Lingbeek

This article was coproduced with Leo Nelissen.

Putting a value on a stock is difficult – very difficult.

After all, it depends on a wide range of factors, including crowd psychology, greed, fear, and market momentum.

However, two other factors may be even more important, which are the expected earnings stream of a company and the interest rate used to discount those earnings.

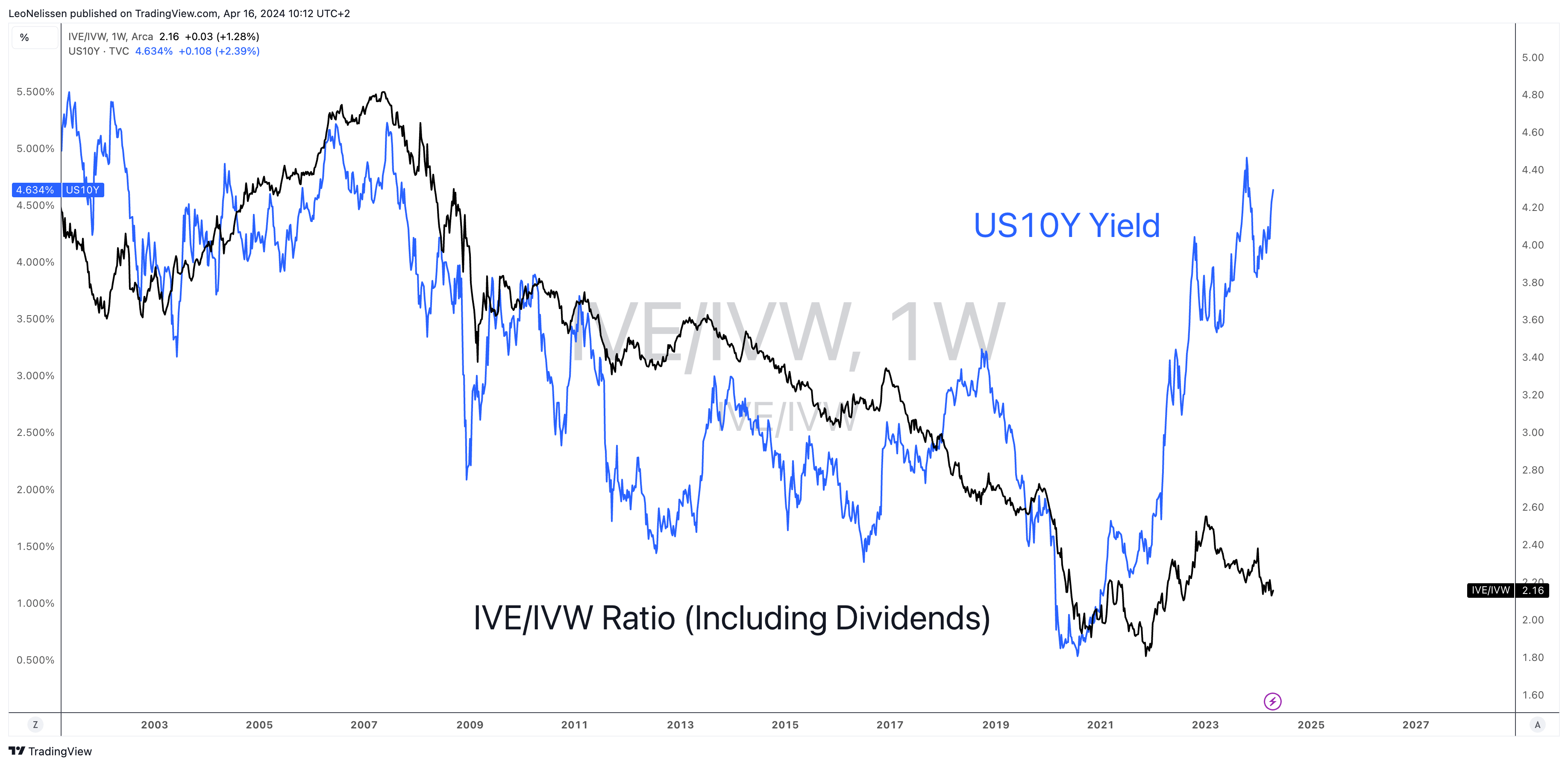

The chart below visualizes this relationship. It shows the ratio between the S&P 500 Value (IVE) and the S&P 500 Growth (IVW) ETFs. If we ignore the recent divergence, the ratio has been highly correlated to the yield on the 10-year U.S. government bond (US10Y).

TradingView - IVE/IVW Ratio, U.S. 10-Year Yield

This relationship makes a lot of sense.

Why?

That’s because, in an environment of rising rates, it becomes more attractive to buy companies that have high current earnings/cash flows.

In an environment of falling rates, the opposite happens, as it becomes more attractive to buy companies with high future earnings and cash flows.

In other words, discounting future growth is more attractive when rates are low. That makes “growth” stocks so attractive in these environments.

