angel_nt

Alliance Resource Partners (NASDAQ:ARLP) is undergoing a process to transition from the coal business to the Oil & Gas royalty business. This fundamental change is essential for its long-term survival, in light of regulatory and financial pressures arising from the existing coal exposure. We believe that if successful, the company could emerge as a leading royalty player and stand to benefit from a potential valuation multiples re-rate. The overall upside potential is around 50%, to $29 per share.

An ongoing transformation: royalties and strategic investments

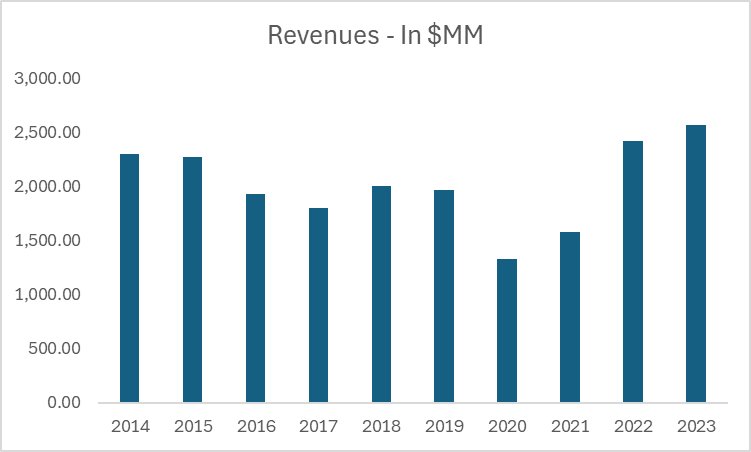

Alliance Resource is primarily a coal company, with roughly $2 billion per year in coal sales, and more than 600 million tons of reserves across the United States. Their mining operations are primarily based in Illinois and the Appalachian basin, where the bulk of reserves and resources are located. As with any commodity business, they are heavily exposed to the pricing environment, as reflected by revenue figures over the years.

Revenue (Seeking Alpha)

Additionally, the coal industry has been facing a rather challenging regulatory environment over the last few years, with ongoing efforts by the current administration to phase out this commodity. It is recent news, that newly proposed regulations aim at shut down coal-fired power plants two years sooner than expected. As reported:

The potential change reportedly under serious consideration would accelerate the required retirement date for coal plants that fail to install carbon removal technology at the sites, a tougher approach than the Environmental Protection Agency's initial proposal last year that would give companies until 2040 to shutter the sites.

This has clear impacts on a coal mining business like ARLP, as demand from utilities makes up the vast majority of the demand for energy commodities. So this draws an initially grey picture for Alliance: a volatile coal business that is facing pricing pressures and regulatory hurdles. But not all is negative.

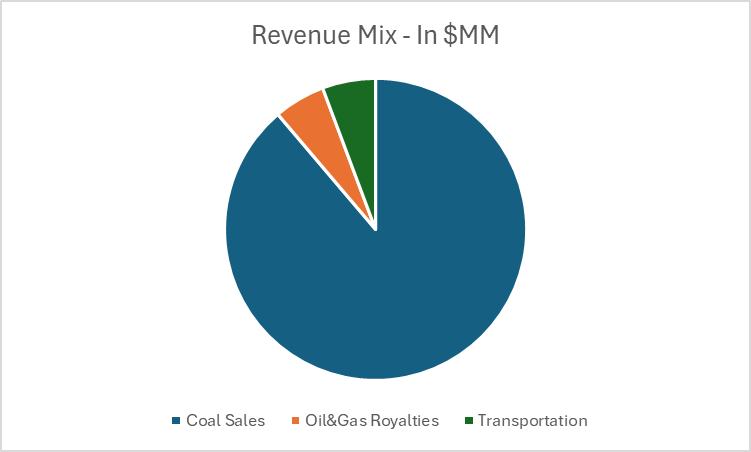

The company does indeed have a brighter side: some revenue diversification in favor of royalties and transport services, and a plan to transform the company over the next years. This is a representative snapshot of the current revenue mix:

