beckariuz

The premise of Decline was that it had a tripartite value proposition of:

- HEPLISAV-B revenues in growth mode;

- CpG 1018 adjuvant in stall mode of uncertain duration; and

- pipeline with no near term candidates.

These combined to support its market cap at the time of $1.92 billion with little margin for error. I hypothesized that it might take a rekindling of revenues from CpG 1018 to support a much higher market cap.

In this article I will report on its latest advice on each of these three following its 02/22/2024 Q4, 2023 earnings per its:

- press release (the "Release");

- earnings conference call (the "Call");

- presentation (the "Presentation"); and

- 10-K (the "10-K").

In this article I list my takeaways from the quarter, which include the fact that CpG 1018 is unlikely to rekindle as an independent revenue source. Dynavax investors should reconcile themselves to HEPLISAV-B as Dynavax's sole discernible source of significant revenue over the next several years. For these reasons as further discussed below I rate Dynavax a "Hold".

The Release reported good news with top and bottom line beats.

In terms of recent earnings, Dynavax was able to just skirt by; it beat Q4, 2023 EPS expectations by the thinnest of margins. It reported Q4, 2023 GAAP EPS of $0.00 beating modest expectations by $0.01. Its revenue of $55.6 million (-69.9% Y/Y) beat expectations by $2.87 million.

Dynavax advised that it was targeting positive cash flow for the year 2024. This was a big setback from its report for 2022 when CpG 1018 revenues gave Dynavax meaningful positive earnings with $0.45 EPS. CpG 1018's big runup during the pandemic followed by its current stall has violently disrupted Dynavax's revenue picture.

As matters now stand CpG 1018 is no longer viable as an independent source of revenue. It is still important in its role as adjuvant for HEPLISAV-B and Dynavax's developing pipeline assets.

During the Call Dynavax set out its forward strategy focused on maximizing HEPLISAV-B revenues and moving its pipeline ahead. This article does not review its pipeline which is unlikely to materially impact revenues over the next several years.

Dynavax's CpG 1018 adjuvant revenues have hit a brick wall.

In Dynavax's halcyon days COVID was running hot and it sold its CpG 1018 adjuvant to diverse vaccine companies around the world. During its Q4, 2022 earnings call CEO Spencer reported:

...throughout the pandemic, we delivered CpG 1018 adjuvant for nearly 1 billion COVID-19 vaccine doses across all five of our commercial supply partnerships, completing our obligations under our commercial supply agreement to support the pandemic response. Our efforts resulted in $588 million of revenue in 2022 and further validated the safety and efficacy of CpG 1018 adjuvant across a variety of protein-based vaccine platforms around the world.

