Yongyuan Dai

Real Estate Earnings Preview

Hoya Capital

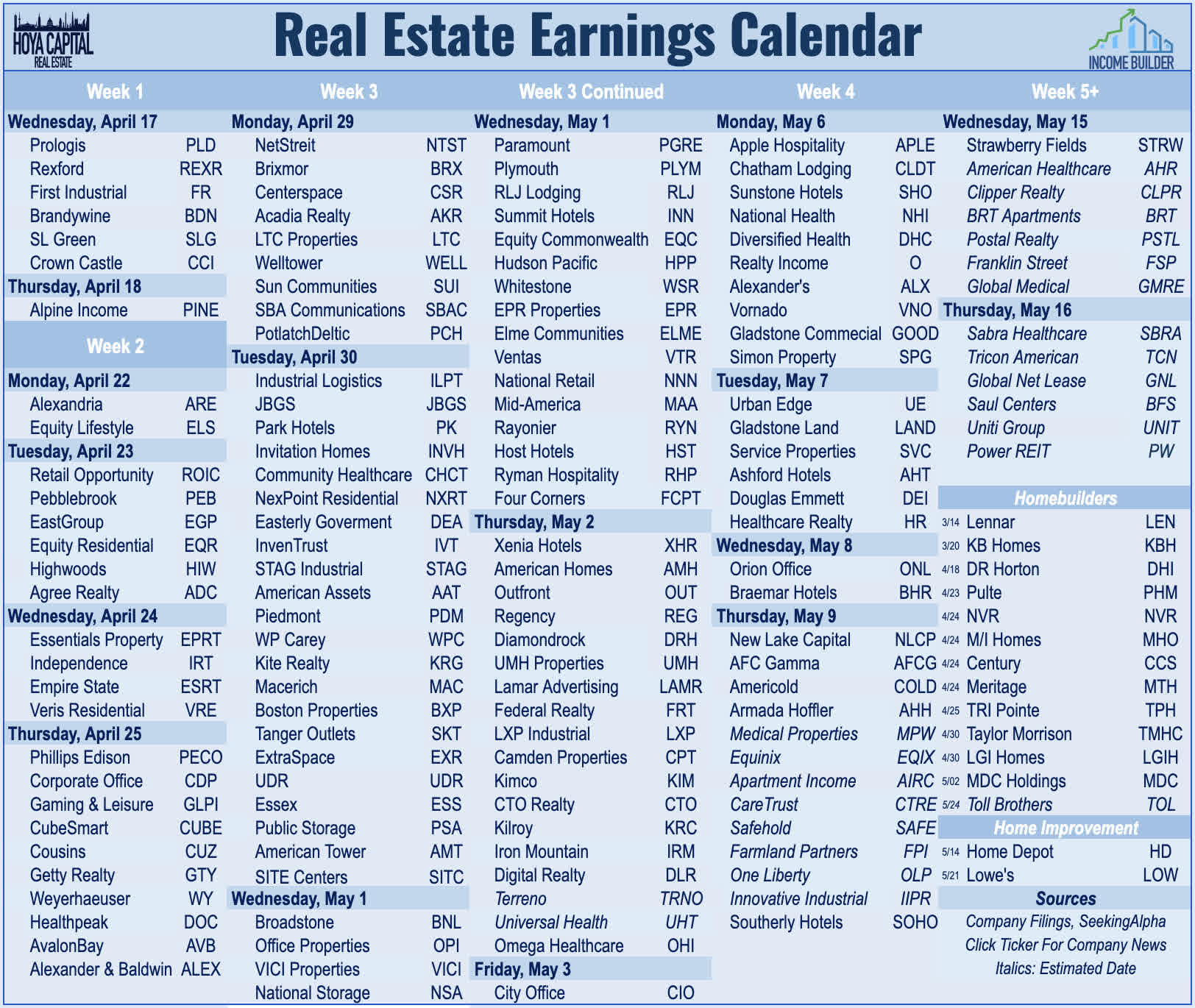

Real estate earnings season kicked off this week, and over the next month, we'll hear results from more than 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies which will provide key insights into how the real estate industry is adapting to the shifting interest rate regime. This report discusses the major high-level themes and metrics we'll be watching across each of the real estate property sectors this earnings season. Below, we compiled the earnings calendar for equity REITs and homebuilders. (Note: Companies that have not yet confirmed an earnings date are in italics)

