Maksim Safaniuk/iStock Editorial via Getty Images

Investment Thesis

I currently see Deere & Company (NYSE:DE) as a hold on the basis that the business is cyclical and it seems as though the cyclicity has not been fully priced in. My valuation predicts an annual return of 9.5% moving forward, therefore I do not see a margin of safety at the moment. On the flip side, in the long term, Deere will do well fundamentally as they will benefit from long-term growth within the agricultural and construction industries. Deere also has a unique opportunity to invest in R&D to drive innovation within the areas of autonomy, machine intelligence and guidance, which will increase productivity on agricultural and construction sites. In the long term, DE should be able to gain a technological advantage due to the scale in which they can invest in R&D, which may lead to industry consolidation and future pricing power.

Company Overview

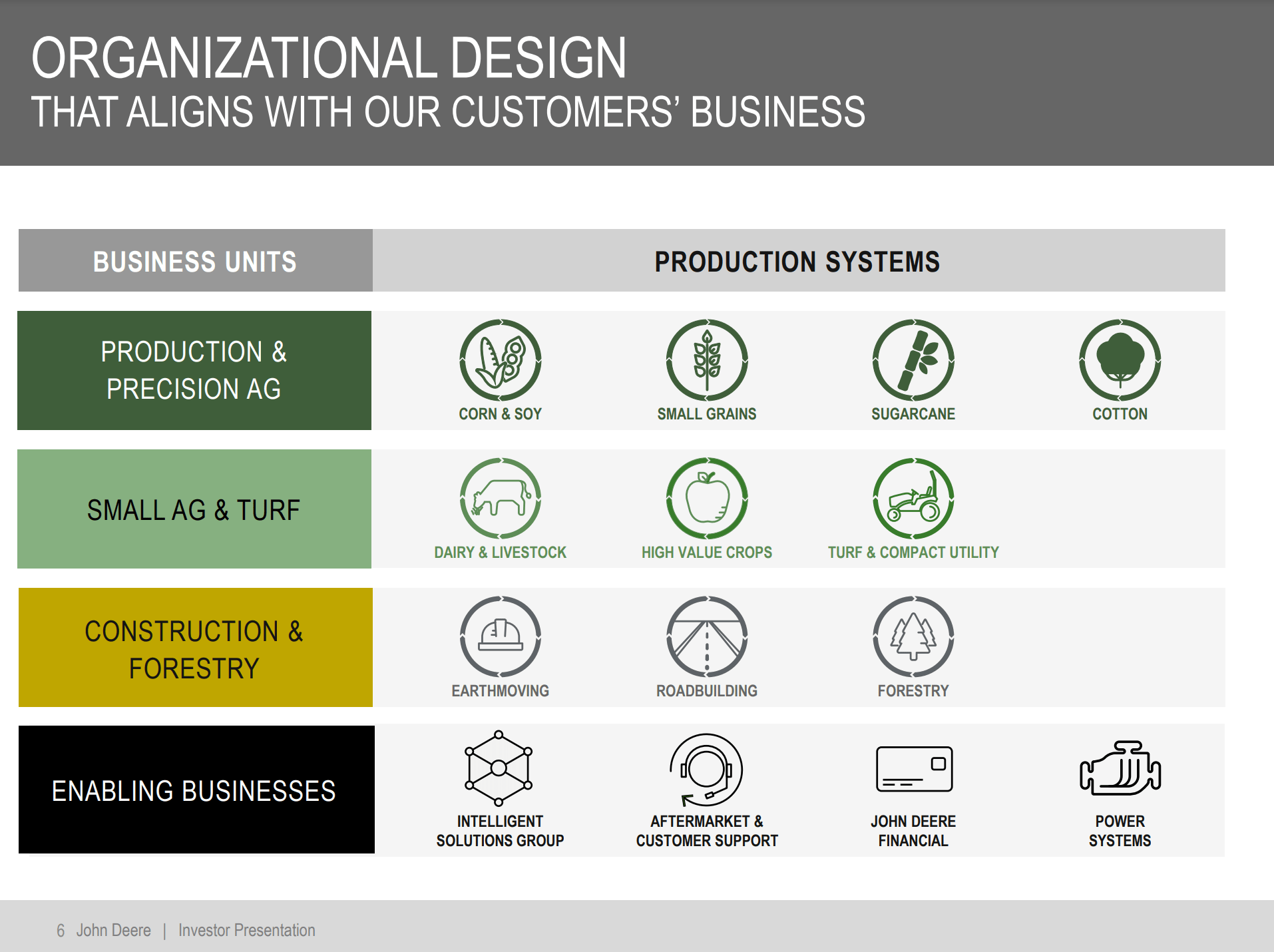

Deere & Company more known as John Deere is one of the leading providers of machines that are used for agriculture, construction and forestry. John Deere has four key business segments being production and precision agriculture, small agriculture/turf, construction and forestry and the enabling businesses segment that focuses on customer support and financing. Deere is in competition with other heavy machinery businesses such as Caterpillar (CAT), CNH Industrial (CNHI) and AGCO Corp. (AGCO) where all three operate in similar geographic markets with a focus on agricultural, construction and forestry machinery.

