payphoto

Overview

Starbucks (NASDAQ:SBUX) is one of that companies that have more global recognition than some religions since they operate all around the world. In their stores, you can get coffee, beans for brewing at home, and snacks like pastries and sandwiches. Starbucks coffee in itself has become so culturally relevant that having a cup of Starbucks in hand has sort of become part of some people's identity. The stuff is deliciously addicting and their stock price below $100/share is even more addicting.

With an excellent dividend growth history and currently trading at a discount to fair value, I plan on adding shares to SBUX here for the long haul. The dividend growth since it was initiated, has proven that SBUX is an ideal candidate for a great combo of capital appreciation and a growing stream of income. The recent earnings report further cements that SBUX is continuing to grow and increase revenues. SBUX is also trading undervalued when using a DCF (discounted cash flow) . When you combine this undervaluation with the growing dividend, of 2.3%, you are looking at double digit returns going forward.

Growing Coffee Market

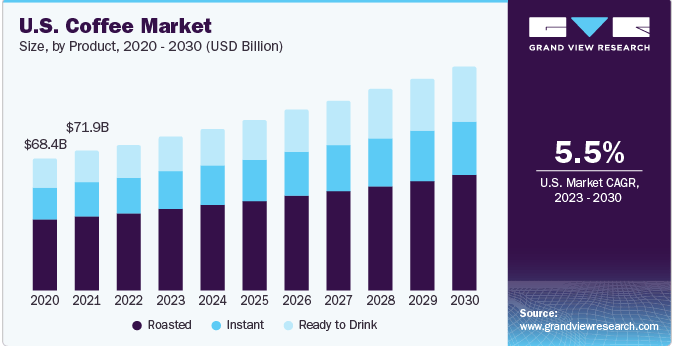

The growing coffee market will help boost SBUX's profitability over the next decade. In 2022, the global coffee market reached an estimated size of $461.25 billion, and projections indicate a compound annual growth rate of 5.2% from 2023 to 2030. This anticipated growth is primarily driven by the substantial demand for coffee on a global scale. Coffee has secured its position as one of the most widely consumed beverages worldwide, with a notable upward trend, especially in emerging markets like the Asia Pacific region.

Grandview Research

Factors contributing to this surge in demand include the increasing disposable incomes, evolving consumer lifestyles, and the strengthening culture of coffee among individuals. As consumers continue to embrace coffee as a daily indulgence, the industry is witnessing significant expansion, presenting lucrative opportunities for market participants and stakeholders alike.

Growing Business

In their latest Q4 earnings report, SBUX highlighted significant growth in various aspects of its business that makes it a strong buy at these levels. The global comparable store sales increased by 8%, with a notable 4% rise in average purchase amounts.

The North America and U.S. segments saw a remarkable 8% increase in comparable store sales, fueled by a 6% growth in average ticket and a 2% rise in comparable transactions. Meanwhile, international comparable store sales increased by 5%, driven by a 6% increase in comparable transactions, despite a 1% decline in average ticket. Specifically in China, comparable store sales grew by 5%, with an 8% increase in comparable transactions and a 3% decline in average ticket.

We can see the revenue in North America alone has grown 2.4% since the last quarter. Throughout the entire year of 2023, the revenue has grown by double digits annually. International growth has also been strong throughout the year, with the exception of Q1 2023 which saw a negative year over year change of -10.4%.

Seeking Alpha - Niloofer Shaikh

During this quarter, Starbucks expanded its reach by opening 816 net new stores, bringing its total to an impressive 38,038 stores globally. Out of these, 52% were company-operated, and 48% were licensed. The U.S. and China remained key players in Starbucks' portfolio, constituting 61% of the company's global stores. The market share that SBUX captures globally is huge, but don't that fool you! These growing metrics tell another story of under valuation.

Financially, Starbucks achieved record-breaking consolidated net revenues of $9.4 billion, reflecting an 11% increase. The company demonstrated strong operating performance, with a GAAP operating margin of 18.2%, up from 14.2% in the previous year. The GAAP earnings per share showed impressive growth, reaching $1.06, a 39% increase over the prior year.

Starbucks Investor Presentation

For what it's worth, the Quant gives SBUX an A+ rating within the profitability metrics. This isn't hard to understand when you realize that this past year's growth has been strong. SBUX's net income margin of 11.4% has grown at a CAGR of 10.54%.

Additionally, Starbucks focused on enhancing customer loyalty through its Rewards program, witnessing a 14% year-over-year increase in 90-day active members in the U.S., reaching 32.6 million members. Overall, these fiscal highlights underscore Starbucks' successful financial and operational performance during the fourth quarter of 2023.

