NurPhoto/NurPhoto via Getty Images

Investment Thesis

Almost 11 months have passed since I first covered Kroger (NYSE:KR) and assigned the stock a "Buy" rating. Despite the stock substantially lagging behind the S&P 500 over the same period, it is difficult for me to say that my bullish thesis did not age well. KR delivered a solid 9% return over the last 11 months, and there were periods of robust rallies. Today, I want to update my thesis because quite a lot has happened, especially in recent weeks. The company's recent and upcoming earnings add optimism to me. However, the lagging behind the scheduled merger with Albertsons (ACI) adds more uncertainty. Still, regardless of a potential business combination, Kroger is still a high-quality business demonstrating consistent profitability and appealing dividend growth. I expect the merger to eventually proceed, but even with the worst-case scenario of the merger being completely banned, I think that Kroger will remain a retail superstar. Moreover, my valuation analysis suggests that the stock is very attractively valued. All in all, I reiterate my "Buy" rating for Kroger.

Recent Developments

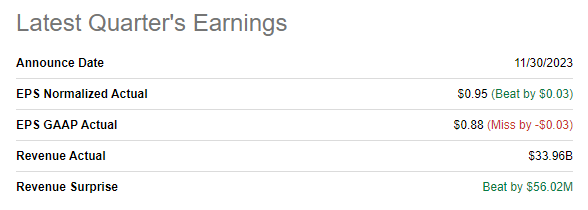

Kroger released its latest quarterly earnings on November 30, when the company topped consensus estimates. Q3 revenue was almost flat on a YoY basis, and the adjusted EPS expanded by seven cents. It has been almost two months since the Q3 earnings release, so I will not waste much of the reader's time. I will underline that Kroger's profitability metrics kept up well despite the uncertain macro environment.

Seeking Alpha

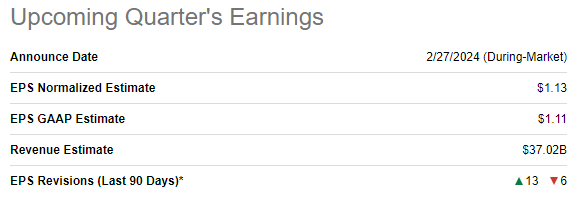

The upcoming quarter's earnings release is scheduled for February 27, and consensus estimates dynamics look quite optimistic. There were 13 upward EPS revisions over the last 90 days, which I consider a positive sign. Q4 revenue is expected to be $37 billion, which means a solid 6% YoY growth. The adjusted EPS is expected to follow the top line and expand from $0.99 to $1.13.

Seeking Alpha

Kroger's Q4 and full fiscal year ends at the end of January, meaning that it captures the U.S. holiday season, which includes Thanksgiving and Christmas. Therefore, looking at the overall dynamics of the U.S. holiday spending would be useful information to assess how well Kroger is likely to be positioned to deliver strong top-line results. According to Mastercard Spending Pulse, U.S. 2023 holiday spending decelerated notably from the previous year, with a modest 3.1% YoY growth.

Mastercard Spending Pulse

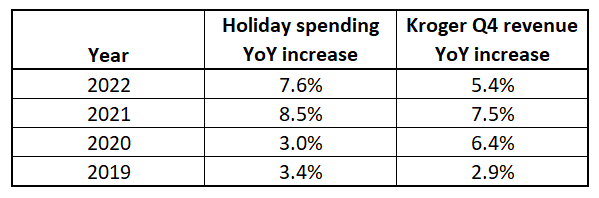

Let me compare how Kroger's Q4 revenue correlated with Mastercard's Spending Pulse data year by year. As we can see below, historically, Kroger's Q4 revenue growth mostly fell behind the holiday spending dynamics, with the pandemic 2020 being the only outlier. Therefore, I am slightly skeptical about the expectations that Kroger will deliver a 6% YoY growth. On the other hand, Kroger usually delivers positive revenue surprises in the last quarter of the fiscal year. Overall, I have mixed expectations about Kroger's ability to deliver a positive revenue surprise in Q4. I am more optimistic from the EPS perspective as Kroger demonstrated improved profitability in each of the three first fiscal quarters, which is a strong sign that Q4 EPS dynamics will also be strong.