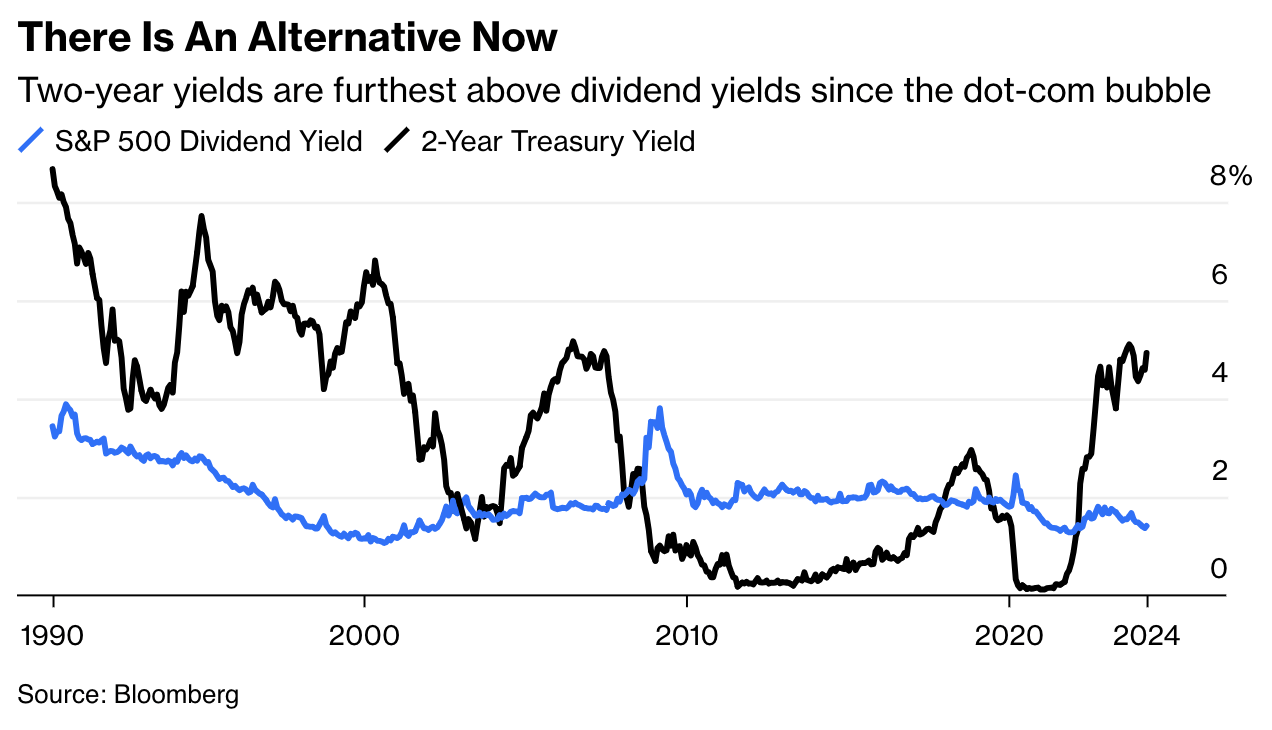

With that in mind, Bloomberg’s John Authers just reported that short-term bonds yield more than stocks.

This shift, labeled TINY (There Is No Yield), is very different from the long-standing TINA (There Is No Alternative) environment that supported stock valuations after the Global Financial Crisis.

Back then, growth stocks did extremely well, as the TradingView chart above shows as well.

Using the chart below, we see that short-term treasury yields are much higher than the S&P 500 (SP500) dividend yield. Between 2009 and 2018, the opposite was true.

