Emerson Automation Solutions office in Calgary, Alberta, Canada

JHVEPhoto/iStock Editorial via Getty Images

In June 2023, I published my article about Emerson Electric (NYSE:EMR) which was in the restructuring phase at that time. The acquisition of new subsidiaries has largely been completed to date, as confirmed by Emerson's management.

Among the most important changes, it should be mentioned that last October, Emerson completed the acquisition of National Instruments in an 8.2 billion dollar transaction. I think that investors' hesitation about Emerson a year ago is gone today.

Restructuring in recent years has been successful for Emerson Electric. This is confirmed by the fact that in two of the last three quarters, the company has beaten profit forecasts by double-digit percentages. The projections for the future years for this company offer decent growth in both revenue and profit. Emerson's restructured business model is aimed at faster growing industries and takes into account factors caused by climate change. Despite the recent rise in Emerson's stock price, I think it is sustainable for it to continue. Also, in my opinion, the company has better opportunities for faster dividend growth in the future.

Business Structure

Since Emerson Electric has undergone significant renewal in recent years, let's take a closer look at the company's business segments below. The company has two business segments: 1. Intelligent Devices 2. Software and Control.

They are divided into sub-segments. The sub-segments of Intelligent Devices are: Final Control, Measurement & Analytical, Discrete Automation, Safety & Productivity.

Final Control offers various types of valves, actuators and regulators. They regulate the flow of liquids and gases. The revenue of this sub-segment was $3.97 billion in 2023, which is 26% of the company's total revenue.

The Measurement and Analytical segment offers devices that measure the physical properties of liquids and gases. The received data is transferred to control systems, where the production process is adjusted based on it. The revenue of the Measurement and Analytical sub-segment was $3.60 billion last year, or 23.6% of the company's total revenue.

The Discrete Automation sub-segment supplies the discrete manufacturing industries with various devices such as solenoid valves, pneumatic valves, pressure and temperature switches, etc. This sub-segment contributed $2.64 billion in revenue in 2023, or 17.31% of Emerson's total revenue.

The Safety and Productivity sub-segment offers different types of tools for professionals and homeowners. This includes pipe wrenches, pipe cutters, pipe threading equipment, sewer inspection cameras, etc. This sub-segment contributed approximately 9% of the company's total revenue, or $1.39 billion.

The Software and Control sub-segments are:

Control Systems & Software. This sub-segment offers control systems and software that control factory processes based on information from measuring devices. This sub-segment contributed $2.61 billion in revenue in 2023, which is roughly 17% of the company's total revenue.

AspenTech is also a sub-segment of the segment under review. Emerson owns a 55% stake in this company. Aspen Tech provides asset optimization software for various industries. The Australian mining sector is particularly important in this respect. AspenTech generated $1.04 billion in revenue for Emerson last year. That's 6.8% of Emerson's total revenue.

National Instruments, a company acquired last year, is reflected as a new sub-segment, Testing and Measurement. This includes software-connected test and measurement systems that enable companies to optimize manufacturing processes. I don't have detailed information about the revenue share of this new sub-segment.

Emerson's Prospects For The Future

As Emerson Electric's business has now been completely restructured, it is not possible to make future predictions based on past data. Therefore, below, I will try to analyze the growth prospects of the most important industries served by Emerson. The company sees the greatest future growth opportunities in the LNG, nuclear, life sciences and mining industries.

The LNG market will likely grow by an average of 6.75% per year until 2029. If in 2023 the size of this market was $73.60 billion, then by 2029 it is predicted to be $103.41 billion. The reason for the increase is the growing demand for gas energy and the increase in the number of fleets running on liquefied natural gas. The growth of the LNG market is also due to the desire to reduce carbon dioxide and greenhouse gas emissions. It will be replaced by cleaner forms of energy, including natural gas. Emerson's renewed product portfolio includes several devices that can be offered to the LNG market.

