Richard Drury

There is no question that the Calamos Convertible & High Income Fund (NASDAQ:CHY) has proved very successful over the years, as evidenced by the fund's performance versus the benchmark and the peer group. Such consistent results are reflected in a double-digit premium to NAV, as opposed to other convertible funds not managed by Calamos investments that generally trade at a discount.

While the fund's heavy exposure to convertibles and particularly to growth sectors is expected to remain beneficial to total returns going forward, current stock market valuation is arguably rich after the rally seen in the previous months. This suggests a cautious, long-term approach might be prudent for the time being.

In spite of that, CHY remains an attractive opportunity for income-oriented investors, given its distribution rate of 10%, and also looking for total return over the long run, due to convertible securities' appreciation potential.

Fund Description & Highlights

The fund positions itself as an enhanced fixed-income option and seeks to deliver both income and capital appreciation through a combination of investments in convertibles and high-yield bonds. The investment in convertibles offers the growth potential of equities, while still generates additional income. Meanwhile, the portion allocated in high-yield bonds aims to achieve higher income compared to traditional fixed-income options.

As of January 31st, 2024, 67.4% of the fund was invested in convertibles, 25.5% in high-yield corporate bonds, a minor allocation of 4.1% in bank loans and 2.4% in cash and equivalents. Still, the fund management has employed a leverage of nearly 37%, what gives the fund an allocation in convertibles of nearly 100%.

The convertibles' portfolio is diversified, with top 10 holdings accounting for only 13.4% of its total exposure in convertibles. As we can notice when looking at its top 10 holdings list (Uber Technologies, Palo Alto Network, DexCom, Ford Motor, On Semiconductor, Shift4 Payments, Wayfair, PPL Capital Funding, Vail Resorts, Sea), its constituents are very different from broader stock market indexes, such as S&P 500, where these are primarily the largest U.S. companies, such as Apple, Microsoft, Alphabet, Berkshire, Exxon, for instance. For context, while S&P 500's constituents have a median market cap of nearly $30 billion, companies with convertibles in CHY's portfolio have a median market cap of as low as $8 billion.

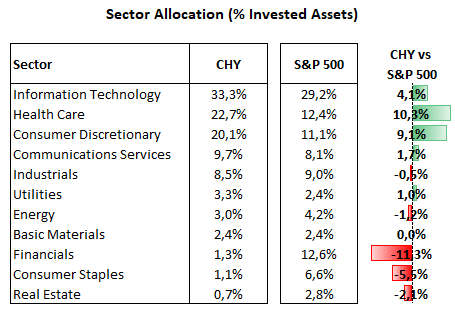

From the sector allocation perspective, the largest exposure of CHY's convertible portfolio is in the information technology sector with 33.3%, followed by health care with 22.7%, consumer discretionary 20.1%, communication services 9.7%, industrials 8.5%, utilities 3.3%, energy, 3.0%, basic materials 2.4%, financials 1.3%, consumer staples 1.1% and real state 0.7%.

That sector allocation is not significantly different compared to the S&P 500 tough, despite CHY's overweight position in health care (+10.1%), consumer discretionary (+9.1%), information technology (+4.1%), sectors where there is typically higher convertible security issuance.

Calamos, State Street's websites, consolidated by the author

While convertibles securities represent by far the largest allocation of the fund, the portion of assets invested in high-yield corporate bonds is still significant and constitutes a core strategy as well.

The combination of these two main strategies, convertible and high-yield corporate bonds, gives CHY a weighted coupon of 3.07%, which is above the category of convertible funds (2.22%), but way below the category of high-yield bonds funds (6.63%).

Meanwhile, CHY's average maturity of 3.8 years is shorter than the maturity of the category of convertibles funds (4.02 years) and high-yield bonds funds (4.74 years), which is consistent with CHY's management goal to keep the fund less sensitive to moves in the interest rates.

The actual performance of the fund over time with the combination of both strategies can be seen in the next section.

Compelling Long-Term Track Record

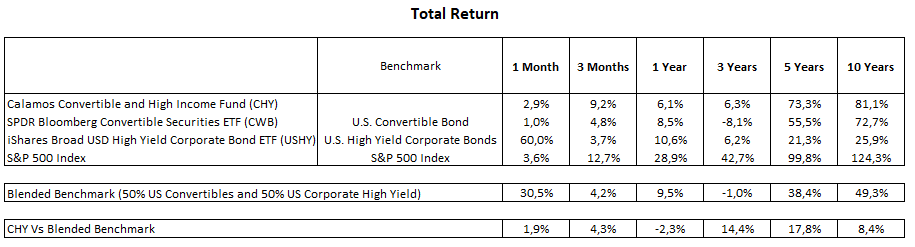

The performance of CHY has been quite solid over time. Compared to a blended benchmark (50% US Convertibles and 50% US Corporate High Yield, as defined by the fund management), and using for comparison purposes two liquid ETFs, SPDR Bloomberg Convertible Securities ETF (CWB) and iShares Broad USD High Yield Corporate Bond ETF (USHY), we have seen the fund outperforming this blended benchmark in longer term periods (3, 5 and 10 years), but also in the short term (1 and 3-month periods). The only exception is the 1-year timeframe, where the fund indeed lagged both the convertible and the high yield benchmarks.