DE Investor Presentation 2023

The Agricultural Machinery Market Has Runway

Deere should be able to take advantage of an agricultural machinery market that should experience a long runway of sustainable growth. The agricultural machinery market going out until 2032 is expected to grow at a compounded annual growth rate of 5.1% where by 2032 the total addressable market should be close to $297.86 billion.

Precedence Research

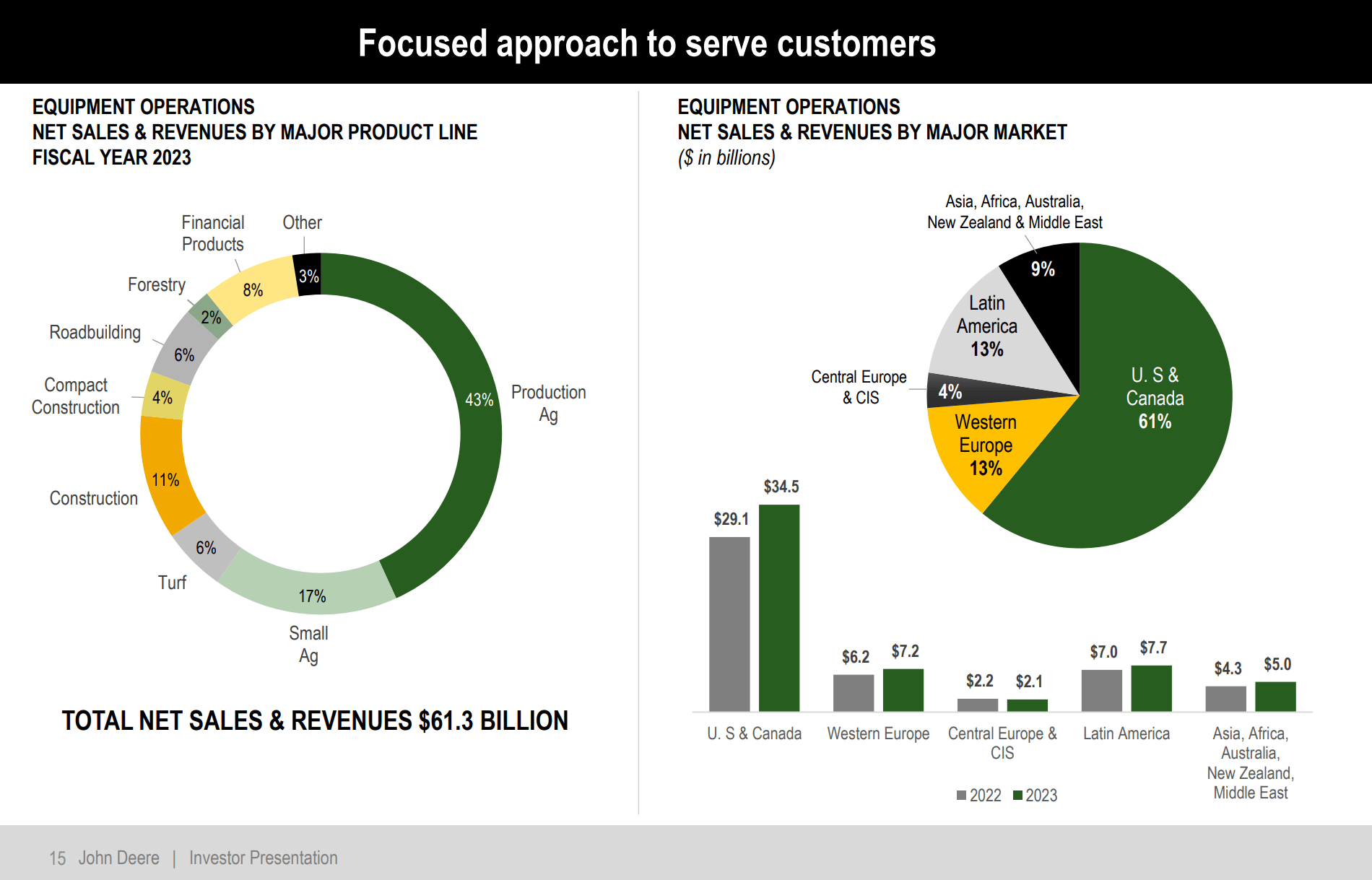

John Deere in my opinion looks like it is well positioned to benefit from this tailwind as currently, agricultural machinery makes up the largest portion of its business where production agriculture and small agriculture contribute 43% and 17% of the revenue, respectively.