Hoya Capital

One step forward, one step back. Pressured by the rebound in benchmark interest rates fueled by several months of hotter-than-expected inflation and economic data, REITs once again enter earnings season on a skid, with the Equity REIT Index now 12% off its recent highs in late December. Whether fundamentally warranted or not, real estate has remained the most "Fed-sensitive" market segment, and REITs have been slammed by the sharp shift in market expectations from a view of 6-7 rate cuts this year in January to just 1-2 rate cuts today. At 4.66%, the benchmark 10-Year Treasury Yield has now retraced roughly three-fourths of its late-2023 decline from a peak of 4.99% in mid-October to its low of 3.79% in late December. Heading into the start of Q1 earnings season, just 2-of-18 property sectors are in positive territory on the year, led by Billboard and Single-Family Rental REITs, while Cell Tower and Specialty REITs have lagged on the downside.

Hoya Capital

Before diving into the specific sector-by-sector metrics we're focused on this earnings season, we discuss the four higher-level themes that we're focused on this earnings season:

- Updated 2024 Property-Level Outlook.

- Impact of "High for Longer" Dynamic.

- M&A Environment: Are REITs Buyers or Sellers?

- Dividend Policy: Office & Mortgage REITs In Focus.

1. Updated Full-Year 2024 Outlook

We're keyed in on these REITs' updated 2024 guidance, especially any changes in property-level fundamentals, which have remained surprisingly resilient across most property sectors during the Fed's aggressive rate-hiking cycle. Notable 'green shoots' we've observed in recent commentary and industry data include a firming in residential rents despite ample multifamily supply, steady positive momentum in retail, a modest rebound in office leasing, some cooling in travel demand, softer leasing trends in goods-oriented property sectors, and an overall slowdown in construction activity. The REIT sector is coming off a relatively solid fourth-quarter earnings season with a 67% FFO "beat rate," which was above the historical REIT sector average in Q4 of roughly 65%, and ahead of the 55% "beat rate" in Q4 of 2022. Consistent with the "Tale of Two Economies" trends that we've discussed, upside surprises this earnings season came largely from the service-oriented procyclical property sectors - retail, hotel, and specialty REITs - and from the still-supply-constrained single-family housing and logistics markets. Pockets of weakness were seen in the interest-rate-sensitive property sectors - net lease and office - along with goods-oriented sectors - farmland, timber, and cold storage.

Hoya Capital

2) Impact of "High for Longer" Dynamic

Amend and Extend, or Delay and Pray? For some highly levered private equity portfolios that "kicked the can down the road" with short-term refinancing, the latest rate resurgence may prompt more aggressive liquidations. As noted in our State of the REIT Nation report, the business models of many private equity funds and non-traded REITs were not designed for a period of sustained 4%+ benchmark rates or double-digit declines in property values. Capitulation from debt-burdened private portfolios should eventually create consolidation opportunities for well-capitalized REITs, and we're listening for commentary on whether the latest surge in rates has started to shake anything loose. Fitch reported last week that its measure of US CMBS delinquency rates stood at 2.19% in March, up 43 basis points from last year. Trepp reported a more significant rise in delinquency rates, with its measure of US CMBS special servicing rates rising to 7.31% in March, up 176 basis points from last year. Green Street Advisors' data shows that private-market values of commercial real estate had started to level off in early 2024 after a 21% decline from April 2022 to December 2023, but we expect the downward pressure on property values to pick up once again in coming months.

Hoya Capital

3) M&A: Are REITs Buyers or Sellers?

REITs have generally "hunkered down" since the start of the Fed's tightening cycle - content with a conservative approach to capital deployment - which has resulted in a historically low pace of transaction volumes in recent quarters. We saw a modest rebound in M&A activity in 2023 from within the public REIT sector itself with a dozen public REIT-to-REIT mergers, but none of these moves were particularly "aggressive." Surprisingly, the activity in 2024 has looked much like that of 2022: private equity firms - namely Blackstone Inc. (BX) - scooping up public REITs. After being "net sellers" throughout 2023, Blackstone and its affiliates have acquired two residential REITs over the past quarter - a $3.5B deal to acquire single-family rental REIT Tricon Residential Inc. (TCN), and a $10B deal for multifamily REIT Apartment Income REIT Corp. (AIRC). Public REIT acquisition activity has generally remained limited to small-scale transactions, and we're interested to hear commentary on which REITs plan to be net buyers or net sellers in 2024 - and whether that strategy has been altered by the recent uptick in benchmark rates.

