Audrius Venclova/iStock via Getty Images

Introduction

As it has been a year since I last reviewed SSAB (OTCPK:SSAAF) (OTCPK:SSAAY) here on Seeking Alpha, I wanted to check up on the company's performance as the share price has been pretty volatile in the past year. The share price is still up by about 200% since my initial article that was published in August 2020 [paywalled] so the total performance is still pretty good, especially as the company paid a cumulative 13.95 SEK per share in dividends since the summer of 2020 which already represents over half the share price at that time.

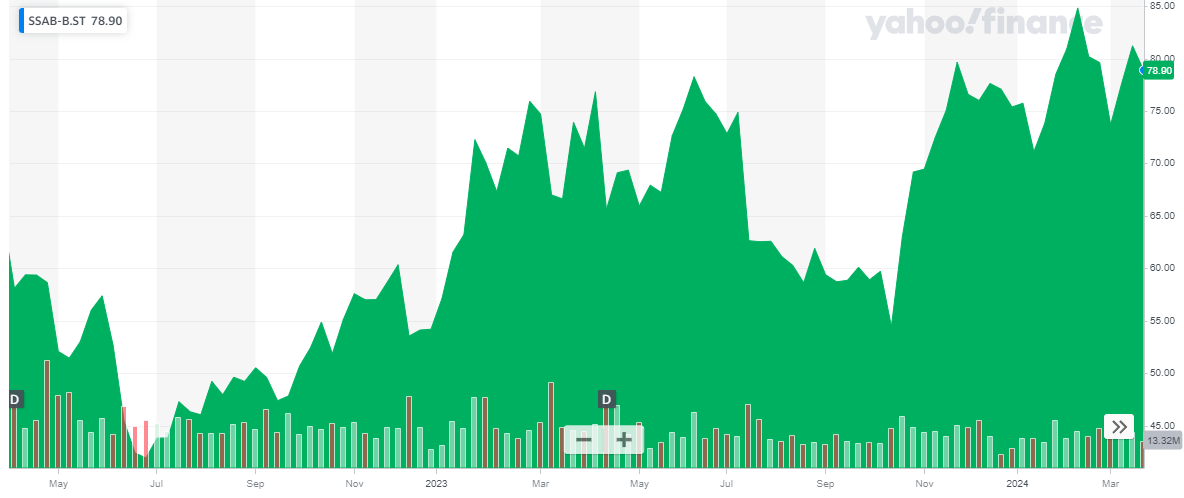

SSAB has its main listing on the Stockholm Stock Exchange where it's trading with SSAB as its ticker symbol. There are two types of shares, SSAB-A shares and SSAB-B shares. Both have the same economic rights but the B-shares are trading at a slightly lower valuation as the voting rights are just 1/10th of an A-share. As I explained in the August 2020 article: As a normal shareholder, it makes more sense to focus on the B-shares as the lower valuation outweighs the lack of a full vote unless you're an activist investor. The average daily volume for the B-shares is 3.5M shares per day while the A-shares are slightly more illiquid but an average daily volume of 1M shares per day is still pretty good. The image below shows the share price performance of the B-shares, and I will refer to the B-shares throughout this article.

Yahoo Finance

The total share count is 1.03B shares of which 304.2M shares are A-shares (representing 304.2M votes) while the remaining 725.7M B-shares represent 72.6M votes. The company repurchased just over 18M shares in the fourth quarter of 2023, which means there are approximately 1.01B shares outstanding. Unfortunately, the company's website still mainly contains download-only links, but you will be able to find all the documents I'm referring to here and here.

2023 was weaker than 2022 but still pretty good

SSAB is a steel producer with a total annual capacity of 8.8 million tonnes per year. Although the company recently focused hard on starting to produce 'green steel', its financial performance obviously still depends on the wellbeing of the world economy. Additionally, FX fluctuations also play a role although the SEK, the currency SSAB reports its financial results in, has been pretty stable.

