Chayantorn

Pinterest (NYSE:PINS) is emerging from a difficult multi-year period, with solid user growth and revenue growth accelerating. Pinterest's margins are also increasing, and the company will begin to generate meaningful cash flows over the next few years. Pricing remains a headwind, though, which is masking some of the improvements.

The company's share price is yet to fully recover from the MAU decline in 2021, and the consequent narrative that characterized Pinterest as a dying platform. Pinterest should see strong earnings growth over the next 5-10 years, along with stable or even improving multiples, leading to strong returns.

I previously suggested that Pinterest's growth was likely to remain strong as its user base was under monetized, but that the company was no longer an obvious buy based solely on valuation. Since then, Q4 results came in softer than expected and the stock is down around 7%. The company's fundamentals remain unchanged, though, and first quarter guidance suggests more robust growth going forward.

Market Conditions

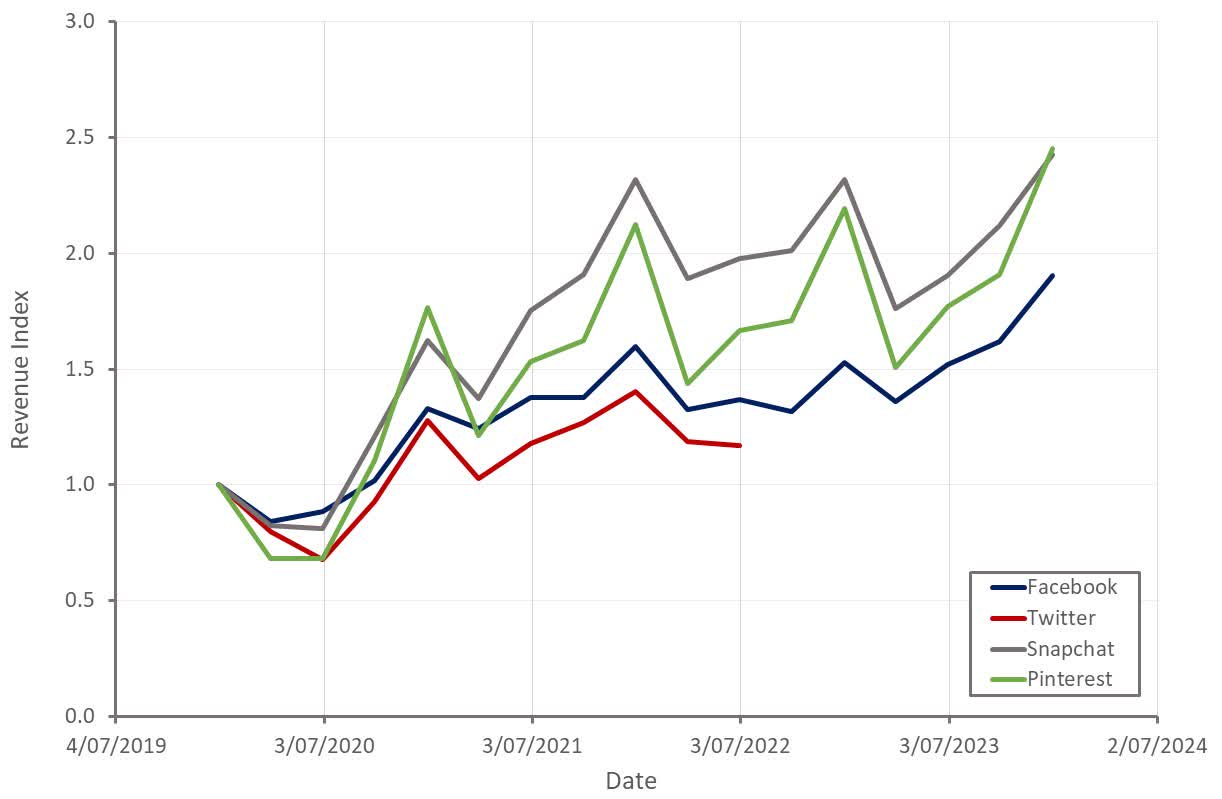

Pinterest has characterized ad market conditions as stable to improving. This is a sentiment that is broadly shared across companies with exposure to digital advertising and is reflected in increasing growth rates for most companies. Financial performance is diverging across companies, though, dependent on end market exposure and the company's ability to adapt to current conditions.