Hoya Capital

4) Dividend Policy: Office & Mortgage In Focus

We've seen 39 REITs raise their dividends so far this year, while 9 REITs have reduced their payouts. On a market-cap-weighted basis, equity REITs pay an average dividend yield of 4.1% - a sizable premium to the 1.4% dividend yield on the broader S&P 500. While sector-level dividend coverage ratios remain quite healthy with an average payout ratio of around 70% - slightly below the long-term historical average - dividend commentary will be a major focus for office and mortgage REITs - the sectors that have been responsible for essentially all the recent dividend reductions across the REIT sector over the past two years. We believe that the "bleeding" in these sectors from a dividend cut perspective is largely contained at this point, but the resurgence in interest rates raises the likelihood that we could see some additional names added to the "dividend cut" list this earnings season. Below, we discuss the key themes we're watching across each of the major property sectors.

Hoya Capital

Office & Hotel REIT Earnings Preview

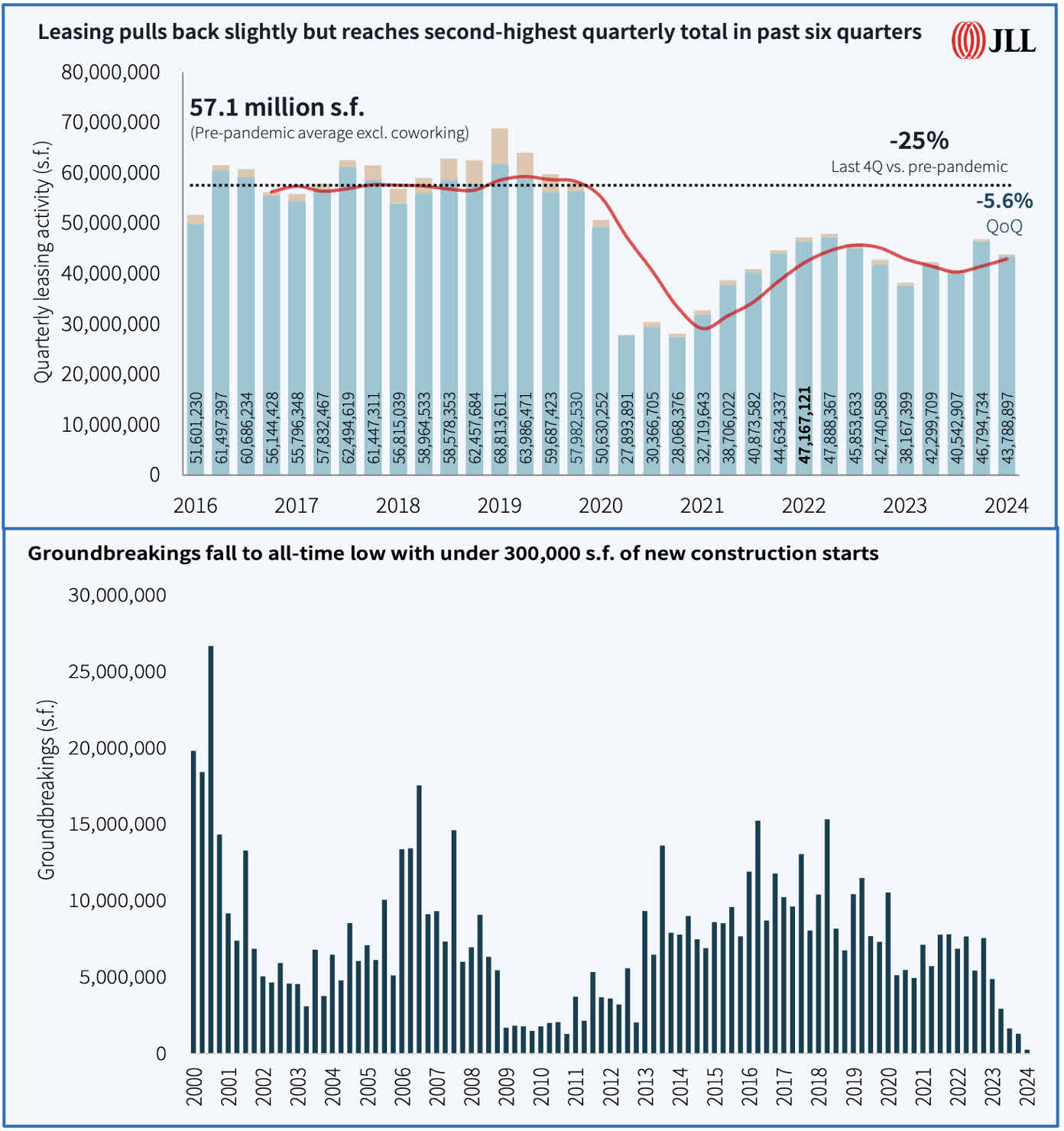

Office: Beneath the pessimistic pivot on interest rates, we've actually observed surprisingly positive green shoots for the office sector in recent months. Brokerage firm Jones Lang LaSalle Incorporated (JLL) released its quarterly office update this week, which showed relatively solid trends in office leasing activity in early 2024, and a "rebalancing" in fundamentals resulting from a "significant uptick" in inventory removals alongside a "rapid slowdown in development activity." Following the best quarter of leasing activity since mid-2022, JLL tracked 43.8M SF of leasing activity in Q1 - slightly below Q4 but still 14% higher