Bloomberg

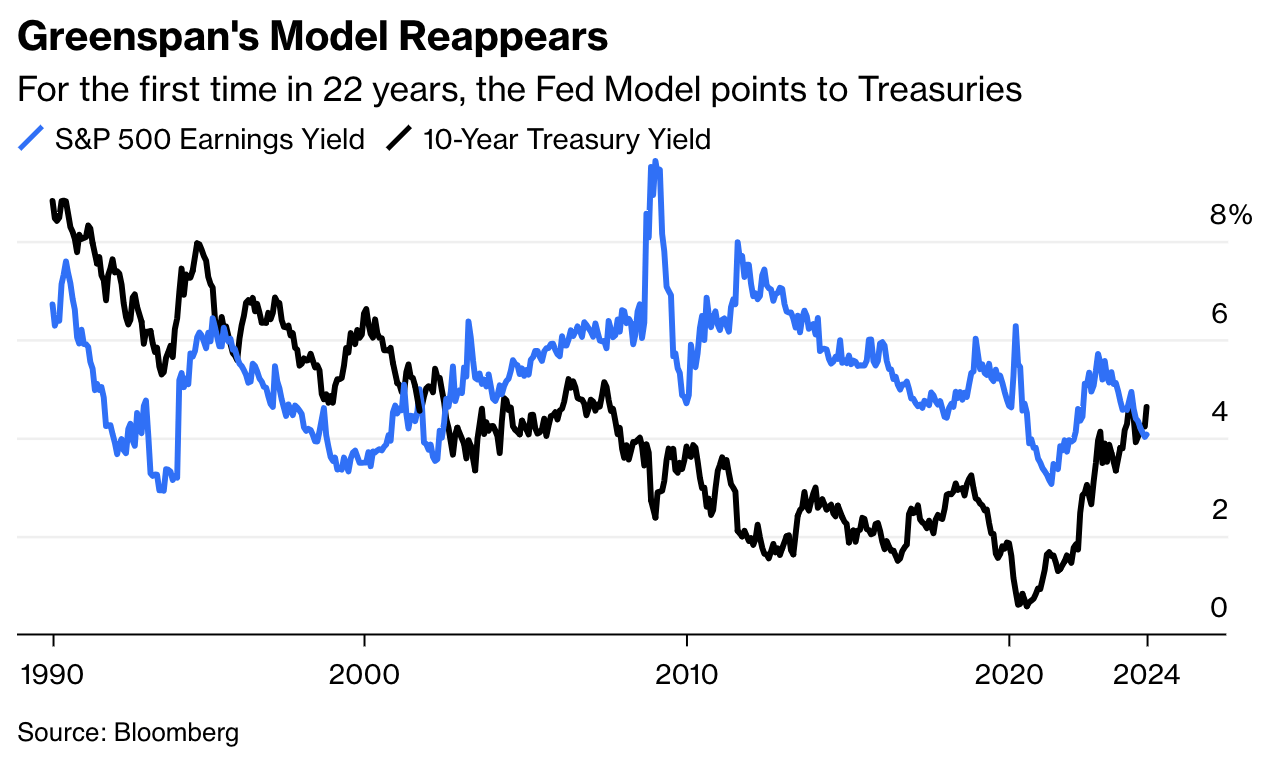

According to Mr. Authers, the resurgence of the “Fed Model” requires a reevaluation of the relationship between bond yields and stock earnings yield. After all, when it comes to yields, there’s much more to it than just the dividend.

Historically speaking, higher bond yields require an increase in the stock earnings yield as well. After all, stocks become increasingly less attractive when bond yields rise. Bonds have lower risks than stocks.

The earnings yield is the inverse P/E ratio. Currently, the earnings yield is lower than the yield on the 10-year government bond.

Bloomberg

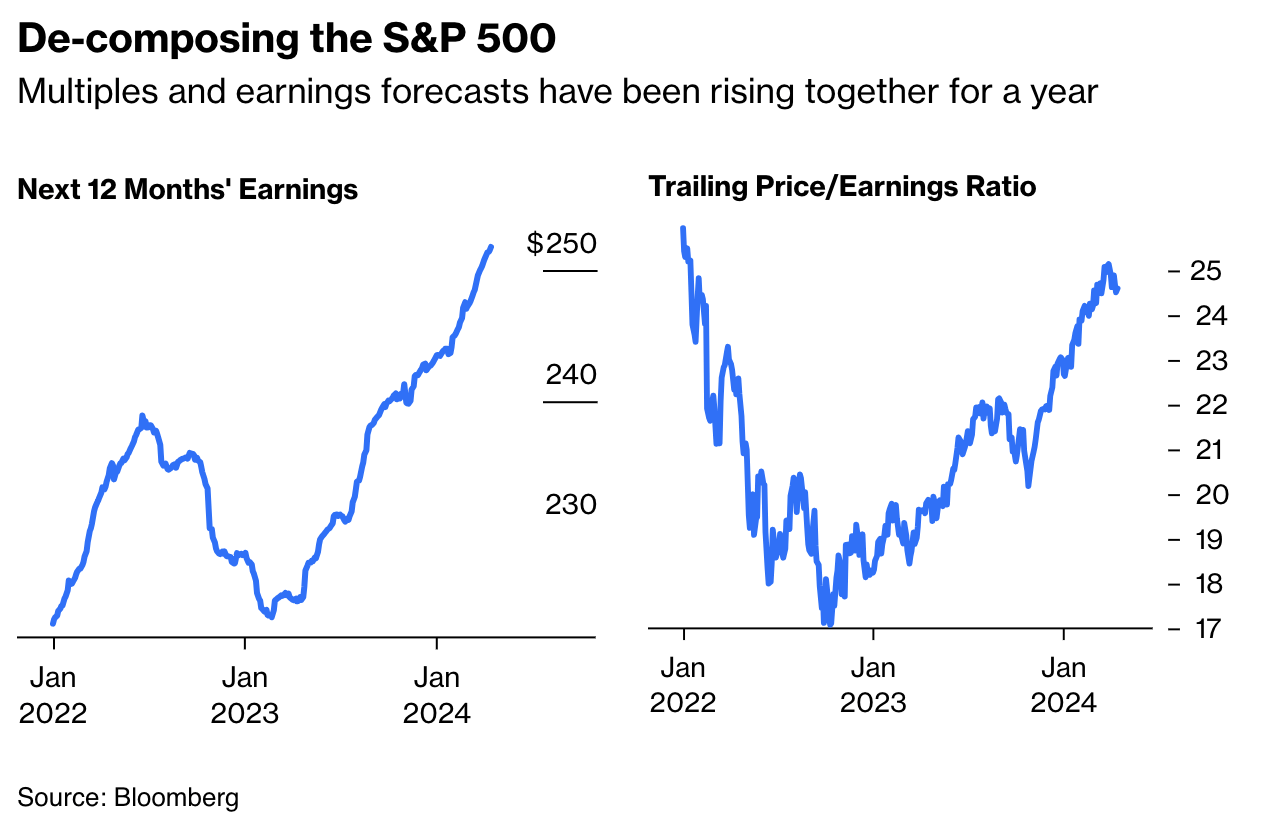

Now, the question is how sustainable all of this is.

While earnings have risen consistently since early 2023, stocks have risen as well, causing the P/E ratio to hover close to 25x. Again, this makes sense, as it’s the inverse function of the earnings yield.

