gopixa

Market conditions continue to be fluid, with overall inflation rates coming down, but price levels generally remain high throughout the economy. While most investors' long-term objectives are by definition not going to change anytime soon, individual strategies still have to evolve as the market environment fluctuates.

Dividend investing has become more common in the last ten years since rates have been at historically low levels for extended periods of time since 2008, and many investors have focused on funds that focus on income and have large and diverse holdings. One well-known exchange-traded fund that focuses on dividends is the Vanguard High Dividend Yield Index Fund (NYSEARCA:VYM).

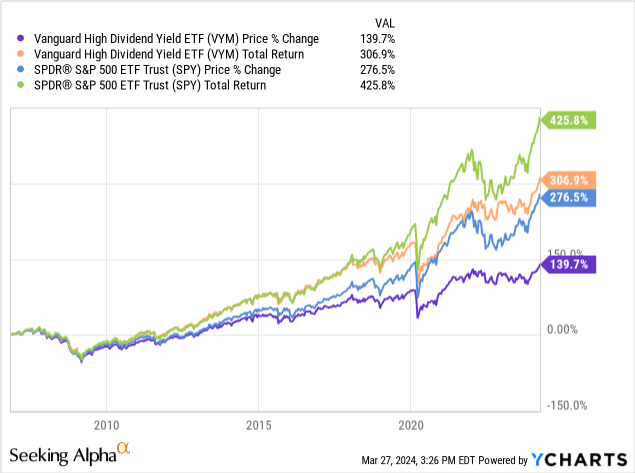

VYM is up a decent 300 percent since the fund's inception in late 2006. Still, the S&P 500 (SPY) has risen 427.88% during this same time period. VYM has offered only minimal income since 2006 as well, so comparing the ETF to the broader index is important.

I last wrote about the Vanguard High Dividend Yield Index Fund in May of 2023. I rated the fund a strong sell primarily because of how I believed a recession would impact the fund's significant cyclical holdings. I am upgrading the fund from strong sell to hold today. The prospect of a significant economic retraction has diminished and the fund is also better positioned today since the rate of inflation has fallen. Still, this fund remains unlikely to outperform the broader indexes or offer the same income as other dividend-focused ETFs for multiple reasons.

