graemenicholson/E+ via Getty Images

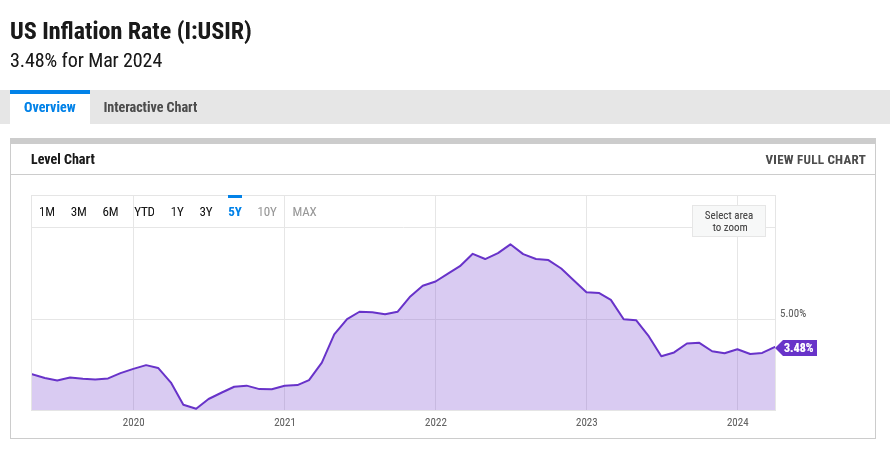

A couple of weeks ago, I penned a bullish article on giant specialty contractor EMCOR Group, Inc. (NYSE:EME) wherein I pointed out that the company, and the industry in general, are clearly benefiting from the trillion-dollar Infrastructure Investment and Jobs Act (IIJA), the Inflation Reduction Act (IRA) as well as secular trends such as AI, ML and electrification. The latest inflation data has prompted me to revisit the construction sector in general, and recently reiterated my Hold recommendation for tiny home builder Legacy Housing Corp. (LEGH). Construction is an inherently high-risk industry thanks to its broad exposure to macroeconomic factors such as commodity pricing, supply chain and labor dynamics, and housing demand. The increase in consumer prices has declined from a peak of 9.1% in mid-2022; however, the disinflationary trend has virtually stalled in recent months. In March, the CPI reading increased 0.4 percent, seasonally adjusted, and 3.5 percent over the last 12 months. That data has forced financial markets to scale back expectations: according to the CME FedWatch Tool, bond traders are betting a mere 19% probability that the Fed will cut rates at its June policy-setting meeting, down from 56% before the report came out. Meanwhile, interest rates have been gradually ticking higher, with the 10-Year Treasury yield up to 4.639% currently from 3.789% at the end of 2023. This scenario is further exacerbated by the fact that the U.S. economy is currently in the late stage of the business cycle, which does not favor consumer cyclicals.

U.S. Inflation Rate (YCharts)

That said, I believe that inflation and interest rates at current levels are more likely to be a problem for the residential housing sector than specialty builders like EMCOR and its peer MasTec Inc. (NYSE:MTZ). Unlike EME stock, which first appeared on my radar as the most overbought stock in the S&P 500, MTZ is fast approaching oversold territory with a 14-Day RSI reading of 41.7. The stock has so far pulled back 12% in April, with the selloff likely having been triggered by lingering fears about the health of the U.S. economy.

So, how’s MasTec a potentially profitable contrarian play? In one phrase, Pricing Power.

