Torsten Asmus

Since late October, large-cap U.S. stocks have seen a furious 25% rally based on the idea that the Fed will soon pivot and dramatically cut interest rates. The move in stocks has been driven almost entirely by a change in valuation and not a change in underlying earnings. I've looked high and low for evidence of an AI-driven earnings boom for stocks, but when you look at the actual data, S&P 500 (SPY) earnings have been roughly flat since 2022. The current scenario of rapidly-increasing valuations without a corresponding increase in profits is unsustainable. Now add in a series of reports that inflation isn't going away as planned, and the market has a problem.

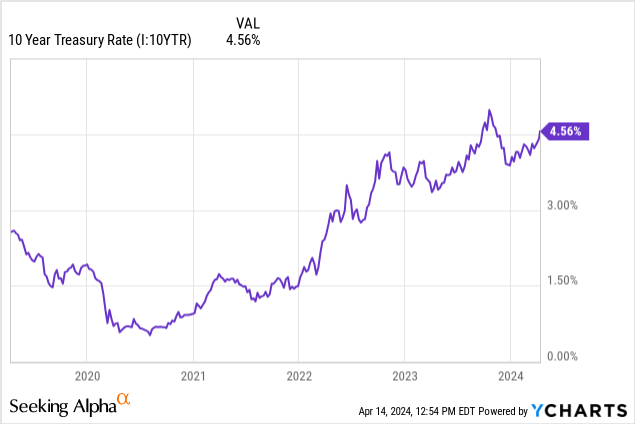

Yields have responded in kind, rallying to more than 4.5% last week as demand for bonds cools and budget deficit-driven Treasury supply continues unabated. In late summer last year, the 10-year yield suddenly rose to 5% after Fitch downgraded the U.S. government's credit. At the time, I compared the effects of rising interest rates to a freight train approaching the U.S. and global economy. This story quieted down this winter with the idea of a Fed pause and likely pivot starting in late October. Now it's back, the Fed can't cut rates with stubborn inflation, and long-term yields are threatening to hit new cycle highs. This has profound implications for housing, autos, banks, tech, and the stock market/economy at large. So far, the stock market has barely moved off of all-time highs, but this is a potential black swan for markets expecting a return to ultra-easy monetary policy. Since this six-month rally in stocks wasn't based on increased earnings, I think it's likely to reverse.

Yields Are Already Near 20-Year Highs

Treasury yields are significantly higher than a year ago. This time last year, the 10-year yield was hovering between 3.3% and 3.5% while the market digested the after-effects of last spring's short-lived bank crisis. Treasury yields are now above 4.5% as of my writing this, with significant upward momentum to boot. The effect is more pronounced in the mortgage markets where failed banks like First Republic operated. This time last year, you could get a jumbo mortgage for 5.96% on average, but now it will cost you 7.51%. For each $1,000,000 in mortgage you take out, your current payment would be $6,999 per month, vs. $5,970 at this time last year.

Insurance costs are through the roof and property taxes are up significantly as well. What happens when millions of U.S. homebuyers see their homebuilder-financed teaser rates expire? We're going to find out. These are all natural consequences of the money-printing binge from 2020 and 2021, and the consequences are now just starting to be felt. We can trace similar effects in the auto market. Carmax (KMX) just reported earnings, and the stock was pummeled after the company missed on earnings, citing affordability pressures, tighter lending standards, and rising insurance costs. Is the problem just with Carmax, or are they onto something? All of this is happening at current levels of interest rates.

Economics 101: Yields Could Go Much Higher

There are theoretical and practical reasons to believe rates should continue to go higher. JPMorgan (JPM) CEO Jamie Dimon recently highlighted the risk of 6% rates in his annual letter to shareholders. 2024 inflation reports have come in hotter than expected, echoing historical patterns where inflation is hard to stamp out. Theoretically, there are reasons to expect yields to rise as well. The CBO expects the U.S. budget deficit to be 5.6% of GDP for 2024. This is probably inflated because student loan forgiveness is baked into these and it's doomed in court, but the budget deficits are honestly quite reckless. Sustainable budget deficits are thought to be in the 3%-4% range, which would require immediate tax hikes of about 1.5% to 2% of GDP. What happens when the government wants to spend money without raising taxes to pay for it? They have to borrow the money to do so. This puts upward pressure on yields.