Bloomberg

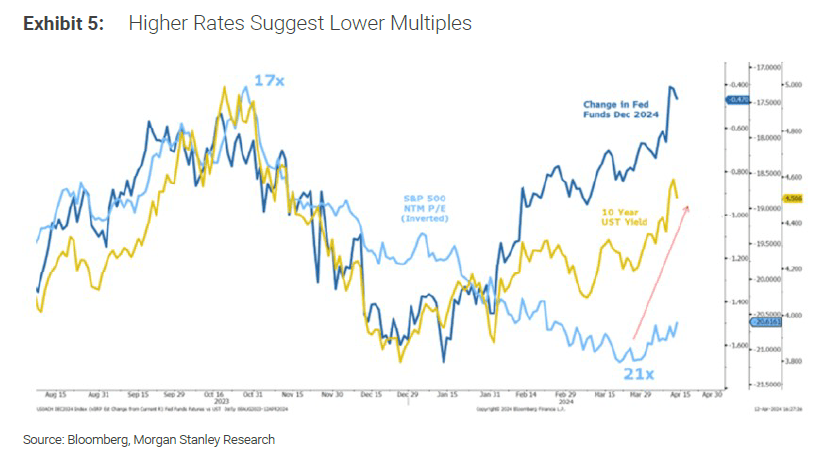

Furthermore, Mike Wilson, the well-known U.S. equity strategist at Morgan Stanley, made the chart below, which shows that last year, higher rates coexisted with lower multiples (which makes sense).

However, this year, multiples have ignored the sharp increase in yields.

Morgan Stanley Research

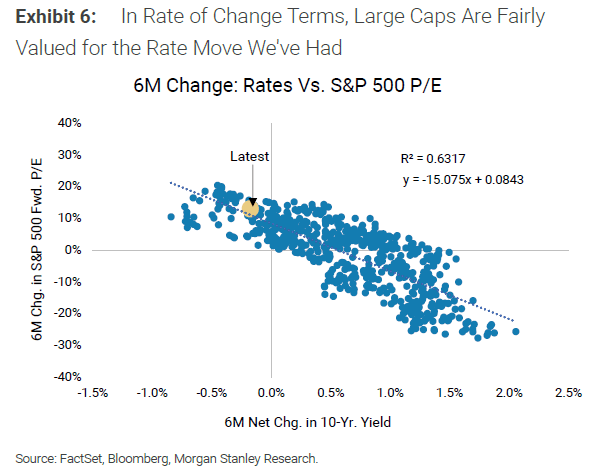

One reason why stocks continue to do so well despite their elevated valuations and competition from higher rates is explained by looking into the change in rates instead of their absolute levels.

As we can see below, there’s a strong correlation between rate changes and the S&P 500’s valuation.

Morgan Stanley Research

For now, this implies two things:

- With the 10-year yield at 4.6%, persistent rates at these levels could be a problem for stocks.

- Anything that causes bond yields to fall makes stocks more attractive.

What I’m Buying

The current environment is extremely tricky. We’re dealing with elevated interest rates, sticky inflation that makes it increasingly difficult for the Fed to quickly reduce rates, declining credit quality, increasing tensions in the Middle East, a major election coming up in November, and elevated valuations – did I forget anything?

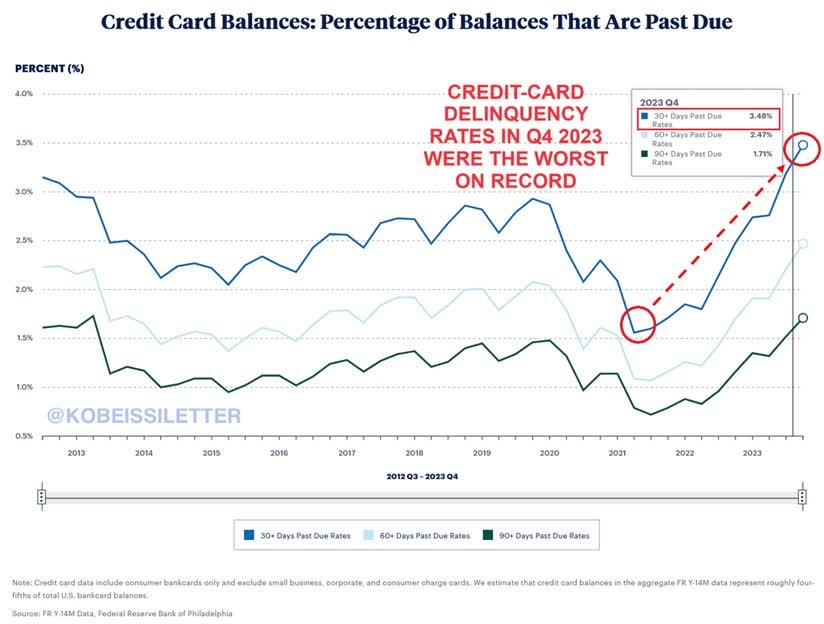

Especially, the mix of sticky inflation and declining credit quality (see the chart below) is making me increasingly nervous!

Twitter/X @KobeissiLetter

I believe the Fed may be pushed into a situation where it has to decide between protecting the economy and fighting inflation.

With everything discussed so far, I’m looking for a few things in new investments:

- I want companies with healthy balance sheets. I make no exceptions anymore. To me, a healthy balance sheet is everything with an investment-grade rating of BBB- and higher. I also watch for net leverage ratios, available liquidity, and the maturity ladder – I try to avoid companies that have to deal with a wave of debt maturities in the next two years, as it would require accelerated refinancing requirements.

- I want companies with pricing power. In other words, if inflation remains elevated for longer, I want companies that can raise prices without being driven out of business. While not all of my companies have high pricing power (some consumer stocks and REITs have limited pricing power), almost all have done well so far. This includes railroads that can use fuel surcharges, healthcare suppliers like Danaher (DHR) who benefit from strong secular growth, energy companies like Canadian Natural Resources (CNQ) and Texas Pacific Land (TPL), and machinery producers like Caterpillar (CAT), whose customers (i.e., mining companies) benefit from inflation as well.

- I want companies that trade below their fair value with decent yield potential. Especially in light of strong competition from bonds and the market’s lofty valuation, I buy companies with decent yields and valuations that give me a shot at beating the market on a prolonged basis. This is tricky, as it’s tough to find good value in a market with an overall elevated inflation. After all, if a stock appears to be really “cheap” in this market, there may be something wrong with the company(!).