Retail is currently Pinterest's fastest growing segment, with the food and beverage category demonstrating weakness in December and continuing through into Q1. While the demand environment has stabilized, the supply of inventory remains strong, undermining pricing.

Ad performance matters more than ever, which is apparent from the revenue growth of public companies in recent quarters. This sets Pinterest up well in 2024, as the company moves down the targeting funnel and improves its targeting and attribution tools. Pinterest users have commercial intent, which should ultimately lead to strong ROAS.

Figure 1: Public Social Media Company Revenue (source: Created by author using data from company reports)

Supply of Inventory

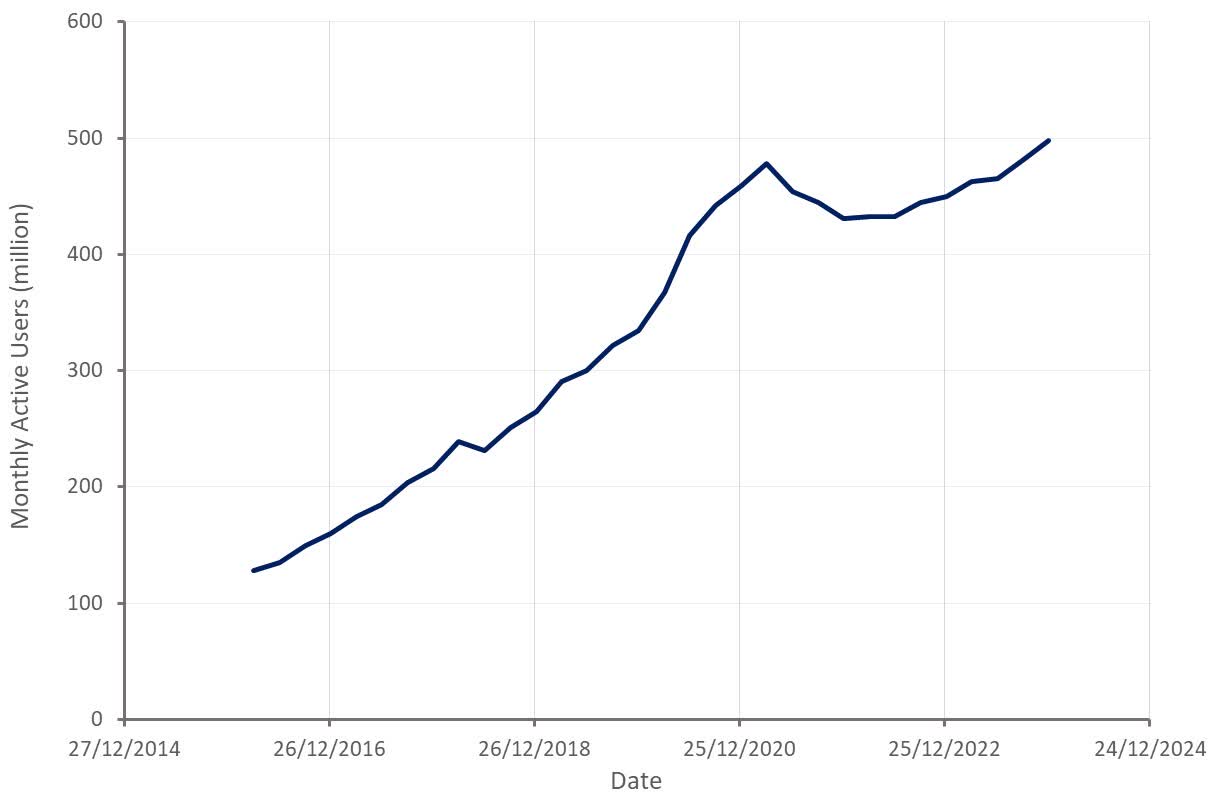

Pinterest's user base continues to expand at a healthy pace, with solid growth across geographic regions. International markets continue to drive the majority of user gains, though. Gen Z is Pinterest’s fastest growing demographic and now represents more than 40% of users on the platform. This is potentially supportive of the long-term health of the platform.