than a year earlier. JLL's TIMs Index - its forward-looking demand tracker which leads leasing activity by 2-3 quarters - shows that 70% of markets recorded a QoQ increase in tenant space requests in Q1, driving a 5.7% sequential increase in this index to 72% of pre-pandemic levels. JLL also notes office groundbreakings fell to the lowest volume in decades in Q1, with just 300k s.f. of new construction beginning. In Q1 2023, just 13.5% of office buildings nationally saw vacancy rates increase - the second lowest level since Q3 2017. We're keyed in on a key question this quarter: will this steadying of fundamentals be enough to steady the ship amid renewed rate headwinds?

Hoya Capital

Hotels: On the other side of the spectrum, the U.S. hotel industry delivered a record-setting year of operating performance in 2023 as travel demand exceeded pre-pandemic levels by 5-10%, but after a very strong fourth quarter for the industry, we've observed some moderation in travel demand in early 2024 across the various high-frequency metrics we track and from the handful of REIT business updates. TSA Checkpoint data shows that passenger throughput was roughly 5% above 2019 levels in March and early April - a mild slowdown from the 10% comparable increase in January and the 7% increase in February. Hotel data provider STR reports that industry-wide Revenue Per Available Room ("RevPAR") was 13% above 2019 levels in Q1 - a slight deceleration from the roughly 15% comparable increase in Q4 - as occupancy rates have weakened in recent months since recovering to pre-pandemic levels in late 2023. Even with the demand moderation, we're expecting another solid quarter from hotel REITs, and foresee these REITs being some leaders in dividend growth once again in 2024.