DE Investor Presentation 2023

As we see the world population continues to increase and the demand for food continues to increase, more agricultural production will be required, and hence more machinery will also be required to sustain the increased demand. Furthermore, based on the graph above, the business is well diversified across the globe, which helps protect the business from geopolitical risk. While agriculture is the biggest part of the pie, I expect to see the construction, compact construction and roadbuilding segments to also grow at a similar pace since as the global population grows this will also call for more public infrastructure such as roads, bridges, airports, etc. Therefore, Deere should also benefit from this aspect.

Deere Investing Into Automation Technologies

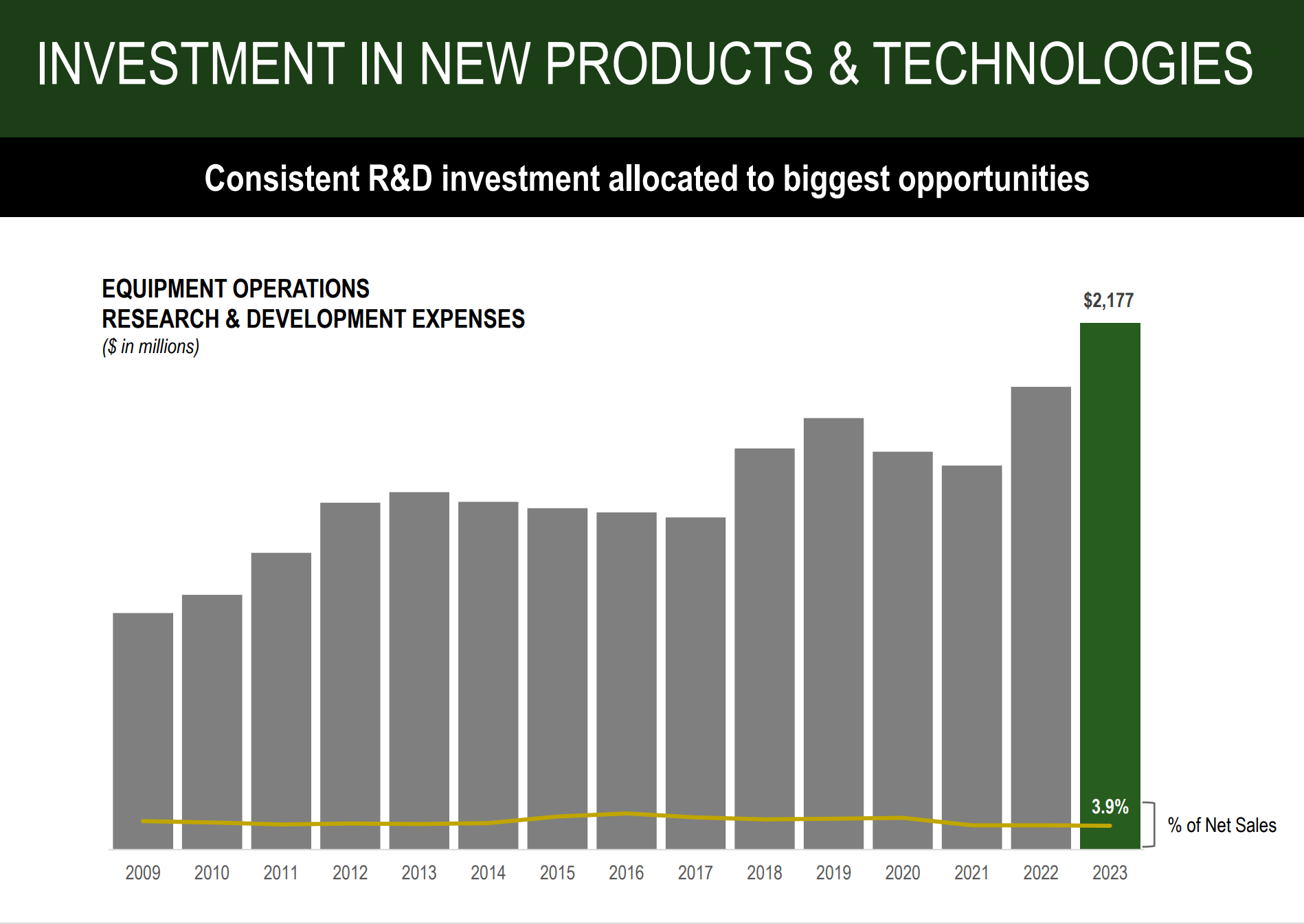

I think over the next decade a key theme within the agricultural and construction machinery industry will be automation. In order to stay relevant, each company within the space will need to invest in research and development to ensure that they do not fall behind in terms of technology. With the rise of AI, I believe agricultural and construction machinery companies will be keen on implementing such technologies into their machines - the technologies will save customers time and money. As we can see below, Deere reinvested $2.177 billion into research and development in 2023.