In the nuclear sector, small SMR reactors and life extension of nuclear power plants are important areas for Emerson. These devices use components manufactured by Emerson. Based on the forecast, the SMR reactor market will grow by 8.7% annually in the period 2023-2032. If in 2022 the size of this market was $5.8 billion, then by 2032 it is predicted to be $13.4 billion. The North American region, which is Emerson's main home market, has the largest market share in this field. However, the fastest growing region is the Asia-Pacific region.

The life science analytics market will also grow at approximately the same pace, or 8.63% CAGR, in the following decade.

Life Science Analytics Market Size 2022-2032 (precedenceresearch.com)

The size of the life science analytics market is broadly on the same scale as the SMR reactor market. If in 2023 it was $10.27 billion, then by 2032 it is predicted to be $24.12 billion. At the same time, North America accounted for 52% of the market in this field in 2022. By comparison, about 41% of Emerson's revenue came from the US last year. However, the fastest CAGR of 10.5% in the following decade is expected in the Asia Pacific market, where Emerson is relatively modestly represented.

The fourth important area for Emerson is the mining industry, as its subsidiary AspenTech offers a variety of equipment to mining companies. While the global mining market is projected to grow at a modest 5.5% CAGR over the next 5 years, the Australian mining market is expected to grow at a CAGR of as much as 11% until 2030. In 2023, the size of the Australian mining market was $53.6 billion. By 2030, this market is projected to be $111.2 billion.

Australia Mining Market Analysis 2023-2030 (globenewswire.com)

Through its subsidiary AspenTech, Emerson has access to this fast-growing market. AspenTech's cooperation partners are large mining companies such as BHP Group (BHP), Rio Tinto (RIO), Fortescue (OTCQX:FSUMF) and others. The catalyst for progress in the mining sector is the rapidly growing Electric Vehicle market, which requires lithium and copper to produce batteries. This, in turn, is again related to the world's climate problems. As can be seen, the key to Emerson's new product portfolio is to bet on one important trend, which is the fight against climate warming. This is indicated by the company's efforts in the field of LNG, nuclear energy and equipment for the mining sector.

Emerson's Quarterly Results Continue To Beat Estimates

In my analysis of Emerson last June, I offered one measure of restructuring success as the extent to which the company can beat analysts' forecasts. Today, it can be stated that in two out of three quarterly results, the company has been able to significantly exceed profit forecasts.

Emerson`s EPS -Actual vs Consensus (Seeking Alpha)

In both cases, earnings surprises have been around 17% better than forecast. In the 4th quarter of 2023, it fell short of the forecast, but only by a minimum of 1.37%. At the end of May 2023, when the referenced article was completed, analysts' forecasts for Emerson's 4th quarter results of the same year were slightly more modest - $1.25. Therefore, it can be said that in fact the company's 1.29 Q4 2023 EPS also somewhat exceeded the then forecasts.

The company's sales of $4.12 billion also beat analysts' estimates by $210 million in the latest quarter.

Although based on the last three quarters, it is still not possible to give a very definite assessment, it still seems that the restructuring has been effective, and the company is moving in a positive direction. I think that the premium paid for the acquisitions has paid for itself because the profit received for it has been higher than predicted.

Decent Profitability Supports Faster Growth

We previously saw that organic growth in key markets for Emerson such as LNG, SMR reactors and life sciences is expected to be 7-9% over the coming decade. I think that Emerson is capable of growing its profits in the next decade at a faster pace than the mentioned 7-9% per year. This is primarily due to the high demand for his high-quality products. This is also reflected in good profitability metrics when looking at a longer time period.