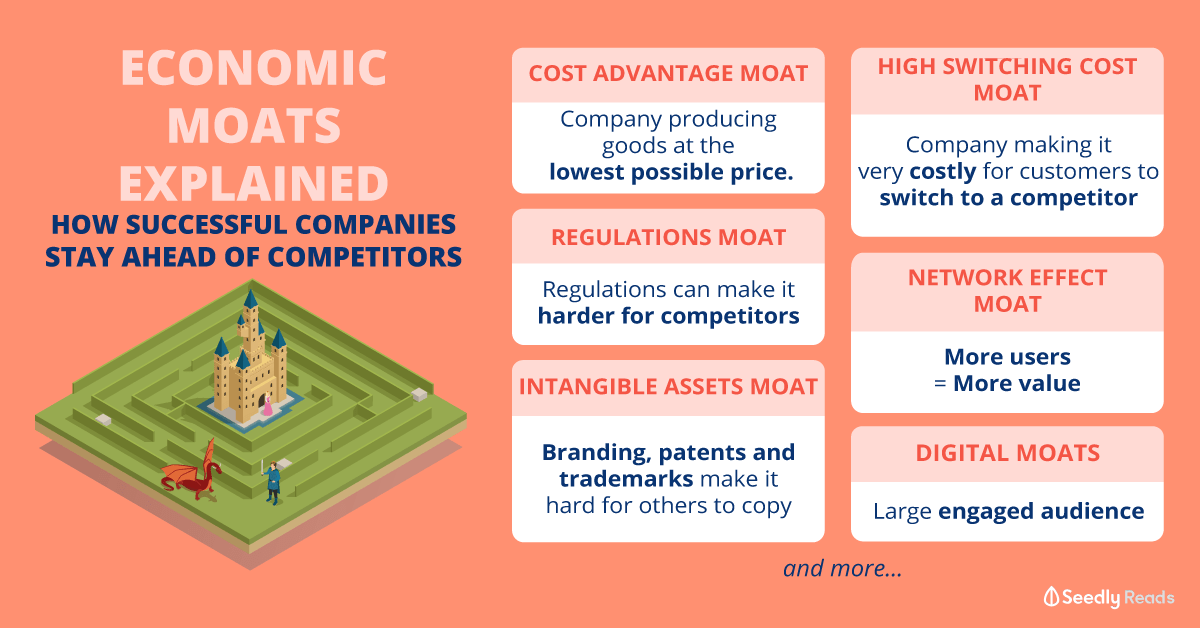

- In light of potential recession risks if the Fed keeps rates elevated for “too long,” I want businesses with wide moats.

Essentially, wide moat businesses combine most of the qualities discussed above.

According to Nasdaq (emphasis added):

“Wide moat stocks typically have significant competitive advantages that allow them to fight off competition and maintain high profitability and returns on capital. A moat can come in several forms. Some firms create moats through a superior brand. Others do it via pricing power that competitors can't match. Still others do it through operational advantages.”

Seedly Reads

Currently, some of my favorite wide-moat dividend businesses are railroads, which have the benefit of controlling North America’s rail transportation – just six companies dominate North America’s Class I railroad shipments.

This includes companies like Union Pacific (UNP).