Mainstream economic theory says that excessive government borrowing will "crowd out" the private sector. To put this in practical terms, the Biden administration needs to borrow many trillions of dollars to finance increased military spending, the green energy transition, and the social programs they want. But doing so without paying for it with tax increases drives up yields, "crowding out" potential homebuyers looking for mortgages, small businesses looking for loans, etc. There always are inherent tradeoffs between government spending and the private sector. This is a structural problem. In an attempt to solve it during COVID, Congress decided to test out modern monetary theory. In 2020 and 2021, the government borrowed a ton of money, and they had the Fed buy basically all the debt they issued. Printing money and spending it predictably led to runaway inflation. If you're in power and want to spend money without raising taxes, you're bound to increase yields. And if you make your central bank print money to cover the deficits, you're bound to cause a surge in inflation.

Neither borrowing money nor printing it is a magic trick. Our society's resources are what they are, and politics can only redistribute them in the short run, not fundamentally solve the problem of scarcity. The reason why millions of Americans are struggling with the cost of living is because the government printed too much money during COVID. And now the reason that millions of Americans can't buy homes is because the Feds are crowding them out by investing billions in pork-barrel projects in swing states. What happens next? The government won't slow down its spending, and they (probably) won't raise taxes, so yields are liable to hit new highs in 2024. Taken to its logical conclusion, that means the potential for 6% Treasury yields, 9% mortgage rates, and 8% car loan rates.

Recent History Also Shows The Potential For Higher Rates

Readers might expect me to draw parallels with the 1970s to show how high interest rates might go. We don't have to go back that far though. During the 1990s, prevailing nominal 10-year interest yields were above 6% for most of the decade, most notably during the dot-com bubble when yields peaked near 7%. Then, government budget deficits were much lower than today (or nonexistent in some years), and inflation was lower.

Looking at real yields (10-year yields less inflation), we see that the typical inflation-adjusted yield in the 1990s averaged about 3%. This was during a time of minimal government deficits. During the dot-com bubble, real yields were closer to 3.5%. During the 1980s when markets were more concerned with Reagan-era deficits after the inflationary 1970s, real yields closer to 4% were the norm. In this historical context, it's not difficult to justify yields of 5.5% to 6.5%, even with inflation at relatively benign levels. 2.5% inflation plus a 3.5% real yield gets you a nominal 10-year Treasury yield of 6%. Another plausible scenario of 3% inflation plus a 3% real yield would yield an identical result. Given the crazy levels that government deficits are currently at, I think these numbers are conservative if anything. The Clinton administration was famously crushed by the bond market in the 1990s and forced to raise taxes to finance its spending, and the second Biden or Trump administration could find itself repeating history.

The Economy Is Built On A Foundation Of 0% Rates

Short-term interest rates were roughly 0% from late 2008 to early 2022, and rates for mortgages and corporate debt were extremely low as well. This allowed thousands of unprofitable companies to stay in business and allowed millions of people to build their business models around cheap financing. Stock valuations gradually rose over this time, first from levels that were unusually low, then to normal levels, then to high levels, and finally to bubble levels. Popular housing markets also increasingly detached from fundamentals like rents or local salaries.

No one seems to be considering the possibility that yields could rise another 150 bps this year, despite the government running fiscal policies that are custom-made to cause it to happen. As yields continue to rise, expect there to be consequences. I wouldn't expect the Fed to be able to rescue this, either. The Fed could easily cut short-term interest rates and steepen the yield curve, but that's no guarantee that 10-year yields would go down. If rate cuts cause the market to expect more inflation in the future, long-term yields could go up. If the Fed were to reverse its policy of shrinking the balance sheet, inflation would likely break out and surge again. The Fed is more or less stuck letting the market set yields after shattering the public's trust during COVID.

The housing market is still priced as if mortgages were at 4%, automakers still make $80,000 trucks designed to be financed at 84 months, and hundreds of money-losing stocks can only stay in business by borrowing money at ultra-low rates. These business models don't work so well with interest rates no longer at zero. For the entirety of the 2010s and early 2020s, savers were losers while borrowers and speculators were huge winners. With the temperature set to turn up a few more degrees on yields, I'd expect some cracks are forming in the economy. The upshot to savers perhaps no longer being losers – you can make good money in money markets, and niche investments like preferred stocks and merger arbitrage plays.

Bottom Line

Given that theory, history, and common sense indicate the potential for yields to continue to rise, investors should consider the possibility that Treasury yields will soon rise to 6% or higher. Is this a black swan in plain sight? Perhaps. No one seems to think yields can go higher, and many investors think that if yields start to get out of line, the Fed will simply wave a magic wand to make them go back down. This line of thinking is wrong – the only solution to the rising yield problem is to sharply raise taxes or cut government spending. Unless and until either of these happens, 10-year yields are liable to hit 6%, mortgages 9%, and used car loans 8%. We can debate the consequences this would have on the stock market, but I certainly wouldn't be buying stocks for a ~4% earnings yield when you can get 6% guaranteed instead in Treasury bonds.