magicmine

This is my second UroGen (NASDAQ:URGN) article following 12/2023's "UroGen: Binary Bet On UGN-102" ("Binary Bet"). In Binary Bet, I cautioned about UroGen's gut wrenching volatility; this volatility is likely to continue as it awaits developments on its lead therapy UGN-102 in treatment of low-grade intermediate risk non-muscle invasive bladder cancer (LG-IR-NMIBC).

I suggested that for those interested in investing in this name, it makes more sense to ease in on downdrafts. In this article I update my review in light of its earnings as reported in its 03/2024 earnings press release (the "Release"), conference call (the "Call") and 10-K (the 10-K).

JELMYTO, UroGen's sole approved therapy has limited potential albeit Q4 2023's double digit growth

As described in Binary Bet:

The FDA approved JELMYTO (mitomycin gel) in treatment of low-grade upper tract urothelial cancer (UTUC) on 04/15/2020. Urothelial cancer is a cancer of the lining of the urinary system. It ran into a buzzsaw of COVID disruption chilling its launch.

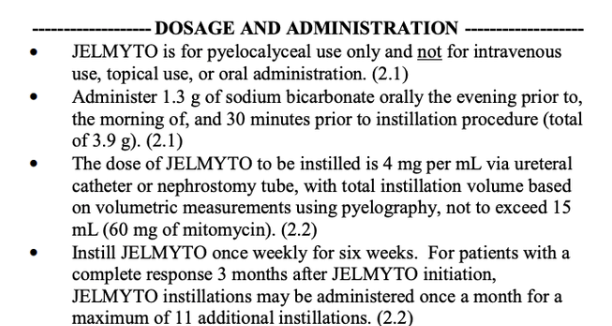

Yes, the pandemic slowed things down and disrupted JELMYTO's launch, but as handy as it is as a scapegoat one must not lose sight of JELMYTO's own structural challenges. The problem is obvious from the DOSAGE AND ADMINISTRATION section of JELMYTO's label below:

accessdata.fda.com

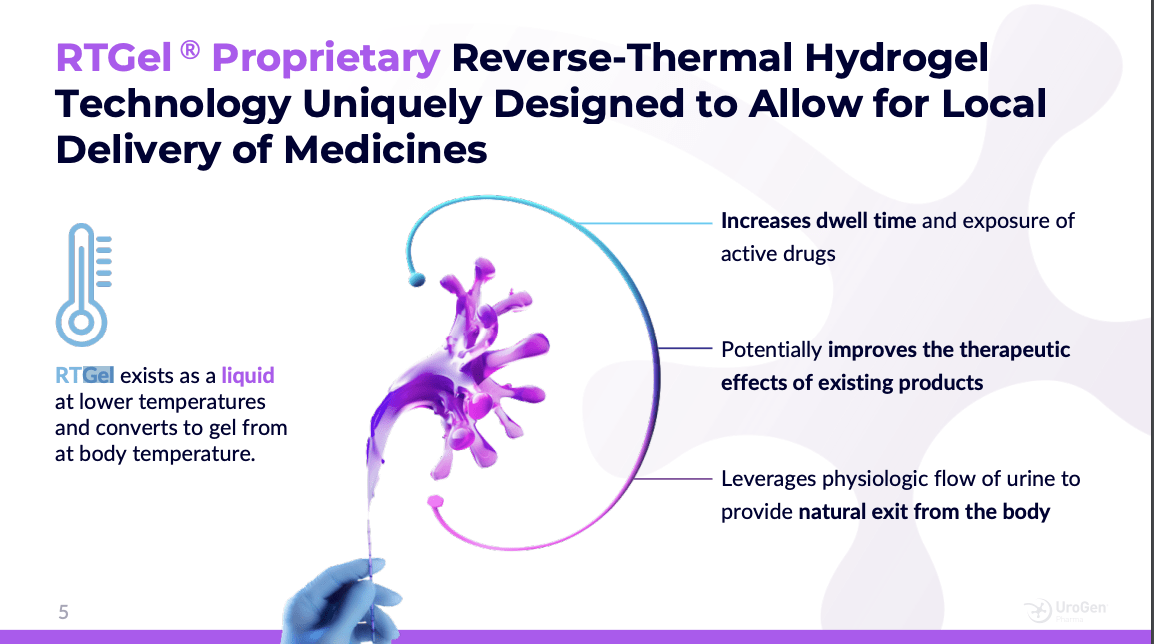

JELMYTO is not a therapy that fits seamlessly into a busy clinical practice. It requires special tools. These include a Chilling Block and a Uroject 12 syringe lever. These odd devices are employed to administer JELMYTO which employs UroGen's unique proprietary RT Gel technology described on slide 5 of its 03/2024 website presentation (the "Presentation"):

urogen.com

RTGel takes a minute to wrap your head around. Unlike matter that we are familiar with it exists as a liquid at lower temperatures and warms to a gel in the human body. One of the challenges associated with this is JELMYTO's limited shelf life of 1 week.

During the Call CCO Bova noted that:

...Despite achieving our targeted unit sales, the value of each unit was lower than anticipated, primarily due to gross to net erosion driven by higher-than-forecasted 340B rebate and estimated Medicare refunds for discarded drug...

Guided finances for 2024 assure that UroGen's accumulated deficit will continue its upward trajectory

The 10-K sets out UroGen's accumulated deficit as of close of 2023 at ~$0.68 billion; this is not bad for a development stage biotech that already has one approved therapy with a second set to launch as early as H1, 2025. UroGen's revenue guidance for 2024 as set out in the Call projects JELMYTO revenues ranging from $95 million to $102 million (midpoint $98.5 million).

