Su Arslanoglu

Camden Property Trust (NYSE:CPT) anticipates lower Core funds from operations, or FFO, per share and flat same-property NOI due to weaker leasing spreads caused by increased apartment supply. Revenue growth is challenged by rising expenses, while leasing spreads decline ahead of NOI changes.

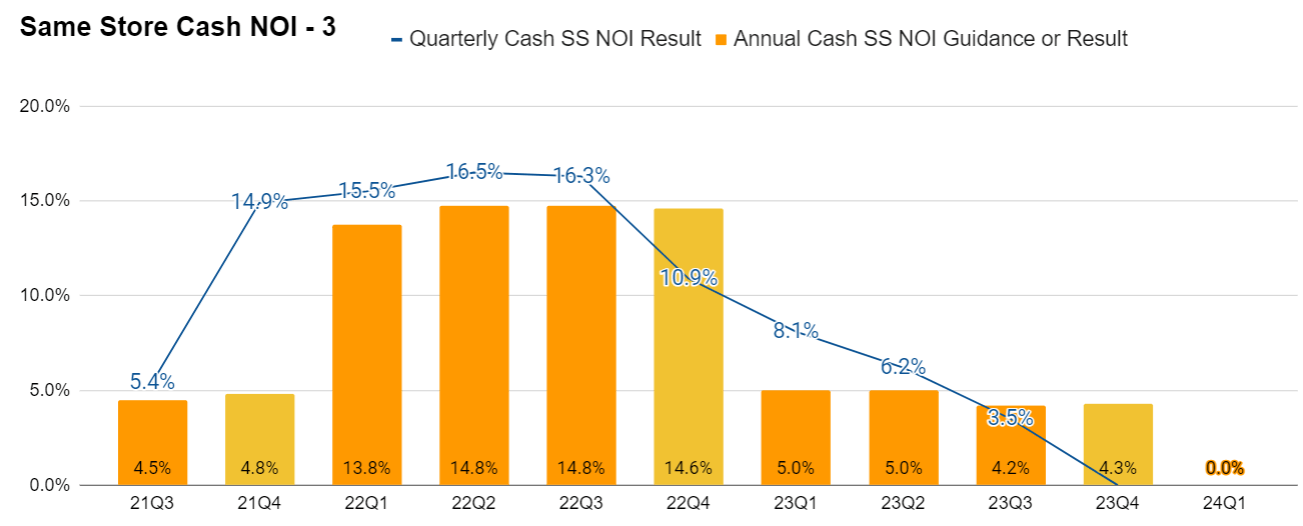

Same Property NOI

Let's take a look at same property NOI:

The REIT Forum

Notice how there’s a bit of a lag?

In 2021 Q3, the same property NOI wasn’t blistering yet. The leasing spreads were huge, but the same property NOI wasn’t hot yet.

In 2022, all the numbers were strong.

However, you can see that leasing spreads in Q3 and Q4 of 2022 were coming down much faster than the same property NOI.

That happens because leases renew throughout the year. Each time they lock in huge leasing spreads, it locks in much higher revenue on that apartment for the next year.