Hoya Capital

Tech and Industrial REITs Earnings Preview

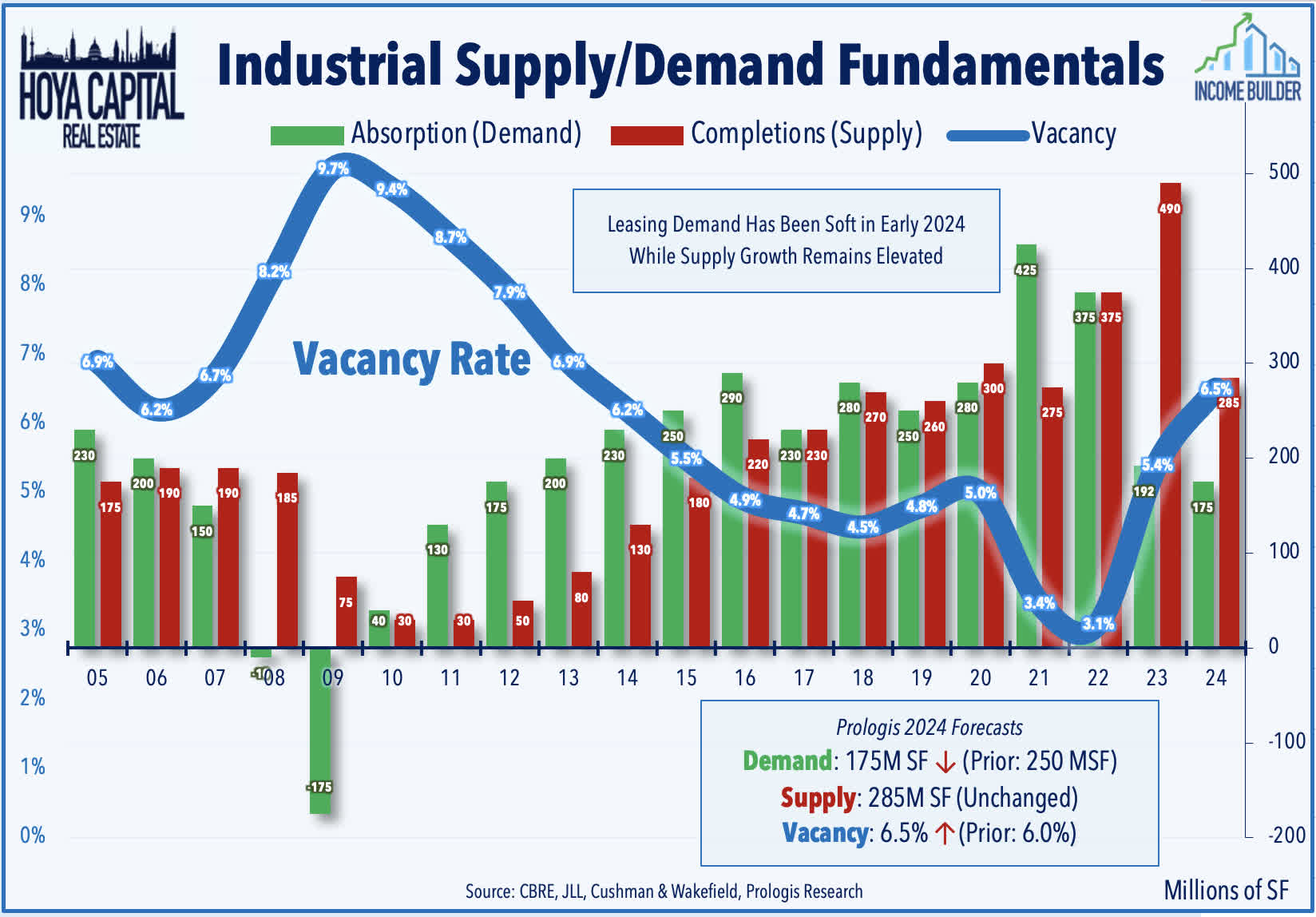

Industrial: After delivering surprisingly strong results throughout 2023 in the face of a "goods economy" recession, the resilience of industrial REITs is expected to be tested this year as moderating leasing demand clashes with elevated supply growth. We've already seen results from three industrial REITs this week. Logistics stalwart Prologis, Inc. (PLD) kicked off REIT earnings season this week on a sour note, reporting surprisingly soft results trimming its full-year outlook, citing softer demand and particular weakness in its Southern California portfolio. PLD attributed the demand slowdown to "indecision" from its tenant base driven by cost-cutting, higher interest rates, and geopolitical concerns. Prologis trimmed its 2024 outlook for all of its comparable metrics, citing expectations for net absorption "to be lower than our prior expectations and leasing to stay competitive in a handful of our larger, higher-rent markets." Prologis now expects 175M SF of nationwide industrial absorption this year - down considerably from its prior forecast of 250M SF - which would be the weakest since 2012 and expects the national vacancy to rise to 6.5% this year, which would also be the highest since 2012. First Industrial Realty Trust, Inc. (FR) reported similarly soft results and lowered its full-year outlook. Results from Rexford Industrial Realty, Inc. (REXR) were a bit stronger, but comparable cash rent spreads cooled to nine-month lows. We're interested in hearing whether other industrial REITs share Prologis' outlook on supply-demand fundamentals, and for any commentary on prospects for private market acquisition activity.

Hoya Capital

Data Center: The top-performing property sector last year, Data Center REITs have been under pressure in recent weeks after short-seller Hindenburg Research published a short report on Equinix, Inc. (EQIX), making several allegations including that EQIX overstates its AFFO, oversells capacity at its facilities, and faces increased competition from "hyperscale" cloud providers. EQIX - which had been one of the top-performing REITs over the prior year - was already under pressure after it announced that its CEO Charles Meyers will transition to the role of Executive Chairman, and be replaced by Google executive Adaire Fox-Martin. Concerns about competitive positioning and weakened pricing power are certainly nothing new for data center REITs, however, and similar claims were the core of a short report from Chanos & Company in July 2022, which ironically came at the "bottom" of a half-decade-long slump in rental rates. Even with the pullback, Data center REITs have been the top-performing REIT sector since that July 2022 report. We'll be watching closely for a more direct response from EQIX to the short thesis, and we'll be keyed-in on renewal pricing trends and leasing volumes this quarter.

