XH4D/iStock via Getty Images

ASML (NASDAQ:ASML) is recognized as the world's leading supplier of photolithography equipment, integral for the production of microchips and integrated circuits. ASML's machines are critical components in semiconductor manufacturing, enabling semiconductor companies like Taiwan Semiconductor (TSM) and Samsung (OTCPK:SSNLF) to manufacture incredibly powerful chips.

Of all the companies involved in the semiconductor industry, ASML may have the most to benefit from the AI boom. Unlike the top companies in other semiconductor sectors, ASML has a virtual monopoly in the advanced EUV photolithography. The company even has a dominant presence in the relatively less-advanced DUV photolithography space. This means that ASML is likely to capture the vast majority of growth in the photolithography space for the foreseeable future.

Insurmountable Moat

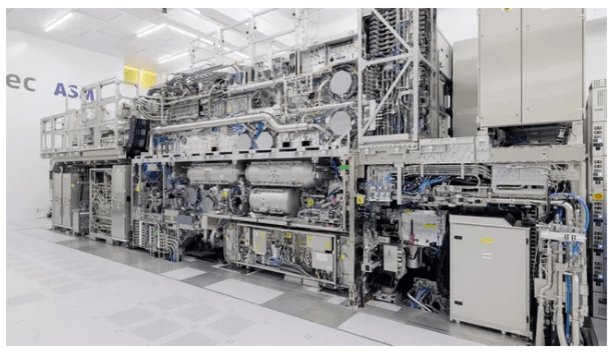

ASML arguably has the largest technological moat of any company right now. The advanced photolithography machines that ASML produces are so complex in design that even entire nations like China are finding it nearly impossible to replicate the technology. After all, these are the machines that are responsible for creating single nanometer chips, which are in their own right some of the most advanced technology in the world right now.

ASML photolithography machines typically cost hundreds of millions of dollars per unit, with its latest high-NA lithography machine costing up to a whopping $380 million. The level of complexity involved in manufacturing such machines is truly mind-boggling, as a single machine can involve hundreds of thousands of different components. Moreover, many of these components are technological marvels in their own right.

The sheer complexity and technological sophistication involved in making such machines have allowed ASML to slowly widen the gap between itself and competitors over the years. As it currently stands, it appears there are no competitors that are even willing to dip their toes in this arena, allowing ASML to even further widen the gap as the company continues to innovate on even more complex machines.

ASML's lithography machines are arguably the most complex machines in the world. They are so complex that ASML enjoys a virtual monopoly, especially in EUV machines.

ASML

Capturing all the Upside of the AI Boom

Given the near-monopoly ASML holds on advanced lithography machines, the company is in the unique position to capture nearly all the upside of the AI boom. While there are a few companies that manufacture lithography machines like Canon (OTCPK:CAJPY) and Nikon (OTCPK:NINOY), the machines these companies focus on are less advanced and older DUV lithography technologies.

As AI continues to drive demand for smaller nanometer chips, only ASML's advanced machines will be able to meet such demand. As such, the company will not have to worry about competitors cutting into margins or taking away demand. ASML also has unparalleled resources to throw at R&D, which will only allow them to pull further ahead.

While the semiconductor manufacturing industry also has incredibly high technological barriers to entry, evident in TSMC's dominance, this industry is starting to see major competition. This is partly a result of the AI boom and also a result of government entities assisting in their own respective semiconductor companies. The USA, for instance, is providing a great deal of assistance to US semiconductor companies via the CHIPS Act so that they do not have to rely on foreign companies for crucial semiconductor technologies.

It is only natural for nation states to want their own semiconductor industries given how increasingly important semiconductor technologies are to virtually all industries, particularly national defense. This competition will only drive demand for ASML's most advanced machines as it is impossible for semiconductor companies to meaningfully compete without them.

Benefitting from the AI Arms Race

Demand for the most powerful chips is starting to rise exponentially as a result of the AI arms race between the tech giants. OpenAI, which is backed by Microsoft (MSFT), has vast resources at its disposal and an incredibly ambitious CEO pouring staggering amounts of resources into its AI projects. Google (GOOGL) (GOOG), which I believe rightfully views OpenAI as an existential threat, is now being forced to spend untold billions into developing AI systems that are comparable to those of OpenAI.

