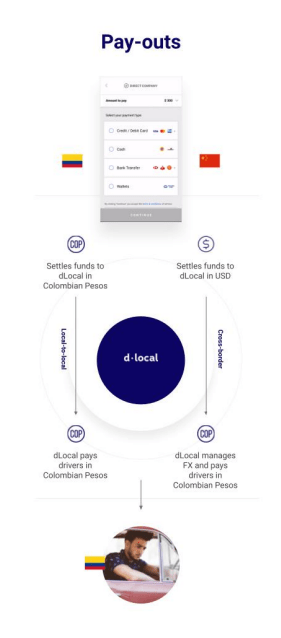

Pay-Out

Pay-outs (Dlocal presentation)

Pay-Out - Launched in 2016 to meet the growing needs of our users. Enables our users to pay for their partners, suppliers and contractors in the emerging market. Pay-Out has shorter processing times (same-day or same-day settlement for cross-border transactions), while focusing on customer service and improving flexibility and transparency, providing the ability to scale pay-out operations while reducing risks and operational burdens. in emerging markets. Pay-Out competes primarily with global and regional banks, and also competes with payment specialists who focus on direct relationships with merchants.

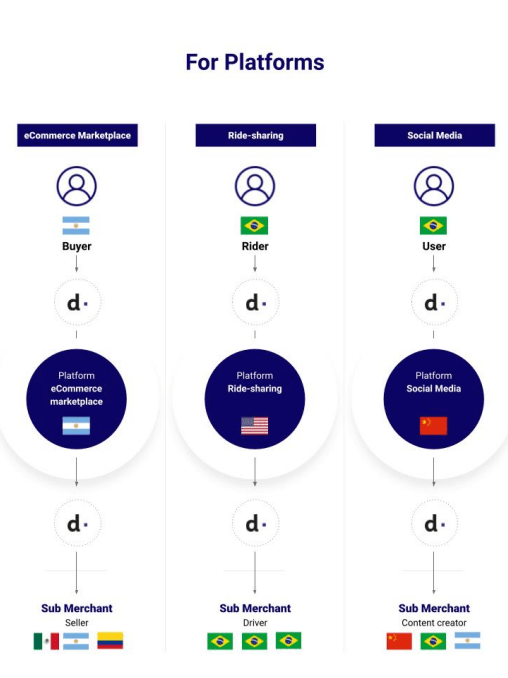

Platform

Platform (DLocal presentation)

In 2022, DLocal announced "dLocal for Platforms", an innovative white-label payment whose main solution is to provide a comprehensive and scalable approach to managing global platform payments in one place. Designed for e-commerce marketplaces, ride-sharing companies, social networks, etc. One of the offerings that "Platforms" provide is Know Your Customer (KYC) and Anti-Money Laundering (AML) verifications with minimal disruption, making it easier for platforms to manage user verification, reducing fraud risks and ensuring compliance with local regulations. Moreover, this solution offers dynamic tax and fee calculations based on the sellers behind the purchase, ensures that the platform can handle complex payments with ease and accuracy, also offers money management services, platforms can split transactions between multiple accounts, deduct platform fees and pay to local or international users. Finally, our solution provides comprehensive platform management tools, including unified reporting, refund and refund management, and account configuration management via API or our merchant dashboard.

Direct Issuing

Launched in 2021, Issuing as a Service is a solution that allows global merchants to create their payment system. DLocal offers their global sellers the ability to issue prepaid credit cards and credit cards to their end users.

After doing a comprehensive business breakdown, let's dig into the company's fundamentals, and valuation and see if the company is as great an opportunity as SA analysts say it is

SA Analyst Rating (Seeking Alpha)

Growth Trajectory

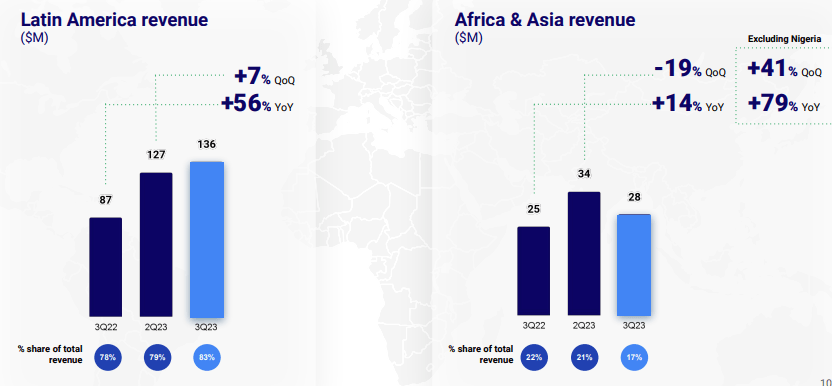

DLocal's Q3 2023 paints a contrasting picture across continents. In Latin America, the company dominates the record, showing a steady increase of 7% QoQ and 56% in annual revenues, consolidating its market share of 79%. This area remains a growth engine, driving DLocal's overall success. However, Africa and Asia (excluding Nigeria) present a different story. A 19% drop in QoQ and 8% in revenue this year, despite a healthy 17% market share, raises questions. While this may be a blip after a stellar Q2 performance, macroeconomic factors or increased competition are worth checking out. However, this year's positive growth and DLocal's ongoing expansion efforts point to long-term potential in this diverse region. The key is DLocal's strategic dominance in Latin America, along with its ambitious reach in emerging markets such as Africa and Asia, positioning it for continued growth and strengthening its competitive advantage in the global payments landscape.