Hoya Capital

Cell Towers: Cell Tower REITs have been the weakest-performing property sector since the start of 2022 - lagging even the battered office sector - amid a telecommunications industry-wide slump inflamed by tight monetary conditions. Cellular carriers have curbed their capital-intensive network expansion plans in recent quarters following a significant wave of investment and tower equipment upgrades from 2019-2022 to deploy nationwide 5G networks. Crown Castle Inc. (CCI) kicked off the earnings slate with an in-line report in which it maintained its full-year outlook, while providing some updates on the ongoing strategic review of its fiber business. In earnings commentary, CCI indicated that carrier leasing activity remains status-quo at levels that are 50% below the peaks at the initial outset of the 5G cap-ex cycle in 2022, and noted that it hasn't seen anything that would alter its full-year outlook. Regarding its fiber strategy review - which is the result of activity investor pressure to re-focus the business following several years of peer underperformance - CCI noted that it has "recently engaged with multiple parties, who have expressed interest in a potential transaction involving all or part of our fiber business." Concurrently, American Tower Corporation (AMT) has been in the midst of a strategic shake-up, having completed an exit from the Indian market earlier this year. We're focused on commentary on these strategy shifts and further commentary on expectations for network spending.

Hoya Capital

Residential Real Estate Earnings Preview

Apartments: The state of the U.S. housing market will also be a critical focus throughout earnings season as the interest rate outlook again turns unfavorable. Following two years of record-setting rent growth, residential rents decelerated in 2023 alongside a broader cooling of inflationary pressures, with multifamily rents seeing a particularly sharp cooldown. The wave of pandemic-era development - started at a time when rents were rising double-digits - resulted in a record year of new deliveries in 2023 with similarly elevated supply levels expected in 2024. The pundit-predicted rental market "crash" has remained elusive, however, as demand has stayed surprisingly robust, driven by the combination of resilient job growth, homeownership unaffordability, favorable demographics, and elevated inbound immigration. Recent data from Zillow and Apartment List shows that rental rates have been surprisingly firm in early 2024 despite the record-setting quantity of multifamily deliveries. We'll be closely watching rent growth metrics on new and renewed leases, commentary on supply conditions, and indications of any appetite for external growth via private market acquisitions following a decade of leaning on new development to fuel external growth.

Hoya Capital

Single-Family Rentals: Supply growth has remained more contained on the single-family side, which has kept rent growth more buoyant in recent quarters. With rents likely to settle in the "inflation-plus" range of 3-5% in 2024, expenses will be the "wild card" - especially as it relates to insurance and property taxes. Double-digit percentage increases in insurance premiums and property taxes have become the recent norm for property owners - driven primarily by a "catch-up" effect to reflect the roughly 25% increase in home values over the past two years. The brief period of negative home price appreciation in 2023 and tighter credit conditions quickly neutralized the pockets of speculative housing market activity - including the "fix-and-flips" and highly levered short-term rental ("STR") startups that were beginning to fizzle in 2021 and 2022, and the more challenging operating and financing conditions should give an easier pathway to institutional operators to accretively add to their portfolios. In addition to rent growth metrics, we're interested in commentary about these external growth prospects - specifically, whether these REITs are beginning to see any pockets of private-market distress that could be ripe for the picking - especially in light of the privatization of Tricon Residential by Blackstone earlier this year.

Hoya Capital

Homebuilders: It's all about rates, the U.S. housing industry appeared poised to thaw from its deep freeze induced by historically aggressive monetary tightening, but mortgage rates are again pushing back towards multi-decade highs. Data this week showed that Housing Starts dipped 14.7% in March to a 1.32 million annual pace - the lowest since August and posting the sharpest month-over-month decline since the first month of the pandemic in April 2020. Freddie Mac data this week showed that mortgage rates climbed past 7% for the first time this year, swelling to 7.10% this week - up a half-percentage point from lows in mid-January. It remains the case, however, that higher mortgage rates have merely delayed - but not permanently altered - the existing secular fundamentals supporting the single-family market: a "lost decade" of single-family construction. Builders have a high bar to meet, however, following their incredible rally of nearly 90% in 2023. We're focused on net orders - expecting a modest positive inflection this quarter after roughly two years of year-over-year declines - along with cancellation rates, and gross margins. With builders no longer trading with deep discounts, further upside will require operational execution.