Figure 2: Pinterest Monthly Active Users (source: Created by author using data from Pinterest)

While Pinterest is likely reaching a saturation point in its more mature markets, there is still a significant opportunity to shift users from episodic to more recurring usage. Pinterest is leveraging AI to drive improvements in relevancy and actionability on its platform, contributing to improvements in engagement.

Pinterest is making it easier for users to find content, including using generative AI-based search guides, which help users move from broad queries to more defined searches and ultimately action.

Pinterest has also introduced colleges, a new interactive format composed of cutouts. This feature helps to engage users and provides Pinterest with a strong first-party signal on what users are interested in. Collages were rolled out to most iOS users globally in Q4, and feedback has reportedly been positive.

Pinterest also introduced an auto organization feature in Q4, which leverages AI to create Boards by automatically grouping similar pins based on user interests. For users who generally don't curate on the platform, this feature resulted in a nearly 30% lift in boards created.

Usage of Pinterest’s mobile app continues to outpace MAUs, reducing the company’s dependence on SEO. More than 80% of Pinterest’s users and revenue now come from the app. Engagement growth continues to outpace MAU growth, and ad impressions are outpacing engagement. Pinterest’s most recent user cohorts are also roughly twice as engaged as prior cohorts.

As a result of user growth, increased engagement and increased ad loads, Pinterest has been able to drive significant growth in impressions. Ad impressions increased 33% YoY in the fourth quarter due to a mix of total impressions and ad load.

Demand for Inventory

Pinterest is trying to attract demand to its platform by improving the performance of its ads and opening itself up to third-party demand. Pinterest has introduced a range of tools to assist advertisers, like shopping ads, the conversion API, direct links, and mobile deep linking. At the start of 2023, only 2% of Pinterest’s revenue came from customers who had adopted at least three of its lower funnel tools, a figure that has now reached to 23%. Approximately two-thirds of Pinterest’s revenue now comes from the lower funnel.

The company believes that by delivering sustained improvements in ROI for advertisers, it will receive increased budget allocations. Advertisers that have adopted the company's conversion API and privacy-safe measurement tend to be increasing spend in excess of 30%. Those that have not tend to be reducing spend in the mid-single digits. Pinterest also believes that it is shifting from advertisers’ experimental and social budgets to their performance budgets, which tend to be larger and more resilient.

Pinterest is also trying to bring more automation to the campaign creation experience. For example, automated bidding is now responsible for 85% of Pinterest’s revenue. Pinterest wants to steadily increase automation and reduce the time and effort required for advertisers to set campaigns up.

Pinterest launched its first third-party ad partnership with Amazon in 2023. Third-party partnerships are viewed as a way to fill demand gaps. Pinterest first focused on improving shoppability with Amazon and now international monetization with Google. Third-party ad demand is reportedly scaling as expected, although is not a significant revenue contributor yet. This should change in 2024, with partnerships anticipated to become a material growth driver.

While Pinterest is working to improve the performance of its ads and bring more demand to the platform, ad pricing was still down 16% YoY in the fourth quarter. This is particularly notable given that revenue has been shifting from brand advertising to more targeted advertising.

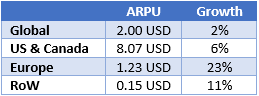

Table 1: Pinterest Average Revenue per User (source: Created by author using data from Pinterest)

