SHansche

Last April, I started coverage of Frontline (NYSE:FRO) with a "Hold" rating, saying the company was riding some powerful market trends, but that they wouldn't last forever. In December, meanwhile, I noted the company was starting to trade at a large premium compared to the value of its vessels. The stock has been a strong performer since both write-ups. Let's take a closer look at the stock following its recent earnings report.

Company Profile

As a refresher, FRO operates a fleet of crude oil and refined product tankers. Its fleet consists of 41 VLCCs, 24 Suezmaxes, and 18 LR2/Aframaxes.

Of the vessels it owns, 99% are considered ECO vessels, while 57% of its fleet has scrubbers installed. The average age of its fleet is 5.8 years.

Q4 Results

Given that all FRO's revenue comes from the spot market, its results tend to follow these rates up and down. For Q4, the company saw a big year-over-year decrease in rates against tough comps, while sequentially rates were steady to higher.

For the quarter, the company realized spot TCE rates of $42,400 for VLCCs, $45,700 for Suezmax tankers, and $42,900 for LR2/Aframax vessels. That was a down considerably from the rates it realized last year of $63,200 for VLCCs, $57,900 for Suezmax tankers, and $58,800 for LR2/Aframax vessels

Quarter over quarter, rates were slightly lower for VLCCs, down -0.4% from $42,500. However, rates were up nicely for Suezmax and LR2/Aframax vessels, jumping 21.5% and 26.5%, respectively.

FRO recorded a net income of $118.4 million, or 53 cents per share. Adjusted EPS came in at 46 cents, down from 97 cent a year ago.

Revenue for the tanker operator sank by -22% to $415.0 million.

Adjusted EBITDA dropped -31% from $198 million a year ago to $287 million.

The company declared a 37-cent dividend for the fourth quarter, up from 30 cents in Q3.

Looking ahead, FRO said that 81% of its Q4 TCE rates were done at $55,100 for VLCCs, which is about a 30% increase from Q4. About 72% of Suezmax TCE rates are at $52,800, which is a 16% sequential increase. LR/Aframax TCE rates, meanwhile, are 69% locked in for Q1 at $67,800, a 58% sequential jump.

The company took delivery of 11 VLCCs vessels it acquired from Euronav NV in December, and 12 more in January. One more will be delivered later in the Q1.

FRO also agreed to sell its five oldest VLCCs and its oldest Suezmax tanker for $335 million. After paying off existing debt on the vessels, it will receive $238 million in net proceeds.

It is also in the process of refinancing eight Suezmax tankers and 16 LR2 tankers. The action is expected to add $408 million in cash proceeds. The company will use the cash from the sales and refinancing to pay off a shareholder loan it took to make the Euronav NV acquisition.

Discussing the current market on its Q4 earnings call, CEO Lars Barstad said:

"So, as you all know, the headlines are covered by the Middle East tension. The situation in Israel and Palestine. Following that the Red Sea/Aden situation and its ton miles implications, looking at it from a tanking perspective. We're also seeing that U.S are increasing the pressure on what's referred to either as the Dark Fleet or the Grey Fleet, and also increasing their focus on potential Russian price cap evasions. It was quite interesting to read earlier in the week that they've analyzed the tanker fleet and found that according to them, the Grey Fleet now consists of 135 VLCCs, 92 Suezmaxes, and 150 Aframaxes. These are vessels on dark trading in Iranian barrels, trading to North Korea and doing all sorts of stuff, and including the Russian fleet. That's a 375 vessels in total in the segments that we worked in. [Up to 700 vessels] are involved in some sort of shady activity, that amounts to 8% of the total tanker fleet. So these numbers are quite shocking. Another thing that's kind of played a part in the last few months has been the high activity in the contracting market. Well, especially so for Suezmaxes and VLCCs, actually to the extent where 2027 is starting to become somewhat tight. Also, another kind of important thing to notice, we've been through a long period of OPEC voluntary cuts, particularly sold by Saudi Arabia. This has maybe or potentially lead to non-OPEC production being allowed to grow quite remarkably. So global oil trade has kind of paused a little bit. … [but] we do see that in oil in transit is on the rise. And we expect it to be due to the longer ton miles around Cape of Good Hope, avoiding Suez Canal."

FRO turned in a solid quarter, as spot rates increased meaningfully on a sequential basis for both its Suezmaxes and LR2/Aframaxes vessels, while VLCC rates were pretty steady. More importantly, though, the company locked in much higher rates for Q1 across all three vessel types.

The issues in the Red Sea and ships being attacked continue to re-direct many vessels away from the Suez Canal to take longer journeys around the Cape of Good Hope. This combined with ships in the gray market transporting Russian oil have led to a tight market for oil tankers. All this is keeping spot rates high.

FRO is clearly benefiting from current market dynamics, given its spot rate exposure. The company has also smartly bought some newer ships, while selling some of its oldest vessels.

The industry order book for VLCCs is minimal and manageable for Suezmaxes, although LR2 vessels could come under pressure as the overall size of the fleet will rise by over 20% this year. However, LR2 vessels are a smaller part of FRO's overall business.