Hoya Capital

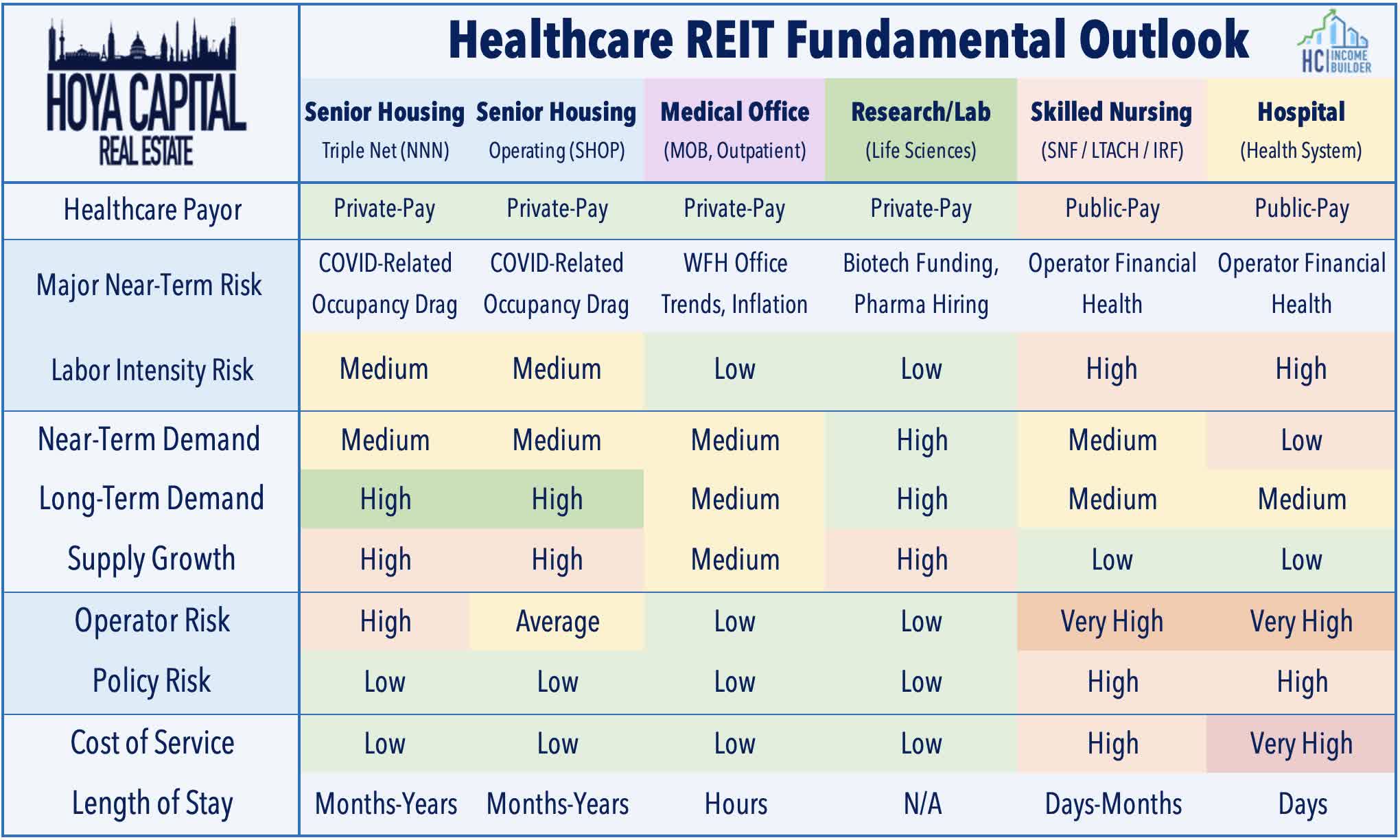

Healthcare REIT Earnings Preview

Senior Housing: Continuing their strong performance from last year, Senior Housing and Skilled Nursing REITs have been among the leaders this year as recent data shows a continued recovery in occupancy rates alongside historically strong rent growth. Earlier this month, industry data provider NIC published its quarterly Market Fundamentals report, which showed that senior housing occupancy rates increased for the 11th consecutive quarter to 85.1%, which is 7.8 percentage points above its pandemic low of 77.8% in the second quarter of 2021. The skilled nursing occupancy rate, meanwhile, rose to 83.9% in the most recent quarter, up 9.2 percentage points from its pandemic low of 74.7%. Fueled by tailwinds from record-setting COLA adjustments in 2023, rent growth across both Senior Housing and Skilled Nursing facilities remained historically strong in early 2024, rising by 4.4% and 4.0%, respectively. Supply growth remains muted as well, with NIC noting that the rolling four-quarter average for construction starts sits at 1.37% of total inventory - the lowest since 2010. Tenant health remains the primary focus of earnings season for senior housing and skilled nursing REITs.

Hoya Capital

Medical Office: Somehow even more "unloved" than traditional office, medical office building ("MOB") REITs enter earnings season as the worst-performing sub-sector this year, and are now trading at average Price-to-FFO valuations that are below that of traditional office REITs. While these REITs do tend to be among the more rate-sensitive segments, the poor performance is a bit head-scratching given the relatively strong property-level fundamentals. JLL's latest report published this month concludes, "[MOB] fundamentals remain strong, and construction starts remain slow, positioning medical outpatient buildings for increasing occupancy and rental rate growth, driving increased allocation from capital rotating from other asset classes." The report notes that absorption has outpaced construction every quarter since Q2 2021 as completions have slowed while demand accelerated. This drove occupancy up from 91.4% at the end of 2020 to 93.0% in Q4 2023. Despite steady demand, construction starts for MOBs have remained below pre-pandemic averages over the past three years. We think MOB REITs have a relatively low hurdle to meet this earnings season, and will be looking for integration progress on recent merger activity from the two largest MOB REITs.

Hoya Capital

