Toni M

Introduction

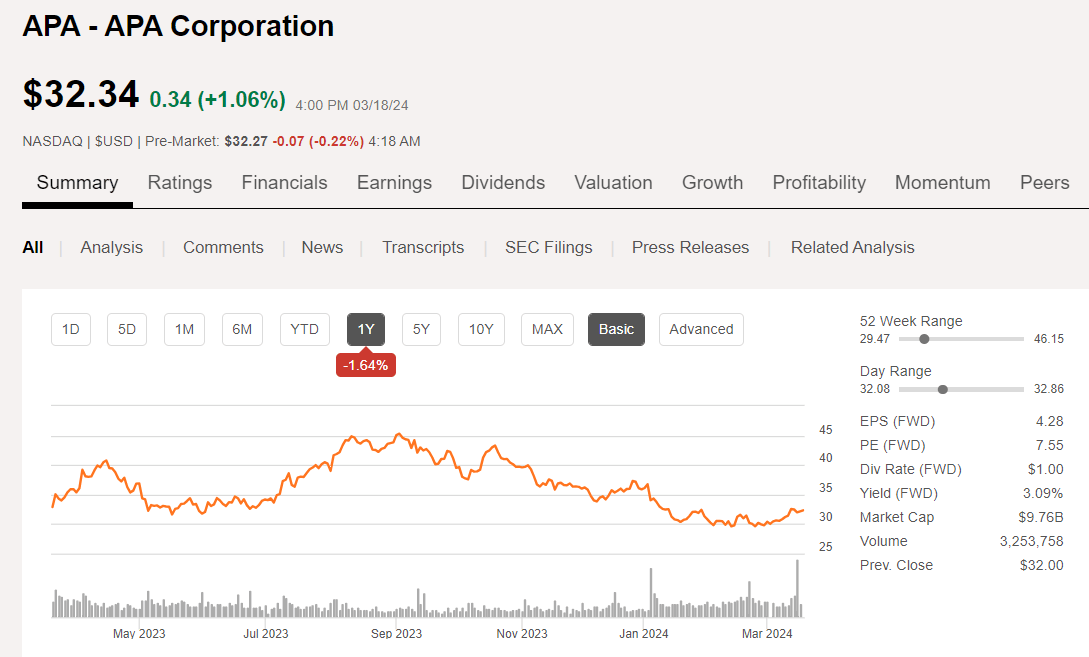

APA Corporation (NASDAQ:APA) stock has struggled for several months, falling from the low forties to around thirty before finding a bottom in early March. In the last couple of weeks it's begun to turn higher, notably as the completion date for its merger with Callon Petroleum drew closer on the First of April.

APA price chart (Seeking Alpha)

Someone got tired of waiting for APA to perk up as the company had a big-22 mm share down day on the 15th. On a technical basis, APA bounced off support at $30.42 - a support line that's held since mid-2022, but remains just below its resistance line at $36.60, and its 200 Day SMA. The chart today looks similar to mid-2023, where APA stock rallied from $32.00 to $48.00 over the course of the next three months, before beginning its long slide lower.

Analysts are all over the map with an overall rating of Overweight. Price targets range from $30.00 to $59.00, with a median of $39.00, so we can assume most of the seagulls view the company as having a limited upside. APA missed Q4 estimates-$1.33 bigly at $1.15, and projections for Q1, 2024 have come down to $0.85 from $1.45. Not a good trend that continues for Q2 2024, with estimates landing at $0.97, down from $1.39.

Let's dig into what the company is telling us about 2024.

First, the Callon Petroleum deal

Shale-centric E&P companies are getting bigger in the Permian or they are being bought out or merged. That is essentially the reality APA faced as 2023 closed out. Competitors were dropping like flies throughout the year, and Callon supplied a strategic lever to boost scale and oil-weighted production.

APA-Callon Deal (APA Corp)

The industrial logic for this merger is not as compelling as some we have reviewed in the past year or so. The acreage Callon brings to APA is not contiguous with their existing positions. What Callon's 145K acres in the Delaware will bring is a significantly higher oil cut-57%, than APA's current 46%. And, that is likely what drove the deal for APA.

APA CEO John Christman noted in the earnings call that APA believed it could do much to improve over Callon's performance in the Delaware:

Callon has experienced operational and productivity challenges in the past, more recently, they have begun to make good progress towards demonstrating the upside potential of their acreage. While the transaction is accretive on cost synergies alone, the big win-win for shareholders of both companies will be the integration of the assets into a larger Permian platform and the technical optimization, capital allocation, process knowledge and discipline that APA brings to the table.