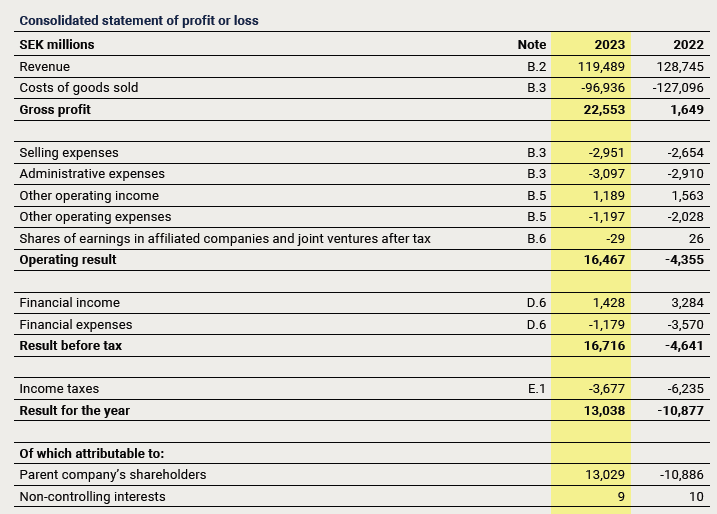

During 2023, the company reported a total revenue of just under 120B SEK which is an 8% decrease compared to the preceding year but as the COGS decreased by almost 25%, the gross profit as reported by the company skyrocketed.

SSAB Investor Relations

That being said, the jump from 1.65B SEK to 22.6B SEK warrants an additional explanation as the company recorded a 33.3B SEK impairment charge in 2022. This means that on an adjusted basis, the 2022 gross profit was actually approximately 35B SEK and on a YoY basis, the company definitely suffered from the lower revenue.

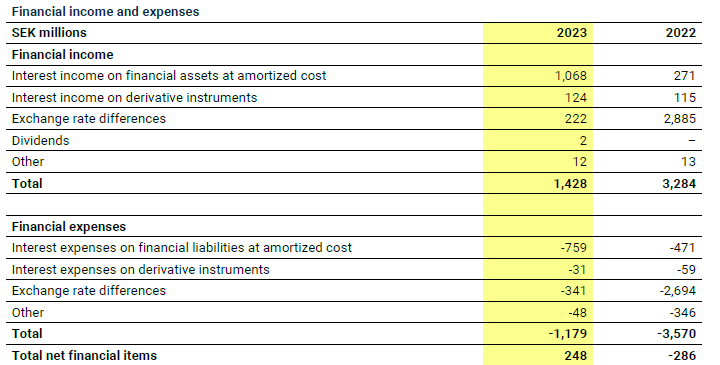

Other operating expenses increased as well. The selling expenses increased by almost 10% while the admin expenses jumped by in excess of 5%, resulting in an operating income of 16.5B SEK. One of the main reasons why SSAB has continued to intrigue me is its clean balance sheet. That's also visible in the income statement as the company converted a net finance cost of about 300M SEK into a net finance expense of approximately 250M SEK. Keep in mind the total net finance income (or cost) includes the impact from FX fluctuations as well, but as you can see below, if you would purely look at the net interest expenses and income you can see there was a very clear improvement in 2023.

SSAB Investor Relations

This helped SSAB to boost its pre-tax income to 16.7B SEK resulting in a net profit of 13B SEK representing an EPS of 12.7 SEK per share. That's better than I expected and the dividend of 5 SEK/share represents a payout ratio of just under 40% of the reported net income.

As you may remember, SSAB paid a very generous dividend in 2023 as its financial year 2022 was exceptionally strong on an underlying basis: the sole reason why it reported a net loss in 2022 was the non-cash impairment charge. The free cash flow was exceptionally strong in 2022, so I wanted to see how [well] the company was able to convert 'paper' profits into a positive free cash flow.