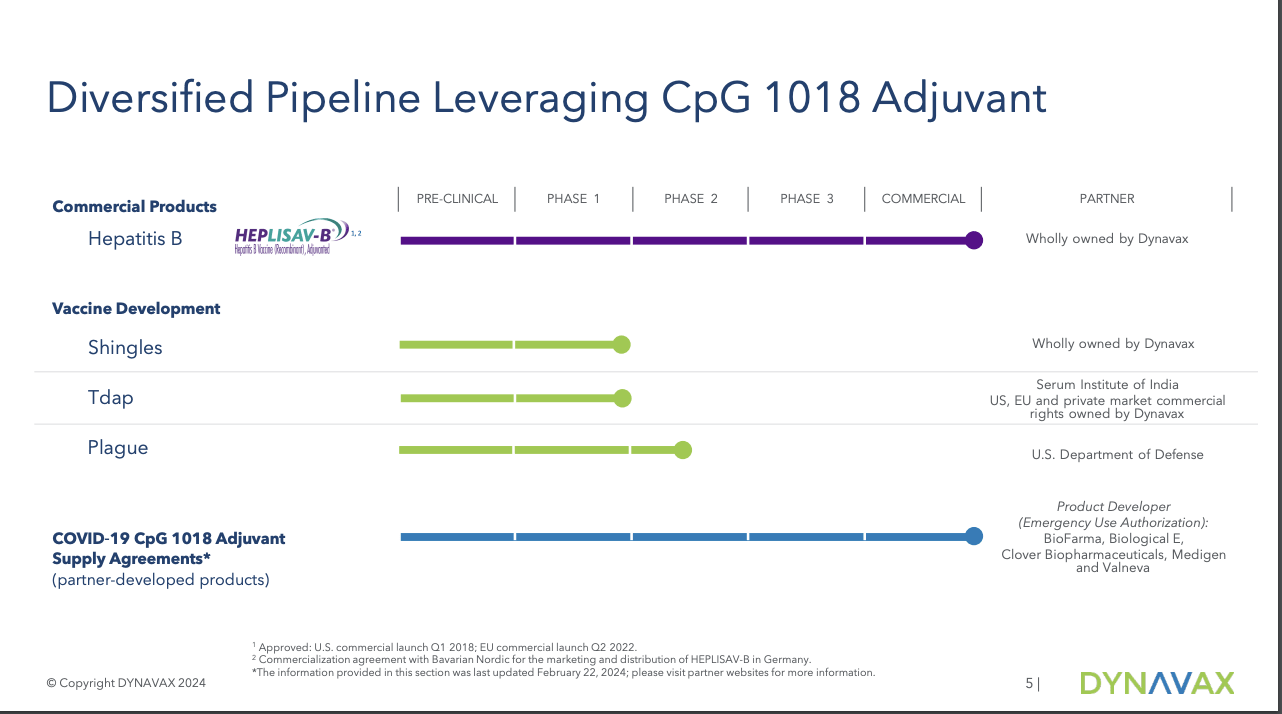

CpG 1018 adjuvant is not a one trick pony adjuvant solely useful in enhancing efficacy of COVID vaccines. Dynavax's HEPLISAV-B, which was FDA approved in 2017, is CpG 1018 adjuvanted. The same is true of Dynavax's entire pipeline of diverse vaccines as reflected by Presentation slide 5 below:

seekingalpha.com

Note that, excluding CpG 1018 and HEPLISAV-B, this pipeline is compact and early stage. Its plague vaccine is in phase 2 development and is its most advanced. During the Call CMO Janssen advised that he expected top line data on this at the end of 2024. The data would inform how Dynavax would move forward from there.

Unfortunately Dynavax has not succeeded in marketing it to third party vaccine makers other than for COVID. During the Call CMO Janssen advised its efforts in this regard are ongoing. He noted:

...we're advancing innovative and diversified vaccines that leverage our CpG 1018 adjuvant with proven antigens. We also continue to identify new opportunities to leverage our CpG 1018 adjuvant through multiple innovative preclinical and discovery efforts with leading collaborators.

Unfortunately for 2023 and anticipated for 2024 such efforts were/will be devoid of revenues. In response to a question about CpG 1018 revenues for 2025 and beyond CEO Spencer was noncommittal advising:

It's unclear. Depends on how the market demand and how the markets evolve and how our individual collaborator's products are utilized and the efforts they put beyond behind keeping up with the shifting landscape including stream managements. So obviously we'll be supportive of our partners and their initiatives. We believe COVID vaccination will continue globally for the years to come and is an important product in the marketplace. And so we will be there to support them as needed.

Not an encouraging answer for Dynavax bulls.

HEPLISAV-B is generating substantial growing revenues on its own.

While the heady days of hundreds of millions in CpG 1018 revenues appear to be over, Dynavax shareholders can count on lesser but significant HEPLISAV-B revenues. My previous article listed its annual revenues for 2018 and 2019 as— 2018 - $6.9 million, 2019 - $34.6 million