Christman has some basis for his optimism. Some of that is due perhaps to better rock, but a case can be made that APA has done a better job of applying technology to obtain superior production results.

The company is looking for a win here. As noted in the release, problems have dogged APA for the last few years, beginning with the nearly $3.0 bn write-down of their Alpine High gas field in 2019, and a suspension of activity there. Then there is the prolonged FID status of their Suriname find - hopefully wrapping up in the next few months. Tax troubles in the UK, also leading to a suspension of activity, and production troubles in Egypt pretty much tied a bow on their troubles. The stock has been largely killed in the process, helped along by periods of low oil and gas prices.

APA is getting Callon for $2.6 bn in stock and the assumption of $1.9 bn in debt that Callon picked up due to some ill-timed and high-priced acquisitions of its own. For that, they are getting 145K net acres and 101K BOEPD, of which 119K acres and 75K BOEPD of oil weighted production come from the Delaware, where APA desperately needs scale. The rest - 26K acres and 26K BOEPD - come from the Midland, where APA is pretty solid. Only in one area - mostly in Howard and leaking over a bit into Martin County - does the Callon acreage fit into the "Industrial Logic" theme.

On an acreage basis, Callon is coming cheaply at $17K per acre. Other deals have been done for several times that amount, so we can tick the acreage box. On a flowing barrel basis, the box gets ticked as well, landing out at $25.7K per barrel, and at less than 2X on an operating cash flow metric. Those are three pretty good boxes to have ticked.

The APA as a standalone company is trading at 2.8X EV/EBITDA and $35K per flowing barrel. Neither are excessive, in my view. The combined company will log in at ~2.44X EV/EBITDA and $33K per flowing barrel.

In my view, the deal makes sense and helps APA Corp to be a stronger company. Worth noting is the fact that APA will have to print about 21 mm shares to pay out Callon, expanding their current float by 8%.

APA's international footprint

Their Egyptian concession is the big kahuna for APA. In QoQ comparison they managed to show a 4% gain, thanks to higher gas production, but dipped slightly YoY. In the call they noted that this was due to a lack of workover rig availability and problems with their Electrical Submersible Pumps-ESPs.

APA Production table (APA Corp)

Christman noted in his comments-

During 2023, we had nine new wells impacted by early ESP failures, two of which occurred in the fourth quarter on high-volume wells. We have traced this problem to one manufacturing facility, and the situation is in the process of being remediated. In 2024, we will gear down the Egypt drilling program a bit, which will free up workover rig capacity to reduce the workover and recompletion backlog.

It is good this has been traced to the manufacturer as ESP problems are often reservoir related. It bodes well for a boost in 2024 as the company has promised.

Suriname

The company and its operating partner, TotalEnergies, (TTE) have identified a resource of 700 mm BOOIP, with first oil slated for 2028. Christman commented in the call that an FID decision will be taken this year. This has the potential to add 15% to APA's daily output when it comes online. Translating to $6-8.00 on the stock price-at some point and obviously dependent on Brent prices.

An Alaskan exploration catalyst

With a 275K acre concession on state lands and the support of the Alaskan government and impact Eskimo tribes, APA plan North Slope drilling with three rigs to test a reservoir concept. Christman noted that it bears similarity to Santos's (Australian operator) Pikka development that was FID'd in 2022. Pikka is targeting ~400 mm bbl and at full production will add 80K BOEPD to their output. A success case for APA would certainly be accretive, but as it's exploration we will hold off adding to their valuation. Put this on the sticky note parking lot for the company though!

Risks

APA is a little debt-heavy with $5.4 bn in long term and adding the Callon $1.9 bn of debt to that. While not in a comfort zone at 1.39 debt to equity ratio, it doesn't seem excessive in current market conditions. The company has repaid $2.0 bn of debt since 2021, and has the cash flow to maintain and even accelerate that pace while meeting dividend, capex and stock repurchase obligations.

Your takeaway

As I noted in our Investing Group chat the other day, I've added to my APA position for what I think will be a turnaround year for the company. We are seeing higher prices for WTI and Brent, and if they deliver on promises made in regard to their Permian-Delaware basin work, and fix Egypt, the company should see higher cash flows and deserve a higher multiple than it now has. A 2.75X multiple would deliver the high end of analyst estimates before any FID news on Suriname is baked in.

I think APA is a buy at current levels for investors looking for growth and modest dividend income at $1.0 per share on an annual basis. APA has also been buying back stock at current levels, at about a 5 mm share per quarter clip, which knocks the total down ~20 mm per year. Since YE 2022, the float has been reduced from 333 mm to 309 mm.

APA Corporation pays a modest dividend, but investors should expect capital returns to be directed toward the share count in the current price range.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.