Justin Sullivan

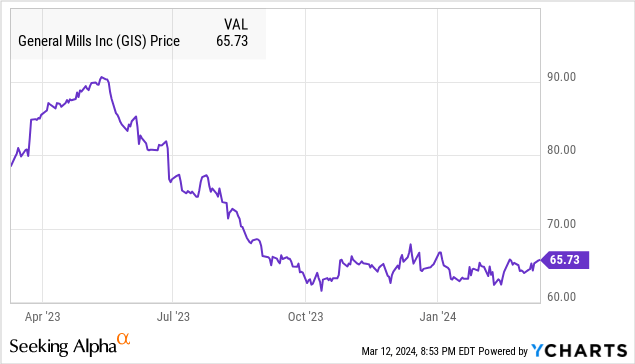

General Mills Inc. (NYSE:GIS) is attempting to navigate a challenging environment within packaged foods and the consumer staples sector. Shares are down nearly 30% from their 2023 high following a string of disappointing results over the past year, highlighted by soft demand trends globally.

We're taking a cautious view of GIS ahead of its upcoming earnings report. While the company is moving forward with efforts to control costs and push pricing in support of margins, declining sales remain a concern.

The next few quarters will be critical for the company to show signs of an operational turnaround to convince the market trends are moving in the right direction. There is also a question on valuation, with GIS continuing to trade at a premium relative to peers. This article covers the key trends to watch.

GIS Q3 Earnings Preview

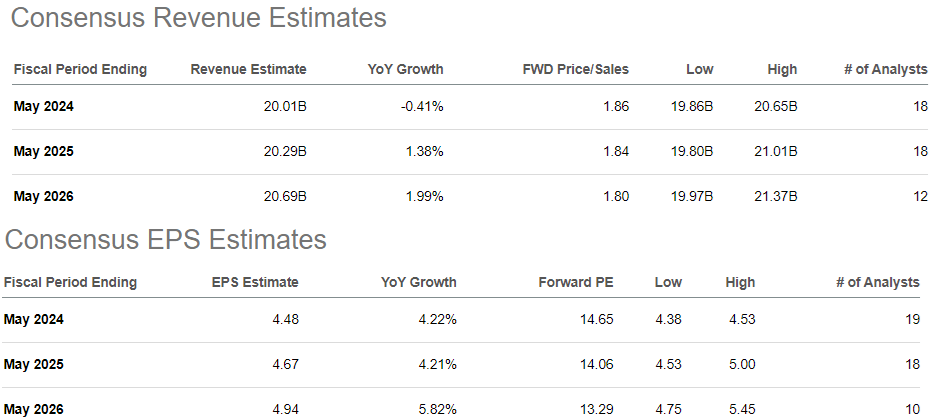

GIS is set to report its Q3 results on Wednesday, March 20, before the market opens. The current consensus is for EPS of $1.04, representing a 7.6% year-over-year increase.

The market is looking for revenue approaching $5 billion, a decline of -3.2% compared to Q3 2023. Within that amount, organic volumes should be a bit lower, balanced by a higher sales and pricing mix.

Seeking Alpha

Reconciling the expected EPS momentum this quarter, some of that considers improved margins through a "holistic margin management" strategy. This includes steps to rationalize expenses as well as higher pricing realizations.

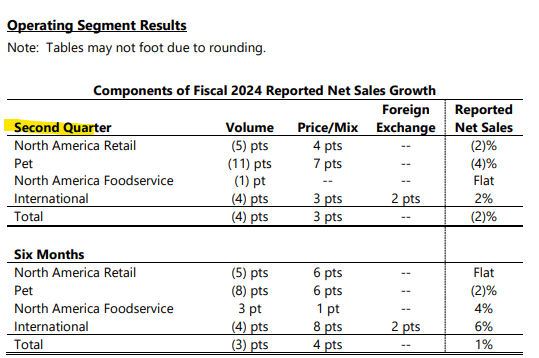

The recent weakness here largely comes down to the sales trends. All four segments between North America Retail, Pet, North America Foodservice, and International posted negative volumes in Q2. Pet food in particular has been a weak point with an -11% volume decline in Q2, where there are signs the company is losing market share.

source: company IR

Management has cited consumer "value-seeking behavior" implying some substitutions toward cheaper brands in cereal products and pet offerings.

