LeoPatrizi

PNM Resources, Inc. (NYSE:PNM) is an energy holding company whose two regulated utilities collectively provide electricity to over 800,000 homes and businesses in New Mexico and Texas.

PNM Resources has two regulated utility segments, PNM, a vertically integrated electric utility in New Mexico with distribution, transmission and generation assets, and TNMP, an electric transmission and distribution utility in Texas.

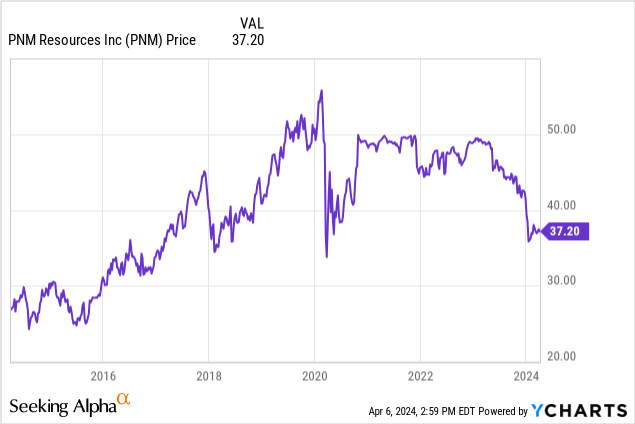

Shares of PNM Resources are considerably lower than their early 2020 pre-pandemic highs.

One key reason for the decline is that Avangrid terminated its merger agreement on December 31, 2023 to buy PNM Resources for $50.30 in cash per share given regulatory hurdles. Other reasons for the poor performance include higher interest rates since 2022 and a disappointing PNM rate decision.

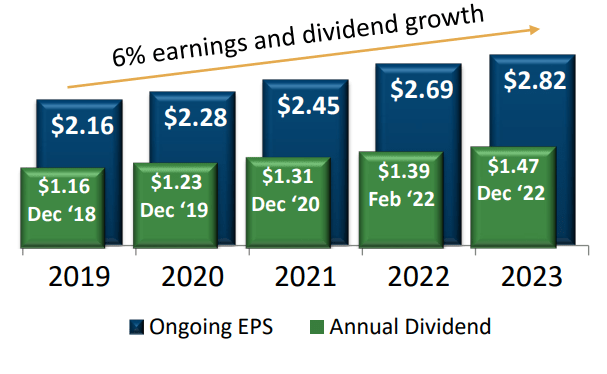

Although its stock has not performed well since 2020, PNM Resources' ongoing EPS and annual dividend has nevertheless grown at around 6% annually from 2019 through 2023.

PNM Resources Investor Presentation

On February 6, 2024, PNM Resources reported 2023 earnings results that indicated further growth. For the medium term with the exception of 2024, management is bullish on the company's EPS growth potential given expected growth in the regulated rate base. Given its leverage, however, PNM Resources doesn't have as much financial flexibility as some other utilities.

2023

For 2023, PNM Resources reported ongoing diluted EPS of $2.82, up from $2.69 in 2022 due to factors such as load growth and weather.

In terms of segments, ongoing diluted EPS in the PNM segment rose to $2.22 in 2023 from $1.90 in 2022 while ongoing diluted EPS in the TNMP segment rose to $1.11 in 2023 from $1.07 in 2022. In the company's Corporate and Other segment, ongoing diluted EPS was a loss of $0.51 in 2023 from a loss of $0.28 for 2022.

One reason for the higher loss in the Corporate and Other segment was higher interest rates on variable rate debt.

My takeaway is that PNM Resources grew in 2023 given continued growth in the company's two utility segments despite higher interest rate headwinds.