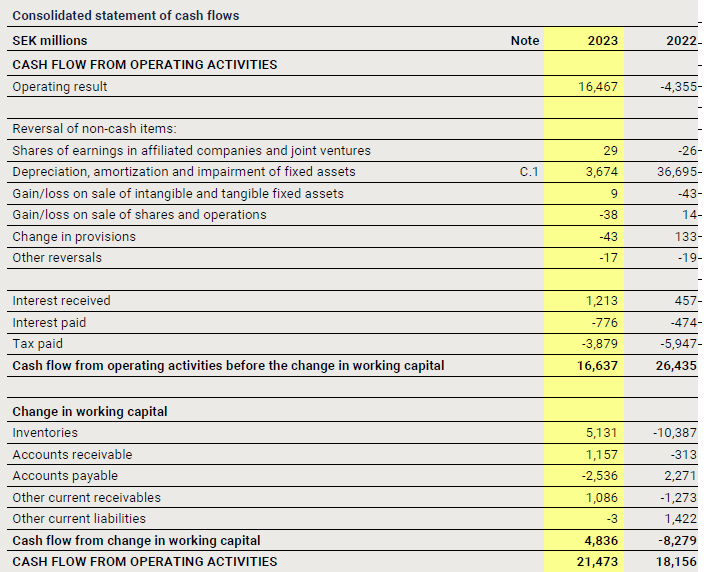

The operating cash flow statement below shows the company generated 21.5B SEK in operating cash flow. However, this includes a 4.8B SEK contribution from working capital changes while it also paid 200M SEK in taxes that weren't owed based on the FY 2023 result.

SSAB Investor Relations

This indicates the adjusted operating cash flow was approximately 16.8B SEK, and approximately 16.1B SEK after also deducting the approximately 700M SEK in lease payments paid in 2023.

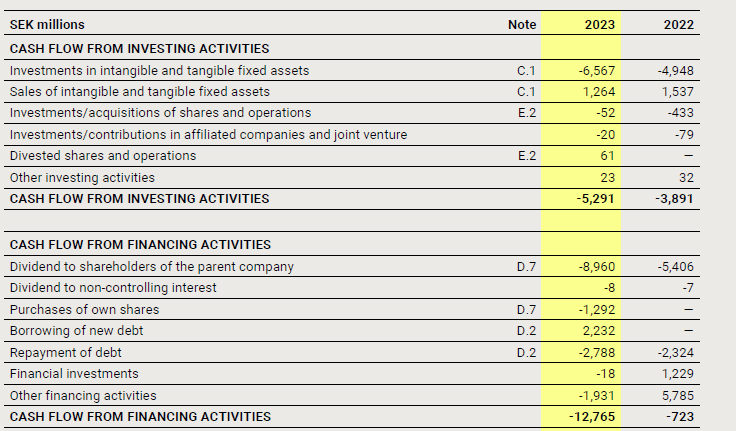

SSAB Investor Relations

As you can see above, the total capex was approximately 6.6B SEK, partially funded by the 1.26B SEK contribution from asset sales. This means the net capex was approximately 5.3B SEK, resulting in an underlying free cash flow result of 10.8B SEK. This represents approximately 10.7 SEK per share. The difference between the EPS and free cash flow result is entirely caused by SSAB's net capex (+lease payments), which is about 2.7B SEK higher than the depreciation and amortization expenses.

What will 2024 bring?

2023 was weaker than the stellar performance in 2022 and 2024 will likely be weaker than 2023. Looking at the consensus estimates for 2024, we see the average analyst consensus calls for an EBITDA of 13.4B SEK which should result in a net profit of approximately 7.5B SEK in both 2024 and 2025. This represents an EPS of around 7.5-7.8 SEK per share, the consensus estimates on the company website are calling for an EPS of around 8 SEK/share.

Meanwhile, the capex will remain elevated compared to the depreciation and amortization expenses, which means the underlying free cash flow result will once again be about 2 SEK/share lower than the reported net income.

SSAB will continue to pay a dividend that will be approximately 40% of the reported net income, so SSAB shareholders can look forward to a dividend of approximately 3-3.25 SEK per share for a dividend yield of approximately 4% based on the current share price. The standard dividend withholding tax rate in Sweden is approximately 30%.

Investment thesis

2023 actually was a pretty good year for SSAB as the company is currently trading at just 6 times its 2023 earnings while the dividend yield exceeds 6%. The cash flows were definitely more than sufficient to cover all the capex commitments, including growth capex while the ongoing 2.5B SEK share buyback program will likely reduce the net share count to less than 1B shares by the end of this year.

At the end of 2023, SSAB had a net cash position in excess of 21B SEK, representing approximately 21 SEK/share which means 25% of the current market capitalization is backed by cash. This also means that, assuming an EBITDA of 12.7B SEK (excluding lease amortization), the current EV/EBITDA ratio is just over 5 (excluding lease liabilities). While that is a higher ratio than, for instance, ArcelorMittal (MT), SSAB's investments in the future still make it an interesting investment and the stock remains attractive on weakness.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Consider joining European Small-Cap Ideas to gain exclusive access to actionable research on appealing Europe-focused investment opportunities, and to the real-time chat function to discuss ideas with similar-minded investors!