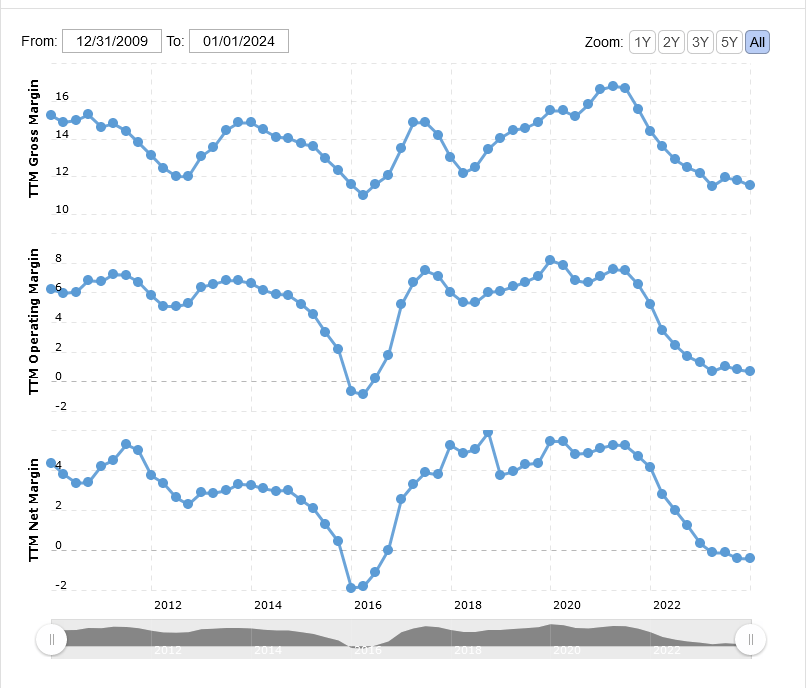

Over the past couple of months, MTZ actually enjoyed a very good run, doubling in value from November 2023 to early April 2024. I believe MTZ is a prime example of a company with weaker pricing power that has, lately, been benefiting from an improving business environment. As Goldman Sachs previously noted, “Unit labor costs have decelerated sharply and more quickly than inflation, supporting corporate profitability. Profit margins should also benefit from operating leverage in a solid economic growth environment. During periods of improving profitability, investors often reduce the scarcity premium assigned to strong pricing power stocks, and firms with less pricing power and more variable profit margins typically outperform.” Stocks with low pricing power are those ranking in the bottom 25% of their sector based on the level and variability of their gross margins during the past five years. With a gross margin of 11.59% vs. 30.67% sector median, coupled with worsening gross/profit margins, MTZ fits this contrarian thesis quite well. MasTec’s margins have deteriorated markedly over the past three years, suggesting weak pricing power.

MasTec Profit Margins (MacroTrends)

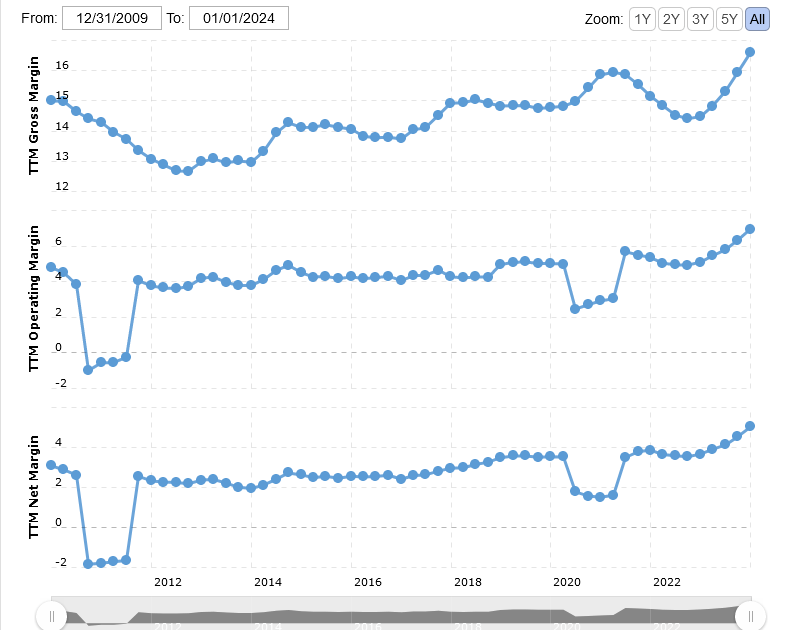

At 16.60%, EMCOR’s gross margin, too, is below the sector median. However, unlike MasTec, EMCOR’s margins have improved considerably over the past couple of years. Further, the company scores much better on key metrics such as Return on Common Equity (28.49% vs. -1.84%), Return On Total Capital (20.60% vs. 1.52%) and Return On Total Assets (9.58% vs. -0.53%), all of which are well above the sector median.

