cagkansayin

Biohaven: Navigating Through Biotech's Competitive Landscape

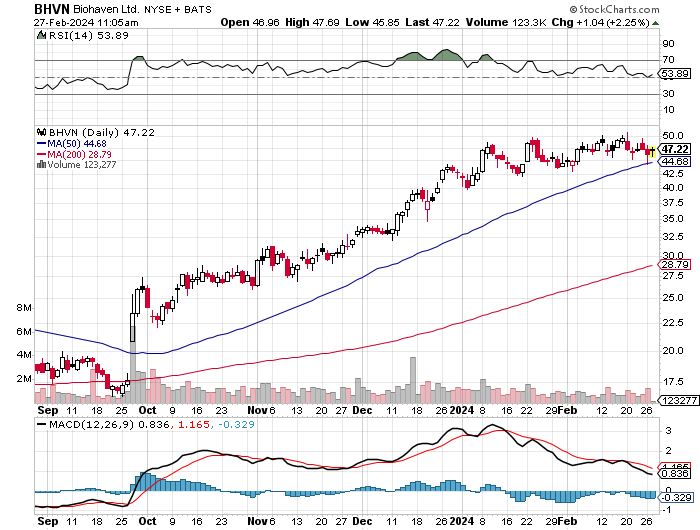

Biohaven's (NYSE:BHVN) stock is up 130% since my "Sell" recommendation back in August. In hindsight, my analysis missed the mark, and it appears I was too focused on their lead program (troriluzole) and overlooked their early-stage assets like BHV-7000. Fortunately, selling's only downside is opportunity cost and, due to the nature of biotechnology, we are still likely in the early innings.

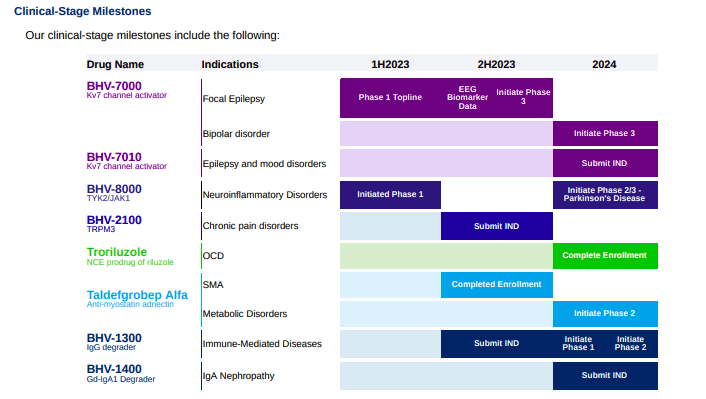

Biohaven's pipeline is diverse and very interesting.