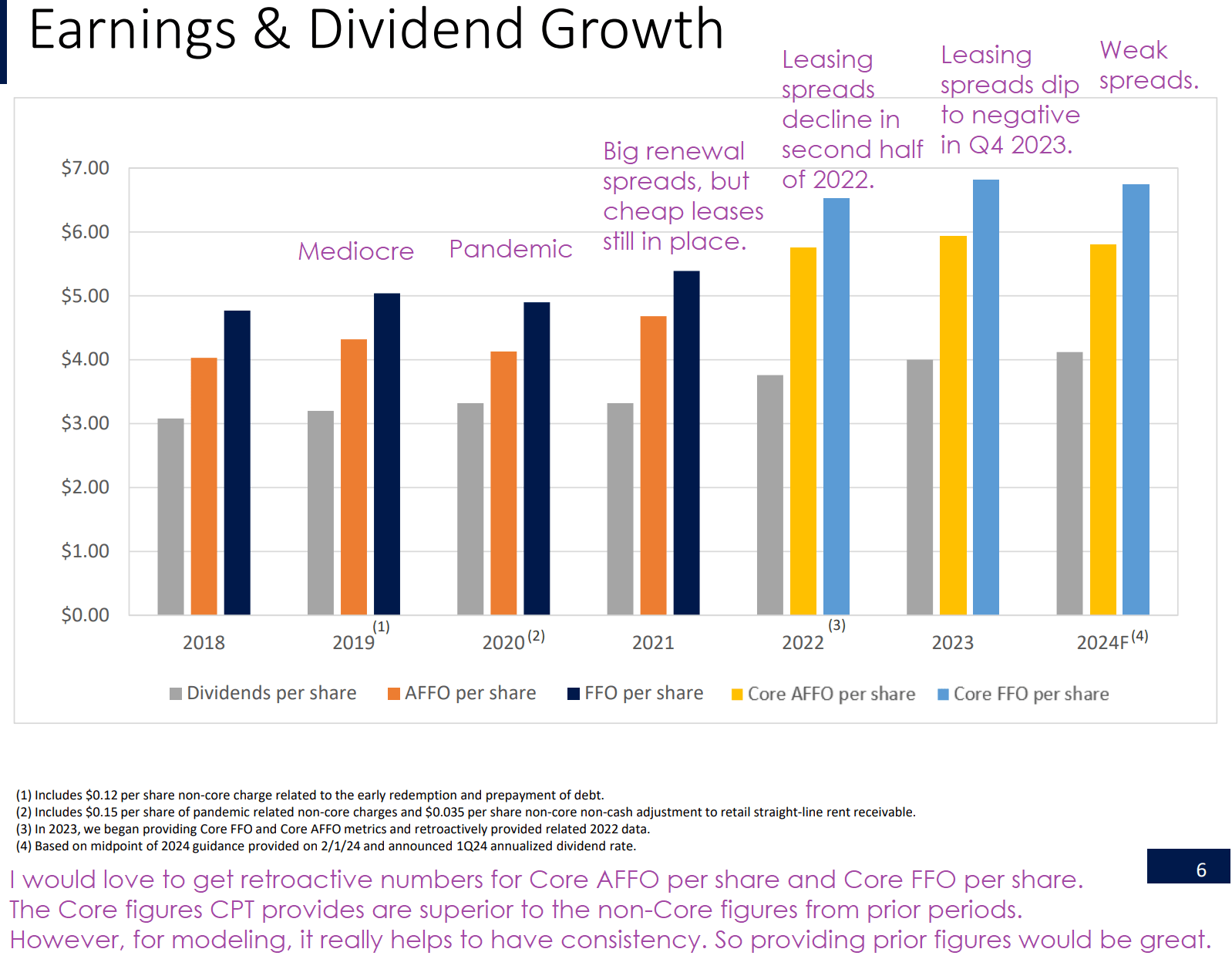

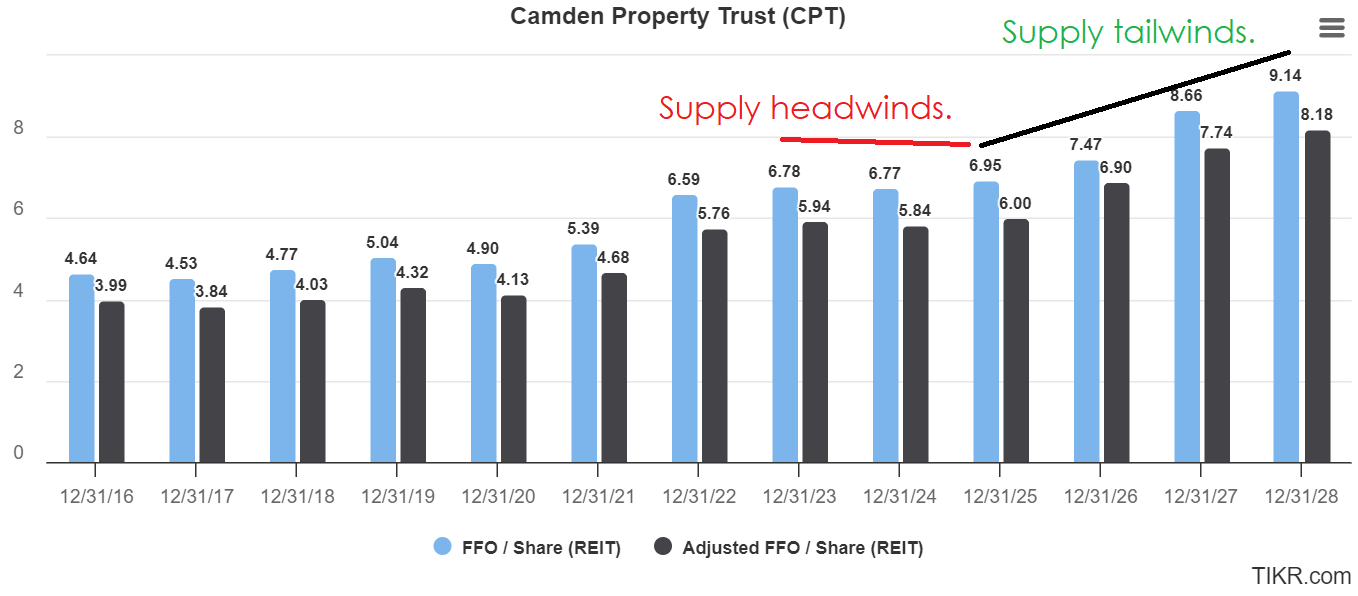

FFO Metrics Over Time

This next chart allows us to evaluate how FFO per share has changed over time.

CPT

We can’t get those metrics retroactively. However, the adjustments in