SmileStudioAP

Rubrik Is Transitioning To A SaaS Company

Rubrik, Inc. (NYSE:RBRK) has filed to raise $100 million in an IPO of its Class A common stock, according to an SEC S-1 registration statement.

Rubrik helps organizations secure their data through the company's cloud platform and software.

While RBRK is making significant progress toward becoming a SaaS subscription company, such transitions can take time, and the firm's topline revenue growth has been muted, with high operating losses.

I'll provide an update when we learn more details about the IPO.

What Does Rubrik Do?

Palo Alto, California-based Rubrik, Inc. was founded to provide a range of data security technologies to companies worldwide.

Management is headed by co-founder, Chairman and CEO Mr. Bipul Sinha, who has been with the firm since January 2014 and was previously a Partner at Lightspeed Venture Partners and was a board member of Nutanix.

The company's primary offerings include the following:

Data protection

Data threat analytics

Data security posture

Cyber recovery

As of January 31, 2024, Rubrik has booked fair market value investment of $980 million from investors, including Lightspeed, Greylock Partners and various individuals.

The firm markets its cloud platform capabilities generally to mid and large-sized enterprises via a direct sales and marketing force in the U.S. and employs a 'land and expand' strategy to grow its business within each client.

As of January 31, 2024, the company had over 6,100 customers from around the world.

Sales and Marketing expenses as a percentage of total revenue have grown as revenues have increased, as the figures below indicate:

Sales and Marketing | Expenses vs. Revenue |

Period | Percentage |

FYE January 31, 2024 | 76.8% |

FYE January 31, 2023 | 69.6% |

(Source - SEC)

The Sales and Marketing efficiency multiple, defined as how many dollars of additional new revenue are generated by each dollar of Sales and Marketing expense, was only 0.1x in the most recent reporting period. (Source - SEC)

The Rule of 40 is a software industry rule of thumb that says that as long as the combined revenue growth rate and EBITDA percentage rate equal or exceed 40%, the firm is on an acceptable growth/EBITDA trajectory.

RBRK's most recent calculation was negative (44%) as of January 31, 2024, so the firm has performed poorly in this regard, per the table below:

Rule of 40 | Calculation |

Recent Rev. Growth % | 5% |

Operating Margin | -49% |

Total | -44% |

(Source - SEC)

The firm's dollar-based net revenue retention rate for its subscription customers was 133%, a strong result, but one that is only based on its subscription customer base and does not include its legacy perpetual license base, which the firm is seeking to convert to a subscription.

What Is Rubrik's Market?

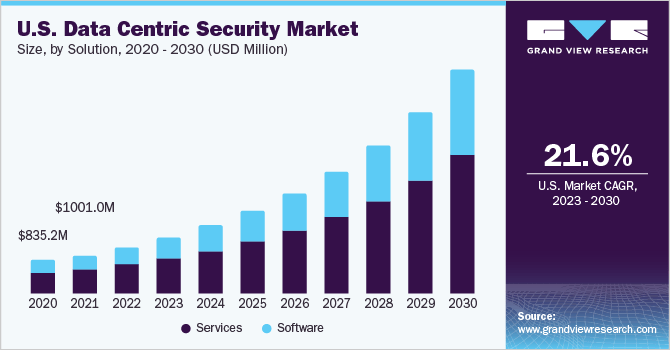

According to a 2023 market research report by Grand View Research, the global market for data centric security was an estimated $4.3 billion in 2022 and is forecasted to reach $24 billion by 2030.

This represents a forecast CAGR (Compound Annual Growth Rate) of 24.2% from 2023 to 2030, a very strong expected growth rate.

The primary drivers for this expected growth are the continued migration of on-premises computing technologies to the cloud and increasing cyber threats against cloud systems.

Also, the chart below shows the historical and expected future growth trajectory of the U.S. Data Centric Security Market from 2020 to 2030:

Grand View Research

Major competitive or other industry participants include the following:

Commvault

Dell EMC

IBM

Veeam

Cohesity

Others

Rubrik's Recent Financial Results

The company's recent financial results can be summarized as follows:

Slowly growing topline revenue

Increasing gross profit and gross margin

High operating losses

A swing to cash used in operations

Below are relevant financial results derived from the firm's registration statement:

Total Revenue | ||

Period | Total Revenue | % Variance vs. Prior |

FYE January 31, 2024 | $ 627,892,000 | 4.7% |

FYE January 31, 2023 | $ 599,819,000 | |

Gross Profit (Loss) | ||

Period | Gross Profit (Loss) | % Variance vs. Prior |

FYE January 31, 2024 | $ 482,930,000 | 15.6% |

FYE January 31, 2023 | $ 417,805,000 | |

Gross Margin | ||

Period | Gross Margin | % Variance vs. Prior |

FYE January 31, 2024 | 76.91% | 10.4% |

FYE January 31, 2023 | 69.66% | |

Operating Profit (Loss) | ||

Period | Operating Profit (Loss) | Operating Margin |

FYE January 31, 2024 | $ (306,506,000) | -48.8% |

FYE January 31, 2023 | $ (261,548,000) | -43.6% |

Comprehensive Income (Loss) | ||

Period | Comprehensive Income (Loss) | Net Margin |

FYE January 31, 2024 | $ (355,096,000) | -56.6% |

FYE January 31, 2023 | $ (278,959,000) | -46.5% |

Cash Flow From Operations | ||

Period | Cash Flow From Operations | |

FYE January 31, 2024 | $ (4,518,000) | |

FYE January 31, 2023 | $ 19,287,000 | |

(Source - SEC)

As of January 31, 2024, Rubrik had $279 million in cash and $1.6 billion in total liabilities.

Free cash flow during the twelve months ended January 31, 2024, was negative ($16.9 million).

Rubrik's IPO Information

Rubrik intends to raise $100 million in gross proceeds from an IPO of its Class A common stock, although the final figure may be higher.

There are no existing shareholders who have expressed interest in buying shares at the IPO price.

Class A shareholders (public investors) will be entitled to one vote per share and Class B shareholders will receive 20 votes per share.

Management says it will use the net proceeds from the IPO as follows:

We intend to use the net proceeds we receive from this offering, together with existing cash, cash equivalents, and short-term investments, if necessary, to satisfy all of our anticipated tax withholding and remittance obligations related to the settlement of certain outstanding RSUs in the RSU Net Settlement and the Additional RSU Net Settlement.

We intend to use any remaining net proceeds we receive from this offering for general corporate purposes, including working capital, operating expenses, and capital expenditures. We cannot specify with certainty all of the particular uses for the remaining net proceeds to us from this offering. We may also use a portion of the remaining net proceeds for the acquisitions of, or strategic investments in, complementary businesses, products, services, or technologies. However, we do not have any agreements or commitments to enter into any material acquisitions or investments at this time.

(Source - SEC)

Leadership's presentation of the company roadshow is not currently available as of press time.

Regarding outstanding legal proceedings, management said the company is not a party to any legal proceedings that it believes would have a material adverse effect on its operations or financial condition.

The listed bookrunners of the IPO are Goldman Sachs, Barclays, Citigroup, Wells Fargo Securities, Guggenheim Securities, Mizuho, Truist Securities, BMO Capital Markets, Deutsche Bank Securities, KeyBanc Capital Markets, Cantor, CIBC Capital Markets, Capital One Securities, Wedbush Securities and SMBC Nikko.

Rubrik's IPO Summary And Comments

RBRK is seeking U.S. public capital market investment to fund its growth plans and working capital requirements.

The company's financials have generated slightly growing topline revenue (overall), higher gross profit and gross margin, very high and increasing operating losses and a swing to cash used in operations.

Free cash flow for the twelve months ended January 31, 2024, was negative ($16.9 million).

Sales and Marketing expenses as a percentage of total revenue have risen as revenues have increased slightly; its Sales and Marketing efficiency multiple was only 0.1x in the most recent fiscal year.

The firm currently plans to pay no dividends and to keep any future earnings to reinvest back into the company's growth and working capital needs.

RBRK's recent capital spending results indicate it has continued to spend on capital expenditures despite negative operating cash flow.

The company's Rule of 40 results have been poor, with slow-growing topline revenue and large operating losses contributing to a negative figure for this metric.

The market opportunity for providing data security cloud services is large and expected to grow at a high rate of growth in the coming years.

Risks to Rubrik's outlook as a public company include the time that it will take to substantially complete the migration of its legacy perpetual customers to its cloud platform, which management forecasts will not be finished until at least fiscal 2026.

Other such firms have sought to make this conversion and their growth trajectory has suffered from the conversion process.

The company's subscription business contribution margin is most recently negative (12%) for the fiscal year ended January 31, 2024, compared to negative (117%) for fiscal 2022, a significant improvement indicating material progress toward producing subscription segment operating leverage in the coming years.

Valuation at IPO will be critical, and management will likely seek to make the 'narrative' case that the company is successfully transitioning to a fully cloud SaaS company.

When we learn Rubrik's pricing and valuation assumptions, I'll provide a final opinion.

Expected IPO Pricing Date: To be announced.

Consider becoming a member of IPO Edge.

Gain Insight and actionable information on U.S. IPOs with IPO Edge research.

Members of IPO Edge get the latest IPO research, news, and industry analysis. Get started with a free trial!