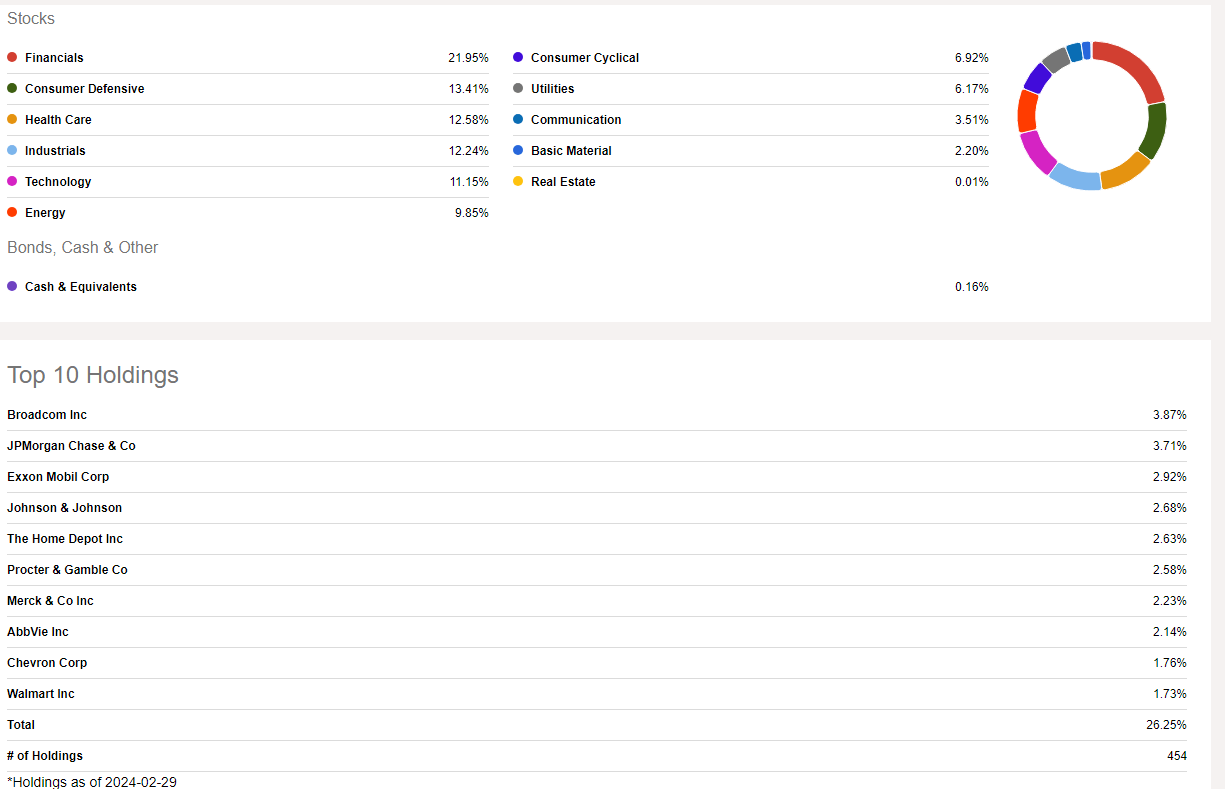

This Vanguard fund has $64.82 billion in funds under management and a yield of 2.88%. The ETF pays quarterly dividends. VYM's holdings are 21.95% financials, 13.41% consumer defensives, 12.58% health care, 12.24% industrials, 6.92% consumer cyclical, 6.17% utilities, 11.15% technology, 9.85% energy, 2.20% basic materials, and .01% real estate. The ETF's largest holdings are Broadcom Inc. (AVGO), JPMorgan Chase & Co. (JPM), Exxon Mobil (XOM), and Johnson & Johnson (JNJ).

A List of VYM's Holdings (Seeking Alpha)

VYM is primarily a growth fund, not an income-based investment. The fund has only raised dividend payouts at a rate of 5.22% per year over the last 5 years, and 6.92% per year over the last 10 years. The current yield is also just 2.88%.

The main reason VYM has offered investors only minimal income since the fund's inception is because this ETF has consistently been overweight the technology and industrial sectors, both industries that usually payout below-average dividends and income. Still, this fund's significant holdings in less cyclical sectors such as health care and the consumer defensive sector are the primary reason this ETF has also consistently and significantly underperformed the broader indexes.

Recent price data show the rate of inflation has fallen to nearly 3% and the economy appears likely to avoid a recession since consumer spending levels remain stable. VYM has never had significant energy and basic material holdings, so the fund predictably underperformed during the recent inflationary period that began in early 2021. This Vanguard fund performs best in a market environment with minimal inflation and solid growth because of the fund's significant holdings in big-cap tech and in more cyclical industries such as the industrials.

Still, while the overall economic conditions are more favorable for VYM now, this fund is still likely to underperform the broader indexes and offer less income than some of the fund's peers for multiple reasons. This ETF's significant defensive holdings make the fund likely to offer less growth than the broader indexes, but the Vanguard's funds significant holdings in the industrial and technology sectors also make this fund likely to offer less income than peers such as the Schwab U.S. Dividend Equity ETF Fund (SCHD) and the WisdomTree U.S. High Dividend Fund ETF (DHS). Both of these funds have only minimal allocations to the technology sector, which historically has paid less income, and these two ETFs also focus more than VYM on industries that tend to pay higher dividends such as the Utility and Energy sectors. VYM's defensive holdings in sectors such as the health care and consumer defensive sector make this fund likely to continue to underperform the broader indexes as well.

VYM does have the potential to offer investors solid growth because of the fund's overweight position in the technology sector and more cyclical parts of the market. The current economic environment is also more favorable for this fund, since the rate of inflation has come down, and growth rates remain stable. Still, most individuals who are interested primarily in growth or income should be able to find better alternative investments that focus more narrowly on specific objectives.