Financial Analysis

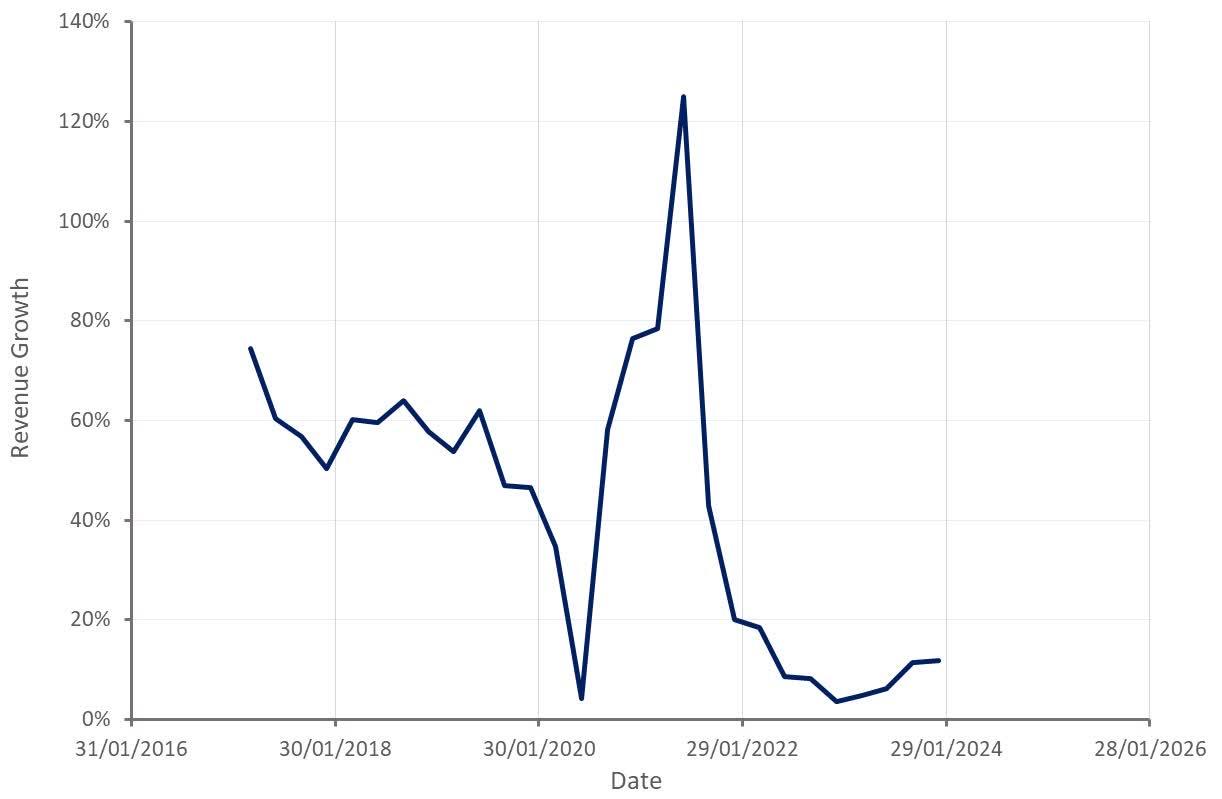

Pinterest’s revenue was 981 million USD in Q4, up 12% YoY. Growth missed expectations and was roughly flat sequentially, although no compelling reason was given for this.

Growth is expected to pick up in coming quarters, largely due to Pinterest-specific factors. Adoption of lower funnel advertising products is leading to improved performance for advertisers, who are in turn increasing their ad budget allocation to Pinterest. Pinterest launched direct links toward the end of 2023, doubling the clicks Pinterest drove for relevant advertisers in Q4. Third-party ad demand is also anticipated to become a more material contributor in 2024.

First quarter revenue is expected to be 690-705 million USD, representing approximately 16% YoY growth at the midpoint. Pinterest is targeting mid to high teens revenue growth over the next 3-5 years.

Figure 3: Pinterest Revenue Growth (source: Created by author using data from Pinterest)

