A shot of high-voltage power lines at sunset. Anton Petrus/Moment via Getty Images

Dividend growth investing doesn't have to be complicated. Better yet, it should be as simple as possible. When I'm screening companies to add to my dividend growth portfolio, I look at several elements.

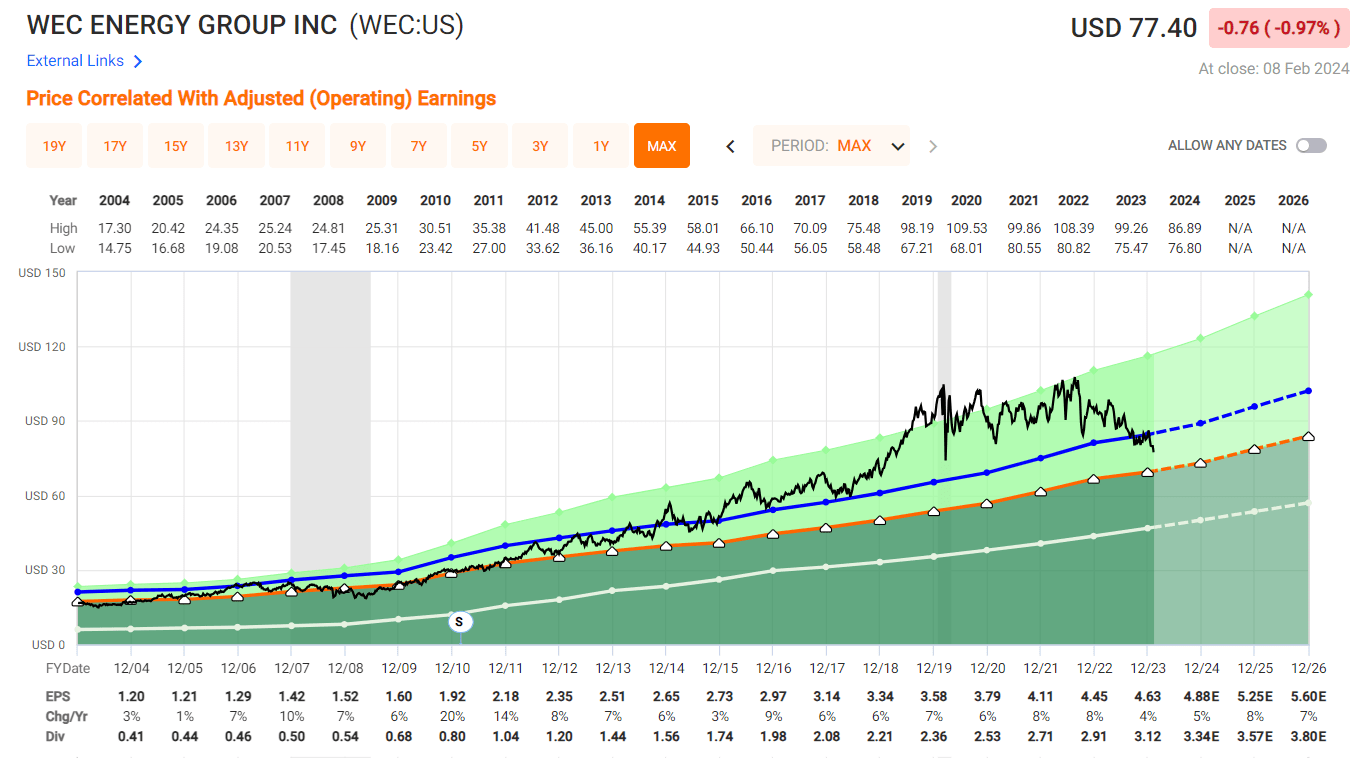

A place that I like to start is to examine the last 20 years of earnings via FAST Graphs. Although it is rare to find, I have a preference that a prospective investment be as close to growing its earnings in all 20 out of the last 20 years as possible. I also appreciate when the forward analyst consensus is forecasting continued earnings growth.

My line of thinking is that if a company can steadily grow its earnings, dividend growth tends to follow. That's often more true if said business has also demonstrated a commitment to shareholders through decades of upping its payout.

Corporate credit ratings are another important filter that I use to discern whether I should buy a company for my portfolio. I tend to target A-rated companies, so most of my holdings possess investment-grade (BBB- and up) credit ratings. This is because such an approach can at least somewhat mitigate the risk of an investment going to nothing (e.g., bankrupt).

One of the holdings within my portfolio that checks off all these boxes is the electric and gas utility, WEC Energy Group (NYSE:WEC). For the first time since December, I will revisit the company's fundamentals and valuation to discuss why I am maintaining my buy rating.

Dividend Kings Zen Research Terminal

WEC Energy Group's 4.3% dividend yield is a bit above the 4.2% yield of 10-year U.S. Treasury notes. But unlike T-notes, the utility has the potential to keep growing its income over time.

WEC Energy Group's 68% EPS payout ratio clocks in below the 75% EPS payout ratio that rating agencies prefer from utilities. The company's 54% debt-to-capital ratio is also favorable compared to the 60% or less debt-to-capital ratio that rating agencies view as sustainable. Thus, S&P rates WEC Energy Group's long-term debt an A- on a stable outlook. That puts the risk of the company going bankrupt through the next 30 years at 2.5%.