Revenue Mix (SEC Filings)

Coal sales make up the lion's share of the topline figures, with royalties accounting for around 5% of the total mix. However, when looking at the Adjusted EBITDA contribution, which is disclosed by segment, we can notice that this segment jumps to around 12% contribution. Transportation services are very low margin and are primarily integrating the existing coal business, to improve the offering mix to customers. So where is the opportunity? Management is signaling its intention to shift the entire business model towards the royalties business, which would mark a marked change from a low-margin highly capital-intensive sector to a high-margin opportunity.

From the last earnings call:

Turning to our royalty segment, we remain committed to growing our oil and gas royalties business, which delivered record volumes in 2023. Over the past year, we acquired $111 million in additional oil and gas minerals, primarily concentrated in the Permian Basin. This marks our largest investment year since 2019.

They are actively pursuing new investments to grow the existing portfolio of royalties-generating assets through several acquisitions. From a first analysis of these deals, several of these investments are acres of undeveloped fields, meaning they are not yet oil-generating. As these properties are developed, the royalties will be applied also to existing sales, driving ARLP revenues higher. The management team also highlighted the rationale and the strategy behind these investments:

As we look to 2024, I would comment that during periods of commodity price volatility, the size and timing of acquisitions can be difficult to predict as our growth strategy relies on strict underwriting standards for investment that we will not compromise in tight markets.

This signals that the transition is not a premature closure of the existing coal business followed by a chaotic shift towards the royalties business marked by expensive acquisitions. The company is committed to delivering value-enhancing deals, and for this reason will maintain caution during these periods of high commodity price volatility, which could skew valuation multiples.

Finally, there was another important signal from the company: exploring opportunities outside the coal and Oil & Gas sector. From an extract:

We also remain committed to pursuing growth opportunities beyond coal and, oil and gas royalties. As we advance these initiatives, our investment decisions will be selective, aligned with our core competencies, and focus on areas where we can add significant strategic value. Let me be clear. We are not interested in building a portfolio of passive venture capital style investments. Initial positions should be thought of as potential platforms for future lines of business with long-term growth and cash flow generation.

We remain particularly optimistic by these words as they signal the intention to perform an organized transformation of the business model, rather than expropriating shareholders’ dividends to be redirected at cash-incinerating opportunities.

The valuation story: now and then, two businesses two multiples

Our core thesis is very clear: the market is evaluating the current company as a coal business, and for this reason, is attaching depressed multiples to its valuation. However, as the transitioning efforts become more pronounced, the stock will experience a re-rate to higher multiples which better represent the new high-margin and innovative business model.

To capture this thesis in numbers, we will present a snapshot of the current valuation framework, and the expected valuation framework post-transition. In terms of timing, we think this is more of a long-term plan, and management itself is not providing any guidance. However, as the market is forward-looking, we can expect that efforts will be noticed well in advance of their completion, likely within 2 years from now.

