Yevhen Smyk

Investment action

I recommended a buy rating for GFL Environmental (NYSE:GFL) when I wrote about it the last time, as I expected the stock to continue trading at a premium. Based on my current outlook and analysis of GFL, I recommend a buy rating. I believe the market is not appreciating the potential upsides in GFL FY24 EBITDA guidance given how the share price has reacted post-earnings. This presents a good opportunity for investors to size up their positions, as I expect GFL to beat the guidance. Also, management FCF guidance for FY24 reinforced my view that it is on track to reach a similar leverage ratio level against peers, which is key to its valuation re-rating.

Review

My high-level take on GFL’s 4Q23 results is that it was great. The business reported 4Q23 adjusted EBITDA of CAD492 million, which was ahead of the consensus estimate of CAD490 million. The beat was primarily driven by higher pricing for solid waste and better Environmental Services performance. GFL continues to see a strong pricing tailwind as solid waste core prices came in at 7.9% in 4Q23, outpacing the volume decline of 3.6%. 4Q23 EBITDA margin also tracked well against my full-year expectation of 26%, coming in at 26.1%, which was up ~200bps y/y.

Contrary to my view on the result, GFL’s stock price remains pressured after the results, which I think is great as it provides an opportunity for investors to size up their positions. I believe the cause of this price action is the conservative guidance (in line with consensus) that management had laid out, which makes it hard for investors to be confident about FY24. My contrarian view here is that GFL will easily beat its EBITDA guidance (FY24e adj EBITDA of CAD2.215 billion), which reflects an EBITDA margin of 27.7%, implying an improvement of 100bps y/y. There are a few reasons for my saying this. Firstly, GFL should see incremental improvement in repair and maintenance [R&M] and labor turnover, which management has explicitly noted will moderate and provide upside potential. Secondly, a key assumption that management made was that commodity prices would be below the current level (i.e., 4Q prices). For context, 4Q prices are 20% above FY23 average levels, and management is assuming 10% below for FY24. The key thing to note here is that this guide was provided 2 weeks ago, or ~7 weeks into FY24, and the fact that management used “current levels” suggests that 4Q23 prices have continued into mid-February. Thirdly, GFL should also see a high incremental margin from the upcoming projects that are coming online at the Arbor Hills facility. Based on management’s words, my inference is that they have only included projects that were commissioned in late 2023 and not those that were expected in 2024. Lastly, GFL is expected to close a deal in 2Q24 (already signed), and that asset is expected to be immediately margin-accretive. Also, to give further confidence on management’s guidance, consider that they have consistently beaten their EBITDA guidance since they started issuing it (since FY20).

We also expect that the cost impact on productivity, cost of risk and repairs and maintenance from labor turnover trends and supply chain constraints will moderate and potentially provide upside to our guidance.

Recycled commodity prices are assumed to be at Q4 levels, which were 20% higher than the 2023 average, but 10% lower than current pricing. If current pricing remains at Q4 levels, there would be upside to our 2024 guidance.

Included in the guide is approximately $30 million of incremental adjusted EBITDA from RNG, all from our Arbor Hills facility that was commissioned in late 2023.

Over half of this amount will go towards a medium-sized acquisition that we have already signed. The asset represents a vertically integrated Solid Waste business within one of our fastest growing existing markets in the Southeast that will be immediately margin-accretive. 4Q23 call

Another aspect that I believe the market is not appreciating is GFL's ability to generate cash to deleverage its balance sheet. In FY24, management guided for an adj FCF of ~CAD800 million, and this guide essentially confirms my previous view that GFL could reach peers’ levels of mid-3x leverage in FY24. Assuming the entire CAD800 million is used to pay down debt and GFL manages to get just half of the potential CAD1.6 billion from divesting assets, the leverage ratio drops to 3.5x.

Deleveraging almost a full turn to over 50% was coming from organic growth of the business. Optimizing our footprint was the divestiture of three non-core US Solid Waste markets for $1.6 billion at mid-teens multiples. 4Q23 call