Core FFO tend to be pretty small. I evaluated the adjustments and I agree with the adjustments CPT is making.

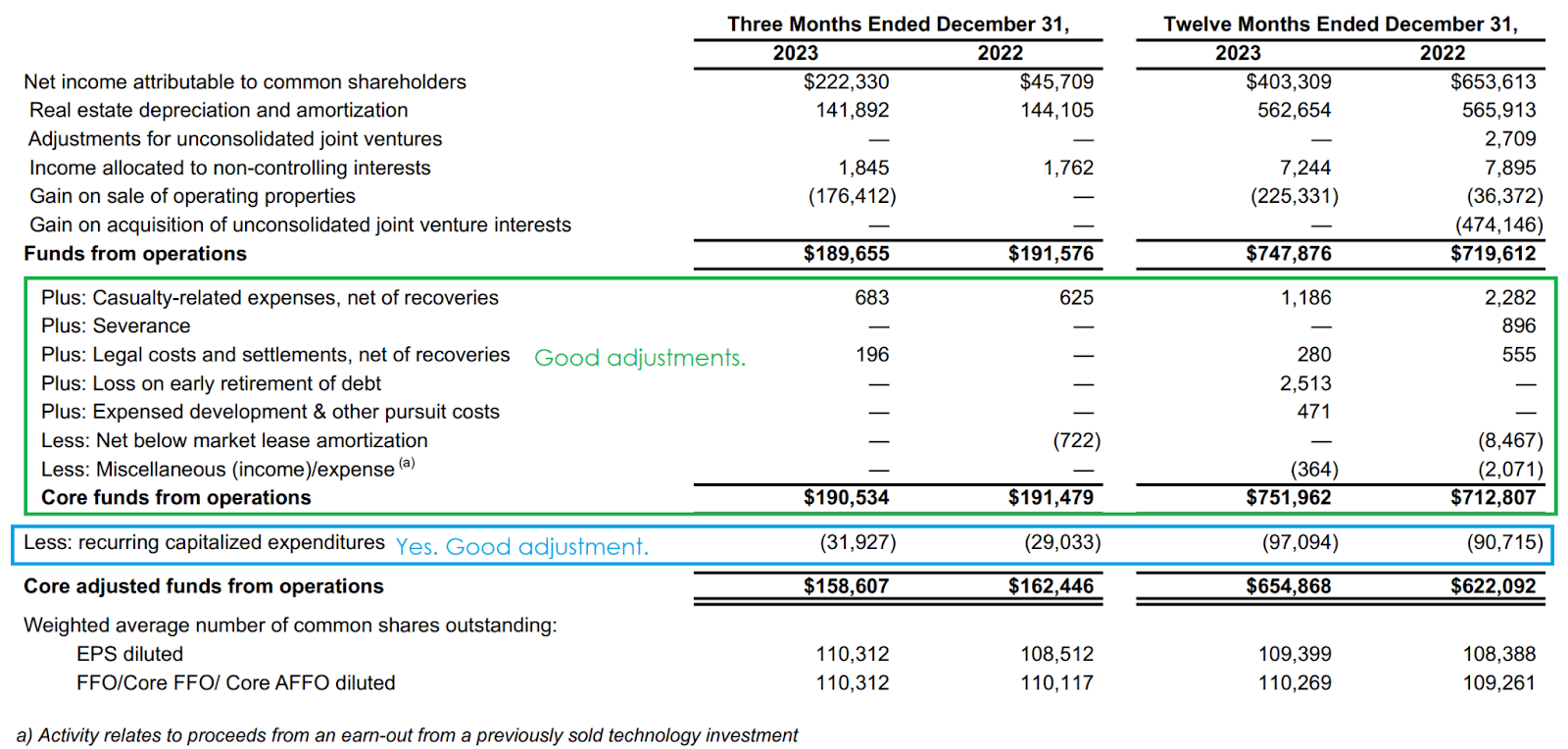

I pulled the figures to demonstrate:

CPT

Those adjustments to reach a “Core FFO” figure are appropriate.