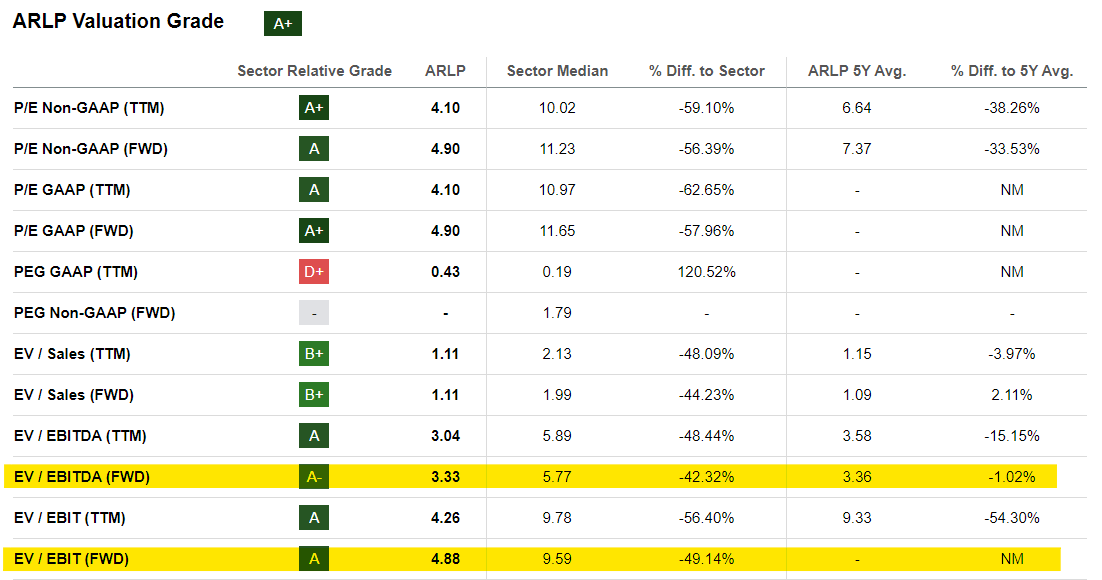

ARLP - Valuation (Seeking Alpha)

Today the stock trades at around 3 times EBITDA, which is around its historical average but below the median sector multiple. We believe this is primarily related to the high coal prices on which their long-term contracts are based. The market remains skeptical that this pricing environment could be sustained, and thus attaches a depressed multiple. However, the true opportunity could lie in the royalty revenues multiples.

Comparables (Seeking Alpha)

A preliminary analysis of some existing pure-play oil and gas and mining royalty businesses reveals that they are generously valued from a P/S standpoint, with an average multiple of around 10x. Right now royalty income is around $140 million if the company is able to bring it to around $280 million, or double the current figure, the value of the royalty business could already be as large as the current EV of the company ($2.8 billion). We estimate three scenarios of targeted royalty income over the next 2 years and the associated fair value.

Royalty revenue | EV associated to royalty business | Probability |

$180 million | $1.8 billion | 10% |

$280 million | $2.8 billion | 50% |

$320 million | $3.2 billion | 40% |

These three scenarios embed a possible spectrum of the outcomes of the transition. To compute the total EV, we also add today’s implied value of the coal business, which stands at around $1.4 billion, but discounted by 20%, to reflect it’s on a declining path. We also assigned probabilities to these three scenarios, as we expect that most likely the company will end up with around $280-320 million of royalty income per year within 2 years. The probability-adjusted fair value of this analysis is around $4 billion. In terms of fair price per share, that would be $29, with an upside potential of 52% from the current levels.

Risks: execution and commodity prices as primary sources of concern

We spot two key risks related to this company: (1) the proper execution of the aforementioned plan, and (2) coal prices. The first point relates to the ability of the management team to deliver on these expectations. This means closing the right deals, at the right valuations. It is not easy given the volatile environment they are currently facing, both from a supply and demand perspective. This could add significant uncertainty over the final outcome, or delay its achievement.

Additionally, like any other commodity company, there is a commodity risk associated with it. So far they have been benefiting from a very positive post-pandemic coal market, but this could change. If they were to sell at significantly depressed prices, this could also affect their ability to shift the business model, by lacking the resources to make royalty investments.

Overall, we feel confident these issues can be tackled by proper cash flow management and conservative deal-making. Additionally, the company operates under long-term contracts, which currently make up 95% of total revenues with expirations up to 2029.

Conclusion

Alliance Resource Partners is undergoing a radical transformation of its business model away from coal and towards royalty assets. This will radically change its financials and we believe will benefit its valuation multiples, eventually causing a re-rate of the stock. We think there is an overall upside potential of around 50% to a fair price of $29.