Next, let's take a look at the company's return on equity over the past ten years. Although in the last few years Emerson's ROE has declined and slightly distorted due to restructuring and rising interest rates, in the period 2014-2021 this metric has been mostly above 20%.

| Year | 2014 | 2015 | 2016 | 2017 | 2018 |

| Emerson's ROE | 21.88% | 27.19% | 22.06% | 21.05% | 27.57% |

| 2019 | 2020 | 2021 | 2022 | 2023 |

| 26.17% | 24.9% | 27.26% | 10.82% | 8.94% |

Emerson Electric's ROE 2014-2023 source: Seeking Alpha

The company's 10-year average ROE in the period 2014-2023 has been 21.78%. Emerson's retention ratio is currently 57.36%. (100 - payout ratio 42.64%=57.36%).

Therefore, by multiplying the company's 10-year average ROE and retention ratio, we get Emerson's sustainable growth rate of 12.49%. This is close to the average annual EPS growth forecast by analysts for the next 5 years, which is 10.96%.

So I think it is likely that Emerson's earnings growth will be in the range of 11-12% per year over the next 5 years. Based on this, it can be argued that the company's growth will be faster than the 7-9% organic growth of its main industries.

Continuing Share Buyback Program

In addition to growing profits, Emerson investors can count on a steady reduction in the number of shares outstanding. This slightly increases profit per share. For this year, the company has planned to buy back its own shares worth $500 million. At the company's current market capitalization of $65 billion, this gives the investor an additional 0.76% value per share.