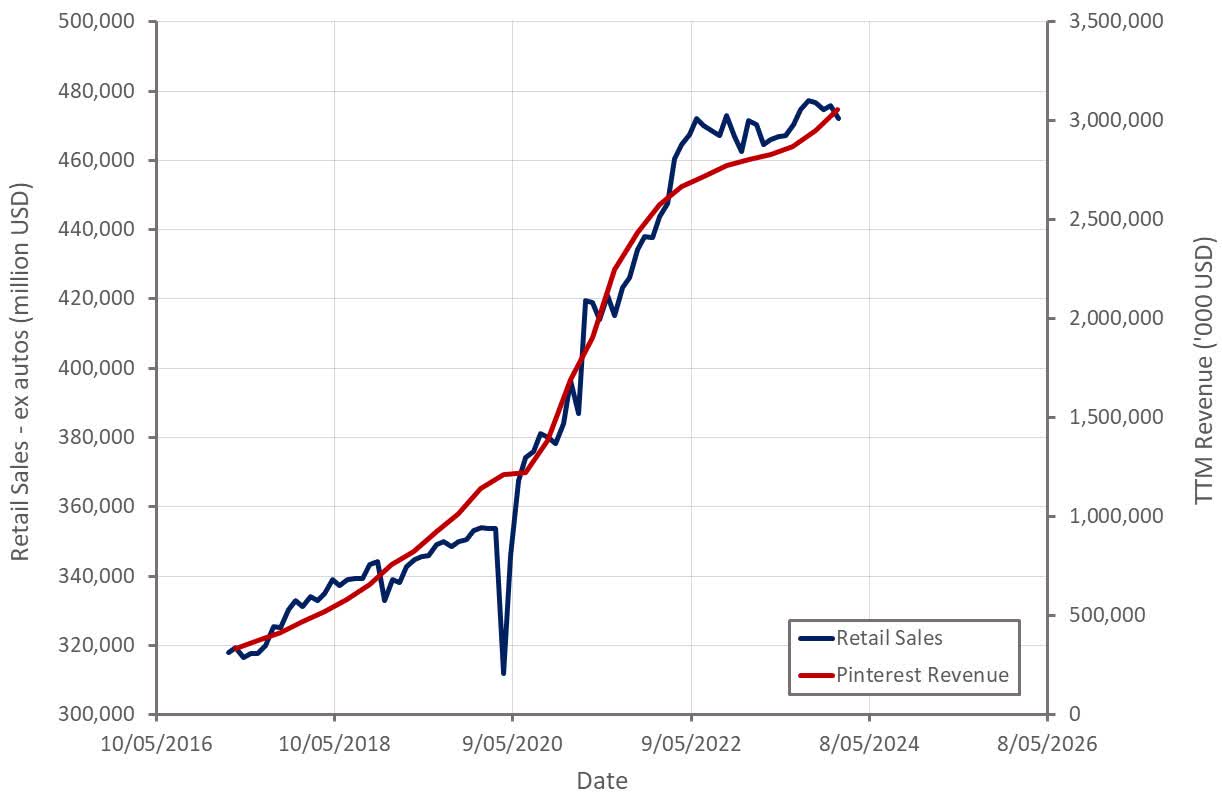

An expectation of improved growth is particularly notable given it is not being driven by consumer spending and comes in the face of ongoing pricing declines.

Figure 4: Retail Sales and Pinterest Revenue (source: Created by author using data from Pinterest)