EPA

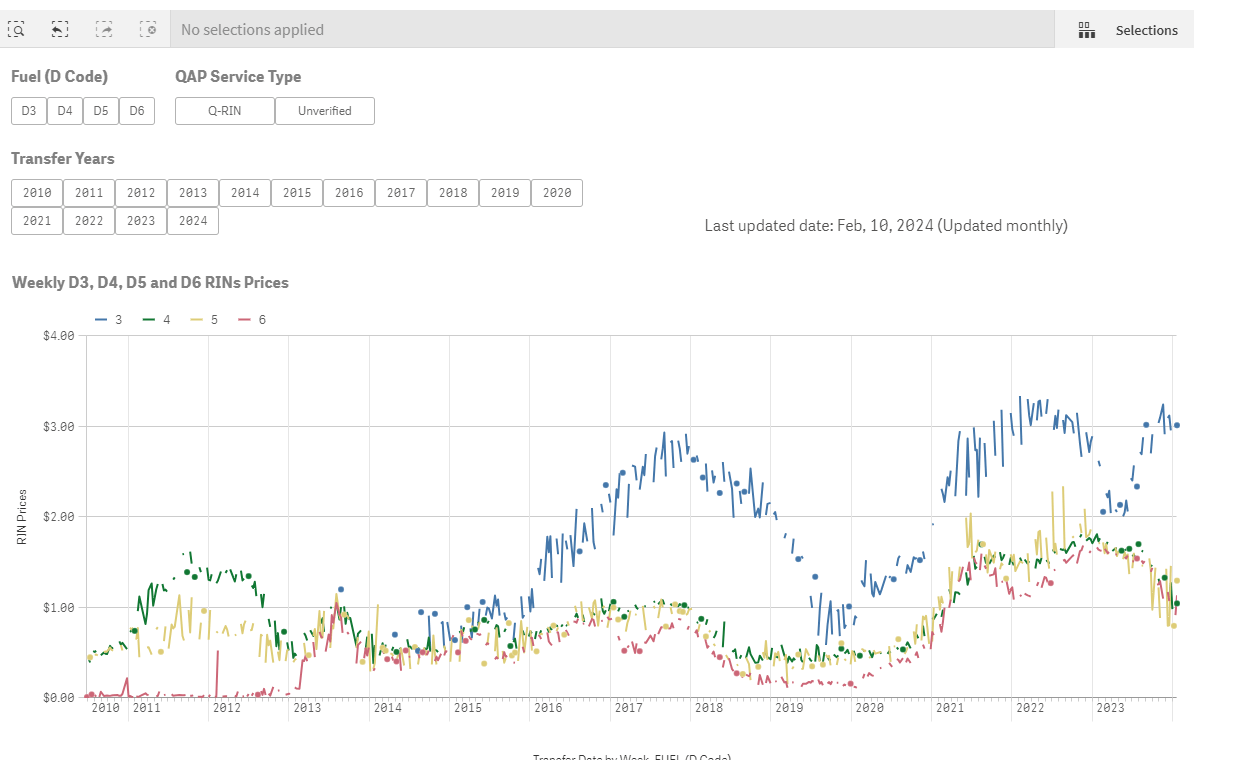

I think it is also important to note that capex for FY24 is elevated because of the inclusion of CAD250 to CAD300 million of growth capex related to EPR and RNG projects, and there is potentially significant upside to management sustainability targets given the price appreciation of D3 RIN values relative to management expectation (it is priced at $3 now vs. management estimate of $2) in their initial EBITDA and FCF assumptions. If prices sustain at this level or go even higher, EBITDA and FCF could go higher, which means the leverage ratio could come down faster than I expected.

Valuation

Author's work

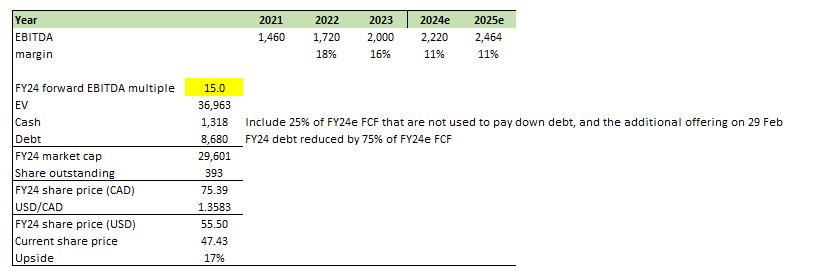

I believe GFL can continue to grow its EBITDA by a low percentage with no issues, given the operating leverage, sustained pricing growth, and potential upsides from the margin drivers I mentioned above. The 11% growth expectation is anchored upon management FY24 EBITDA guidance. Compared to my previous model, FY25 EBITDA is now modestly higher by CAD70 million. The bigger change to my model is that I am expecting GFL valuations to rerate upwards to 15x EBITDA. This conviction is driven by the FY24 FCF guidance, which gives me more confidence that GFL is on track to reach peers’ leverage ratios. As I have noted previously, when GFL shows tangible results that the leverage ratio is shifting downwards to peers’ levels, GFL should gradually trade in line with peers. Currently, GFL trades at 12x forward EBITDA, and I expect it to trade up to 15x.

Author's work

Risk and final thoughts

An economic downturn would result in fewer waste volumes and likely also less price growth over time, which would weigh on earnings. Given that M&A is a key part of GFL's growth strategy, in a bad economy, it could be hard for GFL to continue tapping into the capital markets to execute this strategy, thereby impacting growth.

I am reiterating a buy rating for GFL. I believe GFL has high potential to beat its FY24 EBITDA guidance due to moderating R&M and labor turnover issues, higher-than-expected commodity prices, margin-accretive acquisitions, and management’s strong historical track record of exceeding guidance. Additionally, GFL's strong FCF generation will allow them to deleverage and reach peer leverage ratios, unlocking valuation upside. As GFL demonstrates progress towards peer leverage levels, I expect the stock to re-rate to a higher valuation multiple (15x vs. current 12x).