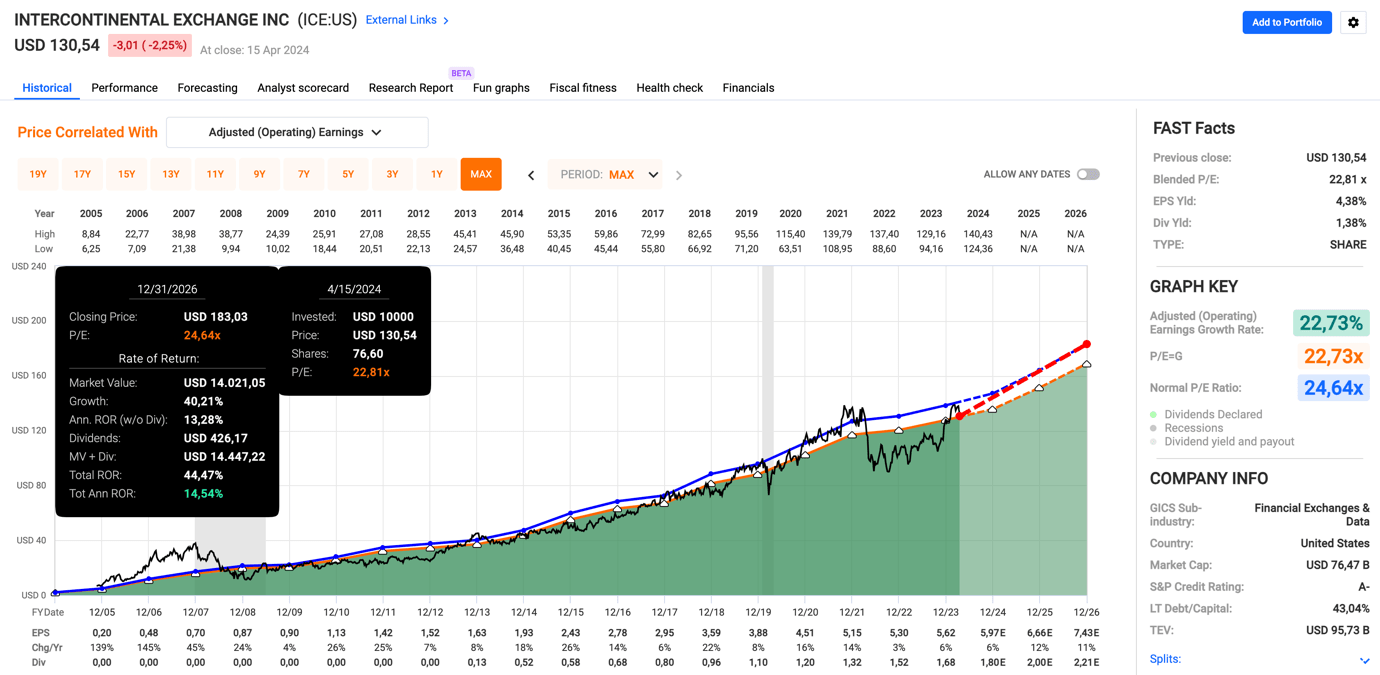

I also love stock exchanges, as these businesses make money on transactions with little competition. The moment volatility picks up, they tend to make more money. My favorites here are CME Group (CME), which pays an annual special dividend, Intercontinental Exchanges (ICE), and Cboe Global Markets (CBOE).