DE Investor Presentation 2023

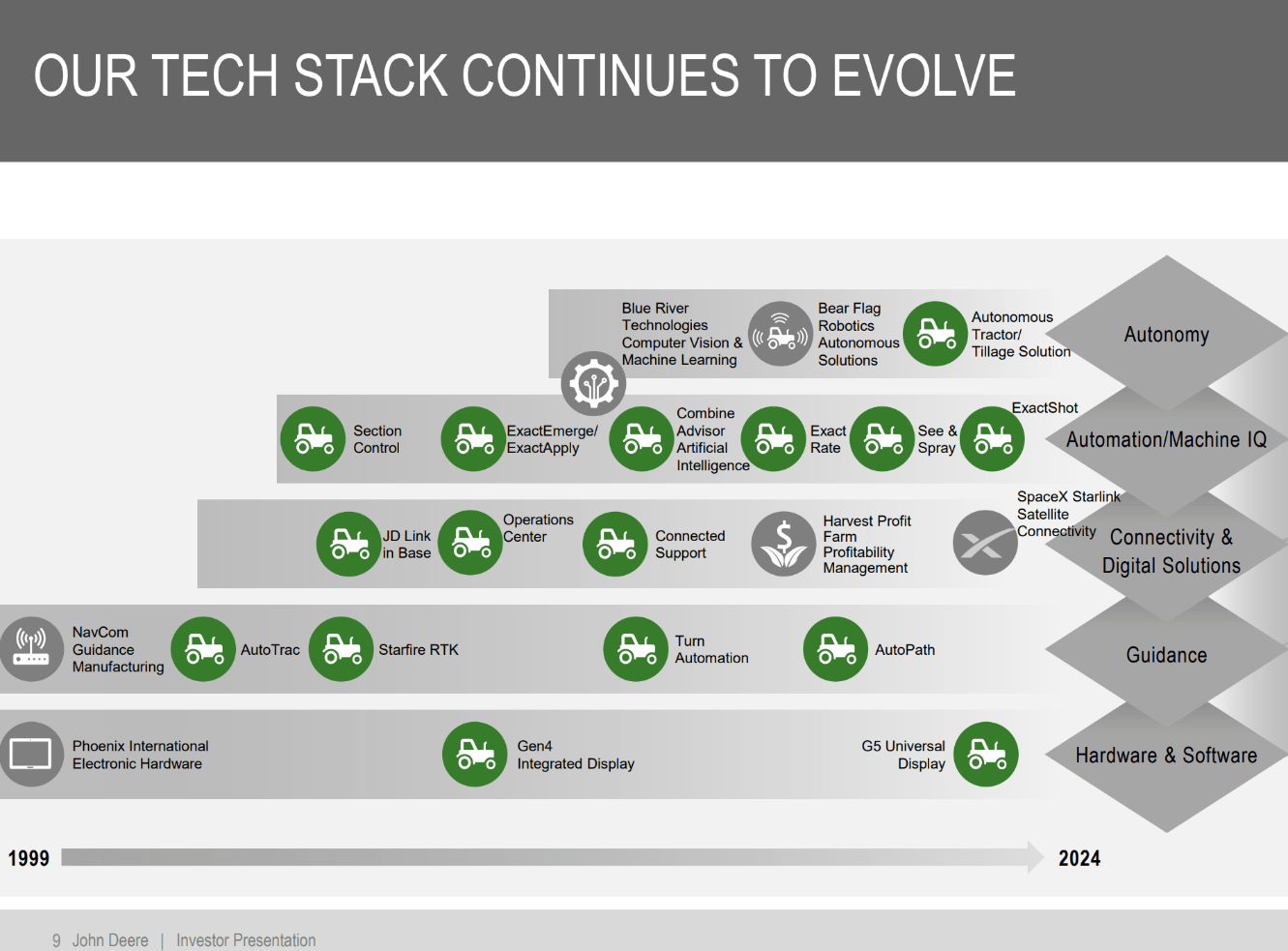

This investment is funneled into developing further technologies such as improved autonomy, better machine intelligence, and more superior guidance systems for the machinery. The improvement of these technologies will ultimately increase productivity on agricultural and construction sites, hence improving profitability and safety. An example of these technologies is the Fully Autonomous Tractor and Tillage that Deere has made available. This particular tractor allows for driverless operations, hence meaning the machine can work nearly 24/7 and without the need to pay for an operator. This then increases the productivity and profitability for agricultural clients of Deere.