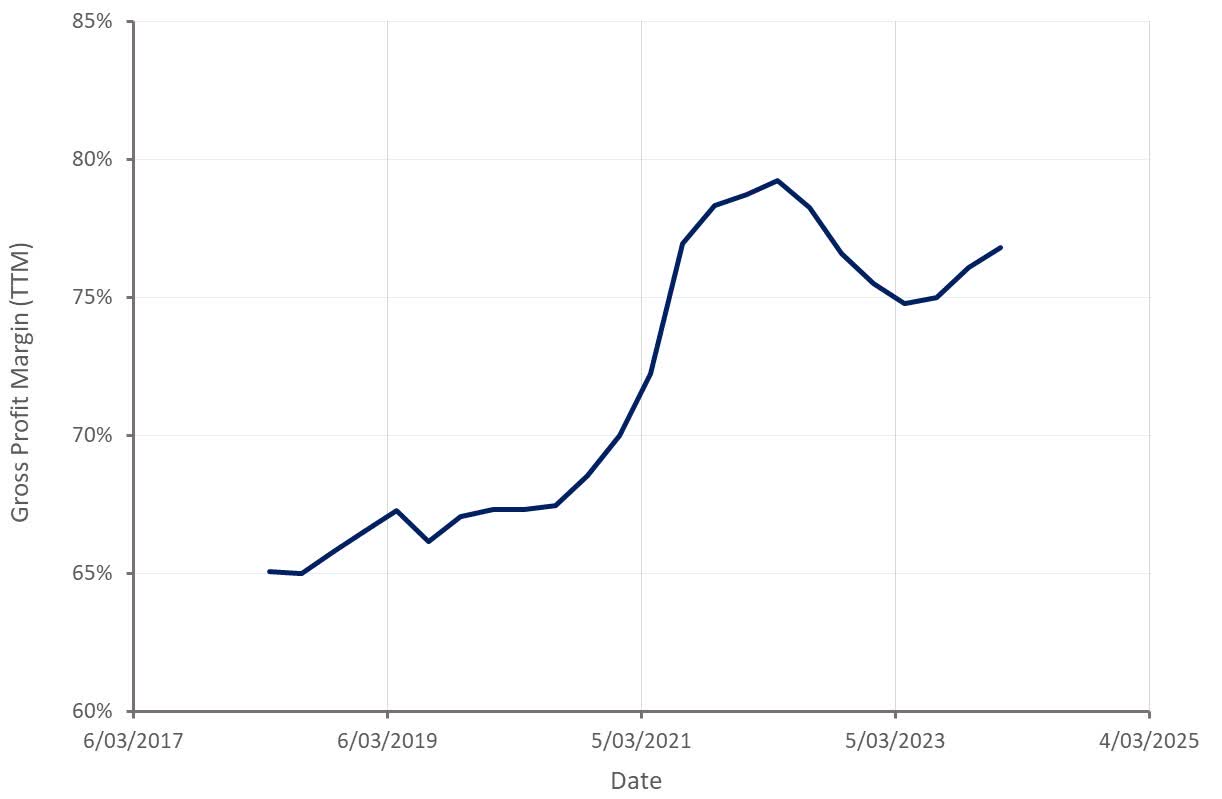

Pinterest's gross profit margins continue to move higher, which is a positive given ongoing pricing pressure and the growing importance of video. Video contributes more than 30% of Pinterest's revenue, and Gen Z tends to be more video centric.

Figure 5: Pinterest Gross Profit Margin (source: Created by author using data from Pinterest)