During the Call CFO Kim advised that full year operating expense was expected to be in the range of $175 million to $185 million (midpoint $180 million); this included noncash share-based compensation expense of $6 million to $11 million, subject to market conditions. Midpoint to midpoint this results in an annual loss of $81.5 million.

As for liquidity he reported:

... UroGen had $141.5 million in cash and cash equivalents and marketable securities at December 31, 2023. Based on our latest financial forecast, we believe our current cash position and resources and projected revenue will support our commercial organization through the potential launch of UGN-102 in early 2025. ...

This UGN-102 potential launch is critical for UroGen shareholders. Its success is highly contingent.

UGN-102 is the primary driver of UroGen's future growth

UGN-102 is a big deal for several reasons set out in the Presentation, including:

- UGN-102 has shown positive complete response rate [CR] data in two phase 3 trials for low-grade intermediate risk non-muscle invasive bladder cancer (LG-IR-NMIBC) with duration of response rate data expected in Q2/2024;

- UGN-102 is being developed as a minimally invasive, non-surgical option that has the potential to set the new standard of care for LG-IR-NMIBC

- the addressable US market for this indication is 82,000 (22,000 newly diagnosed 60.000 recurrent) representing a $3 billion market according to UroGen's market research;

- UGN-102 is furthest along in clinical development as a non-surgical chemoablative therapy;

- in a recent survey conducted for UroGen 92% of urologists said they would use UGN-102.

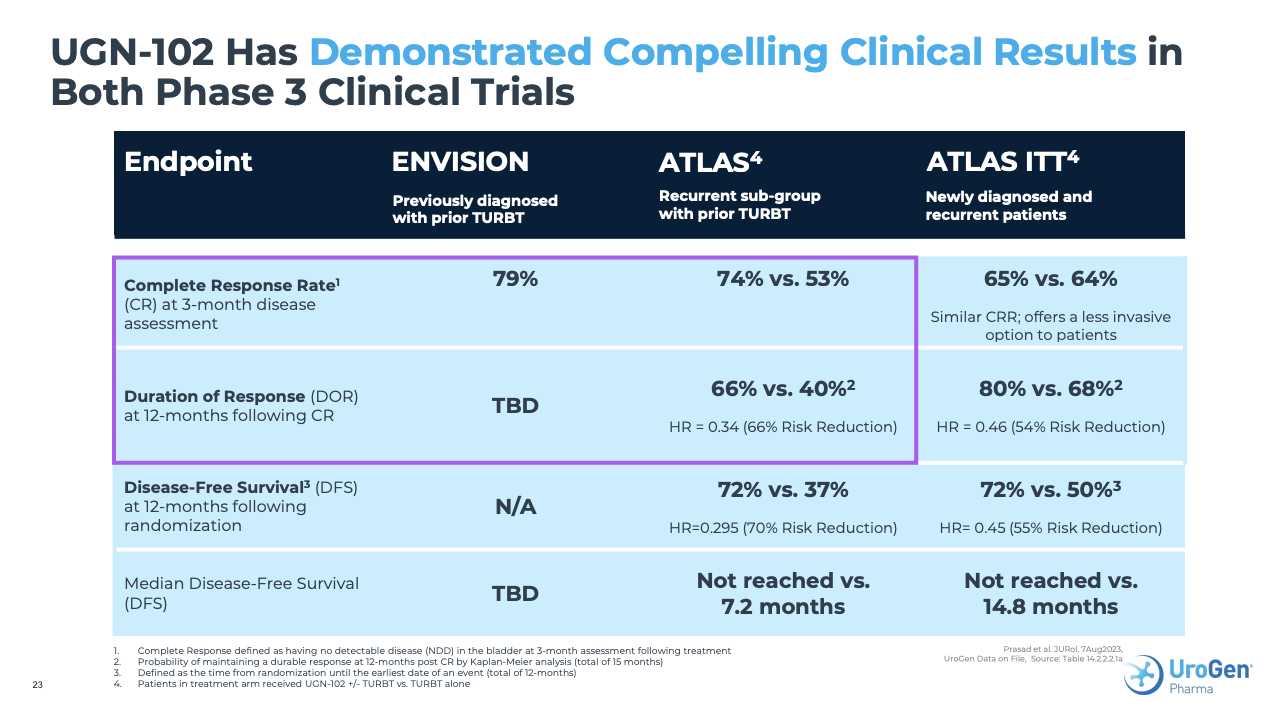

Slide 23 from the Presentation sets out the CR data that UroGen generated to date from its two phase 3 trials, ENVISION (NCT05243550) and ATLAS (NCT04688931):

investors.urogen.com

During the Call UroGen advised that it has developed its path forward with the FDA based on submission of DOR data from Envision during Q2, 2024. In response to a question during the Call CEO Barret explained why she had confidence that the FDA would grant priority review, including:

- the compelling nature of the CR data received to date;

- the high unmet need;

- JELMYTO received priority review.

During the Call CEO Barrett advised:

Assuming the data is as expected, we will complete submission of the NDA late in the third quarter. If granted priority review, we anticipate approval and launch of UGN-102 as early as the first quarter of 2025. The commercial opportunity in low-grade intermediate risk non-muscle invasive bladder cancer is significant.

She of course acknowledged that there could be no assurance that priority review would be available.

Conclusion

UroGen has an exciting story to tell so long as everything falls in line for UGN-102. If there is any slippage in this regard its story may still be exciting but less of a positive type of excitement.

Those interested in this name will be attuned to its ENVISION DOR data expected for release in Q2, 2024. Assuming positive data the next point to watch for will be an FDA submission late in Q3, 2024. Next will be the FDA's response to UroGen's NDA; did it accept the filing and grant priority review?