Scharfsinn86

Investment thesis: As the EU gradually wakes up to the fact that its economy passed the point of no return in its green economy transformation quest, as well as its efforts to completely cut economic ties with Russia, we see that it is waking up to the urgency of increasing its green hydrogen supply as well as its use. Fusion Fuel (NASDAQ:HTOO), which is a green hydrogen startup just saw a very significant boost to its stock price, based on yet another EU government grant meant to help the green hydrogen industry take root in Europe. Recent news coming out of the national government policymaking centers as well as from the EU suggests that this is just the beginning, and Fusion Fuel is well-positioned to take advantage and move out of startup status and become a fully established producer of green hydrogen as well as a seller of its equipment to others. However, if it fails to show signs of being able to make this move by next year, helped by the new EU grant boost, it may mean that it will never manage to take the step, which will amount to one final disappointment for investors, after a long string of already-established track record of disappointments.

After a long streak of disappointments, Fusion Fuel might finally start to see significant revenues flowing.

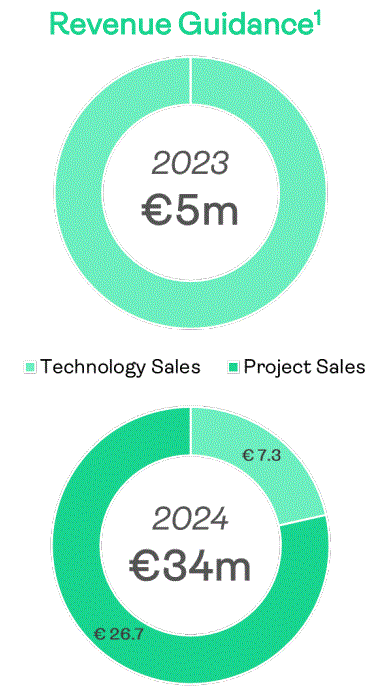

There is still not much that investors can go on in terms of Fusion Fuels' profitability prospects, given that it has yet to sell significant volumes of green hydrogen or its HEVO units. Current estimates for its 2023 sales suggest revenue of 5 million euros, while for 2024 it estimates a seven-fold increase to 34 million euros.

Fusion Fuel

The expected increase in revenues makes for a bullish argument for the company. The problem is that at the end of 2022, it forecast revenues of 25 million euros for 2023 and 80 million euros for 2024.

Fusion Fuel

Given the wide gap between past projections and actual performance, investors can be forgiven for no longer believing that Fusion Fuel is a growth story.

Fusion Fuel stock price (Seeking Alpha)

As we can see, the market all but abandoned this company.

For the third quarter of 2023, Fusion Fuel earned 2.51 million euros in revenues. It took a pre-tax loss of just over 4 million euros. It earned proceeds of $656,000 by selling 377,000 shares in the quarter. The number of shares outstanding increased by almost 6% in the past year. Its cash position declined significantly, from 3.09 million euros to 1.03 million compared with last quarter. There was also a significant decline in inventory from 19.3 million euros to 11.9 million euros, which does not seem to be reflected in a gain in revenues. The trade payables section also increased from 11.52 million euros to 13.43 million.

This significant decline in its financial performance is a possible indication that in the shorter term, it will have to further dilute its stock. The fact that government grants coming in its direction are covering many of its costs is helping to prevent stock issuance out of control and arguably makes for higher potential odds of investors eventually being rewarded for their patience with this stock. However, the poor financial performance of the company also begs the question of whether government grants will be enough to help it succeed.

The HEVO-Sines project in Portugal is expected to eventually produce 62,000 tonnes of green hydrogen per year. At an assumed market price of $5,000/tonne, the yearly revenues flowing from this project could reach over $300 million/year, which is roughly 10x higher than Fusion Fuel's current market cap. I should note that I expect green hydrogen producers to get a price for their hydrogen that will cover the costs of production as well as produce a profit, which is why I am assuming a price of $5,000/tonne to be the longer-term average price.

I am not sure whether the mechanism involved in producing that hydrogen sale price will be mostly driven by government intervention in the market or as a result of mostly regulatory frameworks in place that will mandate hydrogen consumers to buy some green hydrogen as a part of their overall mix. Somehow that sustainable market price for green hydrogen will be reached. With the recent EU grant, the Portugal project is now much closer to becoming a reality, and perhaps the years of investor disappointment are coming to an end.

The main drivers of generous EU and national grants for the emerging green hydrogen industry need to be understood, to understand the attractive nature of Fusion Fuel as an investment opportunity.

- The EU is all in on the green transition, there is no turning back the clock.

I cannot pinpoint the moment when the EU reached what I believe to be a point of no return in terms of its green energy transition agenda. The recent farmer protests and other forms of political pushback, such as voters turning away from pro-establishment parties are in my view a symptom of the fact that European society passed that point of no return and the current leadership is willing to stare down the emerging opposition, as the pain is starting to be felt and it is increasingly directly linked to the green initiatives already in force or being proposed.

Perhaps the point where all bridges were burned came in 2022 when the Russia-Ukraine war broke out into a full-blown confrontation and the EU decided to sever most economic ties in response. In effect, it was a divorce, between the World's most important net exporter of hydrocarbons, and one of the World's most important net importers. As things stand right now, it looks very permanent, and so are the consequences for both parties involved.