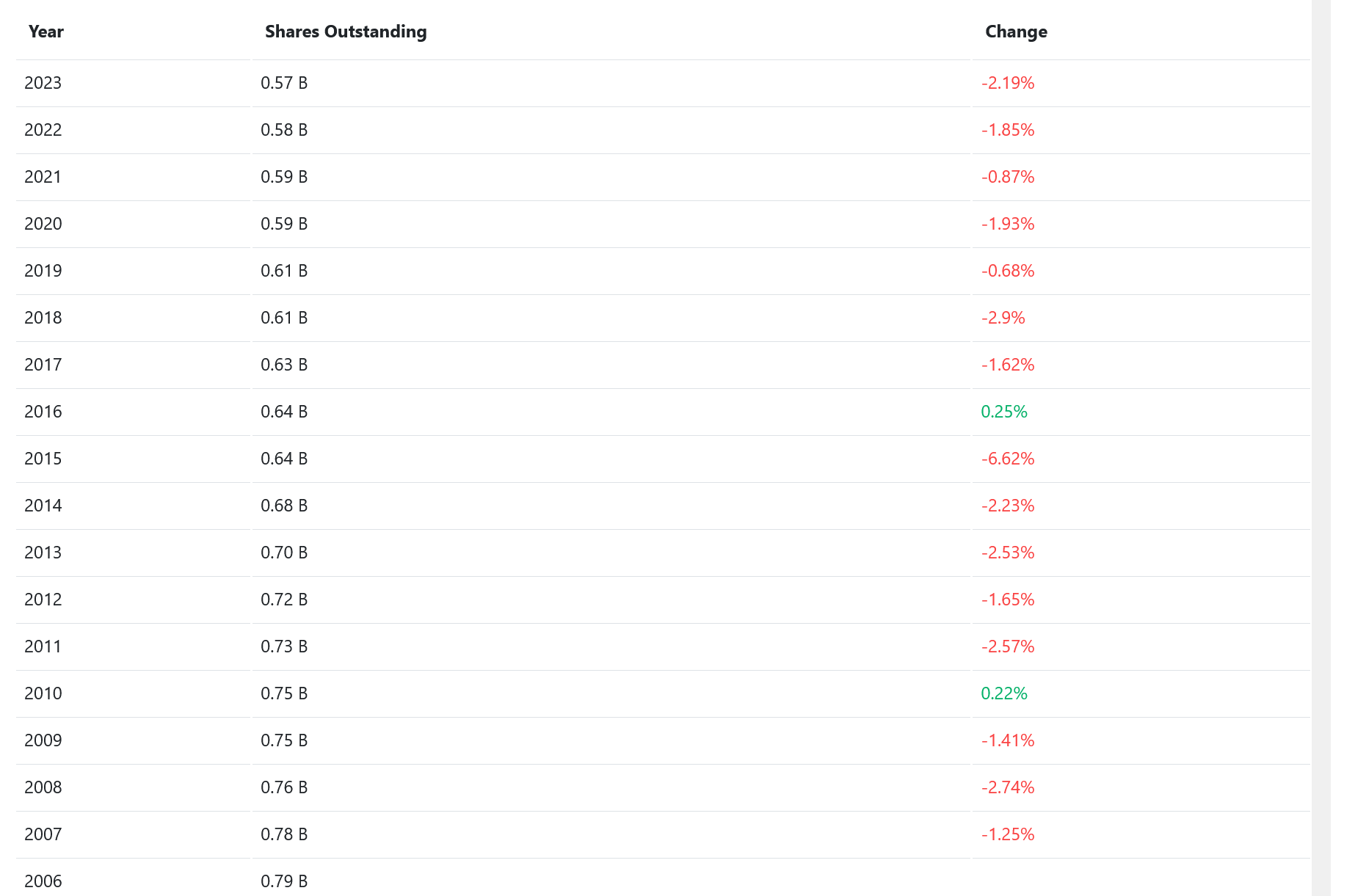

Emerson's share buyback policy has been consistent and has lasted for many years. The following table provides an overview of the company's share buyback history in the period 2006-2023.

Change in the number of Emerson Electric shares 2006-2023 (CompaniesmarketCap.com)

The table shows that over the past 18 years, Emerson Electric has repurchased an average of 1.81% of its shares each year. In just two years during this period, the number of shares has increased slightly. It can be said that in addition to a consistent dividend policy, the company also has a consistent share buyback policy.

Dividend Growth Is Expected To Increase

In the period 2016-2023, Emerson's average annual dividend growth has been only 1.27%. However, in the period 2006-2015, the dividend of this company grew by an average of 8.44% per year. Since 1990 to date, the dividend CAGR has been 5.86%. The chart below shows Emerson's dividend growth over the period 1989-2023.

Year | Payout Amount | Year End Yield | Annual Payout Growth (YoY) | CAGR to 2023 |