Dividend Kings Zen Research Terminal

Trading 28% off its all-time high of around $108 a share set in May 2022, the interest rate hike cycle has taken a toll on shares of WEC Energy Group. This has arguably created a long-term buying opportunity, though. Based on the 10-year and 25-year P/E ratio and dividend yield, the utility is worth $108 a share. Against the $77 share price (as of February 9, 2024), shares are 28% discounted to fair value.

As interest rates eventually make their way back down, I believe shares of WEC Energy Group will rally. If the company can return to its mean valuation as I would argue is supported by fundamentals and meet the growth consensus, here are the total returns that it could produce over the coming decade:

- 4.3% yield + 6.4% FactSet Research annual growth consensus + a 3.3% annual valuation multiple expansion = 14% annual total return potential or a 271% 10-year cumulative total return versus the 10% annual total return potential of the S&P 500 (SP500) or a 159% 10-year cumulative total return

Still A Great Utility

WEC Energy Group Q4 2023 Earnings Press Release

WEC Energy Group's operating revenue fell by 13.3% year-over-year to $2.2 billion during the fourth quarter that ended Dec. 31, 2023. This was $510 million shy of the analyst consensus per Seeking Alpha.

Initially, these results seem discouraging. However, it is important to note that this topline decline was driven by a factor beyond WEC Energy Group's control. The factor to which I am referring is commodity prices, such as natural gas. Since the company is a regulated utility and its costs were lower as a result of cheaper commodity prices, operating revenue allowed by regulators to be collected was accordingly lower.

The good news for WEC Energy Group is that this helped the company's bottom line. Adjusting for a $0.41 charge related to prior capital investments that were disallowed by the Illinois Commerce Commission, WEC Energy Group generated $1.10 in non-GAAP diluted EPS for the fourth quarter. That was up 37.5% over the year-ago period and $0.02 above what the analyst consensus was according to Seeking Alpha.

Operating expenses were much less than they were in the prior year's fourth quarter. That caused WEC Energy Group's non-GAAP net profit margin to soar by nearly 590 basis points to 15.7% in the fourth quarter. This is how non-GAAP diluted EPS surged as operating revenue dipped during the quarter.

WEC Energy Group Q4 2023 Earnings Package

WEC Energy Group upped its five-year capital spending plan from $23.4 billion in November to $23.7 billion. The company will be spending $800 million less on Illinois gas delivery. That is because of the regulatory order received in November per CEO Scott Lauber's opening remarks during the Q4 2023 earnings call. This will be offset by $800 million in additional energy infrastructure spending. Also, the company is allocating an additional $200 million to regulated renewables spending and another $100 million to electric delivery.

This ambitious capital spending outlook should translate into high-single-digit annual rate base growth. That is why WEC Energy expects to generate 6.5% to 7% annual EPS growth in the years ahead.

Just as I discussed in my previous article, $16.5 billion to $17.5 billion of this spending will be funded by the company's cash flow from operations. An extra $150 million in funding will come from incremental debt issuances ($7.15 billion to $8.15 billion) than the prior five-year capital spending plan, with WEC Energy Group's A- credit rating. The remaining $150 million in additional funding will be from common equity issuances ($1.95 billion to $2.35 billion) (unless otherwise mentioned or hyperlinked, all details in this subhead were from WEC Energy Group's Q4 2023 Earnings Press Release and WEC Energy Group's Q4 2023 Earnings Package).

WEC Energy Group Could Achieve A Milestone In 2028

After its most recent 7.1% raise, WEC Energy Group has grown its dividend for 21 consecutive years. This puts it on track to become a Dividend Aristocrat in 2028.

According to Seeking Alpha, the analyst consensus for WEC Energy Group's 2024 non-GAAP diluted EPS is $4.88. Compared to the $3.34 in dividends per share that will likely be paid in 2024, that is a 68.4% payout ratio. This remains within the company's targeted payout ratio range of 65% to 70% of earnings that I noted in December.

Risks To Consider

WEC Energy Group is a well-run utility with a culture of rewarding shareholders, but it isn't without risks.

The recent regulatory outcome in Illinois is a reminder that there are drawbacks to being a regulated utility. Yes, a regulated utility's revenue is more predictable than an unregulated utility. However, its projects are still subject to approval from regulatory authorities. If enough projects are disallowed by regulators, WEC Energy Group's growth prospects could be hurt.

Another risk to the company is the potential for its electric and natural gas infrastructure to explode or cause a fire. Aside from the disruptions to operations that this would cause, it could also result in property damage and possible casualties. If that happened, WEC Energy Group could be fined by regulators and liable for damage beyond what its commercial insurance will cover.

Summary: An Attractive Income And Value Play

FAST Graphs, FactSet

WEC Energy Group is the kind of dividend growth stock that I am pleased to own in my portfolio. In each of the past 20 years, its earnings have grown. That has led to 21 consecutive years of solid dividend growth. Also, the A- credit rating from S&P affords the company a low cost of capital to fund its projects. Lastly, the stock could be an interesting reversion to the mean pick for when interest rates do begin to be cut. This is why I am standing by my buy rating right now.