Biohaven

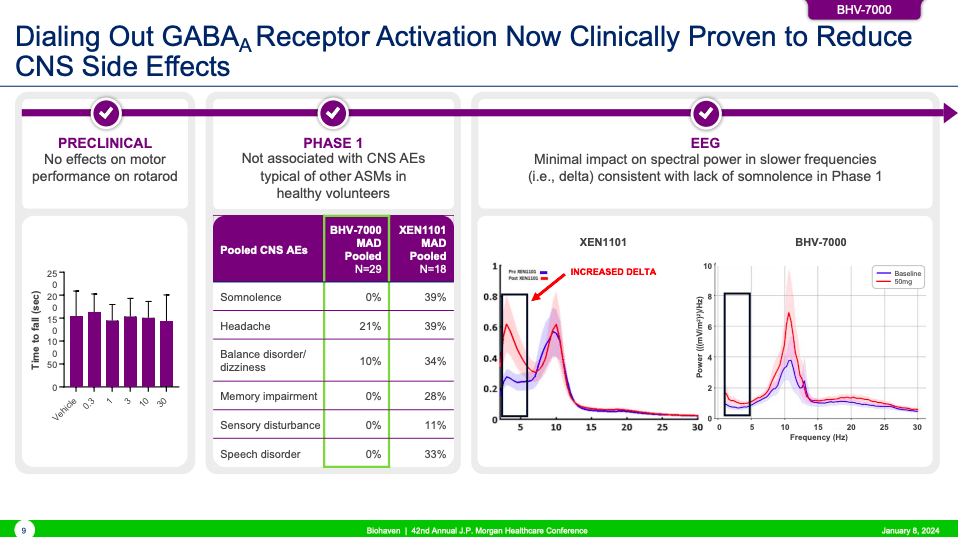

I have discussed the potential of Kv7 channel activators in the past with Xenon Pharmaceuticals (XENE). The biggest potential for Kv7 is in epilepsy. The mechanism of action is well-established for this indication. Recall that ezogabine was an earlier Kv7 activator that had great efficacy in epilepsy but, due to a poor pharmacokinetic profile, had unwanted side effects. The main concern was skin pigmentation changes that would occur in the eyes. The drug was slapped with a boxed warning due to concerns it could lead to vision changes, and its use became limited. Although it later became clear that the color changes were simply cosmetic in nature, the drug was pulled from the market due to "commercial reasons."

Xenon's Kv7 drug, XEN1101, is currently in Phase 3 trials for epilepsy and recently demonstrated efficacy in a Phase 2 depression trial. The breadth of studied indications for Kv7 demonstrates its potential. Biohaven is testing their Kv7 activators in epilepsy and mood disorders. Although conditions like epilepsy, bipolar disorder, and depression have multiple drugs on the market, a novel, safe, and effective drug would certainly have blockbuster potential. These conditions often require a few different drugs to manage and sometimes become treatment-resistant.

The company believes they have the superior Kv7 drug, but it's widely accepted that there is room for at least two on the market, considering their broad potential.

Biohaven

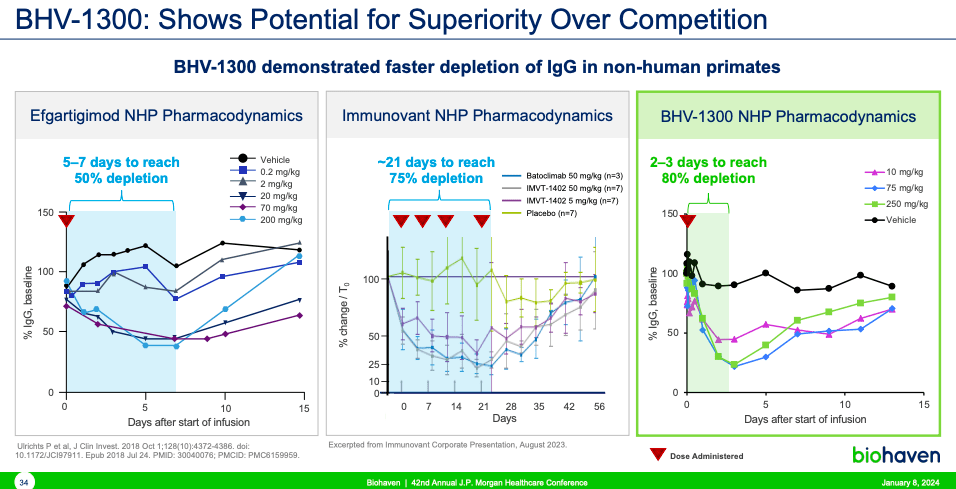

The next asset I'd like to address is Biohaven's IgG degrader, BHV-1300, for the treatment of immune-mediated diseases like myasthenia gravis. The Netherlands-headquartered Argenx (ARGX) is the leader here with their intravenous anti-neonatal Fc receptor efgartigimod. The company has amassed a market capitalization of $24 billion, and efgartigimod figures to be a multi-billion dollar drug.

We have already witnessed the market appreciation that can happen with a subcutaneous drug that can lower IgG levels with Immunovant (IMVT). Their FcRn inhibitor, IMVT-1402, has skyrocketed the company's valuation from sub-$1 billion to over $5 billion on Phase 1 data in healthy adults. Argenx is also developing a subcutaneous FcRn inhibitor to compliment efgartigimod.