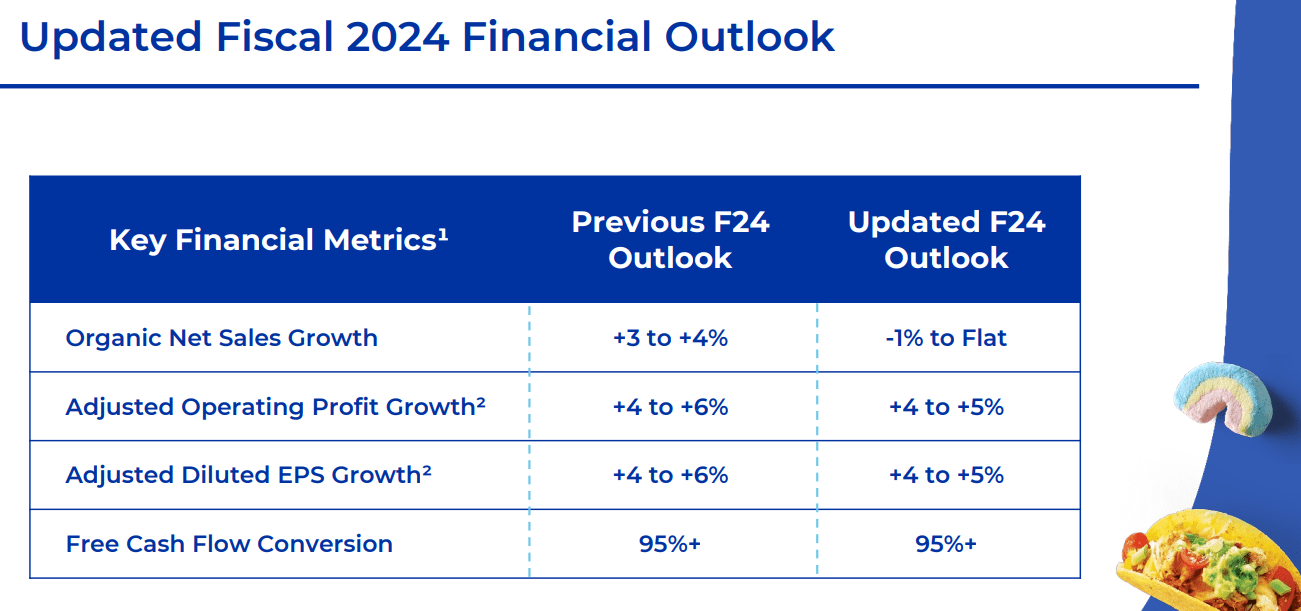

For the full year, the company expects organic net sales growth between a 1% decline to a flat figure. Notably, this was revised lower from the prior 3% to 4% increase forecast, with that change explaining much of the weakness in the stock over the last few months. Adjusted EPS is expected to increase between 4% and 5%.

source: company IR

What's Next For GIS?

When we look at GIS, the case here is that the outlook is hardly inspiring. Beyond what will be softer comps getting into fiscal 2025, there's not much on the horizon to suggest organic sales are set to re-accelerate higher.

We also question how much further room there is to cut expenses and raise pricing as a primary driver of EPS. Ultimately, we just don't see the stock price sustaining a significant rally until there is evidence of a stronger recovery in organic sales.

Seeking Alpha

According to consensus, the market sees GIS sales growth averaging less than 2% over the next two years, while EPS is stronger in the 5% range. The risk here is that this rebound in growth fails to materialize and works to reset earnings expectations lower.

Seeking Alpha

To be clear, many of the headwinds facing General Mills are part of a broader theme facing many companies in the consumer staples sector and packaged foods in particular. The Kraft Heinz Co (KHC) reported its fiscal Q4 earnings in February, with the headline being weak volumes.

WK Kellogg Co (KLG), as a breakfast cereal peer, also posted a decline in sales during its last quarter but noted it had gained market share in the U.S., presumably at the expense of General Mills.

