sanfel/iStock Editorial via Getty Images

Introduction

In my previous article, I had a hold rating on Royal Caribbean (NYSE:RCL). My reasoning at the time primarily revolved around the potential macroeconomic headwind Royal Caribbean may face in 2024. The travel industry is cyclical as consumers often cut discretionary spending in times of tough or uncertain financial environment; thus, as the consumer loan delinquencies were showing strong signs of increase, I believed it to adversely affect Royal Caribbean's business due to weakening consumers' financial health. However, recent data points are showing that my previous thesis was likely wrong. The US economy is moving towards a soft landing. At the same time, the rise in loan delinquencies is seen as a normalization phase after the abnormally low delinquency periods during the pandemic times, and despite my initial macroeconomic concern, Royal Caribbean reported strong financial results with even stronger guidance. Finally, as a result of strong operations, Royal Caribbean's financial leverage is quickly improving with an expectation for this to continue for the foreseeable future. Therefore, I believe Royal Caribbean is a buy. I may have been wrong to rate the company as a hold.

Likely Overblown Macroeconomic Concern

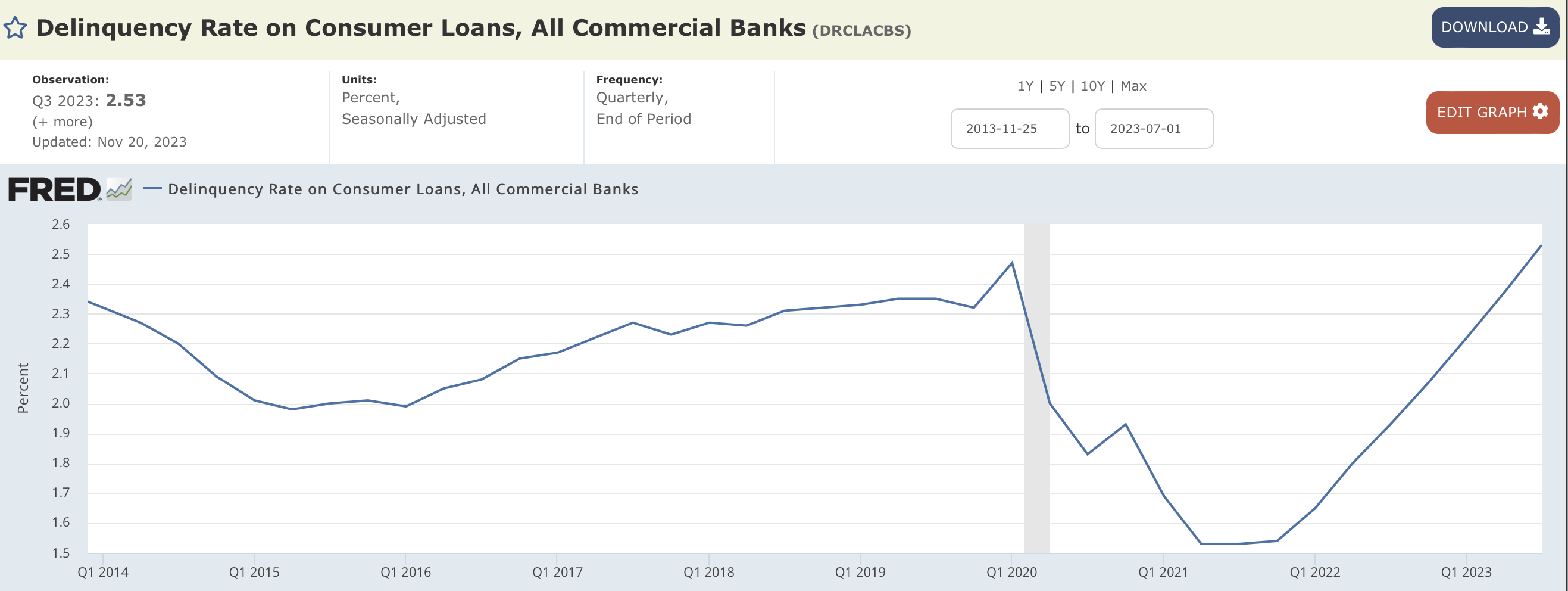

As the chart below shows, consumer loan delinquency rates in the US have been seeing a sharp increase in the past few quarters following the record low rates during the peak of the pandemic due to fiscal and monetary support. As this figure surpassed the pre-pandemic times with no clear indication of a slowdown, I believed it to signal a weakening of the US consumers' financial health potentially impacting cyclical sectors like Royal Caribbean's cruise industry. However, this thesis was likely not the case.

St. Louis Federal Reserve

[Source]

Economic data and viewpoints point to a strong US economy heading towards a soft landing, which would mean that there likely will not be a major macroeconomic headwind impending for Royal Caribbean.