|---|---|---|---|---|

| 2023 | $2.0850 | 2.15% | 0.97% | - |

| 2022 | $2.0650 | 2.21% | 1.72% | 0.97% |

| 2021 | $2.0300 | 2.30% | 1.25% | 1.35% |

| 2020 | $2.0050 | 2.68% | 1.78% | 1.31% |

| 2019 | $1.9700 | 2.86% | 1.29% | 1.43% |

| 2018 | $1.9450 | 3.72% | 1.04% | 1.40% |

| 2017 | $1.9250 | 3.24% | 1.05% | 1.34% |

| 2016 | $1.9050 | 4.14% | 1.06% | 1.30% |

| 2015 | $1.8850 | 4.96% | 7.10% | 1.27% |

| 2014 | $1.7600 | 3.72% | 6.02% | 1.90% |

| 2013 | $1.6600 | 3.17% | 3.11% | 2.31% |

| 2012 | $1.6100 | 4.19% | 12.20% | 2.38% |

| 2011 | $1.4350 | - | 6.30% | 3.16% |

| 2010 | $1.3500 | - | 1.89% | 3.40% |

| 2009 | $1.3250 | - | 7.72% | 3.29% |

| 2008 | $1.2300 | - | 13.10% | 3.58% |

| 2007 | $1.0875 | - | 16.94% | 4.15% |

| 2006 | $0.9300 | - | 10.06% | 4.86% |

| 2005 | $0.8450 | - | 4.64% | 5.15% |

| 2004 | $0.8075 | - | 2.38% | 5.12% |

| 2003 | $0.7888 | - | 1.45% | 4.98% |

| 2002 | $0.7775 | - | 1.30% | 4.81% |

| 2001 | $0.7675 | - | 5.50% | 4.65% |

| 2000 | $0.7275 | - | 9.19% | 4.68% |

| 1999 | $0.6663 | - | 10.12% | 4.87% |

| 1998 | $0.6050 | - | 9.50% | 5.07% |

| 1997 | $0.5525 | - | 9.95% | 5.24% |

| 1996 | $0.5025 | - | 9.24% | 5.41% |

| 1995 | $0.4600 | - | 15.00% | 5.55% |

| 1994 | $0.4000 | - | 8.84% | 5.86% |

| 1993 | $0.3675 | - | 5.38% | 5.96% |

| 1992 | $0.3488 | - | 4.49% | 5.94% |

| 1991 | $0.3338 | - | 4.71% | 5.89% |

| 1990 | $0.3188 | - | 114.29% | 5.86% |

| 1989 | $0.1488 | - | - | 8.07% |

Emerson Electric dividend growth 1989-2023. Source: Seeking Alpha

I think that in the coming years, EMR will be able to regain its usual dividend CAGR of 5-7%. Such a growth rate of dividends is supported by the double-digit projected growth rate of the company's profit for the next five years. At that dividend growth rate, I believe Emerson will have enough free cash to expand the company to benefit more from the ongoing industrial automation revolution.

The company's current (non-GAAP) dividend payout ratio is a safe 42.74%. This is even lower than the five-year average for the corresponding metric, which is 50.33%. I think that an average 5-7% dividend CAGR in the coming years also meets the expectations of investors. A lower dividend growth rate would indicate that management is planning aggressively to expand the business. However, its success may be questionable.

Emerson's new product portfolio now seems to have justified itself, as the company's profits are growing strongly. This gives the investor the opportunity to own a company in Emerson that is both a growth company and a dividend growth company at the same time. I think that an increase in the dividend growth rate in the future could definitely make this company even more attractive to investors.

The Company Is In Good Financial Health

Next, let's take a look at Emerson's financial health. The following chart provides an overview of the company's equity and total debt ratio over a longer time period 1995-2023.

chart Emerson's equity and total debt 1995-2023 (Seeking Alpha) (Seeing Alpha)

Emerson's debt-to-equity ratio as of the most recent quarter was 0.56. This is lower than the median of 0.73 over the past 13 years. The highest debt-to-equity ratio of this company during the period has been 1.18 and the lowest has been 0.41. Thus, the current rate of 0.56 can be considered a financially healthy level.

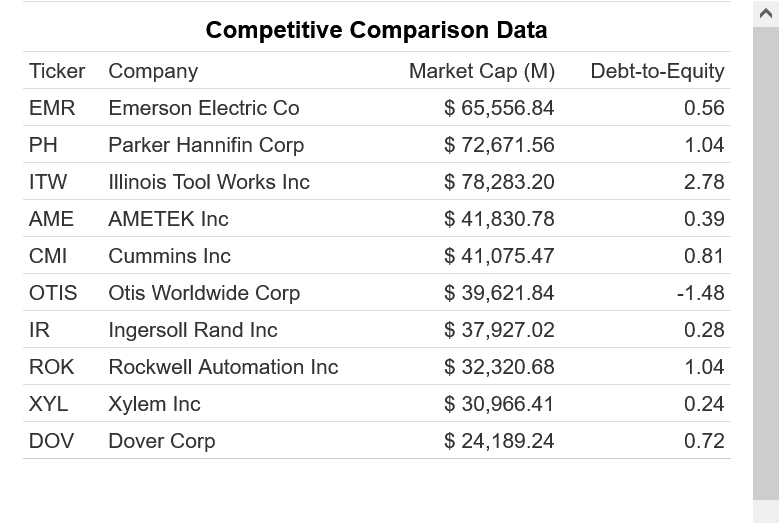

Emerson's debt/equity ratio compared to competitors (gurufocus.com)

The table above provides an overview of Emerson's debt/equity ratio compared to its competitors. Excluding Otis Worldwide (OTIS), six of the nine competitors have higher debt-to-equity ratios than Emerson. This suggests that Emerson's financial health is quite good.