Biohaven points out how BHV-1300 can be different from the competition.

Biohaven

Of course, we will have to await data to see if this is the case.

It is clear that both 1300 and their Kv7 drugs have blockbuster potential and clear paths to the market due to validated mechanisms of action. This gives Biohaven a few shots on goal and, importantly, they're not just aiming in the dark.

Financial Health

Turning to Biohaven's balance sheet, the aggregate of 'cash and cash equivalents', 'marketable securities and investments' totals approximately $240.6 million as of September 30, 2023. When considering debts such as Accounts Payable, Accrued Expenses, and other listed liabilities, the total debt amounts to $92.7 million. The current ratio, calculated as current assets divided by current liabilities, suggests a value of approximately 5.0, indicating strong short-term financial health.

Over the last nine months, the net cash used in operating activities was $216.8 million, equating to a monthly cash burn of approximately $24.1 million. With the addition of $258.7 million from an October public offering, their total liquid assets adjust to $499.3 million. This adjustment extends their cash runway significantly when considering the monthly cash burn rate. The financial analysis, based on past data, may not fully predict future performance, especially regarding cash flow activities that show a significant net loss offset by capital raising efforts.

Biohaven's cash flow activities suggest a reliance on financing activities to support operations and investments. This is typical for a clinical-stage biotechnology company. The substantial net loss and operating cash outflow underscore a potential need for additional financing within the next twelve months, but the recent successful capital raise lowers the immediacy of this need to a medium level.

Metric | Value |

Cash and Cash Equivalents | $111.7M |

Marketable Securities | $128.9M |

Total Liquid Assets (Pre-Offering) | $240.6M |

Total Liquid Assets (Post-Offering) | $499.3M |

Total Liabilities | $92.7M |

Current Ratio (Pre-Offering) | 5.0 |

Monthly Cash Burn | $24.1M |

Cash Runway (Months, Post-Offering) | 20.7 months |

Short-Term Financial Health | Robust |

Long-Term Financial Health | Adequate |

Market Sentiment

According to Seeking Alpha data, BHVN's market capitalization stands at $3.71 billion, reflecting significant investor interest despite the early stage of their pipeline. The company likely remains years away from meaningful revenue, so we will negate analyst revenue estimates in this analysis. Stock momentum is evident, outperforming the S&P 500 (SPY) across all observed timeframes, highlighting positive market sentiment.

StockCharts.com

Per Fintel, short interest is notable at 10.37% of float, suggesting a substantial bet against the stock, yet also potential for a short squeeze. Institutional ownership is robust at 87.03%, with notable movements including Stifel Financial Corp., Janus Henderson Group, and Suvretta Capital Management showing confidence through increased positions. Insider trades reveal positive net activity, with 1,153,307 more shares bought than sold over the past year, indicating insider confidence.

Given these dynamics, BHVN's market sentiment is qualified as "robust."

Is BHVN a Buy, Sell, or Hold?

Biohaven's value proposition is youthful but very apparent. The market is clearly pointing to potential here. Their pipeline, especially their Kv7 activators and IgG degrader, is full of promise and figures to provide investors with plenty of catalysts moving forward. The stock, valued at $3.71 billion, does not appear too expensive in light of these opportunities, and we are still in the early innings here.

I definitely missed the mark with my last analysis. Biohaven's pipeline warrants speculation. Therefore, I am upgrading my recommendation from "Sell" to "Buy," as I think plenty of upside remains here for those with patience.

Despite the overwhelming optimism of late, there is also reason for caution here. As addressed in the article, Biohaven faces intense competition, from larger players, in crowded indications like epilepsy and autoimmune disorders. Moreover, developmental-stage companies like Xenon and Immunovant may eclipse Biohaven's offerings in efficacy or safety. Although Biohaven's pursuits are numerous and diverse, this will lead to considerable cash burn moving forward and there is no guarantee that the company will ever recuperate their heavy R&D investments.

As usual, investors ought to keep their holdings diversified and avoid putting too many of their eggs in one basket. But I believe one that can raise your portfolio's alpha is Biohaven.