Pioneertown, CA CircleEyes/iStock Editorial via Getty Images

Introduction

Occasionally I find securities that are new and have yet to be covered on Seeking Alpha that I think other income investors might be interested in. Upon Banc of California's (BANC) merger and absorption of Pacific Western Bank, the PacWest issued preferred started trading as the Banc of California, Inc. DEPOSITARY SHARE (NYSE:BANC.PR.F).

We'll reviewed the post-merger company, as much as possible, and the renamed preferred stock. My comfort level is strong enough, with the yield and potential YTC, to rate the BANC-F as a Buy.

Banc of California review

Seeking Alpha describes this bank as:

Banc of California, Inc. operates as the bank holding company for Banc of California that provides various banking products and services to small and medium-size businesses in California. It offers personal banking products and services, including checking account, debit Mastercard, certificates of deposit, and savings and money market accounts, as well as online and mobile banking services; personal credit cards; and specialty banking services. The company also provides commercial and business banking products and services. The bank started in 1941. (Source)

Last summer, the Banc of California executed a merger.

Banc of California, Inc. (NYSE: BANC) completes a transformational merger with PacWest Bancorp (Nasdaq: PACW) to emerge as the third-largest bank headquartered in California and one of the nation's premier relationship-focused business banks. The combined bank will operate under the Banc of California name and brand. Banc of California also completed a $400 million equity raise from affiliates of funds managed by Warburg Pincus LLC and certain investment vehicles sponsored, managed or advised by Centerbridge Partners, L.P. and its affiliates. (Source)

While the new BANC may be the 3rd largest bank headquartered in California, it ranks about 8th in branches, with a fraction of Chase (910) or Wells Fargo (838). BANC considers itself a commercial bank, which isn't too important, but it changes the risk profile, as SVB found out in drastic fashion last winter.

In the BANC announcement, they listed several other actions that were part of the merger and assumed "de risking" of the bank's portfolio:

In connection with the merger, Banc of California, N.A. and Pacific Western Bank have sold approximately $1.9 billion in assets as part of the previously disclosed balance sheet repositioning strategy, which strategy includes additional asset sales expected to be completed through the end of the first quarter of 2024. As of the merger closing date, Pacific Western Bank has sold approximately $1.5 billion of its securities portfolio. In addition, the previously announced forward sale of Banc of California's $1.8 billion single-family residential mortgage portfolio. The proceeds are expected to be utilized primarily for the repayment of the combined bank's wholesale borrowings and higher cost funding. (Source)

Other Seeking Alpha contributors covered the merger in great detail and have more expertise than me in that in-depth analysis. Reading those or the SEC Form 8-K is recommended. As it relates to the preferred stock reviewed here, BANC's total stockholders equity is 6.7X in size compared to BANC-F as of the end of 2023. With the merger and equity infusion from well-informed investment houses, but with the caveat that things happen fast (think SVB), I do not currently see preferred investors at risk of not receiving a payment or, even worse, being paid off later. My comfort level is strong enough, with the yield and potential YTC, to rate BANC-F as a Buy.

BANC PFD review

nyse.com/quote/XNYS:BANCpF

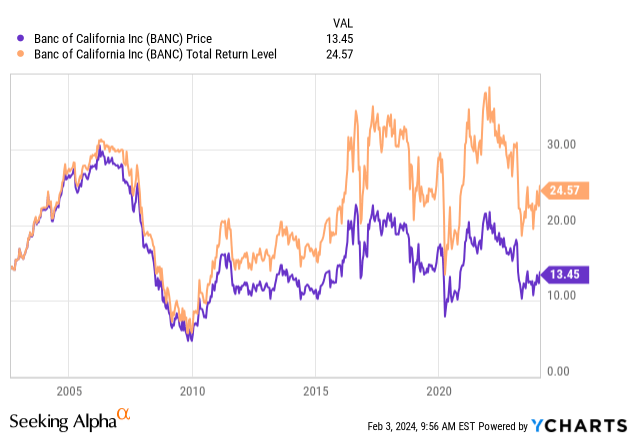

As were almost all, if not all, bank preferreds, this preferred was hit hard when SVB failed last winter. Again, as with most fixed income oriented assets, the price has followed FOMC rate expectations since the fall of 2023.