DE Investor Presentation 2023

It would be my bet that in the long term, the rise of these technologies will further consolidate the industry as smaller companies that cannot spend as much on R&D will eventually fall behind and become redundant. This should allow the big players such as John Deere to gain further market share and should strengthen their competitive advantage as they should eventually keep IP that smaller players simply will not be able to attain due to their scale. This will then lead to increased pricing power as the landscape will become less competitive as only a few large players will hold the technology that the market demands.

Financial Analysis

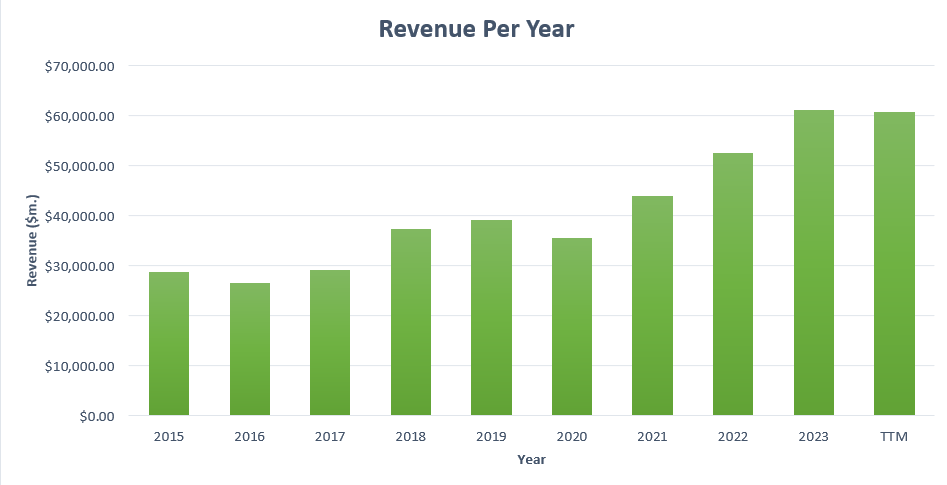

Deere is definitely a cyclical business that is dependent on the upswings and downswings in the agricultural and construction industries. However, if you look at the bigger picture you can see that the business is fundamentally improving financially in each up cycle and each down cycle. We have seen revenue rise from $28,780.80 million in 2015 to $60,755.00 million in the last 12 months which is a solid CAGR of 8.8%.

Created by Author

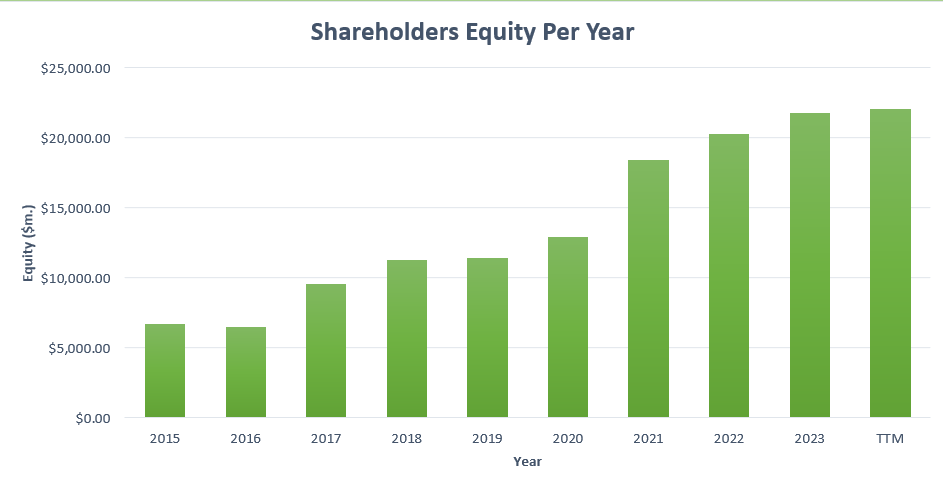

The company's shareholder equity has also seen a steady increase, moving from $6,743.40 million to $22,075.00 in the LTM, this is a CAGR of 14.1% showing that the underlying intrinsic value of the business has increased.