Revenue by Region (DLocal Presentation)

TPV (Total Payment Volume)

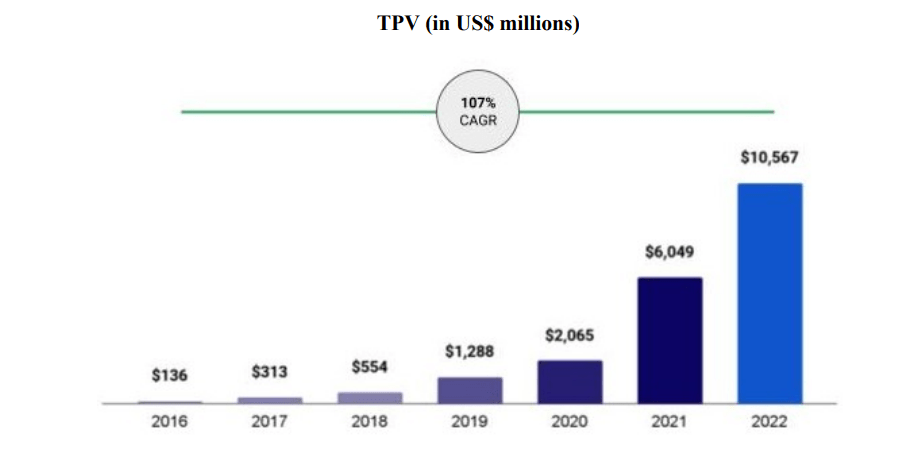

I believe that TPV (Total Payment Volume) is one of the most important indicators of the success of its global merchants, it represents the satisfaction of its end users, the scale and the growth of the business. Since the increase in TPV means that the global merchants are increasing their transaction volume, and DLocal is a company whose revenue comes from a fixed percentage per transaction or a fixed commission per transaction, makes us understand that this is one of the most important indicators for the company if not the most important.

Total Payment Volume (DLocal Presentation)

When you look at the graph above, the graph does not sound in two faces, even a 5-year-old can tell you that this is a successful picture. The TPV has grown by 107% (CAGR) over the last 7 years, and in the last year grew by more than 57% annually. On the face of it, a great image for DLocal, shows its growth, and its strength over the market share it takes from competing companies, establishing itself as a leader in its field. But not everything is shiny, which brings us to the main problem I see with the company that I have yet to see the analysts address.

Gross Profit Margin (Based on DLocal financial data and my own calculations)

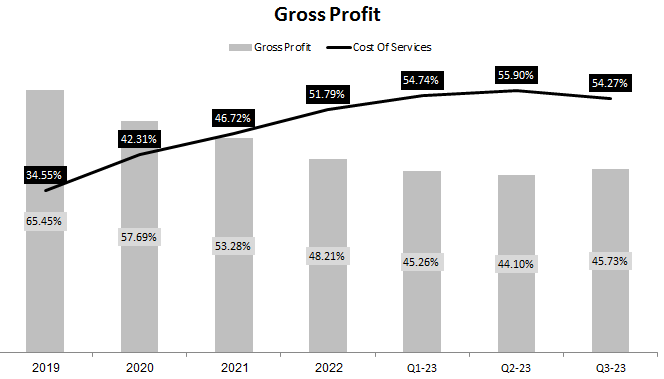

Let's focus on the most important indicator for DLocal, the gross profit from 2019 decreased by 19.72%, while the TPV is growing. Basic software fails to improve gross profit. The increase in processing costs is related to the TPV growth of 74.7% compared between 2022 and 2021, and the average processing cost increased from 1.8% of the TPV to 2% of the TPV. 2021 to 2022 respectively. This means that over the last 5 years, DLocal has not been able to optimize its profit costs, the average processing has increased from 1.8% to 2% in the last year. For me, this is a big red flag flying over the company that cannot improve its gross profit which is a software company after all. As we can see in the last quarter we have seen a decrease in the cost of services, I would like to see this trend continue to move to consider starting a position.