Outlook

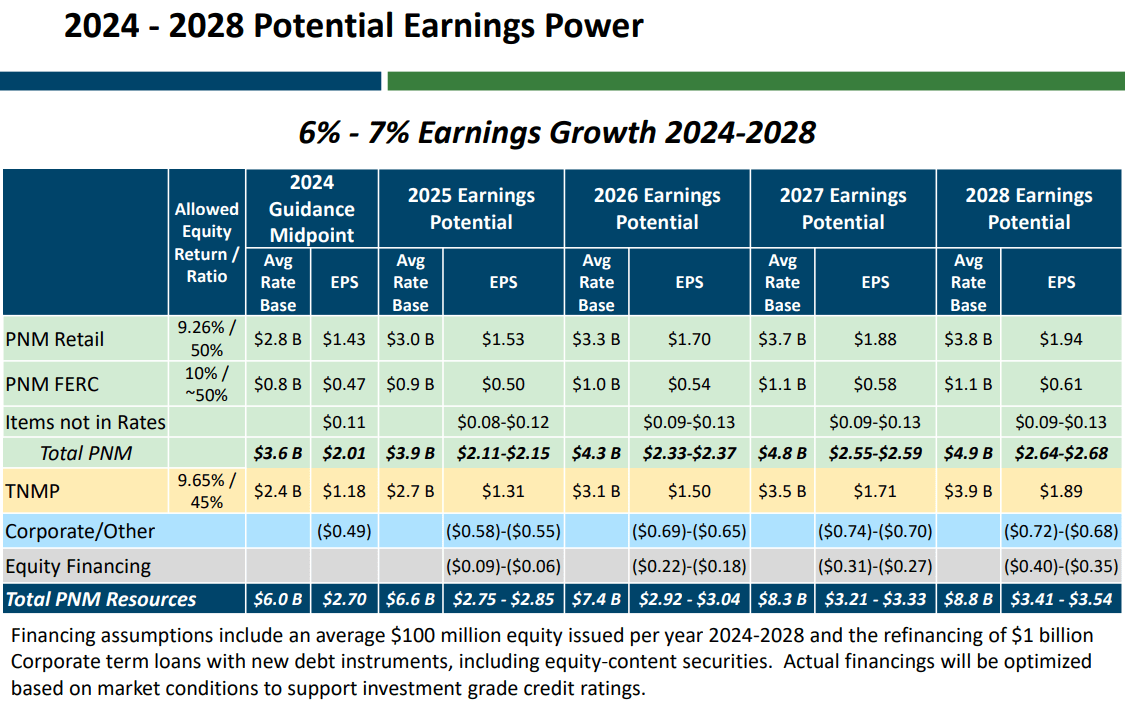

With the exception of 2024, PNM Resources management sees more earnings growth in the future.

For 2024, management has ongoing earnings guidance range of $2.65-$2.75 per diluted share. That compares to PNM Resources' ongoing diluted EPS of $2.82 for 2023.

The fairly weak earnings for 2024 largely has to do with the disappointing PNM rate review outcome as PNM Resources filed for a base rate increase of $63.8 million and regulators authorized an increase of $15.3 million with base rates effective January 2024.

Nevertheless in terms of CAGR, management believes PNM Resources still has 6% - 7% earnings growth potential given expected 10% rate base growth from 2024 through 2028 based on the 2024 ongoing earnings guidance midpoint of $2.70 per share.

PNM Resources Investor Presentation

In terms of its rate base growth, PNM Resources is increasing its regulated rate base to meet growing customer demands, enable the clean energy transition, and to make the grid more reliable and resilient.

My takeaway is that management, with the exception of 2024, sees fairly attractive medium term EPS earnings growth through 2028 given expected regulated rate base increases.

Financial Flexibility

In terms of trailing statistics, PNM Resources has fairly high leverage in my view as the company has a financial leverage ratio of 4.27 as of Q4 2023. In terms of debt, the company has total debt of $4.7837 billion as of December 31, 2023.

When it comes to PNM Resources, the larger debt has a positive and a negative.

One positive is that lower interest rates could help PNM Resources given its debt profile as variable rate debt costs could be more affordable.

According to my calculations, PNM Resources has total variable rate debt of $1.3775 billion as of February 16, 2024 with weighted average interest rates ranging between 6.3% and 6.92%.

If interest rates normalize and decrease 5% in a hypothetical scenario, a 5% decrease in the variable rate debt of $1.3775 billion would mean $68.9 million in less interest expenses. By comparison, PNM Resources has TTM EBITDA of $612.61 million.

With that said, I think regulators will likely decrease the allowed return on the regulated rate base for future years if interest rates decline substantially so the tailwind might not be as great as $68.9 million.

Furthermore, PNM Resources has some hedges for interest rates as well. For 2024, the company has $600 million hedges in place at an underlying interest rate at 3.5% for instance.

Nevertheless, I think lower interest rates will still be a tailwind as I think interest rates will begin to decrease this year and normalize in a year or two and regulators won't decrease the allowed returns on the regulated rate base by nearly as much.

The negative to being more leveraged is that PNM Resources might have to finance more of its capital investments from equity, which might be dilutive.

In 2023, for instance, PNM Resources had $200 million in equity financing with 4.4 million shares issued in December 2023. According to management, the 4.4 million shares issued had a $0.14 impact on year over year earnings per share.

Given its stock price now is lower than December 2023, equity financing could have more of an impact on earnings per share year over year growth.

