Daniel Balakov

CVR Partners (NYSE:UAN) has unperformed since I upgraded the stock in September, when I said it looked like nitrogen fertilizer prices had bottomed. The stock is down over -10% since then. More recently, in December, I projected the company could pay out between a $1.25-$2.30 distribution in Q1. Let’s catch up with the name following its Q4 earnings.

Company Profile

As a reminder, CVR Partners owns two nitrogen fertilizer plants in the Midwest. Its East Dubuque facility, located in the Corn Belt, produces a mix of ammonia, UAN, liquid and granulated urea, and nitric acid. Its Coffeyville facility, meanwhile, upgrades most of its ammonia production to UAN. The plant is a bit unique in that it uses pet coke as a feedstock versus natural gas, which most North American nitrogen fertilizer facilities use.

Q4 Earnings

CVR Partners reported its Q4 earnings earlier this week, recording revenue of $141.6 million, down nearly -33% year over year.

Product pricing at the gate for ammonia fell -52% year over year to $461 per ton, while UAN pricing dropped -47% to $241 per ton.

Ammonia production fell -2% to 205,000 tons, while UAN production fell less than -1% to 306,000 tons. Plant capacity utilization was 94% for the quarter compared to 96% a year ago.

Adjusted EBITDA decreased from $122.3 million to $37.9 million. This was just above the middle of the $31-42 million in adjusted EBITDA I projected in my most-recent write-up based on different commodity price scenarios.

Cash available for distribution fell from $111.0 million to $17.8 million. The company reserved $19.1 million for future turnarounds in the quarter, as well as $1.0 million for future operating needs. A year ago, the company reserved $9.1 million for future operating needs and $2.1 million for future turnarounds.

The company declared a variable distribution of $1.68 per common unit. This was above the $1.55 distribution last quarter. In my most recent write-up I projected a distribution of between $1.25-$2.30 based on different commodity price scenarios, and its payout landed pretty close to the middle of that range. The distribution will be paid March 11th to unitholders of record on March 4th

Looking forward, CVR Partners is looking for utilization of between 86-91% for its facilities in Q4. It is expecting Coffeyville utilization of 77-82% and East Dubuque utilization of between 95-100%.

The company is expecting between $52-57 million in direct operating expenses and between $9-13 million in CapEx.

At the end of the quarter, the company noted that ammonia prices for the Southern Plains were $634 a ton, down -42% compared to where it was a year ago at $1,097 a ton and 48% higher than where it was at the end of September when it was $429 a ton.

Ammonia in the Corn Belt was $696 per ton, down -45% from $1,272 a ton a year ago, but up 39% from $501 per ton at the end of Q3. UAN prices at the end of December were $293 per ton, -49% below the $578 a ton it traded at a year earlier and 8% above the $272 per ton it was at the end of September. Natural gas prices, meanwhile, were -52% lower at $2.92, but higher than the $2.66 it was at the end of Q3.

Discussing current market conditions of its Q4 earnings call, CEO Mark Pytosh said:

“We believe market conditions are steady, and we expect to see strong demand for nitrogen fertilizer for the spring 2024 planting season. Overall, grain market conditions have softened. … Grain prices, coupled with current fertilizer prices support attractive farmer economics, which should bode well for nitrogen fertilizer demand for spring 2024. We believe that the length of this upward demand cycle will, in large part, be driven by grain prices staying at elevated levels, and we see fundamentals for grains remaining steady. As I mentioned on the last several earnings calls, customer purchasing patterns have evolved to become more ratable due to higher inventory carrying costs from higher interest rates. We experienced this new buying pattern after the fall ammonia application, and we've seen more regular ratable buying of nitrogen fertilizer which is matching well with our production schedule. Geopolitical risk continue to represent a wildcard for the nitrogen fertilizer industry with meaningful fertilizer production capacity residing in countries across the Middle East, North Africa and Russia. We are closely monitoring developments in the Middle East that could impact energy and fertilizer markets, and we expect 2024 will be another period of higher than historical volatility in the business.”

Operationally, CVR Partners performed well, despite a strike at its East Dubuque facility. It did see utilization slip a little at East Dubuque, but this was due to a mechanical issue at the end of Q3 that ran a bit into early October. In Q1, meanwhile, it will have some planned downtime at Coffeyville as it has had some issues with an ammonia converter. That’s a bit disappointing and something to watch to make sure the issue doesn’t take longer than expected to fix

Compared to a year ago, fertilizer prices were down a lot, but they have rebounded from their lows. This continued rebound should help bolster Q1 results.