Numerous economists and firms are expecting a soft landing of the US economy. Soft landing, in this context, is a continued robust economic growth just at a slower pace. One such firm is Morgan Stanley (MS). The company is seeing robust growth at a slower pace and an expectation for continued growth in corporate profits supporting the US economy.

I also agree with the economic soft landing thesis. The US economy's strength is showcased through numerous economic data. The unemployment rate, according to the US Bureau of Labor Statistics, was 3.9% in February. Compared to February 2023, the unemployment rate of 3.6%, there was no material increase in unemployment to argue that the labor market is deteriorating. The current rate is healthy. Further, PCE, personal consumption expenditure, and index data show that US consumers continue to spend at an accelerated level. In January, the PCE index increased 2.4% year-over-year logging strong growth.

Considering that the US is a service-based economy, I believe these figures to be significant. A strong labor market will continue to allow consumers to feel confident in their economic situation leading to continued elevated levels in spending. As there are no clear signs of the US labor market deteriorating, the spending will likely be strong for the foreseeable future.

Therefore, as the economy is expecting a soft landing from a robust job market and consumer spending, the potential macroeconomic headwind for Royal Caribbean will likely not be a potential risk to investors. It is highly unlikely for the company to face an impending macroeconomic risk for the foreseeable future.

Royal Caribbean's Performance and Guidance

Royal Caribbean's 2023Q4 earnings report showcased an extremely strong performance and guidance.

The company reported a 2023Q4 revenue growth of about 27.92% year-over-year to $3.331 billion from $2.604 billion. Beyond the robust top-line growth, the company's operating income increased from $15 million in 2022Q4 to $570 million in 2023Q4 as the cruise industry returned to normal operations. Royal Caribbean achieved these growths even as the company maintained a 105% load factor and a fleet growth of 9.1% year-over-year.

Royal Caribbean's guidance was also strong. Going into 2024, the management team said that "the company is very encouraged about the demand and pricing environment" because "the five best booking weeks of the company's history have occurred since the last earnings call" leading to "a record booked position in both rate and volume." As a result, for the full year 2024, the company is expecting net yields to increase 5.25% year-over-year with an adjusted EBITDA growth of about 40%.

Overall, Royal Caribbean has reported and is expected to report strong earnings in 2024 according to the company's financial report.

Strength to Likely Continue

The strength in current operations and guidance Royal Caribbean has reported will likely continue. Royal Caribbean is an industry leader in cruising innovation attracting customers, and for this reason, I believe the ambitious guidance is reasonable.

In early 2024, Royal Caribbean started the sailing of the Icon of the Seas cruise ship. The Icon of the Seas is not only the world's largest cruise ship with 7 swimming pools, 20 decks, neighborhoods, entertainment, shopping, etc., but the cruise ship is a $2 billion icon.

Icon of the Seas is a sailing marketing machine. It has natural media attention for being the biggest cruise ship and a sailing entertainment city. To some extent, it could be argued that the Icon of the Seas is viewed as the pinnacle of cruise travel, and I think this is extremely valuable.

Tesla (TSLA) started with the production of premium vehicles before mass-producing more affordable options. To this day, the company's brand image is aligned with premium. On the other hand, Hyundai launched in the US with a mass-produced affordable vehicle. Today, Genesis, a premium brand, does not have the image of luxury to the vast number of consumers like other industry peers' premium brands.

Many investors may not agree with my analogy; however, my argument is that Icon of the Seas can elevate the Royal Caribbean's brand image to new heights increasing the demand and brand image of the rest of the Royal Caribbean's fleet because the excitement, awe, and longing for the largest cruise ship could translate to an overall positive image of the Royal Caribbean. This is the case because consumers will likely associate Royal Caribbean as the company that operates the pinnacle of cruise vacation or the biggest cruise ship, which is a positive and likely a demand driver for the company.

Therefore, Royal Caribbean, being an innovator in pushing the new heights of cruise entertainment, may benefit from improving consumers' view of the company.

Valuation

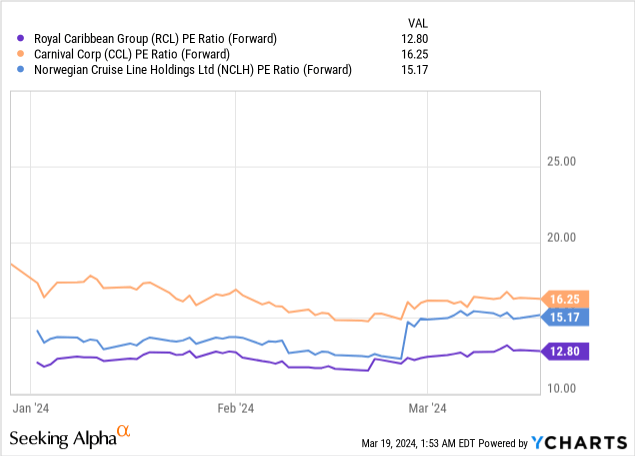

Royal Caribbean is likely undervalued. The company's forward price-to-earnings multiple is far lower than Royal Caribbean's industry peers: Carnival Corporation (CCL) and Norwegian Cruise Line (NCLH). The lower valuation multiple comes despite Royal Caribbean boasting greater EBITDA margin and revenue growth expectations.