Some REITs might put values like the “below market lease amortization” into the “AFFO” line instead. Either way is fine. It’s a good adjustment and they got it in there.

CPT correctly decided not to add back stock-based compensation or debt amortization costs, so there are no adjustments that I need to reverse.

This is a great metric to label as “Core AFFO.”

Interest Expense

With CPT guiding for slightly lower Core FFO per share, I was preparing for some minor interest expense headwinds. However, CPT’s guidance calls for interest expense to decline.

2023: Interest expenses: $133.4 million.

2024 guidance midpoint: $126 million.

That comes out to about $.067 per share.

It’s interesting to see a REIT guiding for lower interest expense in 2024.

We checked into that.

CPT forecasts a lower average debt balance for the year by $185 million. That alone should be able to reduce interest expenses by about the right amount.

Some investors might be concerned that the REIT would simply be capitalizing more interest. That isn’t the case. Projected capitalized interest is also down year-over-year.

Maturities in 2024 are $290 million (pretty small).

Maturities in 2025 are $0.

Overall, debt leverage is fairly low. Given CPT’s A- credit ratings, the weighted average rate of 4.2% is a bit higher than I would expect.

84.8% of debt was at fixed rates, so falling interest rates could provide a small tailwind. However, with minimal maturities, it shouldn’t be as important to CPT as it would be to some REITs.