Meanwhile, the company noted that it was looking to potentially upgrade Coffeyville to be able to use either pet coke or natural gas as a feedstock. With natural gas prices so low over the last few years and LNG permits temporarily suspended, this could make sense if it doesn’t cost too much. Having flexibility to switch between the two, meanwhile, would be a nice advantage. It is also looking at some projects that could increase production at both its facilities.

Modeling Q1

As I've noted in the past, modeling CVR Partners isn't easy, as little changes to the model in prices can lead to some pretty big differences versus actual results, while the pricing it gets doesn't always match tracked pricing.

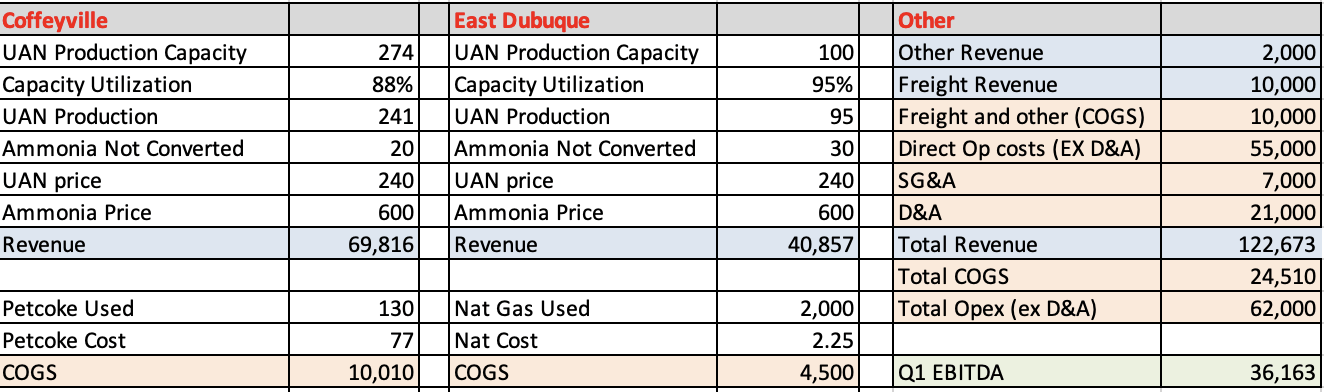

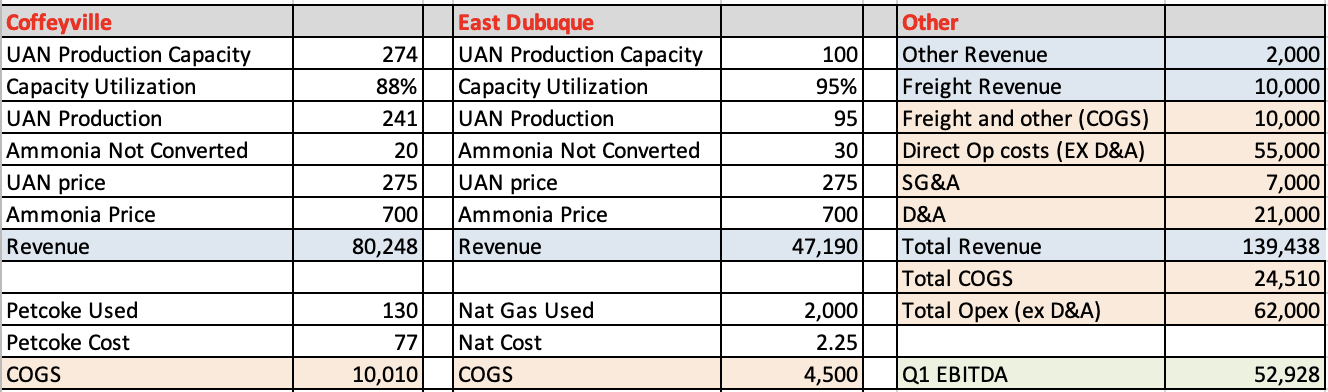

That said, using $240 UAN prices and $600 ammonia, I can get to around $36 million in Q1 EBITDA. Take out $7.0 million in interest expense and $5 million on maintenance capex, as well as $5 million in turnaround and other future costs, and you get $1.80 distribution. Using $275 UAN and $700 ammonia would get you $53 million in EBITDA and around a $3.40 distribution.

UAN EBITDA Model (Filings and Self)

UAN EBITDA Model (Filings and Self)

I could see pricing in 2024 settling in around $275 per ton for UAN and getting $700 per ton for ammonia, which would get you about $210 million in yearly EBITDA with no turnarounds. The company previously said it didn't expect any turnarounds until the fall of 2024 at the earliest, so there could be one this year. Place a 6.5x multiple on that to get you a $90 stock and over $13 in distributions, which would be an over 19% yield. With a turnaround, the distribution could be closer to $10, equating to a 15% yield.