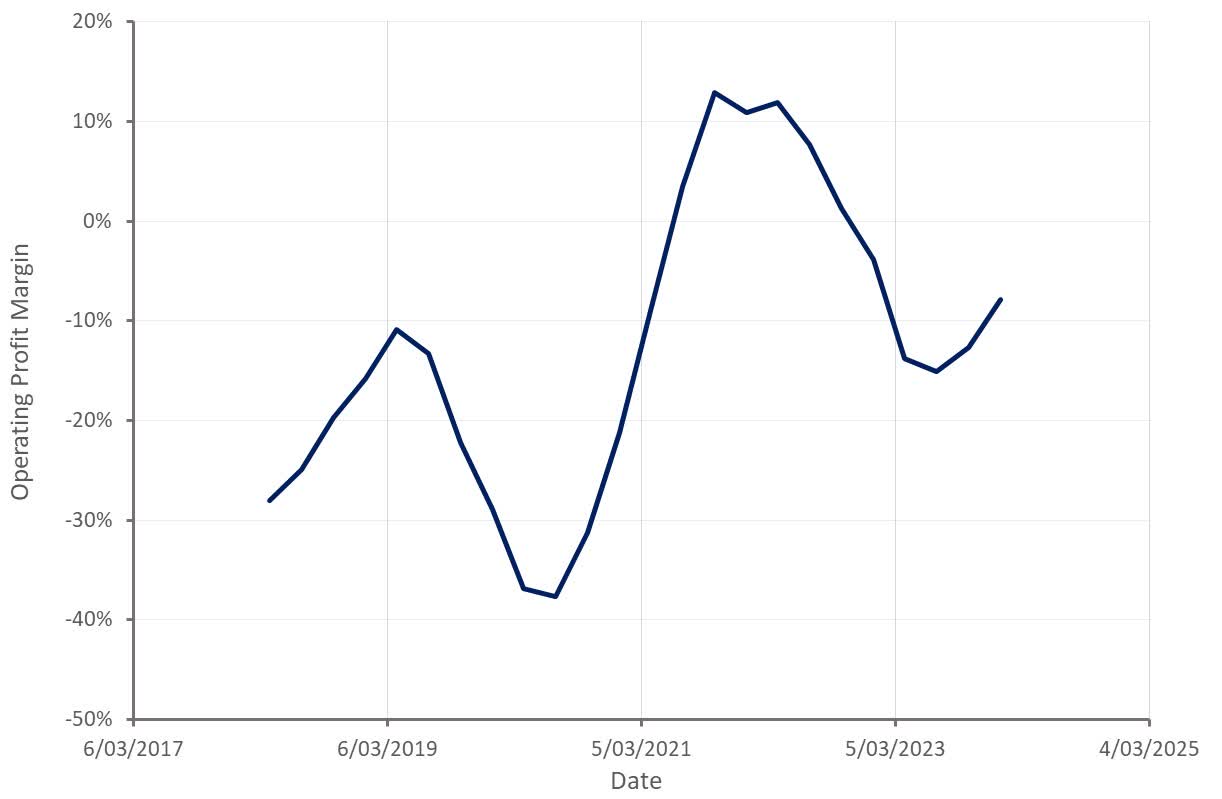

Pinterest's operating profit margins also continue to move higher. Investments in R&D and sales and marketing have been elevated, but the company should begin to reap some of the benefits of this in 2024. Pinterest is targeting an EBITDA margin in the low 30% range in the next 3-5 years.

Figure 6: Pinterest Operating Profit Margin (source: Created by author using data from Pinterest)

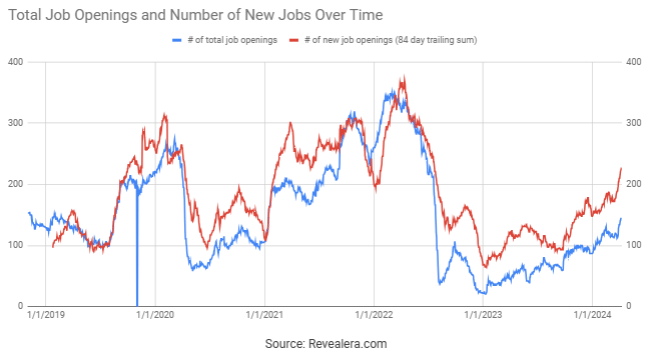

The number of Pinterest job openings has moved steadily higher since the start of 2023, suggesting an improving outlook for the company.

Figure 7: Pinterest Job Openings (source: Revealera)

Conclusion

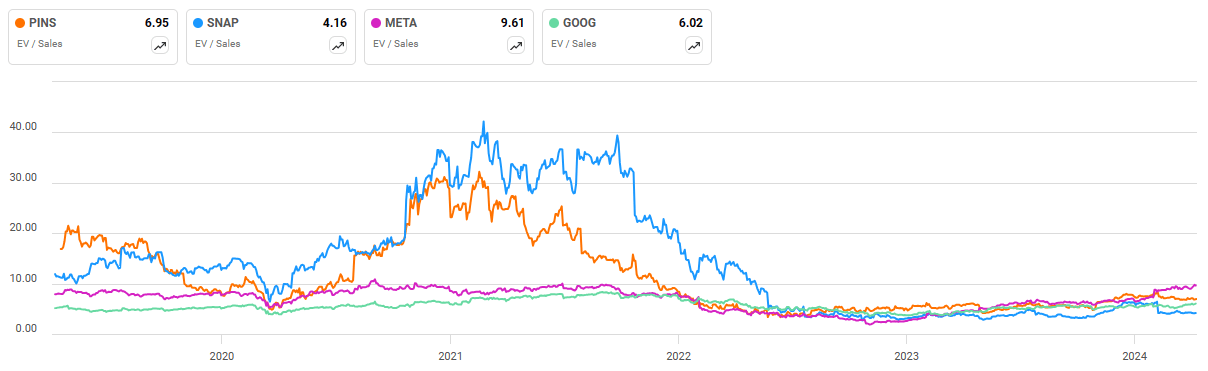

While Pinterest's current valuation may not appear low, investors must look forward to where the company's profit margins and cash flows will be in the next few years. Even if growth doesn't reaccelerate significantly, Pinterest's PE multiple should be below the market average over the next 3-5 years. Pinterest's strong balance sheet (large cash pile and limited debt) also supports the company's ability to return cash to shareholders.

Figure 8: Pinterest EV/S Ratio (source: Seeking Alpha)