Robert Way/iStock Editorial via Getty Images

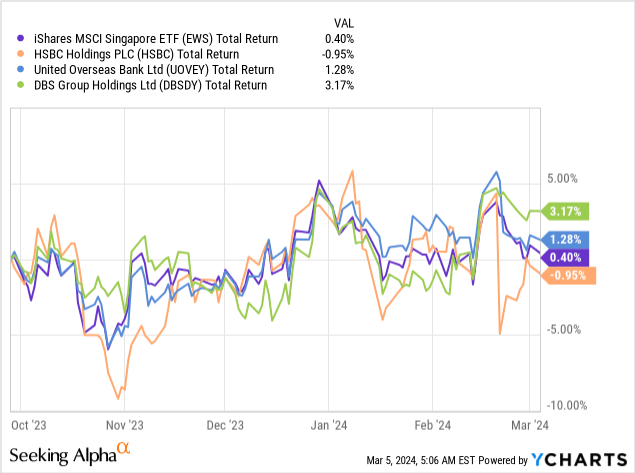

Shares of Singaporean bank DBS Group (OTCPK:DBSDY)(OTCPK:DBSDF) have been relatively quiet since my opening piece last September, returning just 3% in that time even as U.S. equities have rallied quite strongly. While this looks fairly tepid, the stock's performance is not out of line with more apt benchmarks, as the past few months has been a fairly lackluster spell for both the region's equities and specific Asian bank peers like United Overseas (OTCPK:UOVEY)(OTCPK:UOVEF) and HSBC (HSBC).

While DBS has been fairly muted from an investment point of view, the business continues to perform well, with the bank generating a very strong 18% return on equity ("ROE") amid record 2023 net income. With the shares continuing to look modestly valued at around 1.4x book value and a 7%-plus forward dividend yield, I keep my Buy rating in place.

A Record Year

DBS posted record full-year net income of SGD 10.3 billion for 2023, up around 26% on 2022 and mapping to a ROE of roughly 18%. One reason why DBS is so profitable is the nature of its funding structure, with deposits funding the lion's share of assets with a relatively lower reliance on more expensive wholesale funding. Importantly, relatively inexpensive CASA deposits (i.e. current accounts and savings accounts) still account for over 50% of total balances despite the bank experiencing mix-shift into fixed deposits brought about by higher interest rates.

When I covered it back in September, DBS's net interest margin ("NIM") was expected to peak in either Q3 or Q4, with funding cost pressure and slowing loan growth ultimately set to outweigh higher yields on earning assets. While NIM was 2bps higher in H2 compared to H1 (2.16% versus 2.14%), the Q4 exit rate of 2.13% was around 6bps lower than Q3, meaning NIM did indeed peak as expected. At the same time, customer loan growth now appears sluggish as borrowers face paying much higher interest rates on their loans, reducing overall demand for credit.

Source: DBS Group 2023 Annual Results Presentation

Despite some of the headwinds discussed last time materializing, performance in the latter part of 2023 remained strong, with Q4 net income of SGD 2.39 billion down 9% sequentially but still translating to a very healthy 16% ROE. Importantly, Q4 earnings were negatively impacted by some one-offs in the expenses line, which increased 8% sequentially in reported terms but by a modest 2% on an underlying basis. Despite this elevating the bank's cost/income ratio by nearly 5ppt sequentially, the Q4 figure of 44% would still be the envy of most banks in the world, and note this is actually high by DBS's standards.

Source: DBS Group 2023 Annual Results Presentation

On the plus side, credit quality remains supportive of earnings. Despite higher interest rates and slowing growth, DBS has yet to see any meaningful deterioration in asset quality. Non-performing loans were 1.1% of total loans in Q4, which was actually down a touch sequentially and unchanged on Q4 2022. This is contributing to still-low levels of provisioning expense, with provisioning for loans landing at just 11bps last quarter.

A Muted Near-Term Outlook, But That's Okay

DBS remains a NII-heavy bank, as this ultimately accounts for around 70% of the top line. By reducing its floating-rate asset exposure, management has lowered the bank's interest rate sensitivity, so NII should be a bit more resilient even if interest rates start to come down later in the year as implied by the forward curve. The outlook for loan growth still isn't great, but DBS will get a modest tailwind from continued upward repricing of assets, while it will also benefit from a full-year of ownership of Citi's (C) consumer business in Taiwan, with that deal closing in H2 2023. This should help keep NII relatively flat in 2024. Alongside guidance of double-digit growth in fee income, overall revenue should grow this year.

On the flip side, "low-40s" guidance for cost/income would be slightly higher than 2023, eating into pre-provision earnings, while on cost of credit, specific-allowances guidance of 17-20bps would be higher than the 11bps recorded last year. This would offset the positive impact of higher revenue, pointing to flat-to-down net income overall.

Now, I highlighted previously that DBS was a good way to play Asian growth. While a fairly muted near-term outlook for earnings appears at odds with this, I see this more as a feature of the business cycle rather than something more structural in nature. Or said differently, banks are cyclical businesses and this just isn't a great point in the cycle for earnings growth.

More importantly, capital returns potential and DBS's valuation remains compelling. On flat net income, ROE would still be attractive and within the 15-17% range that management targets. With the ADSs at $99.75 (SGD 33.40 in Singapore trading), DBS trades for around 1.4x book value per share. That looks quite modest given the bank's earnings power, as in theory it could return circa 11.5% to shareholders at that valuation assuming a ~16% ROE. DBS did raise its ordinary dividend in Q4 to SGD 0.54 per share, while it also declared a 1-for-10 bonus issue of shares. With management pledging to maintain the higher ordinary payout post-issue, shareholders are essentially looking at a 7%-plus forward yield in total.

Although the dividend hike brings the annualized run rate to SGD 2.16 per share (~$6.45 per ADS), this still equates to a fairly modest payout ratio of ~60% post-share issue. Furthermore, obscuring DBS's current ROE and capital returns potential is the strong health of its balance sheet, with the bank reporting a 14.6% CET1 ratio in Q4. This remains comfortably above management's 12.5-13.5% target range, implying significant levels of surplus capital. Because of the bank's relatively high ROE and still-modest payout ratio, DBS will either have to distribute more cash to shareholders or do more M&A if it is to reach management's capital ratio target.

Source: DBS Group 2023 Annual Results Presentation

For that reason, management maintains the firepower to carry on hiking dividends even if earnings growth flatlines in the near term. This feature of the bank was part of my buy-case at initial coverage, and indeed management's target of SGD 0.24 per share in annual dividend hikes out to 2026-2027 remains in place:

We should be able to sustain the 24-cent per year increase for two to three years. It is not just payout from earnings for the year, but there is also an element of a capital return from the stock position as we currently have a CAR ratio that is quite high.

Piyush Gupta, CEO DBS Group, Q4 2023 Earnings Call

This would equate to a CAGR of around 8-9% from the current annualized run-rate. With this coming on top of a 7%-plus base yield, DBS stock remains attractive despite a softer near-term earnings outlook, and I remain comfortable with my initial Buy rating here.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.