Dividend

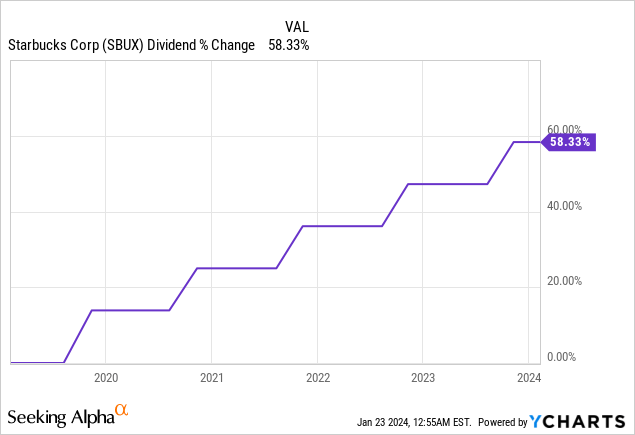

As of the latest declared quarterly dividend of $0.57/share, the starting yield is about 2.3%. The dividend has been raised for 13 consecutive years and I don't see a threat of any cuts in the future. The payout ratio sits around 60%, which is high in comparison to the sector median of 33%, but low enough that I don't anticipate any trouble sustaining the growth.

Speaking of growth, the dividend has grown nearly 60% since 2019. Over the last decade, the dividend CAGR (compound annual growth rate) has been a whopping 17.5%! With FCF (free cash flow) per share growth of 14% and a year-over-year operating cash flow growth of 36%, I have no doubt Starbucks is on the way to being a dividend aristocrat.

SBUX has also made it clear that they plan to resume buybacks in the beginning of their fiscal year 2024. Stock buybacks can be beneficial for companies and their shareholders for several reasons. When a company repurchases its own shares, it often signals confidence in the company's future performance. By reducing the number of outstanding shares, earnings per share tend to increase as well.

Portfolio Visualizer

Running a back test with Portfolio Visualizer, we can confirm this strong divided growth. An original investment of $10,000 in 2010, would have saw your value and income sky rocket. Your original investment would now be worth over. $105k with only dividends reinvested and no additional capital deployed. This would represent a CAGR of 18.4%. Your dividend income would have grown from only $157 up to an insane $2,352.

Valuation

The average Wall St. price target sits at $111/share which represents about a 20% upside from the current level. In addition, the current P/E sits at 23x compared to the 5 year average P/E of 36x. In addition, over the last five-year period, the revenue has grown by about 8%.

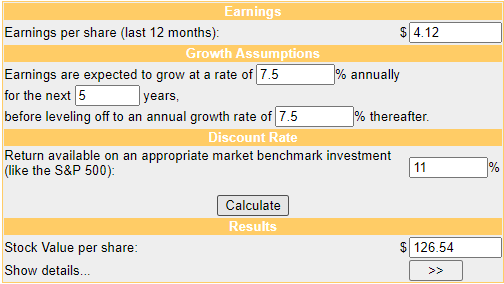

Running a quick DCF (discounted cash flow) calculation, we can determine a rough estimate for fair value. For their fiscal year 2024, the estimated EPS (earnings per share) is about 4.12x. Combining this with the average 7- 8% growth, we come to a fair value of estimate of $126.54/share. This would represent an upside potential of nearly 36%.

Money Chimp

With such a large double digit upside combined with a solid dividend growth history, this is a strong buy to ride out the price recovery. Lastly, it's expected that the Fed will lower interest rates a few times over the course of 2024. Lower interest rates benefit companies like Starbucks in several ways. Firstly, it reduces the cost of borrowing, allowing Starbucks to access funds for expansion or strategic initiatives at a lower cost. Secondly, lower interest rates stimulate consumer spending, potentially boosting sales for Starbucks.

Risk

Starbucks' significant focus on the growth of its business in China is something that I see as a negative. It seems that Starbucks does not have the same kind of cultural significance or brand value in China as it does in the US. Economic and geopolitical uncertainties, such as tensions between the U.S. and China, regulatory changes, or shifts in consumer preferences, could impact Starbucks.

In addition, if rate cuts are delayed this year, the price of SBUX may stay flat for the near future. Interest rate cuts typically stimulate economic activity and consumer spending. However, if the expected rate cuts do not occur, it could lead to higher borrowing costs for both the company and consumers. This, in turn, might impact consumer spending patterns and the overall economic environment, potentially affecting Starbucks' sales. This would mirror what we saw during the height of the pandemic when stores were closed and money was being allocated towards more necessities. Moreover, without the anticipated interest rate relief, investors might seek higher returns in alternative investments, diverting attention away from stocks like SBUX. This would be where the higher yielding dividend stocks or funds would come in.

Takeaway

In conclusion, Starbucks (SBUX) has proven that management has made smart moves to continue expanding business. The increase in global comparable store sales, expansion of stores globally, growing dividend, and strong financial performance reinforces Starbucks' resilience and ability to adapt to evolving consumer needs. The robust dividend growth history, coupled with the potential for stock buybacks, positions SBUX as an attractive choice for investors seeking a combination of capital appreciation and a growing income stream.

Despite the positive outlook, potential risks should not be overlooked, such as the heavy reliance on the Chinese market and the impact of delayed interest rate cuts on the stock price. Investors should carefully consider these factors alongside the impressive growth potential and favorable valuation, recognizing the dynamic landscape in which Starbucks operates. Overall, SBUX presents an opportunity for long-term investors seeking a blend of stability, growth, and dividend income.