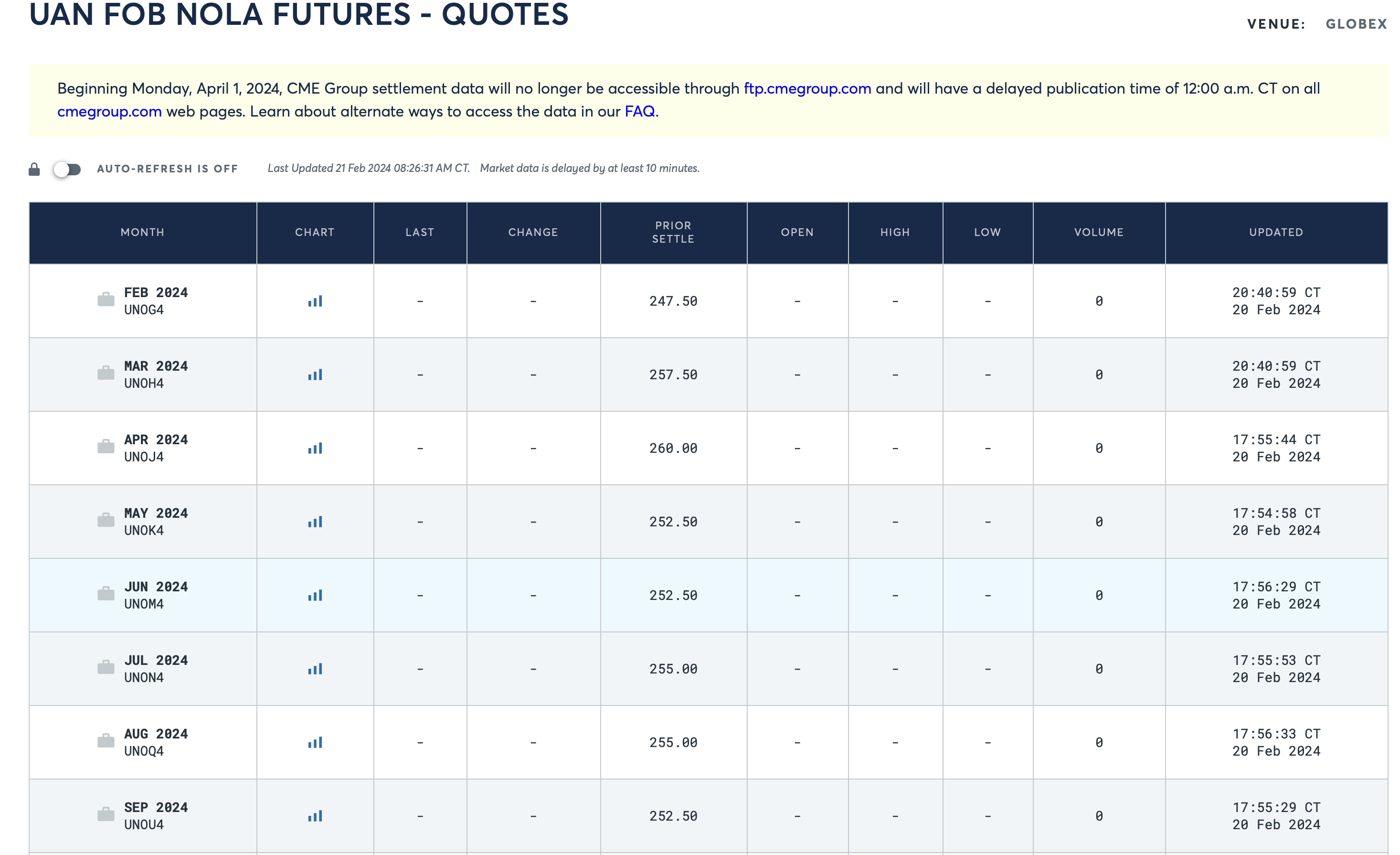

CME

Conclusion

Nitrogen fertilizer prices have been showing some strength compared to what CVR Partners realized in Q4. In the past, the company has tended to forward sell their production, so in a rising price market, its results often lagged a bit. More recently, though, it has been selling closer to the time of production. As such, I’d expect 2024 to be stronger than the back half of 2023, as prices appear to have bottom last year and are working their way back up.

Nitrogen fertilizer prices will continue to be the biggest driver for the company and its distribution. With the market looking up, I’m going to keep my “Buy” rating and move my price target down slightly to $90 from $95 due to some minor operational issues.

The biggest risk to the stock is lower nitrogen fertilizer prices, followed by any large operational issues. CVR Partners has a good track record on this front, but with only two facilities, one being down for an extended period of time would greatly negatively impact results.