Compiled by the author

After discussing the latest and upcoming earnings, I now want to move to the "elephant in the room", the potential Kroger-Albertsons merger, which is now uncertain since Washington state wants to block the deal. The state's Attorney General's concerns are related to the potential adverse effect on prices, which might ultimately hurt consumers. I think that rumors regarding potential mass layoffs as part of two businesses integrating are also seen as a potential long-term problem for local governments. On the contrary, in its press release of January 15, Kroger announced that the combined business would mean lower prices and a better shopping experience for consumers. The company also announced in the same press release that the company is committed to retaining frontline employees after the deal.

While concerns of governmental bodies might look sound, I tend to believe that the merger will indeed be beneficial for customers. Kroger and Albertsons are both retail giants with extensive retail, storage, and logistics facilities. Leveraging Kroger's impressive track record of achieving remarkable profitability in the highly competitive retail sector, I am confident that the amalgamated business will generate substantial synergies from its consolidated facilities. This synergy, in turn, is poised to reduce operational costs, ultimately translating into added value for customers. Therefore, I believe that after more thorough scrutiny from the governmental bodies or the court, the merger will likely eventually get a "green light."

Seeking Alpha

I would also like to draw readers' attention to the fact that Kroger's stock price does not vary far from the October 14, 2022 levels, when the first official announcement regarding the merger went live. Furthermore, the stock has maintained a relatively narrow trading range for several months, indicating that news about the merger has had minimal influence on its price. I believe this stability is attributed to the market's recognition of Kroger as a high-quality business, irrespective of its association with Albertsons. The company demonstrates consistent profitability, its balance sheet is healthy, and its dividend growth is solid. Moreover, let us also not forget that the expected merger will not only potentially unlock more cost synergies but will also bring a substantial portion of challenges related to integrating the two businesses.

Valuation Update

KR delivered a 3.3% return over the last 12 months, substantially lagging behind the broader U.S. stock market. Kroger looks attractively valued based on the valuation ratios. Current multiples are mostly in line with historical averages, which means the stock is approximately fairly valued.

Seeking Alpha

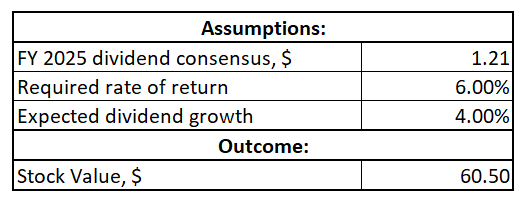

Since Kroger has a rich dividend history, the dividend discount model (DDM) looks like the best option to proceed with. I use an FY 2025 dividend consensus estimate, which projects the annual payout at $1.19. I think consensus estimates are reliable enough to incorporate into the DDM since the company has a strong history of dividend consistency. I use a 6% WACC recommended by GuruFocus, which is higher than my previous input data, but I believe it is fair given the increased uncertainty regarding the merger and the decelerated holiday spending growth. While Kroger's dividend growth rates were stellar in several previous years, I prefer to be more conservative in the current uncertain environment. Therefore, I use a rounded-down to 4% sector median forward dividend per share growth.

Author's calculations

According to my DDM analysis, the stock's fair price is $61 per share. This is a slight downgrade from the previous $64 target price, considering the decelerated holiday spending growth in 2023 and the potential uncertainties regarding the merger. Still, the stock is around 30% undervalued, even after the target price downgrade.

Risks Update

Markets are frequently driven by hot headlines in the short term. That said, potential news that the Kroger-Albertsons merger has been banned might lead to a short-term stock sell-off. But I consider such a stock price decline to be temporary because Kroger remains a high-quality business, with or without Albertsons. Moreover, a potential pullback on this news might represent good buying opportunities.

Both Kroger's and Albertson's workforce are subject to collective bargaining agreements that require regular renegotiation as they necessitate periodic renewal. This recurrent renegotiation process introduces a layer of uncertainty and might lead to increased labor costs for these businesses. Negotiations might result in higher wages, improved benefits, or other concessions to the workforce. This will ultimately adversely impact the companies' profitability and overall financial performance.

Bottom Line

To conclude, Kroger is still a "Buy". While the vast uncertainty regarding the merger might add volatility to the stock price, my valuation analysis suggests that the stock is massively undervalued. If the merger is banned, a potential stock price pullback will provide even better buying opportunities. However, I still believe that the merger is poised to be closed after a more thorough scrutiny. But even if the merger does not get the green light from regulatory bodies, I believe that Kroger standalone is still an excellent company to invest in.