Emerson's interest coverage ratio of 11.49 is currently very strong. For EBIT of $3.183 billion, interest expense is $277 million. True, in previous years this metric has been even stronger, as can be seen in the chart below.

Emerson Electric's interest coverage rate 2014-2023 (finbox.com)

Valuation

Since Emerson has been thoroughly restructured in recent years, I don't think it's wise to use relative valuation metrics to determine valuation. The reason is that Emerson today is very different from the same company five years ago. That's why I use the DCF method

Emerson Electric's intrinsic value (finmasters.com)

I used the 2024 free cash flow forecast of $2,655,000,000 as the free cash flow data because I think it's a more objective number than the current $634,000,000.

Other data used in the calculation are as follows: Total Cash $2,076,000,000, Total Debt $9,405,000,000 and Shares Outstanding 571,700,000. I used a conservative 5% as the expected growth rate for the next 10 years, although the company is projected to have an average annual profit growth of 11% for the next five years. I used 9% as the discount rate given the current interest rate environment. Based on the above data, I got an intrinsic value of Emerson stock at $126.2, indicating that the company is undervalued by 11.35%.

Given the undervaluation, I get Emerson's average annual total return for the next five years, including dividends, of 7.07%. I will describe this calculation process below. Emerson's earnings per share forecasts for the next 5 years are shown in the table below.

| Year | 2024 | 2025 | 2026 | 2027 | 2028 |

| EPS forecast | 5.40 | 5.89 | 6.51 | 7.08 | 7.47 |

Emerson Electric's EPS forecast 2024-2028 source. Seeking Alpha

The amount of the next 5-year earnings forecast is $32.35. Adding this amount to Emerson's intrinsic value of $126.2 gives us a result of $158.55. By putting the company's current share price of $112.65 and the closing price of $158.55 into the CAGR calculator, we get an average annual return of 7.07% for the next 5 years. Since EMR stock is currently 11% below its intrinsic value in my estimation, plus $5.4 in projected earnings per share this year, I rate Emerson a buy. I propose a target price for Emerson for the next 12 months of $129.5.

Risks

For Emerson, Trump's possible victory in the upcoming presidential elections is seen as one of the risk factors. Because Emerson operates in so many countries, tariffs may be imposed on Emerson products, among others, in response to Donald Trump's tariff policies. This would reduce the competitiveness of the company's products in foreign markets. Ingersoll Rand Inc. (IR), Kennametal Inc. (KMT), Flowserve Corp. (FLS) and some other industrial companies are at risk for the same reason.

Another risk factor is that Emerson stock is quite vulnerable during market downturns. For example, during the Great Recession in 2008, EMR stock fell 54%. In the period 2014-2015, its stock fell by 27%. The most recent decline occurred from June 2021 to February 2023, when Emerson stock again lost 27% from its peak. The vulnerability is increased by the fact that 76% of the company's shares are held by large institutional investors. Among them, The Vanguard Group has the largest holding, which owns 9.1% of Emerson's shares. If any of the major shareholders decide to sell their stake, it could cause a sharp drop in Emerson's stock.

Conclusion

Looking at the structural changes undertaken in Emerson Electric in recent years, the fact that the company's management is not just looking for growth opportunities, but sustainable growth opportunities, stands out. This is expressed, for example, in industries where new acquisitions have been made. LNG, nuclear energy and the mining sector have become important areas. They are all about providing solutions to climate problems. It is a growth strategy with a long-term vision. I think that this approach adds stability to the company's growth, which is very important from an investor's point of view. Although the restructured Emerson is still at the beginning of its journey, the latest quarterly results show positive surprises exceeding forecasts, confirming that the restructuring has been successful.