For the EU, it means that its hydrocarbons-based energy security model is permanently gone. There are still some pillars standing, such as its imports of natural gas and oil from Norway, but Norway's oil & gas production seems set to start declining at some point in 2026.

Norway oil & gas production history & forecast (Norwegian Petroleum)

Aside from the uncertain outlook for Europe's Norwegian hydrocarbon supplies, the assumption that America can and is willing to take care of Europe's energy shortfalls going forward is now questionable, given the recent decision to stop the expansion of LNG export facilities. It should be mentioned that the EIA's most recent forecast for US hydrocarbon production growth seems to point to impending stagnation, as I pointed out in a recent article. Resources from elsewhere, such as from Africa, the ME region can be made available to a certain extent, however, supplies and transport are increasingly subject to growing uncertainty related to political & geopolitical instability in the region.

In the aftermath of the 2022 intensification of the Ukraine-Russia conflict, EU natural gas demand saw a significant decline across the board, as I pointed out in a recent article.

Seeking Alpha

The steep decline in natural gas usage in Europe since 2022 means that there is no more room for further cuts in consumption, without causing deep economic & social damage. It is therefore imperative for the EU to ramp up renewable energy production, not so much in the interest of fighting climate change as it is often presented to the public, but rather because it needs to plug its current energy gap.

As the EU found out in 2021, intermittent energy sources can lead to severe long-term shortfalls in energy supplies, for which ample backup electricity production capacity is needed. For now, natural gas remains the backup generation capacity of choice, but Germany for instance just announced plans to build new natural gas turbines that will be ready to take hydrogen as an alternative fuel source starting about a decade from now. In other words, EU leaders expect green hydrogen to play a prominent role in electricity generation in Europe about a decade from now. In the meantime, the almost non-existent industry needs to be built up, which is why Fusion Fuel is seeing so much government support, and it will continue to see government funds flowing for perhaps the rest of this decade.

Investment implications:

- Government grants amount to subsidized capital investments, which should help to keep debt issuance and stock dilution needs low.

Many investors tend to react with skepticism to business models that depend to a large degree on government aid. The concern is that in the event of a shift in government policy, which tends to happen as the political winds shift, the industry benefiting from government support may fall out of favor. While this often tends to be the case, in my view, the EU no longer has much of a choice, as I laid it out. It is not so much that it may still believe in the green energy economy and its relative competitiveness. More than anything, it is a matter of the hydrocarbon-powered economy no longer being an available option.

Within this context, Fusion Fuel is set to receive financial help for many years to come, after which I expect that there will be a mechanism in place to ensure that green hydrogen production will be sustained by adequate green hydrogen pricing. It will probably be an industry that will be permanently subsidized. For Fusion Fuel, this means that it does not have to be overly aggressive in diluting its stock. It also lessens the need to take on debt to finance capital spending needs. Once production facilities are up and running, the EU will also ensure that the green hydrogen produced is sold at a sustainable price for producers. The way I see it, the EU is stuck in this policy, and in the process, Fusion Fuel has a high chance of rising from a startup to established producer status.

- Nuclear green hydrogen is the main risk to wind & solar hydrogen producers.

Last year, France led a group of Eastern EU members in carving out a special label for nuclear-powered hydrogen production, which came to be labeled as "pink hydrogen", thanks to the emissions-free nature of nuclear power. While many EU nations opted to do away with nuclear power in past years & decades, there are a few countries that can potentially opt to allocate some nuclear power capacity to the production of pink hydrogen, which seems poised to be treated on equal grounds to green hydrogen produced with wind or solar power. It remains to be seen how this will play out in terms of just how much pink hydrogen might hit the EU market, but I guess that it will have a competitive advantage over green hydrogen in terms of production costs, as well as reliability of supply volumes since it does not depend on the weather. I regard this particular threat to Fusion Fuel's solar-powered hydrogen production approach to be far more serious than the risk of government support for green hydrogen in Europe to disappear.

Conclusions:

By this time next year, we will probably have a clearer view of Fusion Fuel's ability to step out of its current pre-production phase into full production status, with continuing growth potential for many years to come. If it fails to take off, even with the recent EU grant for its Portugal project, then the odds are that investors will probably need to brace for a final disappointment on this investment.

Judging by the market's reaction since the announcement of the EU grant, where it recently gave up about half of the initial gains from the recent pop in its stock price, it seems that the market is already betting against this company, with many investors seeing the most recent rally in Fusion Fuel's stock as an opportunity to bail. This is understandable, given the long string of disappointments fed by constantly overly optimistic company forecasts that never materialized. If the negative sentiment continues, Fusion Fuel's stock could potentially still dip below $1/share, at which point I will consider adding more shares. I am currently sitting on an average share price of about $3.50. I do believe that with the recent EU grant approval Fusion Fuel's chances of success improved a great deal, it is therefore less risky to invest in this company, while the odds of investors being rewarded eventually have increased, and the timing of it has moved up. We will see in the next few quarters what Fusion Fuel will do with this opportunity. At some point next year, investors will know with a greater degree of certainty whether this stock is poised to soar, or whether it will leave them permanently disappointed.

Editor's Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.