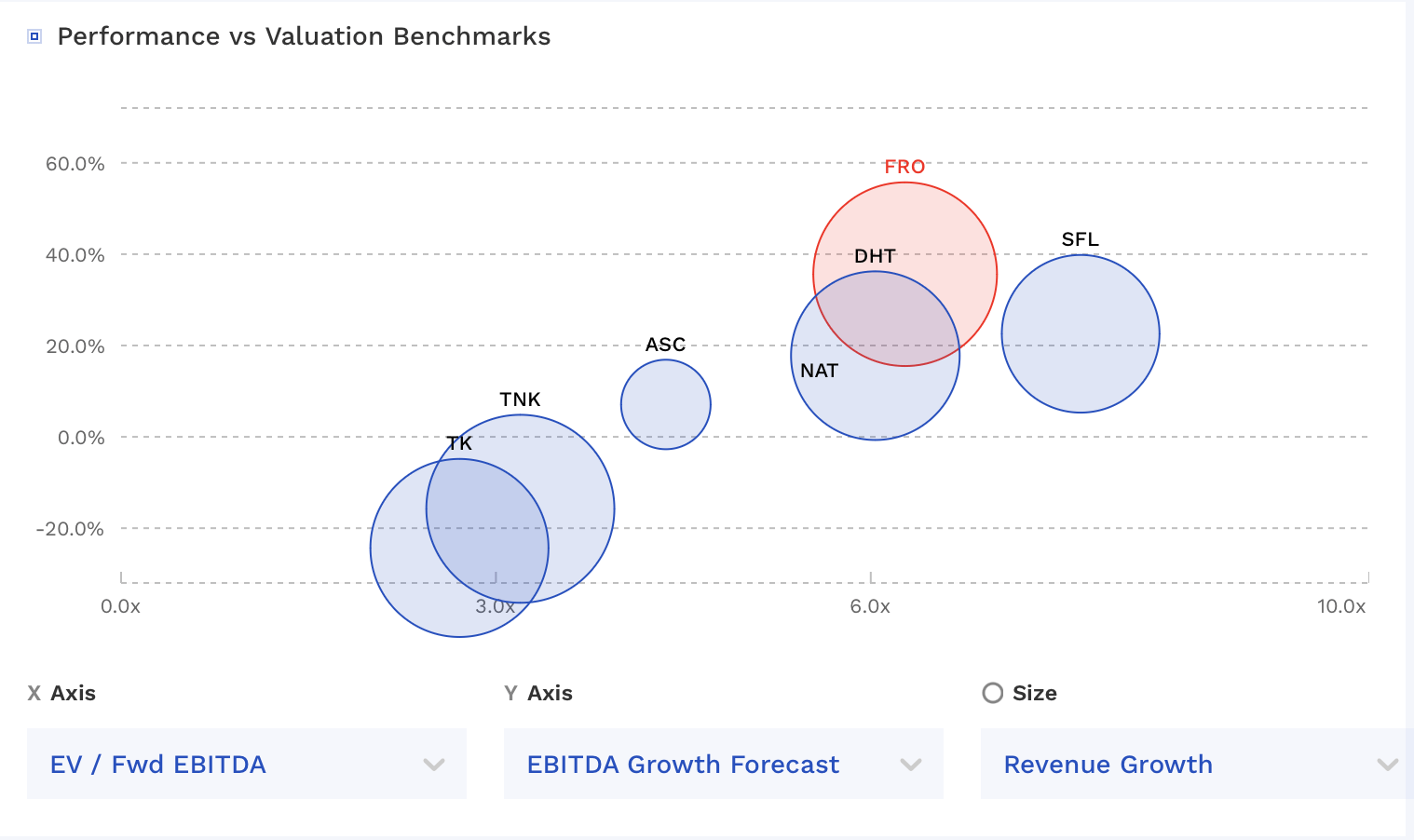

Valuation

FRO trades at 6.5x the 2024 EBITDA of $1.29 billion. Based on 2025 EBITDA, it trades at 6.0x the $1.39 billion estimate.

On a PE basis, it trades at 7.4x EPS estimates of $3.31. Based on the 2025 consensus for EPS of $3.88, it trades at 6.1x.

FRO stock trades towards the higher end of other marine shipping companies.

FRO Valuation Vs Peers (FinBox)

The price of 5-year-old VLCCs has been on the rise, with Clarkson now valuing them at around $111 million. Second-hand Suezmaxes are cheaper, valued at about $85 million, and Aframaxes are at around $70 million or more. That would value its fleet at about $19.50 per share, considering its recent sales and the $504.4 million it drew on its facility to add the vessels in January and the $100 million it needs to pay for the last vessel.

This is much higher than the $14 per share I last pegged the value of its fleet. This is in part due to higher vessel prices. However, the biggest difference it that company's debt went up much less than I anticipated from the acquisition.

Conclusion

FRO continues to operate in an attractive environment for tanker operators. This is likely to continue until the issues in the Red Sea clear up and vessels routes return more to normal. When that actually happens though is very uncertain.

At this time, investors can enjoy the ride with FRO. However, I do think there is a cap on where both vessel prices and the stock can go from here. As such, I continue to rate the stock a "Hold." My target range is between $20-24.

When looking at risk to the downside, lower spot rates, which could be caused by economic weakness or an improvement in the Red Sea, is one risk. In the past, a cure to high shipping rates has always been more ships, so over-ordering is another risk.

On the upside, any more global disputations to ocean-based shipping or an improvement in oil consumption could be a boost to the stock.