FAST Graphs

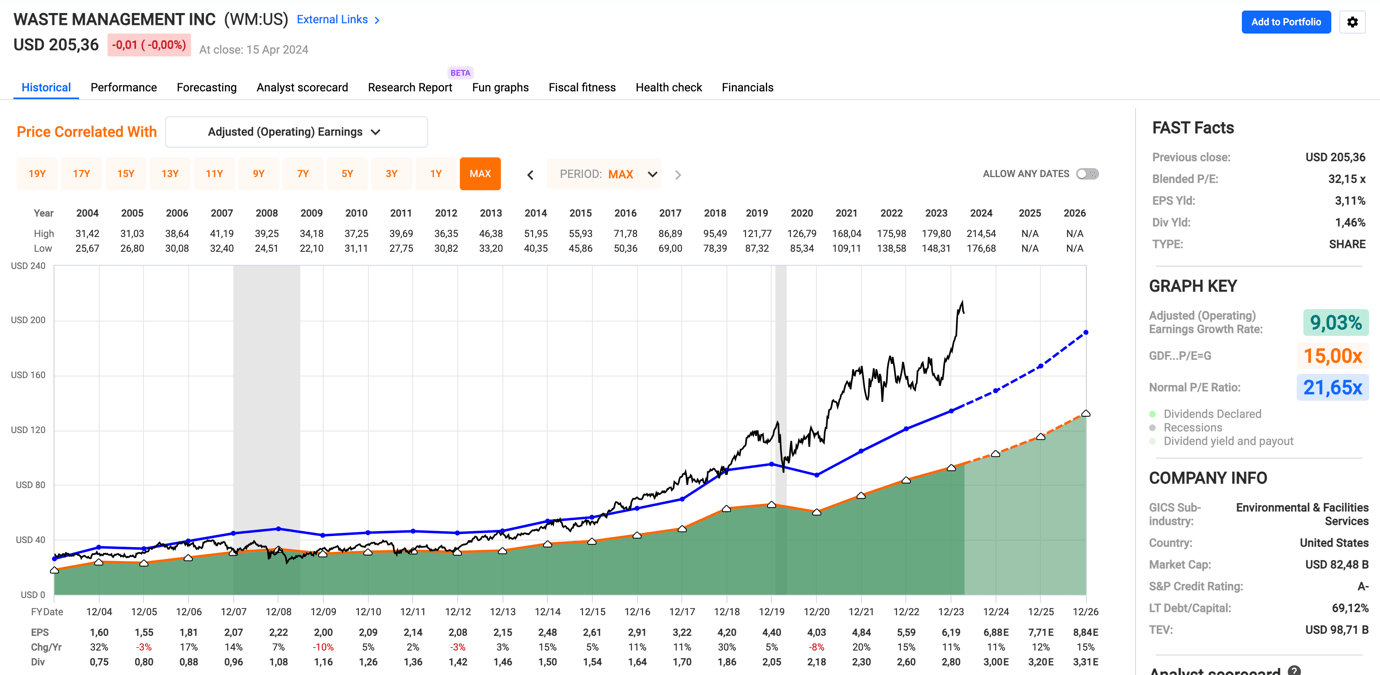

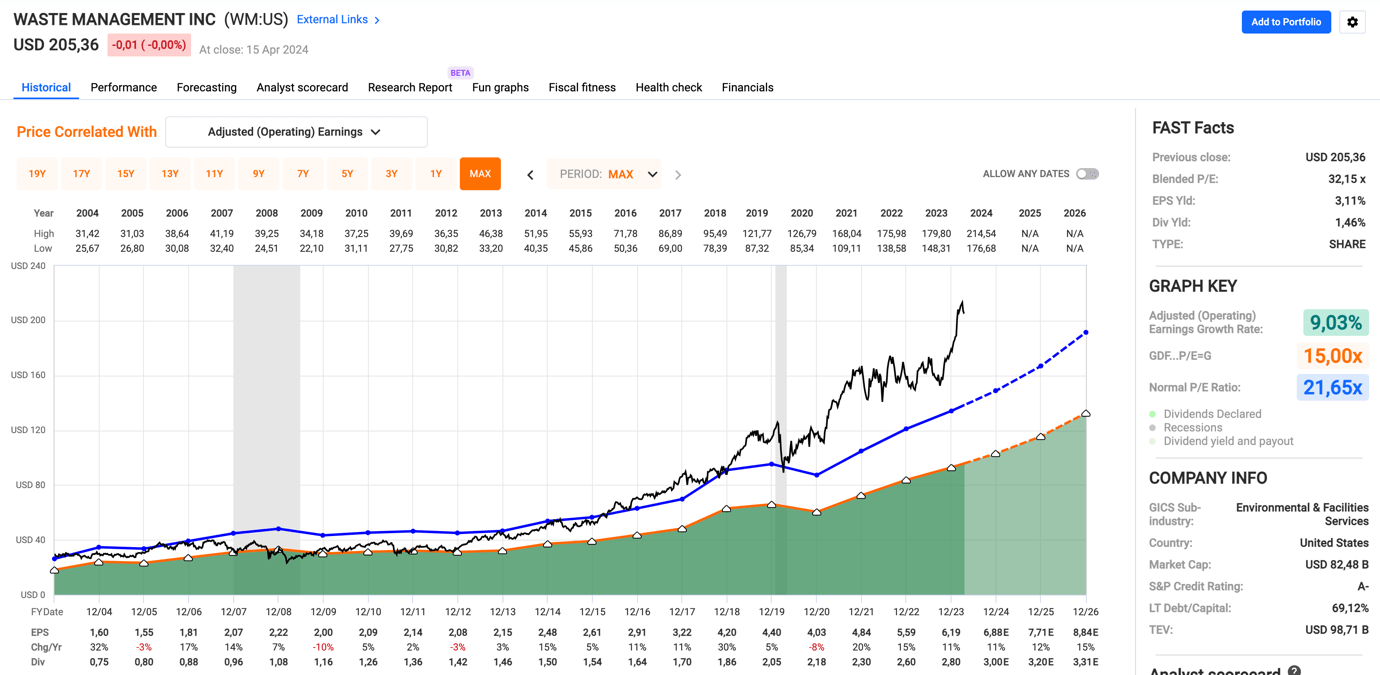

I like waste management companies like Waste Management (WM) and Republic Services (RSG), which have long-term contracts tied to inflation and anti-cyclical demand profiles. Both of these stocks have performed really well, which is why they are trading above their longer-term normalized P/E multiples. WM, for example, needs to drop below $190 to become attractive to add to my portfolio.

FAST Graphs

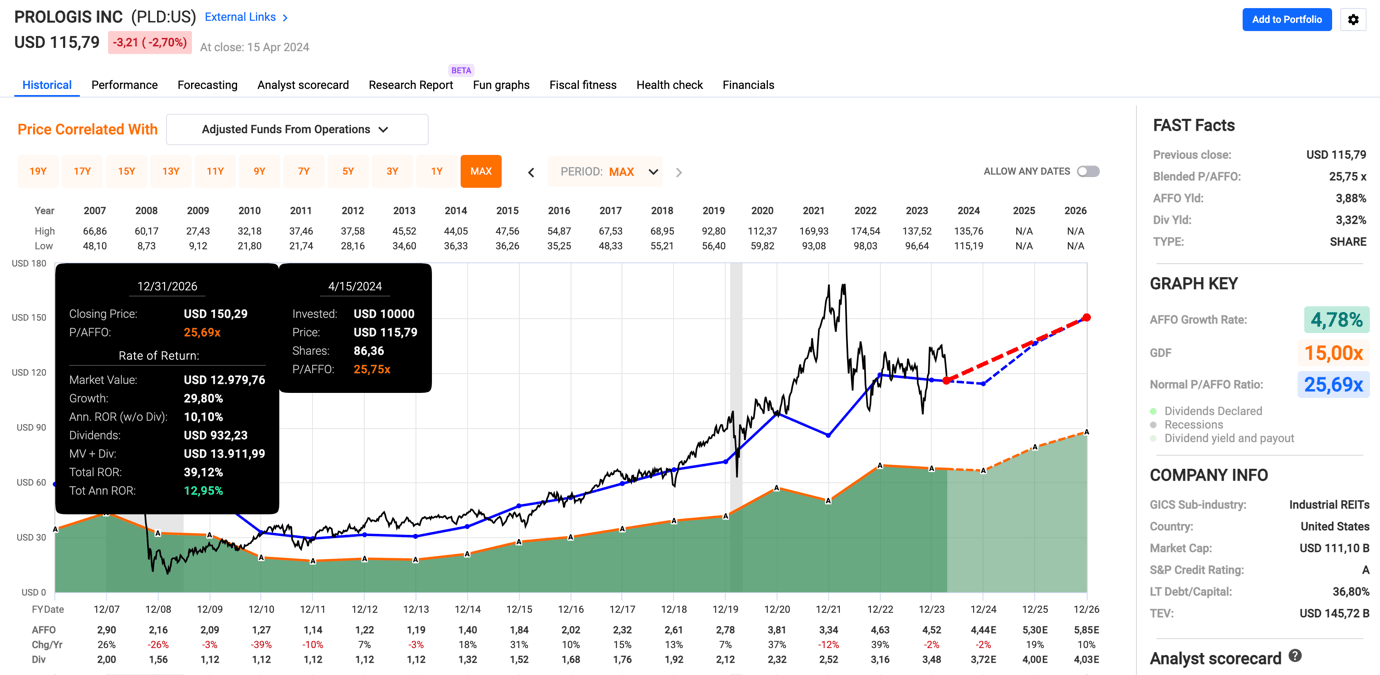

Even in the REIT space, some fantastic companies come to mind.

While it’s very difficult to build a moat in real estate, industrial real estate like Rexford Industrial Realty (REXR) and Prologis (PLD) have assets in areas with subdued supply growth risks. This provides pricing power. They also benefit from secular growth like e-commerce and economic reshoring.