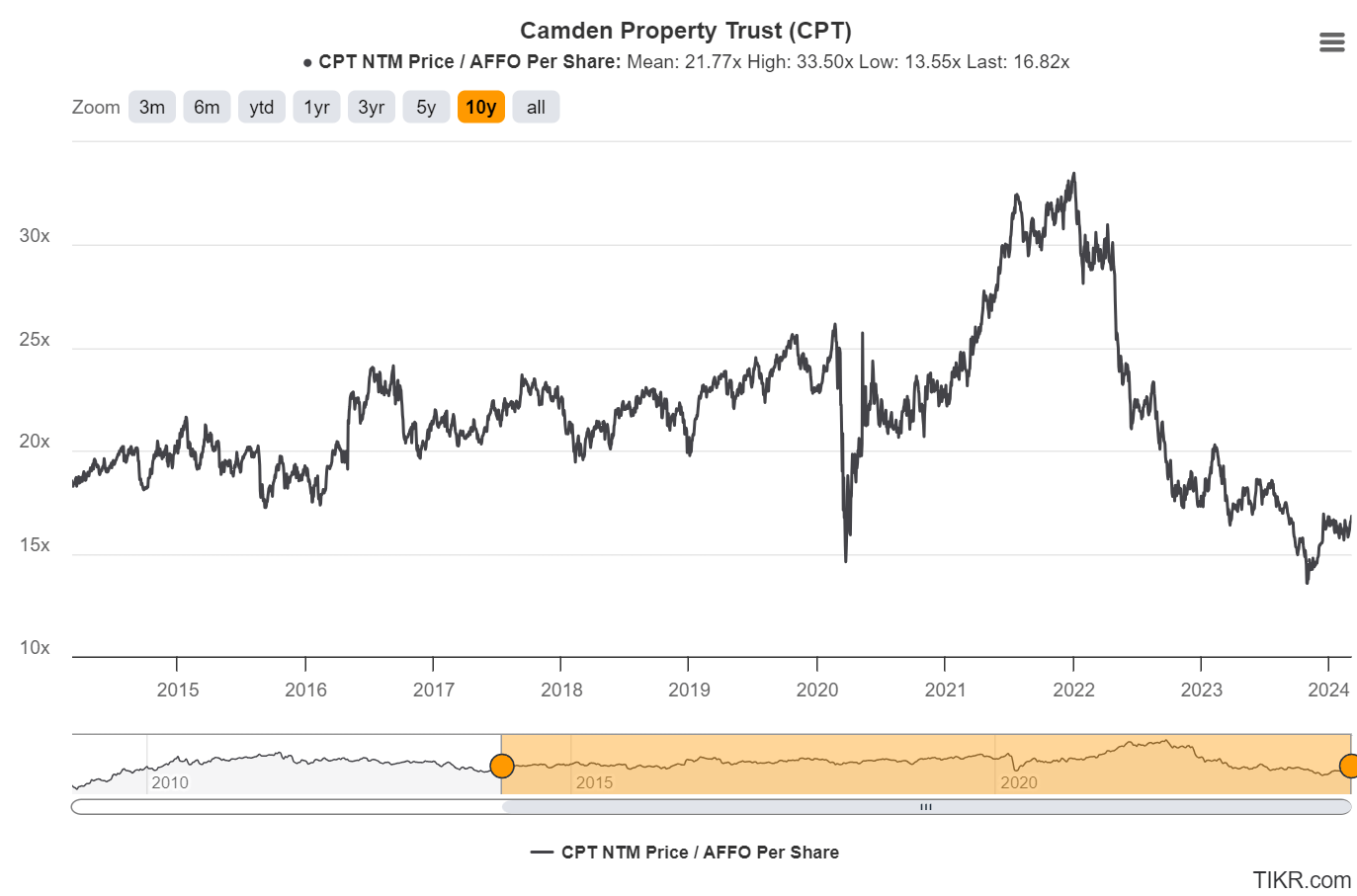

Valuation

Shares currently trade at $98.48 (written March 7th, 2024). That is 16.86x the consensus 2024 AFFO estimate (not Core FFO) of $5.84.

Note: CPT provides guidance on Core FFO, but did not provide guidance for Core AFFO.

TIKR

That’s much lower than the average multiple. Given the expectation for weak growth in 2025, that makes sense.

Analysts are catching on to the upcoming surge in supply and the consensus forecasts are reflecting it.

