Nataliia Gorsha/iStock via Getty Images

Powersport vehicle company, Polaris (NYSE:PII), was recently upgraded by analysts at Morgan Stanley (MS) with an "overweight" rating due to its attractive risk-reward profile. The upgrade came just prior to the company’s Q4 earnings release. While I believe PII can rise to Morgan Stanley’s $113/share price target over time, it may take much longer than desired for most investors.

In my prior coverage on PII, I noted that elevated manufacturing costs, a more cautious consumer, and rising promotional activity would be key factors that ultimately would lead to lower-than-anticipated results. I believe my viewpoint came to fruition.

While PII reported better than expected revenues in Q4, earnings missed by $0.62/share due in part to weaker margins, higher promotional activity, and elevated warranty costs. The company also put forward underwhelming full year guidance for fiscal 2024.

Though PII’s strong cash flow profile and current trading valuation are high marks for attracting inventor attention, I believe a more pronounced turnaround in the discretionary consumer environment needs to be a prerequisite before any new or further positioning in the stock.

Recap Of PII Q4 Results

In the final quarter of the fiscal year, PII turned in results that came in below expectations and provided underwhelming guidance for fiscal 2024.

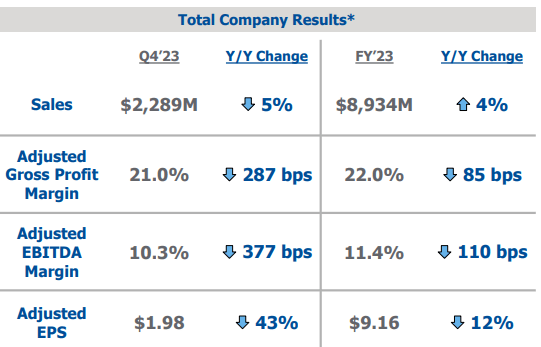

On an overall basis, the company reported a 5% YOY decrease in sales and 43% lower earnings. Driving the topline weakness was a combination of reduced shipments and lower retail trends, including elevated promotions and continued weakness in PII’s recreational unit.

PII Q4 Investor Presentation - Summary Of Total Quarterly And Full-Year Results

PII’s setbacks on shipments are twofold. First, PII’s dealers are still operating on higher overall inventory levels; in Q4, dealer inventory was up 56% in relation to 2023. This created friction with dealer sentiment. It is also creating challenges regarding new shipments. PII was also negatively impacted by factors outside of their control during Q4, namely by a muted snow season, which withhold sales growth of PII’s lineup of snowmobiles.

Higher promotional activity to move existing inventory, as well as rising expense, led to a 377 basis point YOY decrease in adjusted EBITDA margins. Gross margins didn’t fare much better with reported declines of 287 basis points. Moreover, margins were down in all three segments, with the Off-Road and Marine segments down 350 or more basis points. The On-Road segment, on the other hand, reported a margin decline of 323bps.

PII is expecting existing headwinds to carry into the first quarter of fiscal 2024. This includes the elevated promotional activity, as well as continued softness in recreational retail in their Off-Road segment. Unfavorable snow conditions is also expected to remain a drag for snowmobile sales.

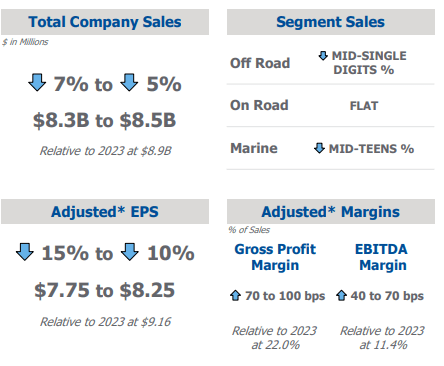

Overall, PII guided for a 6% decline in total annual sales at the midpoint, with marine expected to be down double-digits on the year. While the margin outlook is expected to improve relative to 2023, PII still expects adjusted EPS to land several notches below the $9.16/share reported in 2023. At the midpoint of $8/share, earnings would be down double-digits YOY.

PII Q4 Investor Presentation - Summary Of FY24 Guidance

Two Notable Takeaways From PII Q4 Results

Higher Product Liability Costs: One controllable factor that weighed on PII in 2024 was product liability and warranty spend. Both were above expectations during the year and were notable reasons why EBITDA margins were down nearly 380 basis points YOY. More specifically, during the quarter, PII incurred a +$23M warranty charge in their On-Road segment. The charge pertained to a failed battery supplied by a now-defunct vendor. The resulting charge and expectations for a more litigious environment moving forward led PII to increase their accrual rate for productivity liability claims, impacting both the current and future margin outlook.

Negative Dealer Sentiment: Higher interest rates and a cautious consumer with respect to the discretionary outlook is clearly weighing on dealer sentiment. The dealer concern is compounded by their current inventory position, which is more than 50% above 2022’s benchmark. The higher levels of inventory are consequently creating a more promotional environment. While it is helping sales, most dealers believe that system inventory is too high, according to PII’s biannual survey 700 dealers. In my view, PII’s outlook is very much dependent on dealer sentiment. If the dealer’s aren’t doing well, it’s unlikely PII will either.

Is PII Stock A Buy, Sell, Or Hold?

In concluding remarks in my last coverage on PII following the release of its Q3 earnings, I noted that PII would be negatively impacted by continued promotional activity. And I also noted that the company faced dimmer margin prospects and was more likely to hit the lower end of their EPS target. In as little words, PII’s Q4 results were a realization of my viewpoint.

At the end of Q3, PII was trading about 4% lower than today. Nevertheless, the average Wall Street price target on PII stands at just above $100/share, implying double-digit percentage upside potential.

It’s possible the stock can rise higher on broader bullish sentiment. After-all, PII does trade at about 11x forward earnings, a value compared to the 22x average investors would pay for a stock trading on the S&P 500 index.

In considering PII’s value proposition, it’s worth considering the company’s cash flow position. In 2023, PII reported +$507M in free cash flow, up 154% from fiscal 2022. In addition, PII remains a dividend aristocrat, with 28 consecutive years of raising its dividend. Moreover, PII continues to aggressively repurchase shares. In 2023, PII repurchased 1.6M shares and had 1.2B remaining on their authorization.

In my view, their strong positioning from a cash perspective is enough to warrant a reconsideration in the company’s trading multiple; perhaps a $100/share target, then, as estimated by Wall Street is appropriate.

But one must also consider PII’s current challenges in the face of a weaker operating environment. On the recreational side of their Off-Road business, for example, PII has reported five consecutive quarters of negative retail. This is notable since it represents 40% of the segment’s total revenues.

And looking ahead, it’s unlikely there will be a swift reversal, given the current economic mood of the consumer. Additionally, PII was negatively impacted by factors outside their control. Here, a muted snow season negatively impacted their snowmobile sales in Q4.

In my view, a bullish turn on PII would be supported by a reversal in the economic sentiment and mood of PII’s customer base. At this point in time, most consumers are more focused on gearing their dollars to necessities and to travel-related luxuries. While PII has had a history of nimbly navigating through past down-cycles, that hasn’t necessarily been the case today. I, therefore, find it best to remain on hold on PII.