YCharts, consolidated by the author

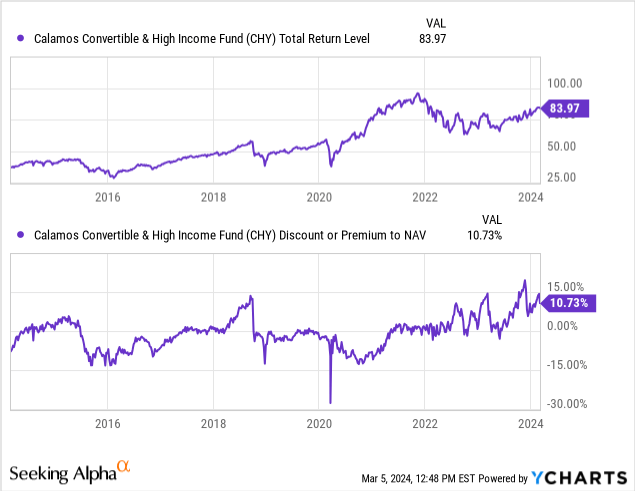

Of course, the appreciation in the stock market has been a major contributor for the performance seen in convertibles over this 10-year period. Even so, while gains for the benchmark has been solid, the total return seen in shares of CHY has been quite strong and, unsurprisingly, the fund has been consistently in the first quartile relative to other convertible funds.

Navigating a Challenging Environment for Distributions

CHY's current distribution rate of 10.11% is a little lower than a few other convertible funds, where we can see distribution rates of nearly 11% or even 12%.

A positive here is that the fund has been able to keep the monthly distribution unchanged since the beginning of 2021 at $0.10 per share, returning to the level seen for much of past decade, after a period of distributions of $0.085 started in late 2018.

While the broader market has experienced a rally since October 2023, the period preceding it was quite challenging for the fund. The last annual report for the 12-month period finished in October 2023 illustrates very well those harsh conditions undergone by the fund.

According to its annual report, the fund generated $21.25 million through net interest after amortization and $5.44 million through dividends, totaling an investment income of $26.69 million. After netting out $35.62 million relative to net expenses during the period, there was a net investment loss of $8.94 million. In addition, there was a net realized gain from investments of $95.77 million and an unrealized loss of $96.45 million. The fund also reported a net increase from capital stock transactions of $7.78 million.

Based on this report, we noticed that the proceeds generated by realized capital gains and capital stock transactions totaled $103.56 million, which were more than enough to cover the net investment loss of $8.94 million and a distribution of $91.18 million. However, the fund saw a net decrease in net assets of $93.01 million over that period, or nearly 11% in net assets that ended the period at $724.82 million.

To be sure, a double-digit decrease in net assets is something relevant. The flip side of the equation is that the fund had $96.45 million in unrealized losses that could potentially recover once the convertible and bonds prices that hindered performance are back to previous levels.

In my view, these mixed numbers showed in the annual report are consistent with the relative underperformance of CHY in the last 12 months. The overweight position in convertibles, which lagged high-yield corporate bonds, alongside securities and sector selection in convertibles, dragged down the return during the period, according to the annual report.

Nonetheless, my view is that the fund's management deserves some credit, given its long-time execution. I also see the fund allocation as constructive, with its overweight allocation to higher-growth sectors, such as technology, health care and consumer discretionary, while maintaining a limited exposure to the financial sector, especially given a still volatile interest rate environment.

That said, as CHY can continue to show positive performance, distributions are expected to remain unchanged for the time being. However, the fund's ability to cover current distributions without relevant returns of capital to shareholders is something to watch in the event of a broader market correction, given the sharp rally in the recent months and elevated valuation multiples now in place.

High Premium Reflects Strong Performance, But It Is A Bit Extended Now

All three convertibles closed-end funds run by Calamos Investments (CHY, CHI and CCD) are trading at nearly double-digit premiums versus NAV, in a stark contrast to other convertible funds that trade at a discount.

Granted, the outsized returns achieved over the years by Calamos' family of convertibles CEF warrant higher premiums relative to their peers, but I see the current premium of 10.7% of CHY near peak levels. On the other hand, premiums close to zero seen in 2022 and during stock market bottoms in 2023 are a reference for short-term pullbacks.

That said, while an ideal entry point would be with premium at low single-digit, investors may have a more reasonable cushion for safety if premium drops to the range of 7-8%, as seen in December 2023.

But, overall, CHY is an investment opportunity, given its historical outperformance versus peers, a portfolio positioned for growth and a juicy distribution rate of nearly 10%.

Investors should take a long-term view though, as the broader market has just hit record levels and current valuations may limit the short-term upside potential.

On top of that, after this strong move upwards since October, market is probably more vulnerable now and any bad news on the macroeconomic front may trigger a selloff. In such an event, CHY's portfolio is expected to have a greater downsize risk, given the convertible securities are generally composed by smaller cap companies with worse financials and more restrict access to capital than well-established names.

In turn, high-yield corporate bonds are particularly subject to experience higher credit spreads if the economy deteriorates. While an adverse environment may be short-lived, the impact on the short-term price action should be detrimental for the portfolio and therefore impact the fund total return over this timeframe.