TIKR

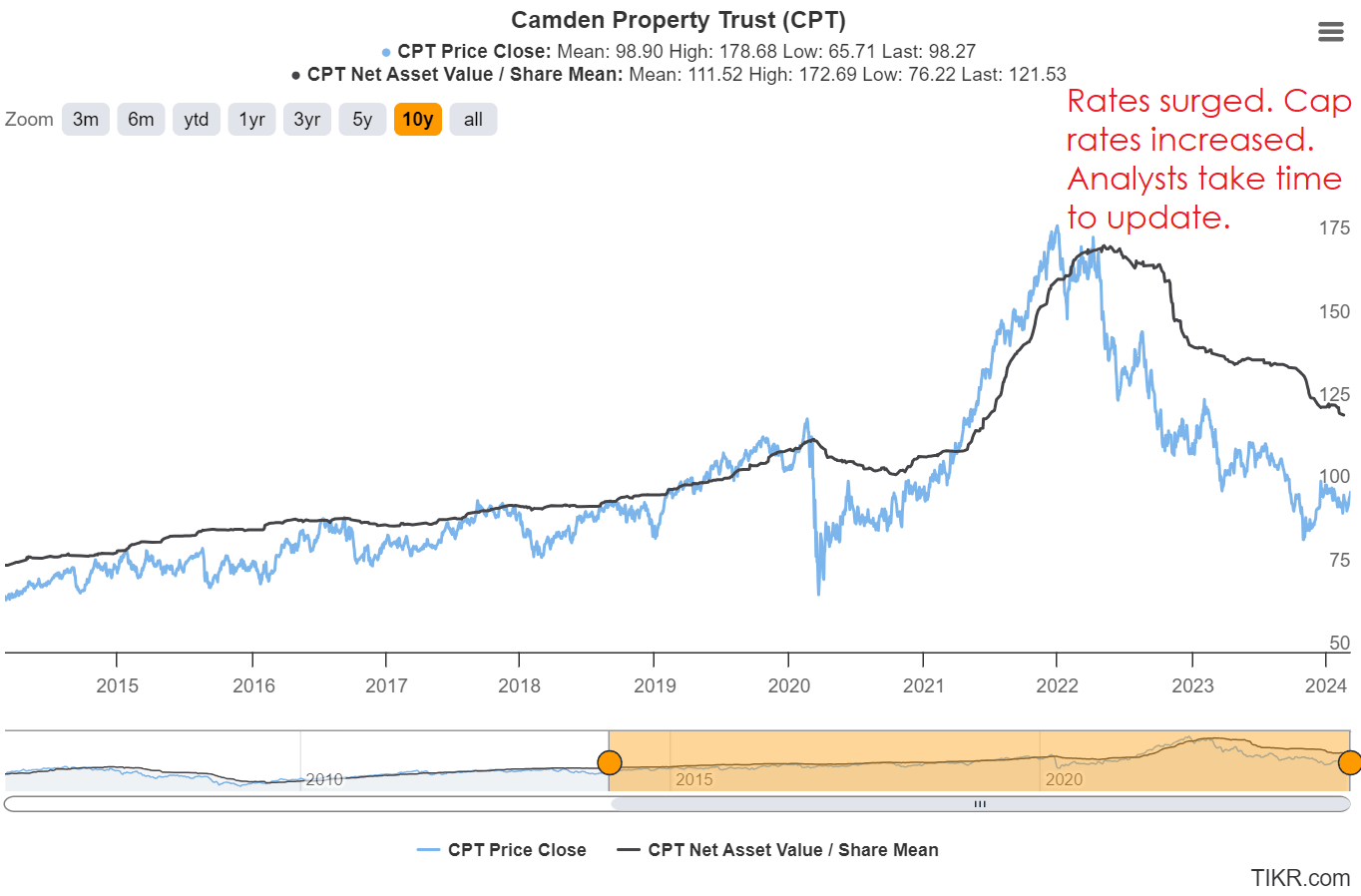

Finally, we can also look at the difference in share prices and consensus NAV estimates.

TIKR

For equity REITs, I find the share price often moves before the NAV. However, the NAV can still contribute to pulling the share price back up.

While Treasury yields soared, analysts were slow to update estimates for NAV. Then we saw an abrupt drop in NAV estimates several months later.

If interest rates stabilize (or decline), we may see NAV stabilizing soon as well. If that bears out, then the discount to NAV is unusually large and that’s pretty attractive. Positive catalysts are lower interest rates (could hit sooner) or a reduction in supply (takes years to play out).

Summary

Camden Property Trust faces headwinds from much weaker leasing spreads as new supply hits the market. We’re forecasting this headwind to last about 2 years.

The weaker leasing spreads should lead to same property net operating income running around 0%. The headwind might be a bit bigger in 2025 or it might be similar. Probably not a big improvement.

After 2025 (or perhaps even in late 2025), the headwind should decline rapidly and turn into a tailwind over the next 12 to 24 months.

We can make those projections based on the volume of apartments under construction and the expected completion periods.

Core FFO per share is projected to decline slightly in 2024. I’m expecting it to also be pretty weak in 2025. Whether it is up slightly or down slightly, I wouldn’t expect it to be substantially higher or lower.

Investors in CPT are looking at this as an opportunity to collect a 4.2% dividend yield while waiting for the supply picture to change and the growth rate to resume.

The dividend is easily covered by AFFO, so I have no concerns there. It’s simply a matter of waiting patiently.

There are two viable cases for a bull thesis:

Interest rates may decline leading to lower capitalization rates and improving NAV. Only a minimal impact to FFO and AFFO per share unless rates move significantly.

In a few years, the supply headwind turns into a supply tailwind as fewer units are started due to the higher cost of financing.

I see the second factor (supply) as the more certain story here and it is the second part that attracts me to the idea.

Because it takes so long to play out, I’m not in a rush to build the position. Instead, I’ve been leaning towards gradually working into apartment REIT positions.

Potential Target Adjustments

I’ll split it into a few factors:

Neutral: Results are largely in line with our expectations. So that favors keeping targets similar.

Positive: Relative to our prior update, interest rates are down. Higher interest rates drive more long-term revenue growth by reducing supply, but lower interest rates reduce interest expense, improve sentiment, and improve the dividend yield to bond yield comparison. Therefore, lower rates are generally going to be positive. This comes out as a net positive for targets.

Negative: On the other hand, we’re still looking at a fairly long-term thesis with no near-term positive catalysts expected (except potentially cutting rates). That makes it hard to justify material increases to targets. There is also a risk of negative sentiment as landlords nationally come under fire for antitrust violations from using software designed (in my opinion) to function as a tool for price fixing. Some other industries (like hotels) could also come under fire for price fixing.

Given that mix, I am inclined to expect target adjustments to be minimal. After we finish reviewing the apartment REITs, we’ll set the changes for targets. So far, it looks like those will be very small.

You should try our service. Unlike most services, our service is backed by a real portfolio. Not a "model" portfolio. Not hypothetical positions. Not 7 different portfolios we made up in Google Sheets so we can brag about the good one. None of that crap.

You get real-time alerts on every trade. See current and past positions. I'm sick of analysts who have to retroactively pick a "portfolio" or get creative about defining "returns". Beat the index or get out.

Ask your analyst to share their portfolio value each month so you can verify their returns. When they object, try us.