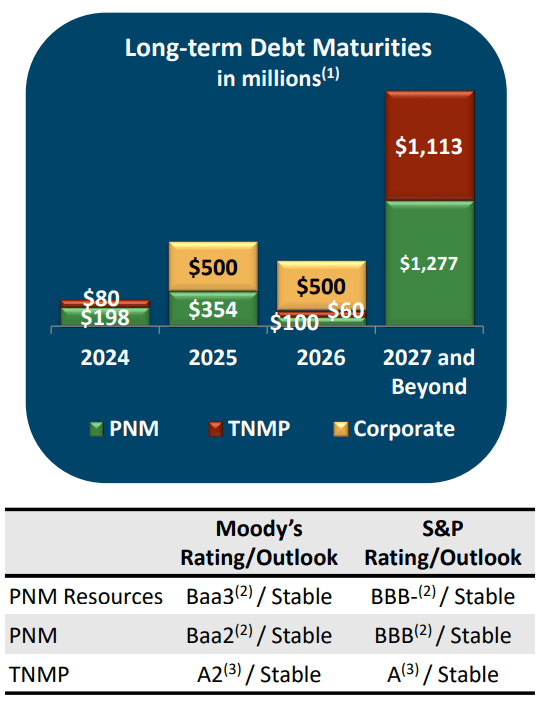

Given the current balance sheet, it isn't clear if PNM Resources can add substantially more debt and maintain an investment grade rating. Without an investment grade rating, PNM Resources might have higher interest rate expenses.

In terms of equity financing outlook, PNM Resources sees another $500 million in equity financing from 2024 through 2028 or around an average of $100 million per year.

Management has also said actual financing will be optimized based on market conditions to support investment grade credit ratings so there's a chance of more equity financing if they can't raise as much debt as expected while maintaining investment grade status.

In terms of its maturing long term debt schedule, PNM Resources has $278 million in 2024 and $854 million in 2025. Ideally PNM Resources will be able to replace the maturing debt with new debt and not with equity but this depends on market conditions and whether the company can maintain its investment grade credit rating.

PNM Resources Investor Presentation

Solar Costs

While there might be more need for capital spending, it isn't clear if PNM Resources will make as much return on its regulated rate base in the future as in past years given decreasing solar electricity generation costs.

Given PNM Resources operates in New Mexico and Texas, there's more solar potential in many areas in the two states as they get more sunlight than average.

As a result, PNM Resources is arguably more on the leading edge of solar energy's effect on energy generation for utilities.

By being more on the leading edge, I think there is a risk where regulators don't allow PNM Resources to make as much return on its regulated rate base as expected given the increasing competitiveness of solar electricity generation. The effect of regulatory decisions on the rate base can be a significant headwind as PNM Resources' 2024 ongoing EPS outlook illustrates.

Nevertheless, I think PNM Resources is in a better position than many other utilities to handle lower electric bills if that should occur given the average monthly residential PNM bill is $73.95, versus the national average of $132.15.

Risks

Electricity prices could decline more than expected given the decrease in cost of solar energy generation.

PNM Resources has fairly high leverage. If electricity consumption is less than expected or expenses increase more than expected, the company's financials could be under more pressure.

Regulators might not allow PNM Resources to make as much return on its regulated rate base as the market expects.

Valuation

In terms of estimates, analysts on average expect PNM Resources to earn $2.67 per share for 2024, $2.82 per share for 2025, and $2.99 per share for 2026 according to Seeking Alpha. That gives the company a forward PE ratio of 13.93 for 2024, 13.18 for 2025, and 12.44 for 2026.

Seeking Alpha

In terms of management estimates, they see ongoing earnings guidance range of $2.65-$2.75 per diluted share for 2024, $2.75-$2.85 for 2025, $2.92-$3.04 for 2026 so the analyst estimates are within management guidance range.

When incorporating debt, PNM Resources has a forward EV/EBITDA ratio of 9.85, versus the sector median of 10.42 and the company's 5 year average of 11.23.

Given the forward EV/EBITDA and its forward PE ratios, I'd say PNM Resources has a fairly attractive valuation if it can meet EPS estimates, which are within management guidance ranges.

As 2024's soft earnings outlook illustrates however, regulatory decisions could cause the company's results to underperform management guidance.

In the future, I think there is the possibility that the increasing economic competitiveness of solar electricity generation lead to less than expected allowed returns on the regulatory rate base.

With that said, even if solar energy generation costs is a headwind, I am cautiously optimistic that the increases in electricity demand, given growth in EVs, data centers, and other relatively new sources, will still increase PNM Resources' EPS in the long run as it could increase the regulatory rate base substantially.

Given I think interest rates will decline this year and be a fairly decent tailwind, I think PNM Resources will be able to meet or exceed 2024, 2025, and 2026 estimates.

As such, I rate PNM Resources a 'Buy' and I would own it in a diversified portfolio that includes the Magnificent Seven. I would not 'overweight' it however as the company isn't that large and is also fairly leveraged. There is also uncertainty given potentially decreasing energy generation costs in the future.

In terms of my price target, I think PNM Resources should trade for a forward EV/EBITDA of 10.42 which is the sector average which gets me around $42.59 per share.

I think earnings reports and any potential news of interest rate decreases will be catalysts and I would follow interest rates, rate base decisions, electricity prices, and electricity consumption trends.