As the chart above shows, Royal Caribbean has a forward price-to-earnings ratio of 12.80, which is far lower than its industry peers. Carnival and Norwegian Cruise Lines have 16.25 and 15.17 forward price-to-earnings, respectively.

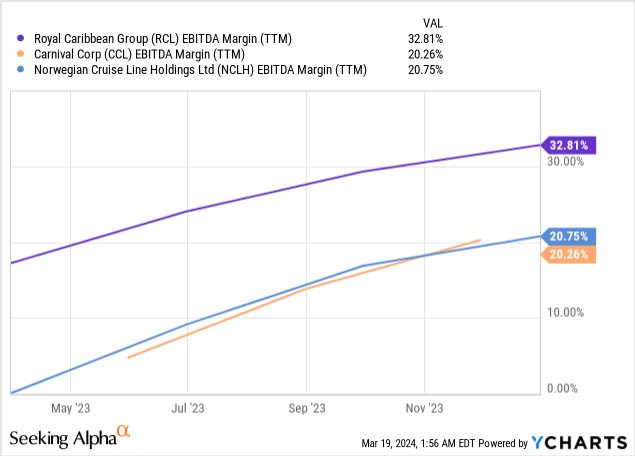

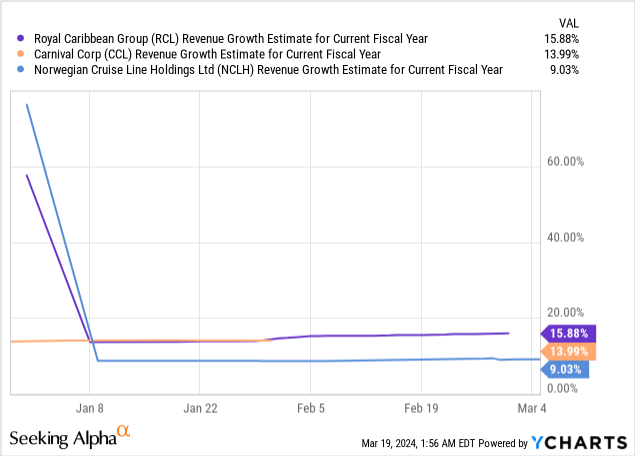

However, although Royal Caribbean has a lower valuation multiple, the company boasts a greater margin and growth rate expectation. As the charts below show, Royal Caribbean has a TTM EBITDA margin of 32.81%, which is more than 50% higher than that of the company's competitors. Carnival and Norwegian Cruise Lines have a TTM EBITDA margin of 20.26% and 20.75%, respectively. Further, Royal Caribbean's current fiscal year revenue growth rate expectation is highest at 15.88% compared to Carnival Cruise Line's at 13.99% and Norwegian Cruise Line's at 9.03%.

Therefore, I believe Royal Caribbean is undervalued. The company is trading at the lowest valuation multiple among its industry peers while boasting the highest margin and growth rate expectation.

Risk to Thesis

The US economy, as discussed earlier, continues to be strong with an expectation for the current strength to continue for the foreseeable future. My conclusion was that investors will likely not have to worry about potentially impending macroeconomic headwinds. However, investors should closely monitor the consumer loan delinquency rates. The rise in delinquency rates did not have a profound effect on the Royal Caribbean's operations and guidance; however, if it is the case that the delinquency rates continue their upward movement at a similar or a greater magnitude for the coming few quarters, it could mean that the consumers' financial health is in serious deterioration phase. Therefore, while the delinquency rates are likely not an imminent threat, investors should continue monitoring the data in case it evolves into a potential headwind for Royal Caribbean.

Summary

Royal Caribbean is in a strong position. The company reported a strong 2023Q4 earnings report with strong guidance for 2024. The optimistic guidance is likely reasonable as the company is the innovation leader and likely an icon for the cruising public generating a positive image for future growth. Further, what was initially considered to be a potential macroeconomic headwind, increasing consumer loan delinquency rate, did not put a strain on the company's operations likely due to the strong US economy. Thus, the company will likely not experience any material macroeconomic headwind for the foreseeable future. Finally, Royal Caribbean is undervalued relative to its industry peers. Therefore, I believe Royal Caribbean is a buy.