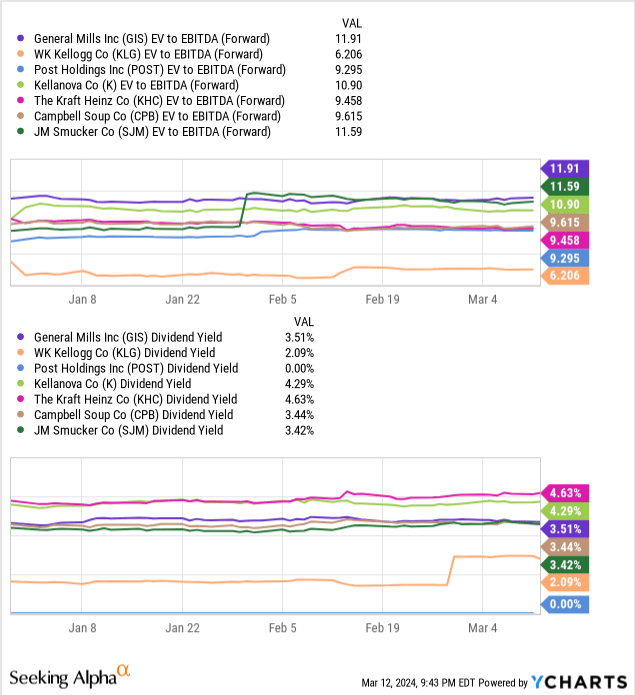

The other factor we're watching is that despite the numerous weak points from GIS's outlook, we note that shares remain valued at a premium over comparable packaged foods stocks. GIS EV to forward EBITDA multiple of 12x is well above an average among names like WK Kellog Co (KLG), Post Holdings Inc (POST), Kellanova Co (K), Kraft Heinz, JM Smucker Co (SJM), and Campbell Soup Co (CPB) closer to 9x.

A similar dynamic is observed across other valuation multiples, including through the P/E and in terms of sales. GIS's 3.5% dividend is also below the 4.3% level from K or 4.6% in shares of KHC. While GIS's larger size and category positioning may justify some spread, our takeaway is that the stock appears expensive, all else equal.

Final Thoughts

We rate GIS as a hold, implying a neutral view on the stock price from the current level under the assumption that the large selloff over the past year has already incorporated many of the weak points.

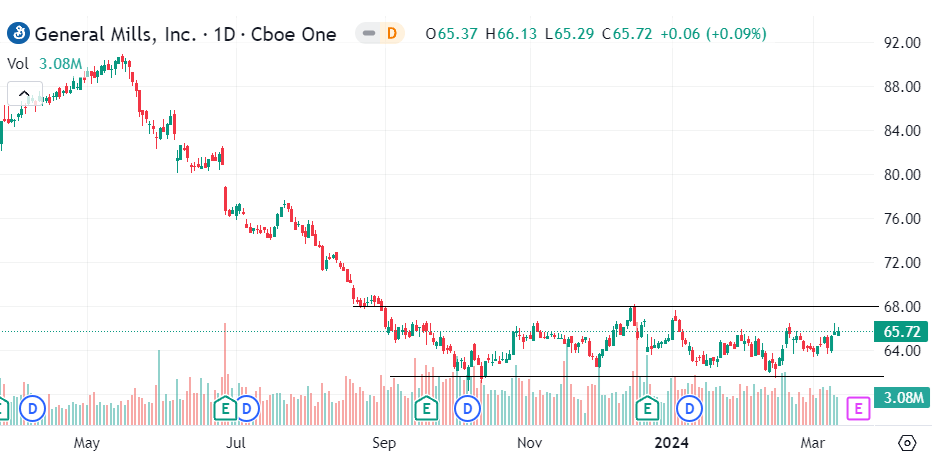

Naturally, the bullish case for GIS is that the company will prove us wrong when it reports results and outperforms expectations for the rest of the year. While that is a possibility, we're not convinced this quarter will mark that turning point. The base case is for the stock to remain stuck in a tight range between $60 and $70 per share for the foreseeable future.

Monitoring points in this Q3 report include the trends in volumes, margins, and any updates to full-year guidance.

Add some conviction to your trading! Take a look at our exclusive stock picks. Join a winning team that gets it right. Click for a two-week free trial.