tupungato/iStock Editorial via Getty Images

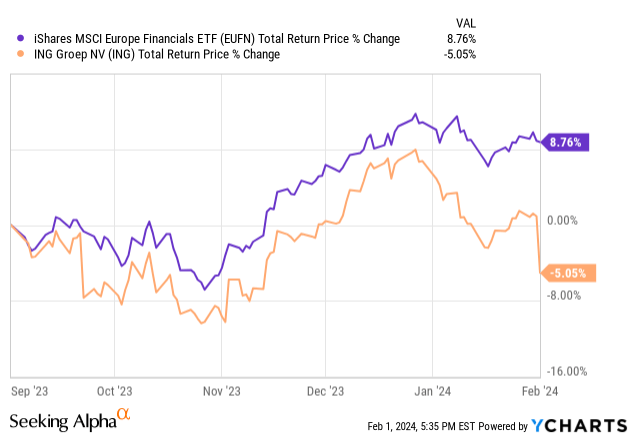

ING (NYSE:ING) continues to frustrate. Shares of the Dutch lender are down around 6% since prior coverage, materially underperforming broader European financials following poor Q4 2023 results and guidance.

Results were clearly disappointing, with a bottom line beat driven by provisioning never going to offset both a disappointing miss on net interest income ("NII") and similarly weak 2024 guidance.

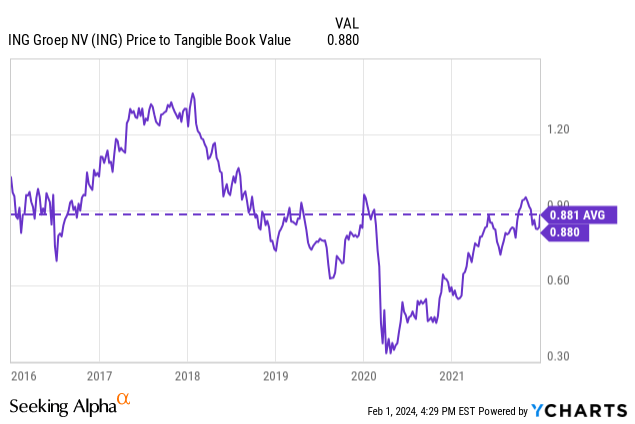

At approximately 0.8x tangible book value ("TBV"), ING stock remains cheap, but catalysts for a re-rate are admittedly thin at this point. The one bright spot remains the bank's significant capital returns potential. While there may have been some disappointment here too, with management only promising an update later in the year, the prospect of a step-up in buybacks and dividends is attractive given the stock's current valuation.

NII Lands Short Of Expectations

Though fourth quarter net income of €1.56 billion was technically a slight beat, the nature of the beat is what counts, and provisioning-driven ones aren't going to win the bank any credit now. That is especially true given the top line miss, with Q4 NII of €3.88 billion down around 4% QoQ and landing around 3% below consensus. Fee income was likewise lackluster, declining 1% year-on-year and missing consensus by around 5%. At least one analyst was fairly scathing about management's transparency on the earnings call, suggesting that a lack of communication was a major driver of the stock price decline, not that this is much of an excuse.

Bright spots were few and far between, though lending margins were stable QoQ and YoY at 130bps. Lending growth was also a modest positive, with core loan growth coming in above 1% QoQ. Credit quality remains stable, with Stage 3 loans flat QoQ at 1.5% of the total.

Source: ING Group 2023 Results Presentation

2024 guidance has NII at circa €15.25 billion at the mid-point, implying a decline of around 5% year-on-year and well below prior consensus of around 1% growth. Driving that is a contraction in the liability margin down to 100bps by year-end, which is a function of deposit dynamics (volumes, beta and so on) and the bank's €480 billion replicating portfolio. The replicating portfolio can conceptually be thought of as a portfolio of fixed-income securities, around half of which matures within 12 months. Baked into NII guidance is around 150-200bps in ECB rate cuts this year, a bit more aggressive than implied by the current forward curve.

Now, the bull case for ING was not that income and earnings hadn't peaked. That has been on the cards for a while now, albeit Q4 NII and guidance were both weaker than anticipated. It was more that the stock's valuation didn't reflect any kind of structural step-up in profitability when compared to the zero/negative interest rate era pre-2022. Indeed, relative to TBV ING trades even cheaper than it did when Eurozone interest rates were on the floor.

Given levers on deposit pricing, management thinks it can maintain the liability margin at around 100bps going forward. That equates to around €6.25 billion as things stand, which would leave it well above the levels seen in the 2019-2022 period before considering further deposit growth and so on.

Source: ING Group 2023 Results Presentation

Looking at other aspects of guidance, 5-10% fee income growth would imply around €22 billion in total 2024 income, a decline of around 3% versus 2023, though this looks aggressive to me given the Q4 miss. Operating costs are seen up 3%, while ROE has been guided at 12%. Altering the latter figure to reflect my preferred use of tangible equity implies a ROTE around 20bps higher. Although not explicitly guided by management, cost of risk would appear to land at around 20bps if my math is right, a shade under across-the-cycle guidance of 25bps. Said differently, ING is still plenty profitable in a modestly positive interest rate environment and assuming cycle-average provisioning expenses.

Capital Returns Potential Remains Compelling

Higher profitability in a favorable macro environment is, of course, something that could have been said about most European banks to varying degrees recently. A more ING-specific plus-point was the bank's above-average capital returns potential, with management previously guiding for a 100%-plus payout ratio given the surplus capital position. With that, a final dividend of €0.756 per share (~$0.82 per ADS) will bring total distributions announced in 2023 to €7.8 billion, including €4 billion in share buybacks, making for a total payout ratio of just over 100% of net income.

Management continues to target a 12.5% CET1 by 2025. Interestingly, the bank's capital ratio actually strengthened over the year, increasing around 20bps to 14.7% and opening up questions around the current rate of shareholder distributions. Management disappointingly dodged those questions on the earnings call, promising instead to provide further clarity post-Q1 results. Given the stock's current discount to TBV, more color with respect to share repurchase plans wouldn't have gone amiss.

Source: ING Group 2023 Results Presentation

The above notwithstanding, the math is certainly eye-opening looking forward. The bank is now sitting on around €7 billion in surplus capital, which is of course topped-up by over €6 billion in 2024-2025 annual earnings power. This is relative to a current market-cap of €43 billion, implying a significant double-digit annual shareholder yield (i.e. dividend yield plus net buyback yield) if management is to meet its 2025 goal.

Buy Rating Maintained

ING's ADSs change hands for $13.37 at time of this writing, putting them at just over 0.8x TBV per share and on a P/E of ~6.7x forward earnings. The valuation continues to puzzle me, with the market applying an even lower TBV multiple than when interest rates were at rock bottom levels before 2022.

Granted, recent results and 2024 guidance definitely underwhelmed, but the bank is still on track to deliver a comfortable double-digit ROTE. That is around 4ppt above the figure it averaged between 2016 and 2022: so long as interest rates remain modestly positive in the Eurozone, ING will remain structurally more profitable versus its recent past. With that, anything below TBV per share looks cheap to me, with around 1.2x TBV, or roughly $19.50 per ADS, looking fair given the bank's ROTE profile.

Against the backdrop of weak Q4 income and guidance, catalysts for a re-rate are admittedly sparse, though a prospective double-digit shareholder yield through 2025 looks like good compensation. As such, I maintain my Buy rating here.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.