EMCOR Profit Margins (MacroTrends)

Upbeat Guidance

MasTec is coming off a mixed year when it managed to grow the top-line at a faster clip than its competitors but saw its bottom line contract. Q4 2023 Non-GAAP EPS of $0.66 beat by $0.22 while revenue of $3.28B (+9.0% Y/Y) beat by $20M. For the full-year, revenue was up 23% to $12.0 billion, compared to $9.8 billion for the prior year, but posted a GAAP net loss of $47.3 million, or a loss of $0.64 per diluted share, compared to net income of $33.9 million, or earnings of $0.42 per diluted share in 2022.

The company finished the year with an 18-month backlog of $12.4 billion, with sequential growth in each segment totaling $373 million. Only the company’s Oil & Gas segment recorded a backlog decrease from $1,740 million at the end of 2022 to $1,225 million at the end of 2023, which the company attributed to the expected 2024 completion of a large natural gas pipeline project.

Thankfully, the company provided very upbeat, long-term guidance:

Fourth quarter results were in line with our expectations after a challenging 2023. We look forward to the opportunities we have this year and expect to deliver record levels of revenue and adjusted EBITDA in 2024. Demand is very strong for our services, and I expect 2024 will position us to deliver double digit revenue and earnings growth in 2025 and beyond," Jose Mas, MasTec's Chief Executive Officer, commented.

For the current year, MasTec offered guidance as follows:

Full-year 2024 revenue of $12.5 billion, a record level.

Full-year GAAP net income and diluted earnings per share are expected to approximate $105 million and $1.04, respectively.

Full year 2024 adjusted EBITDA is expected to approximate $955 million, representing 7.6% of revenue, and adjusted diluted earnings per share are expected to approximate $2.69.

During the March earnings call, MasTec’s management reported that the company has significantly expanded its relationship with AT&T (NYSE:T), its biggest wireless customer. In addition to the maintenance contract the company announced in its third quarter call, AT&T expanded its scope and geographic territory on MasTec’s core wireless work. According to MasTec, this expansion, coupled with the recently announced complete swap-out of Nokia equipment to Ericsson equipment over a five-year period, is likely to single-handedly increase the company’s 2025 segment revenues by double-digits and improve margins. The expanded AT&T deal will also provide MasTec with great revenue visibility in the coming years. Communications is MasTec’s second-largest segment after Clean Energy & Infrastructure, contributing 27% of consolidated revenue in 2023.

Takeaway

MTZ stock appears to have benefited from deflationary tailwinds until the trend recently stalled. However, the recent increase in the inflation rate is more likely a temporary blip rather than a complete reversal in the downtrend. Bond traders have now tempered their expectations for the number of rate cuts starting March from five to just two, with a target range of 4.75%-5.00% to close out the year from the current target range of 5.25%-5.50%. Traders are betting a 30% chance that only one cut will be in the offering in 2024. In other words, the markets still expect inflation to [mostly] continue falling as the months and quarters roll on. We, probably, will see a few more blips whereby inflation ticks up 10 or 20 bps month-over month, but I believe the longer-term downtrend will hold till the end of the year. That’s bullish for MTZ stock. Further, the company appears to have laid the groundwork for years of robust growth thanks to the AT&T deal.

On the risk side of my thesis, MTZ will not be out of the woods, probably until inflation drops below 3.0%. According to UBS, companies with weaker pricing power have historically underperformed their stronger counterparts by a nearly 14% margin over the next 12 months whenever the two-year breakeven inflation exceeds 2.5%. With U.S. inflation a whole percentage point above that threshold, stocks with weaker pricing power like MTZ are likely to continue facing pressure whenever inflation data turns bearish.

I rate MTZ a Hold at this point.