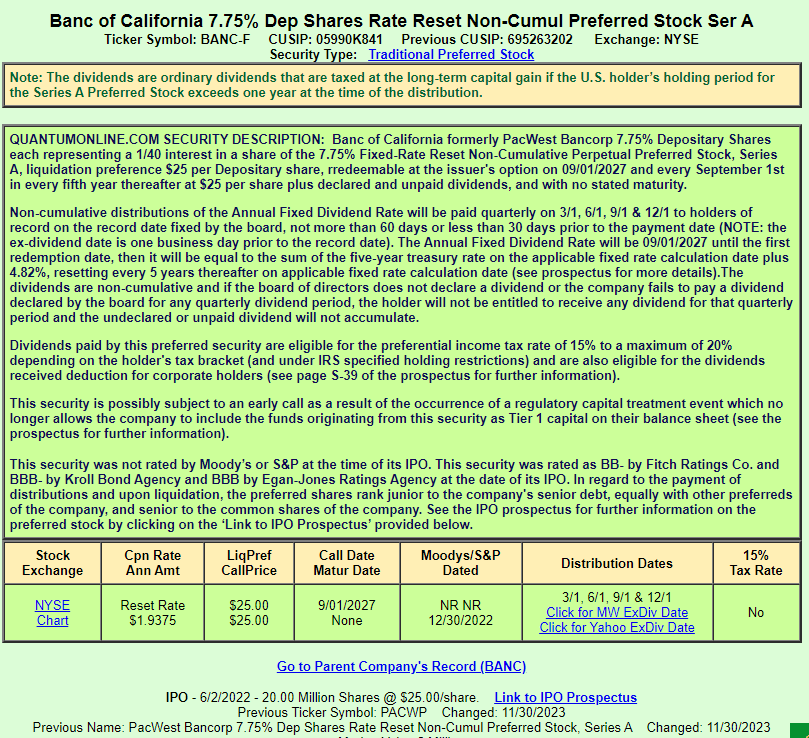

quantumonline.com BANC-F

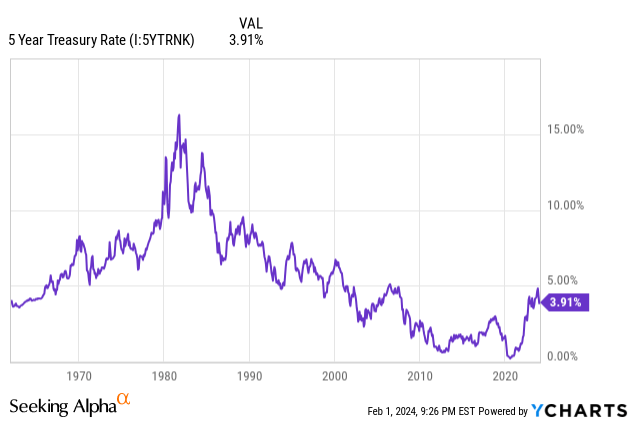

While the Call date is listed a 9/1/27, BANC has the right to call the preferred early if the Tier 1 capital rules change and BANC-F no longer qualifies, though that action must be approved by the Federal Reserve. Since it is part of Tier 1, the issue must be non-cumulative. On its Call date, BANC-F converts from a fixed-rate to a floating-rate based on the 5-Yr UST rate + 4.82%, then resets every five years. The next chart shows how that rate has moved. It would take a rate just under 3% for the floating coupon to closely match the fixed coupon.

Conclusion

One thing I look for when considering adding a preferred shares to my portfolio is the companies' issuance and redemption history for these and its Notes. Between 2018 and 2022, BANC Called three preferreds and one Note matured: coupons were between 7% to 8%. First, I rated BANC-F as safe; next I looked to see if the yield makes for a good investment by comparing it to other bank preferreds and a non-bank that all use the 5-yr UST as its floating component. These are:

- Huntington Bancshares Incorporated 6.875% DEP PFD J (HBANL)

- KeyCorp 6.2% DP SH PFD H (KEY.PR.L)

- Rithm Capital Corp. 7% RT REST PFD D (RITM.PR.D)

I have recently reviewed each of these issuers, article links provided at the end of this article.

| Factor | BANC-F | HBANL | KEY L | RITM D |

| Coupon | 7.75% | 6.875% | 6.20% | 7.00% |

| Call date | 9/1/2027 | 4/15/2028 | 12/15/2027 | 11/15/26 |

| Price | $22.74 | $24.22 | $22.53 | $22.74 |

| Yield | 8.52% | 7.10% | 6.88% | 7.70% |

| YTC | 10.83% | 7.75% | 9.27% | 10.81% |

| Floating rate | 5Y UST + 4.82% | 5Y UST + 2.704% | 5Y UST+3.132% | 5Y UST + 6.223% |

Based on this limited analysis, BANC-F shows the following:

- The highest yield, indicating the market sees it as risker than the others.

- The highest YTC, especially compared to the other two banks.

- Amongst the banks, it will have the highest floating rate. While that also starts first, the same feature increases the odds it will be Called.

My comfort level is strong enough that with the yield and potential YTC to rate the BANC-F as a Buy. I would go with the HBANL if one's main objective is locking in a yield for the longest time and least likely to then be Called.

Portfolio strategy

After the January FOMC meeting, the futures market shifted to neutral for a March cut in the FFR, but jumped to a 90% probability for one in May. The ebb and flow of investor expectations on when cuts will start, maybe more so than their depth, played a large part on how these assets have priced since the summer as that sets the yield assuming the fund's payouts hold steady. Of course, if the fund holds a high percent in floating-rate assets or is highly leveraged, both of those factors then come into play, with each slightly offsetting the other.

Final thoughts

While this article was the first to focus on the renamed BANC preferred, there are six Seeking Alpha articles, each by a different contributor, discussing the merger's impact on BANC, thus its ability to service this preferred. Potential investors should consider those opinions as their banking industry knowledge most likely exceeds mine. That is a benefit of using a site like Seeking Alpha; take advantage.

Article links

If readers think one of the comparison preferreds looks attractive, start your own due diligence with these articles:

Alex Pettee is President and Director of Research and ETFs at Hoya Capital. Hoya manages institutional and individual portfolios of publicly traded real estate securities. Alex leads the investing group known as the Hoya Capital Income Builder, which uses the investment knowledge of several Seeking Alpha analysts provide members with insightful articles covering mostly individual stocks or funds. Occasionally an article cover will cover an investing strategy or other topic that investors need to be aware of, such as law changes that might effect their long-term strategy.

For more information about this Investors Group, click on this link: