KSChong/E+ via Getty Images

Investment Thesis

The airline sector of stocks has not had the leisure of enjoying a formidable start to the year. The markets moved ~4% higher on average year-to-date, with technology stocks again leading the way as they did last year. But as can be seen in the chart below, the basket of airline stocks represented by the U.S. Global Jets ETF (NYSEARCA:JETS) underperformed the markets.

sa

I believe some of that bearish sentiment may have been spurred by reports by many investment banks, such as this one by Bank of America, indicating that consumer discretionary stocks may underperform in 2024. To complicate matters, quality control issues in some Boeing 737 Max 9 planes cast a darker cloud on the airline industry. My analysis shows that the profitability outlook for JETS is either priced in at the moment and/or uncertainty is weighing down on JETS. At the moment, I rate this ETF as a hold until I get a clearer picture.

About JETS fund

JETS is an ETF whose assets are managed by U.S. Global Investors. Through the fund, the firm seeks to offer exposure to companies involved in the air travel industry, including airline operators, airports and terminal services, and other miscellaneous manufacturers related to the industry. According to the fund's prospectus, assets are invested in companies related to the airline industry with global exposure.

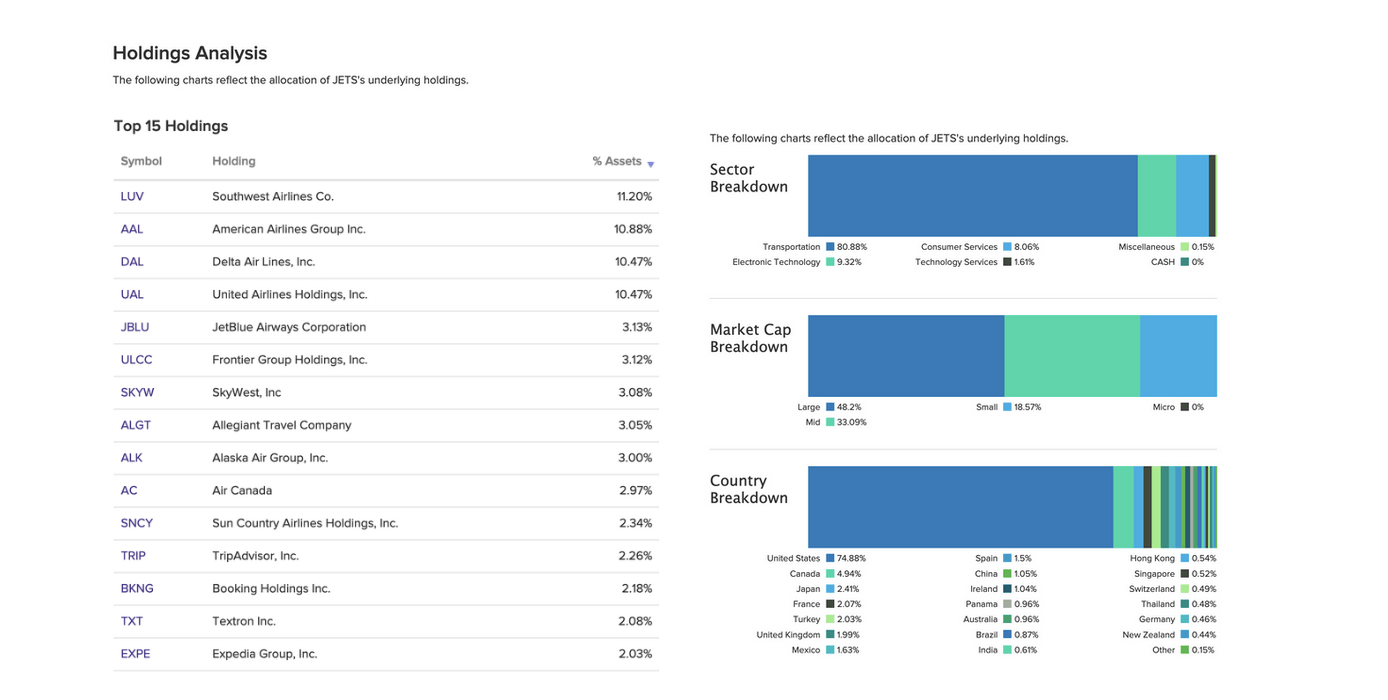

JETS achieves its fund objective by tracking the U.S. Global Jets Index, which is reconstituted on a quarterly basis. I have attached a summary of the fund's holdings below.

etfdb

Peer comparison

In order to round out the insight derived from conducting a peer-to-peer analysis of JETS, I looked at a few other ETFs that either tend to directly compete with JETS in terms of assets or are related to the broader tourism industry. JETS is positioned as a pure-play airline-focused ETF, but I think it would also be prudent to look at other ETFs in the larger tourism space rather than only focus on JETS. There are some inherent risks with JETS, which I will discuss in a later section. For now, I will observe the ETFs below and compare them to JETS.

sa

What immediately stands out to me is the expense fee of 0.6% for investors. This is quite high, especially given that JETS is the largest ETF in the consumer discretionary tourism space and is also one of the oldest of the lot. While the ETFMG Travel Tech ETF (AWAY) and the Defiance Hotel, Airline, and Cruise ETF (CRUZ) are more diversified by investing in a combination of airlines, hotels, and travel technology, the SPDR S&P Transportation ETF (XTN) invests in assets that also diversify towards areas such as logistics and commercial transportation.

In terms of past performance, it is easier for me to observe how the pure-play airline value proposition for JETS does not necessarily stand out. Yes, AWAY and CRUZ are new-age ETFs, but since these ETFs have endured the harsh realities of the 2022 bear market, it still gives me plenty of room to compare all ETFs over a 3-year period. I observe how JETS does not necessarily stand out in performance versus other ETFs. Even in shorter time frames, such as the 1- or 3-month periods, it is only able to etch a smaller lead in terms of performance when compared to the smaller CRUZ, which also offers a relatively better dividend yield.

Macroview for airlines industry & JETS is mixed

The International Air Transport Association (IATA), the trade association for the world's airlines, representing some 300 member organizations, published its FY24 outlook last month. IATA sees the airline industry's profits as a whole to increase by 10.3% on a y/y basis in FY24, driven by slightly better passenger yields and a record number of passengers expected to fly this year. 4.7 billion people are expected to travel globally by airline this year. This will be ~8% higher than expected global passenger volumes in FY23 and, for the first time, will beat global passenger volumes in 2019 by ~4.4%. But the trade association also says that profitability will "largely stabilize in 2024" after capping off a strong 2023.

Further, I also observed that in the U.S., passenger volumes of checks at TSA checkpoints were already up 8% on a ytd basis, this year. Passenger volumes at TSA checkpoints suddenly dropped around Thanksgiving last year but have since stabilized, as seen in the weekly 2024 passenger volumes below.

tsa.gov

This looks like a good start to the flow of passenger volumes in the U.S., which is mostly in line with what the IATA is seeing. In recent earnings calls, airlines reported seeing strong demand continue into this year. American Airlines' (AAL) outlook for FY24 remained upbeat. United Airlines (UAL) also reported a strong close to FY23, although its FY24 projections were at the market's estimates. However, Delta Air Lines cut its FY24 outlook (DAL), citing higher input costs and lower airfares. To me, these are very important factors because higher input costs such as fuel and labor costs, together with lower airfares, will apply pressure on the airline companies that are part of JETS's fund composition.

Assuming the 10.3% y/y profits that I noted earlier, these profit margins are still lower than the 10.9% expected in the S&P 500 this year. The S&P 500 is already trading at a forward PE of 20, which is higher than the 5-year average of 18.9 and above the 10-year average of 17.6. With the airline companies expected to lag the S&P 500 in terms of profits, I do not see any room for upside in this case. Moreover, there would need to be significant upward revisions in airfare, currently down -9.4% y/y and downward trends in hourly wages, currently up +4.5% y/y and fuel, currently down -1.6% (CL1:COM), for me to upgrade my outlook about this ETF. Moreover, there are some risks too, which I will cover in the next section. Given all these developments, I am currently issuing a HOLD on JETS.

Risks & other factors to consider

The biggest risk to investing in JETS is exposure to airline stocks. Per the prospectus I shared earlier, ~74% of the fund assets are invested in airline companies. Most airline companies always have to manage their input costs while delicately using airfares to manage consumer demand. If either of the two sides of the equation is imbalanced, it could lead to major headwinds for the profit outlook for airline companies. I believe these factors are very important for JETS because most airline companies carry significant debt on their balance sheets due to the high capital costs incurred from the purchase or lease of airplanes. If input costs, such as fuel or wages, trend higher, it could be detrimental to their profit outlook. Most recently, I observed how quality issues with the 737 Max 9 airplanes by Boeing have caused Alaska Airlines and United Airlines to downgrade their profitability outlook. The profitability gets impacted due to higher input costs from unexpected areas such as lower capacity, higher cancellation costs, etc. United Airlines management mentioned on the recent earnings call that "it is going to impact United in the near term because of some of the challenges they've had" when asked about Boeing's Max 9 airplane quality issues.

Moreover, geopolitical tensions also affect companies in the JETS ETF. Since the pandemic, there has been an increase in geopolitical tensions around the world, with Russia/Ukraine and Israel/Gaza tensions taking center stage. Both of these conflicts have created uncertainty among travelers but have also pushed up fuel costs, which make it difficult for airline companies to operate efficiently since they drive up their input fuel costs.

Finally, consumer demand is expected to remain strong this year as well. But with the IATA already projecting a record 4.7 billion passenger volumes in FY24 as well, I believe most of that growth is already priced into the growth outlook for airline companies. Moving further, any significant upgrade or downgrade in the outlook for airline companies will provide headwinds and tailwinds, respectively.

Takeaways

After reviewing the JETS ETF, I believe the conditions for airlines and other companies as represented by the JETS ETF are priced in for now. There are risks that still persist, and the Boeing Max 9 issues that I talked about earlier have created another quality-control headache for many airlines that are part of the JETS ETF. However, if the macro outlook for the consumer continues to get better, it may provide the necessary boost for the JETS ETF. With uncertainty still persisting and the outlook for the year priced in, I rate this ETF as a HOLD.