FAST Graphs

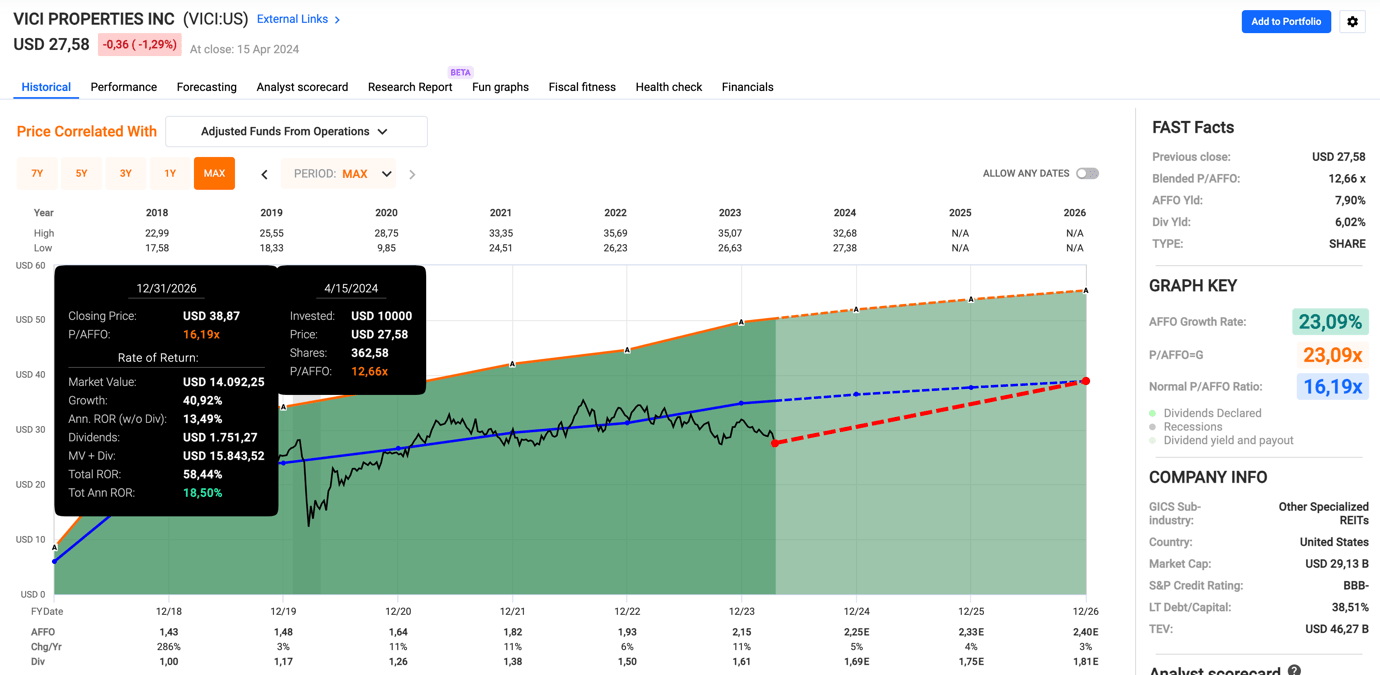

I also like VICI Properties (VICI), which owns entertainment assets, including major buildings on the Las Vegas Strip. These are non-commoditized assets that are difficult to replicate. Moreover, VICI comes with a well-covered 6% dividend yield!

FAST Graphs

Furthermore, I like healthcare companies with a strong competitive position. In addition to Danaher, which I already briefly mentioned, I like Zoetis (ZTS), which produces veterinarian drugs and vaccines that come with strong secular growth and a leading market position in almost every single veterinarian health segment.

FAST Graphs

I currently have all of these businesses on my watch list – except for CME, UNP, CNQ, TPL, and CAT, which I own – and I aim to buy (some of) them if the market keeps correcting.

Given the challenging macro environment, I expect all of these businesses to allow investors to beat the market by a wide margin over time.

Besides these picks, the main message of this article was to keep a close eye on valuations, balance sheets, and competitive moats.

Especially with higher rates providing alternatives to stocks and the mix of sticky and elevated inflation, investors need to be careful when they make new investments.

The current environment is not the same as the easy years between the Great Financial Crisis and 2021.

Takeaway

Navigating today's complex investment landscape requires a keen focus on fundamentals: valuations, balance sheets, and competitive moats.

With elevated interest rates and persistent inflation, the attractiveness of stocks faces new challenges.

Seeking wide-moat dividend stocks, such as railroads, stock exchanges, waste management firms, and select REITs and healthcare companies, offers resilience in uncertain times.

These businesses have strong competitive advantages, pricing power, and healthy balance sheets.

As I monitor these opportunities, I remain cautious yet optimistic, as I expect these resilient businesses to outperform the broader market over time.

Needless to say, there are a LOT more wide-moat businesses on the market that will get more attention in the next few weeks and months on our Investing Group.

Sign Up For A FREE 2-Week Trial

Join iREIT® on Alpha today... for more in-depth research on REITs, mREITs, Preferreds, BDCs, MLPs, ETFs, Builders, and Asset Managers. You'll get more articles throughout the week, and access to our Ratings Tracker with buy/sell recommendations on all the stocks we cover. Plus unlimited access to our multi-year Archive of articles.

Here are more of the features available to you. And there's nothing to lose with our FREE 2-week trial. Just click this link.

And this offer includes a FREE copy of my new book, REITs for Dummies!