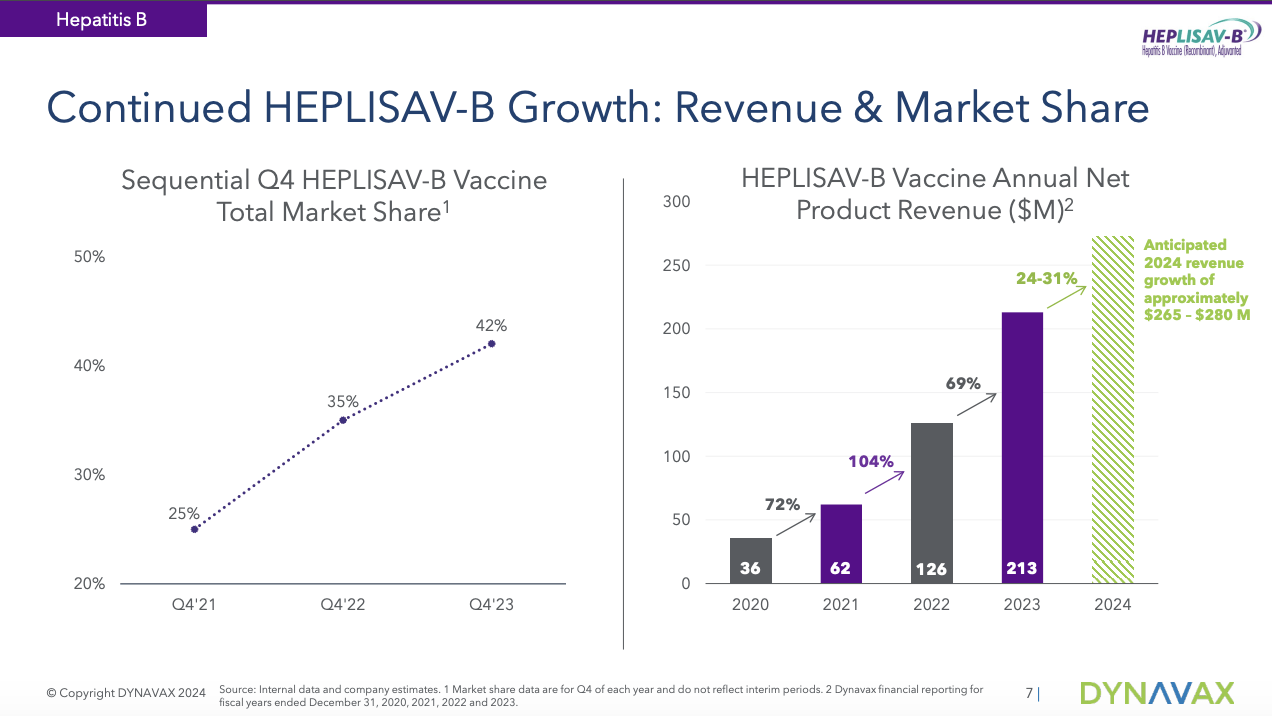

Presentation slide 7 lists its updated revenue and market share growth as shown below:

seekingalpha.com

During the Call CFO MacDonald advised HEPLISAV-B net product revenue grew to $239 million in 2023. She guided for continued net product growth with HEPLISAV-B expected to report product revenues between ~$265 million and ~$280 million during 2024.

Of interest in respect to HEPLISAV-B is Dynavax's HEPLISAV-B sBLA in hemodialysis. It is under review by the FDA with a PDUFA action date expected in 05/2024.This would allow Dynavax to offer a four dose regimen to the dialysis population. In response to a question during the Call CEO Spencer declined to advise whether its guidance included revenues from this group.

Growing HEPLISAV-B revenues support Dynavax's market cap of $1.58 billion.

The three ratings regimes reported by Seeking Alpha all rate Dynavax as a "Buy" as shown below:

seekingalpa.com

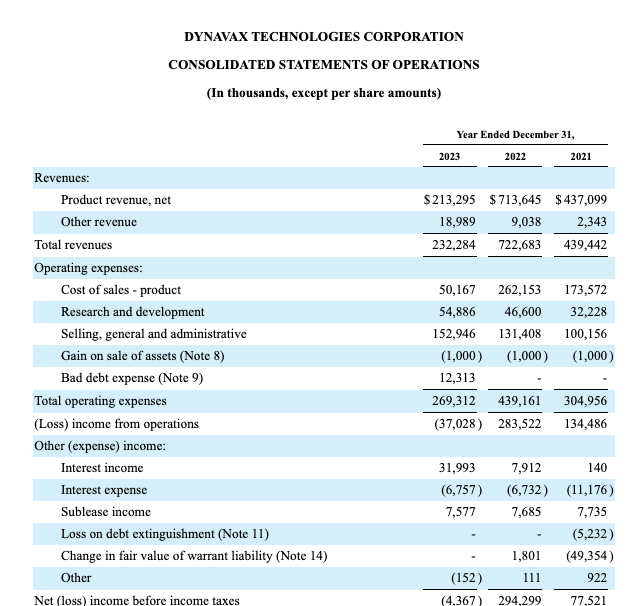

I submit that this is a highly optimistic assessment. Take a look at its excerpted income statement from its 10-K statement of operations (p. 76):

seekingalpha.com

It reported exceptional earnings when it had significant CpG 2018 revenues. Now that those have disappeared, it is back to adding moderately to its long term accumulated deficit which stood at $930.6 million at the close of 2023. Per its Full Year 2024 Financial Guidance slide 13 of the Presentation it expects to be cash flow positive for full year ended 2024 which seems entirely possible given its Q4, 2023 performance as shown above.

This is indeed a positive development; it would be based on HEPLISAV-B revenues alone. How ought one to assess the peak revenue potential of HEPLISAV-B?

Presentation slide 8 pegs HEPLISAV-B revenue 2027 revenue potential at $800 million. What share of that market Dynavax will command is a known unknown. During the Call CCO Casale asserts Dynavax will claim a majority of this by 2027. Let's peg this at $400 million. Tacking on a medium multiple of 4X would support a market cap of $1.6 billion.

Conclusion

Bulls and bears will never agree on a stock's value. That is how markets are made. Certainly there are lots of ways one might argue for a different Dynavax valuation, for example:

- electing a different peak revenue for HEPLISAV-B;

- applying a different multiple; I prefer the medium 4X multiple, bulls likely prefer 5X, 3X supports a more bearish view;

- hypothesizing a rekindling of CpG 1018;

- hypothesizing pipeline revenues.

Pick your poison. I assess Dynavax as an archetypical hold stock for the reasons stated. In my previous article I pegged it as a hold, noting that its then market cap of $1.92 billion, left it little margin for error. This is generally in line with my current thinking; the $1.92 represents a more aggressive 5X multiple.

I am not currently a shareholder; if I were monitoring the stock I would be alert to developments impacting items 1, 3 and 4 above.