Created by Author

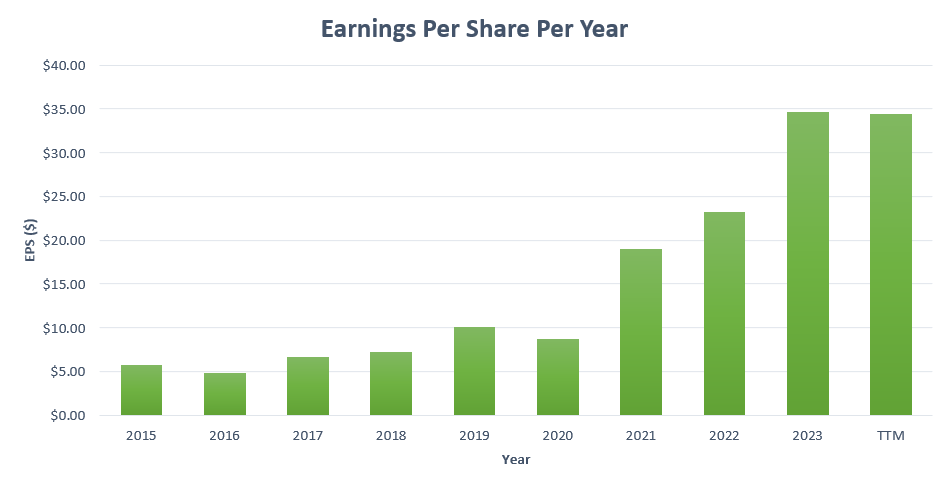

The EPS has definitely had some swings in the past decade; however the overall trend has most certainly been up as seen in the graph below. Through the decade EPS has increased considerably, growing at a CAGR of nearly 22% per year. It's important to consider since 2021, the company has experienced some standout years. In 2024 it is expected that revenue and consequently EPS will decline driven by a cyclical slowdown in the agricultural and construction industries.

Created by Author

When looking at the balance sheet, the company's total debt is $7,215.00 million, however this is easily covered by about two years’ worth of DE’s current free cash flow. They also have $3,828.00 million worth of cash and cash equivalents on the balance sheet as a cushion.