As a result of Google's increasingly advanced Gemini AI, developed in response to OpenAI's ChatGPT, Android phones like the Samsung Galaxy and Pixel now have access to incredibly powerful AI. Now, Apple is being forced to respond by creating its own comparable AI so that its own smartphone and devices business is not disrupted. Amazon (AMZN) is also being forced to help develop a comparable ChatGPT AI product so that AWS stays competitive with Microsoft's Azure, which will be using ChatGPT. In fact, Amazon recently invested $4 billion into OpenAI competitor Anthropic.

In the background of all this, Meta's (META) CEO Mark Zuckerberg has made his intentions clear that Meta will be at the forefront of the AI race, indicating that Meta will have an AI infrastructure consisting of a whopping 350,000 H100 Nvidia (NVDA) graphics cards. The company is also developing its own competitive generative AI known as LLaMA. Meta's own AI ambitions are not surprising as it is also competing in several of the same markets that the aforementioned tech giants are competing in.

OpenAI's ChatGPT was the first domino that started a massive AI wave among tech giants. It will not be surprising to see these tech giants spend hundreds of billions of dollars on AI training and inference alone over the next few years. In fact, Anthropic's CEO Dario Amodei said it would not be surprising to see a $1 billion AI model in 2024 and $10 billion AI models in 2025 given that the scaling laws seen in AI have not meaningfully slowed down. As such, there is still far more room for parameter growth as the data needed to feed these AI models are not running out anytime soon.

ASML is the only company in the world that can supply the machines needed to manufacture the chips used for training by LLMs. The company will effectively capture all the upside of this demand with no competitors to speak of. Even dominant chip manufacturers like TSM and chip designers like Nvidia have competitors. ASML's technology is so advanced that reverse-engineering its machines are nearly impossible without the technical knowledge and supply chain needed to manufacture and put together all the parts.

Strong Financials

ASML maintains relatively strong financials amidst growing demand for its machines. In 2023, the company reported €27.6 billion in net sales and €7.8 billion net income, which are figures that will likely only grow in the coming years as the adoption of AI accelerates. While ASML expects net sales to be similar in 2024, much of this flat growth is due to trade restrictions to China. As the company adjusts to this new reality, it should start to see sales accelerate dramatically after 2024.

The company's strong financials allow it to invest far more into research and development than other competitors in the space like Canon or Nikon. The company currently spends around $4 billion a year in R&D, which is a figure that is only growing larger. It is hard to foresee any competitors willing to make a serious effort to take market share away from ASML given how increasingly resource-intensive and complex EUV and DUV machines are becoming.

ASML

China Presents a Major Risk

ASML has been facing a growing number of restrictions on exports to China. The US-led effort to push China out of the chip supply chain is expected to severely hamper ASML's growth, especially considering the huge Chinese demand for ASML's machines. It could take a few years for ASML to recover from the lost demand that has resulted from the Chinese trade restrictions.

To make matters worse, the act of freezing China out of the global chip-supply chain will effectively force China to invest in its own lithography technology. In fact, China appears to have already figured out how to create 7 nm chips despite the sanctions placed on it. China's shocking rapid development on this front may not be so shocking in hindsight given the importance of chip technology and the Chinese government's vast resources.

If China can figure out how to manufacture lithography machines that come even close to the quality of machines produced by ASML, this will be a huge blow to ASML. Fortunately for ASML, such technology is incredibly hard to replicate, and is only getting harder as the limits of photolithography are pushed even further. However, if any entity can make a solid attempt at catching up to ASML, it is the Chinese government.

Conclusion

ASML continues to widen the gap between itself and the rest of the field with every passing year. The level of sophistication and complexity involved with manufacturing cutting-edge lithography machines and orchestrating its supply chain is becoming increasingly hard to replicate. While ASML is richly valued at its current valuation of $389 billion and forward P/E of 48, I believe the company's growth potential actually makes it undervalued in the long-term.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.