Operating Costs (Based on DLocal financial data and my own calculations)

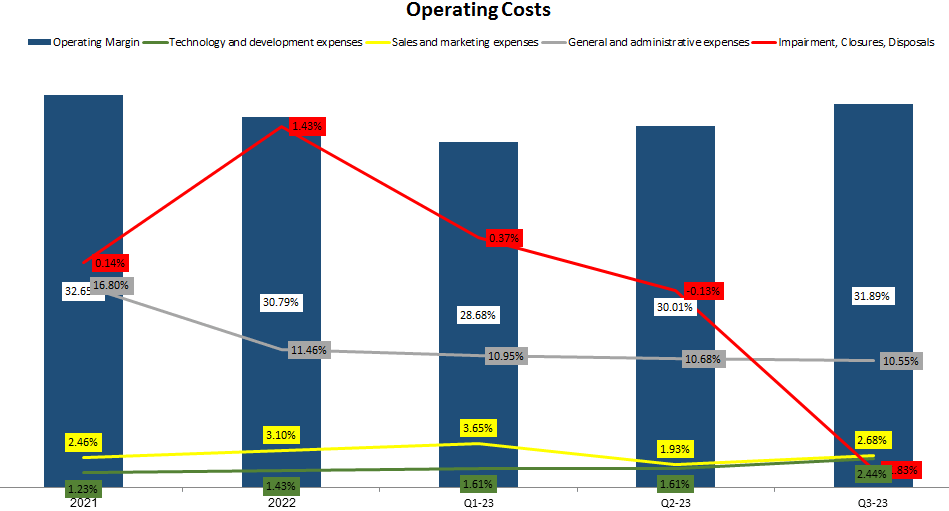

Moving on to the operating profit, as we can see DLocal has remained stable at an operating profit rate of 30% in the last 3 years. As technology and development spending rose 1.21% from 2021 to 3Q23, mainly for higher employee wages and salaries, and a higher headcount in information technology to support its growth strategy. Sales and marketing expenses increased slightly (0.22%), mainly the increase in wages and salaries and marketing expenses. General and administrative expenses decreased by 6.25% from 2021 to the third quarter-23. Impairment, closures, and disposals decreased from 0.14% in 2021 to 1.83% in Q3-23.

NRR (Net Revenue Retention Rate)

NRR - Net Revenue Retention Rate is a dollar-based measure of DLocal merchant retention and growth. Simply put, NRR is a metric used to measure the retention and growth of revenue from your existing merchants over some time, usually a year. It shows how successful you are in keeping your current customers, encouraging them to spend more and preventing churn.

| Interpretation of NRR: | ||||||||||

| NRR above 100%: This indicates you're growing your revenue from existing customers, meaning they're spending more on average. | ||||||||||

| NRR around 100%: This means you're barely maintaining your existing revenue base. | ||||||||||

| NRR below 100%: This indicates you're losing revenue from existing customers, potentially due to churn or contractions. | ||||||||||

I believe long-term revenue growth is correlated with growth in existing merchants and existing PSP partners, as a company that strives to maintain industry-leading levels of customer service and platform capabilities to maximize customer success and retention, to continue to grow its revenue. DLocal should strive to increase the number of global merchants using its platform.

Revenue by merchants (Dlocal -10K)

As we can see above, DLocal manages to keep its merchants as the NRR was 165% for the full year ending 2022, meaning as I wrote above:

NRR above 100%: This indicates you're growing your revenue from existing customers, meaning they're spending more on average.

When DLocal manages to keep existing merchants, they add $17,091 from new merchants.

Valuation

I decided the best way to value DLocal is not to model DCF which is very far away from achieving steady-state metrics, we'll do some simple back-of-the-envelope valuation first.

Today, DLocal trades at a multiple of 26.2x EV/EBITDA. let's apply a more conservative multiple of 16x. Now, let's take 2028 as our target year, Given DLocal's projected expansion in emerging markets, targeting 2028 assumes it will achieve a stable operating state within five years.

In 2028, I expect DLocal to generate just over $2.3 billion in sales, reflecting a CAGR of 28.9% from 2023 levels. Taking an EBITDA margin of 35%, which is my assumption for 2028, we arrive at $840 million of EBITDA. Multiplied by our fair multiple of 16x, our back-of-the-envelope takes us to a $13.4 billion EV in 2028, representing a 194% upside to today's valuation.

While I expect DLocal to return an annualized return of 38% over the next five years. In my opinion, that's a bit high. Considering all the unknowns, I would ask for an annual return of at least 25%.

Conclusion

DLocal presents a compelling investment opportunity in the burgeoning emerging markets payments space. Its robust business model, impressive growth trajectory, and strong merchant retention indicate significant potential for long-term value creation.

However, concerns regarding rising processing costs and the sustainability of growth in Africa and Asia warrant further consideration.

Therefore, DLocal is a "Buy" with a cautious outlook. While the potential upside is undeniable, investors should monitor key metrics like gross profit margins and regional performance closely. A conservative annualized return target of 25% seems more reasonable than the 38% suggested by the back-of-the-envelope valuation.