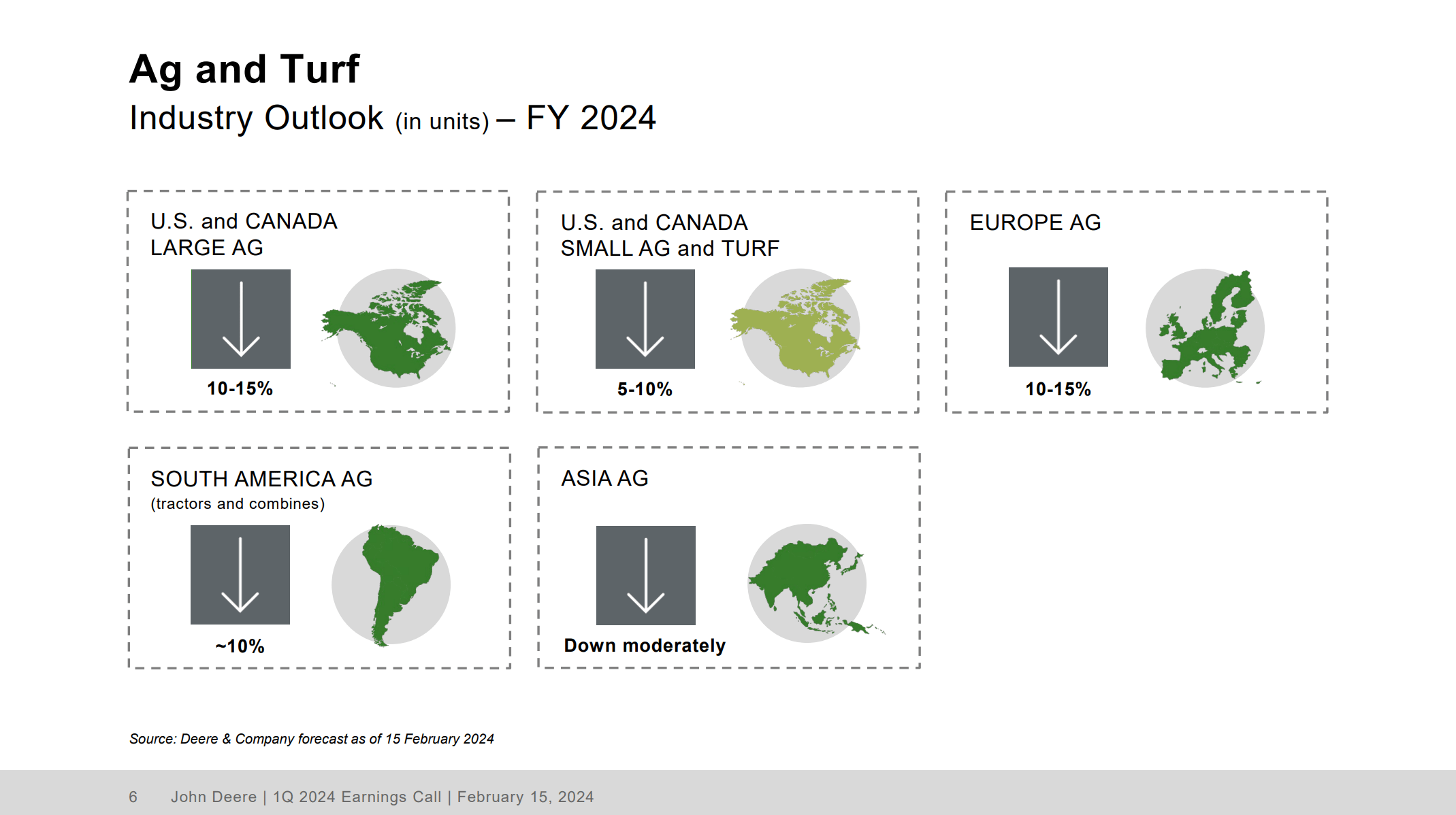

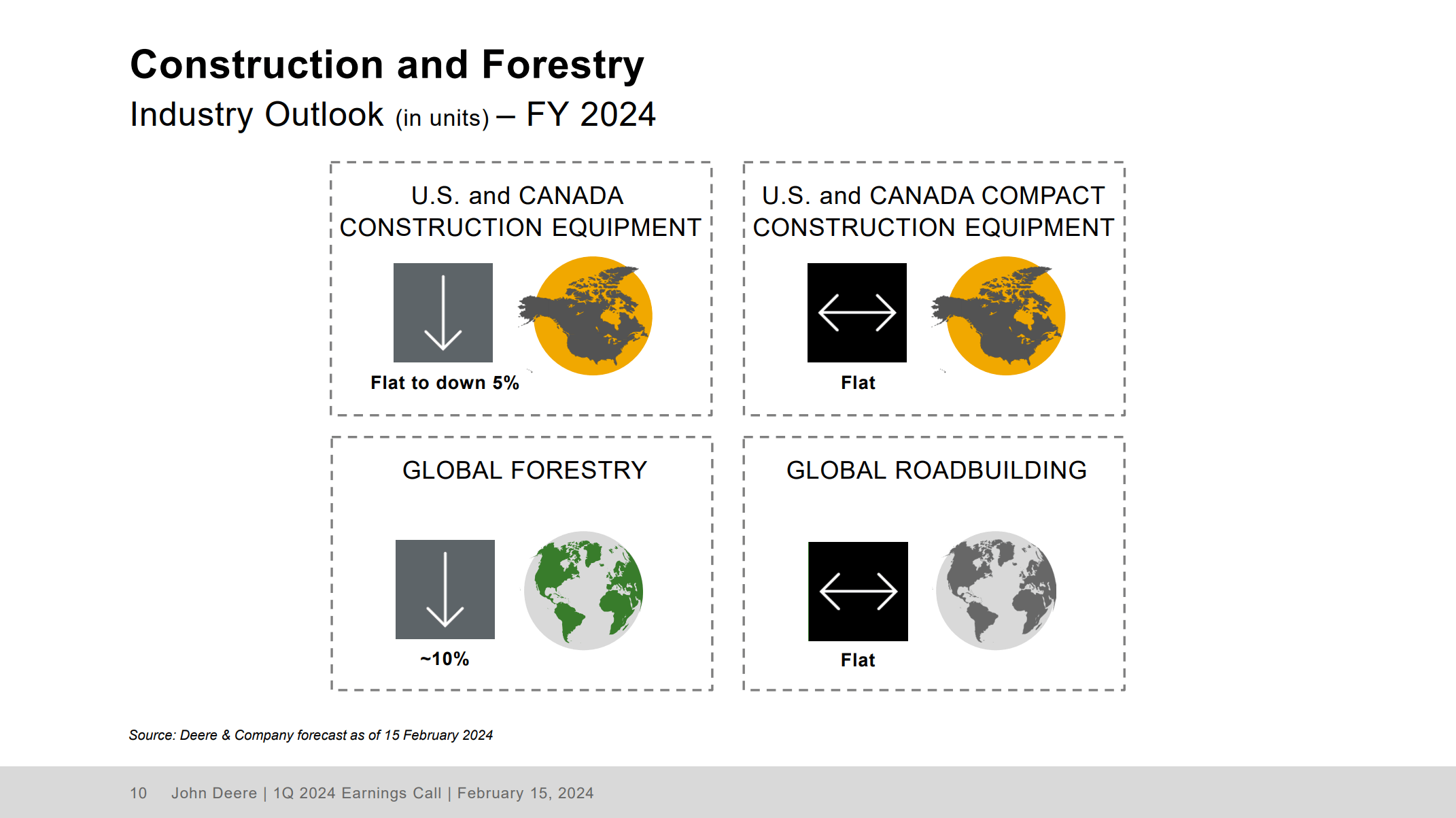

Moving forward I see the biggest risk to investors being an economic slowdown which seems to be playing out at the moment. We can see management is guiding weakening demand across global markets within the agriculture and turfing segment where U.S. and Canada, the biggest revenue region is expected to decline 10-15%. In general, all regions will decline in FY2024, including Europe, South America and Asia.

DE Q4 2023 Earnings Presentation

It is also the same story within the construction industry where all segments despite geographic region is expected to be flat or to decline this year. If you want to invest in Deere, you must understand the cyclicality of the business and try to use it to your advantage by trying to purchase the stock if it gets beaten down in a downturn as this is what can lead to outsized returns.

DE Q4 2023 Earnings Presentation

Valuation

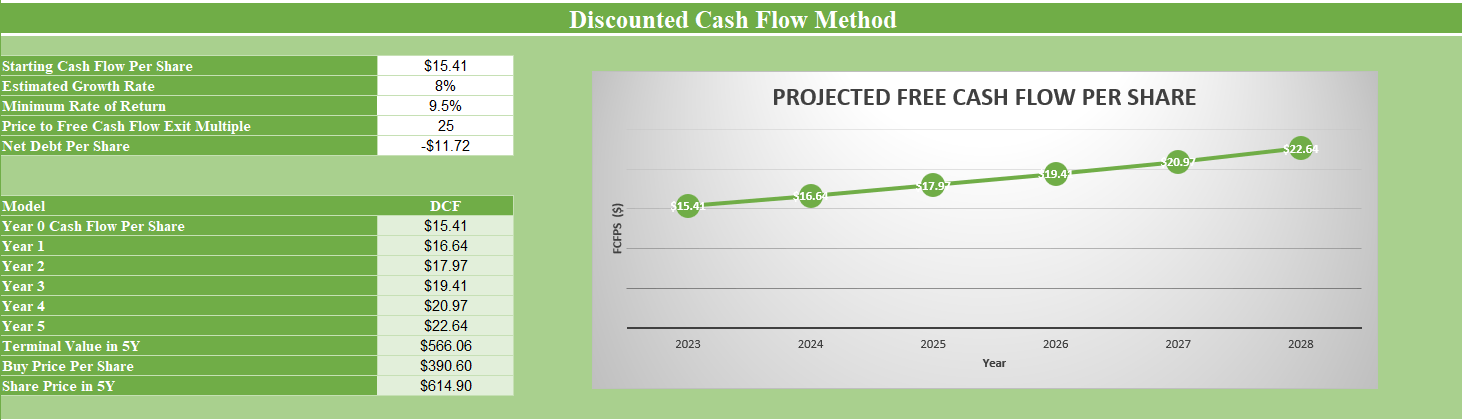

As of Q4, 2023, DE's current TTM free cash flow per share is $15.41. Given the growth expected in the agricultural and construction industry, I anticipate a conservative long-term annual growth rate of 8% for DE's TTM free cash flow per share over the next five years. Taking this growth into account, the projected TTM free cash flow per share for DE by Q4 2028 would be $22.64.

Using an exit multiple of 25, which I see as conservative as it is much less than DE’s historical price to free cash flow ratio, the estimated price target for the stock in five years would be $614.90. Therefore, if you invest in DE at its current share price of $391.51, the expected Compound Annual Growth Rate would be 9.5% over the next five years, based on these calculations.

Created by Author

Therefore, I see DE as a hold as I prefer to see an annual rate of return of at least 15% so that I can buy with a margin of safety. I think a margin of safety in this case is quite important due to the cyclicality of the industries in which DE operates.

Conclusion

Let me make it clear, I think Deere is a great business and the underlying fundamentals of the business will continue to improve in the long term. However, due to negative short-term guidance that I feel hasn’t fully been priced in, I see this stock as a hold. While my valuation estimates an annual return of 9.5% per year over the next five years, I cannot justify a purchase knowing that there is a risk that investors are still too optimistic about the stock. Therefore, for now, I will keep DE on my watchlist and continue to follow the stock. If things get ugly and the stock price drops considerably, expect a follow-up article and possibly a buy rating.