Hospital: Embattled hospital owner Medical Properties Trust, Inc. (MPW) - which is the most heavily-shorted REIT - enters earnings with upside momentum after it announced that it's ahead of schedule in its liquidity transactions slated for this year as it seeks to divest from several struggling operators. MPW has soared this month after it announced a $1.1B portfolio sale of five hospitals and announced that it maintained its quarterly dividend. MPW announced that it sold its five Utah hospitals - which were managed by struggling operator Steward Healthcare before its operations were acquired by CommonSpirit Health in 2023 - into a newly formed joint venture with an unidentified institutional asset manager. Earlier in the month, MPW announced that it closed on its sale of five facilities in California and New Jersey to Prime Healthcare for a total of $350M. The pair of deals brings MPW's total portfolio sales to $1.6B, which is 80% of its initial FY 2024 target. MPW is "now confident that we will exceed our initial target of $2.0B in liquidity transactions in 2024 based on the valuations achieved on recent transactions and the terms we are actively negotiating" for other asset sales.

Hoya Capital

Retail REITs Earnings Preview

Strip Centers & Malls: Retail REIT fundamentals have improved materially over the past year and continue to be underappreciated in the market as a decade-long "retail apocalypse" narrative has been tough to shake. Data this week showed that Retail Sales were considerably stronger than expected in March, posting a back-to-back acceleration in the annual growth rate for the first time since late 2022. Notably, the nearly 5% year-over-year increase in Core Retail Sales was the second-strongest month of the past year. The combination of near-zero new development and positive net store openings since 2021 has driven occupancy rates to record highs and allowed both Strip Center and Mall REITs to enjoy some long-awaited pricing power. Despite several high-profile retail bankruptcies - including Bed Bath & Beyond and Party City - store openings outpace store closings by about 10% in 2023, and recent data from Coresight shows that the positive momentum has continued into early 2024. We'll again be focused on leasing spreads and occupancy rate trends - which have been impressive of late - and on updates on re-lease progress at these vacated Bed Bath and Party City locations, in particular.

Hoya Capital

Net Lease: The most "bond-like" and interest-rate-sensitive property sectors, the rebound in benchmark rates has added renewed pressure on net lease REITs. Thriving in the "lower forever" environment, the industry has been reluctant to acknowledge the higher-rate regime, keeping private-market values and cap rates surprisingly "sticky" and resulting in compressed investment spreads. Strong balance sheets and lack of variable rate debt exposure have positioned net lease REITs to be aggressors as over-levered private players seek an exit, but these REITs can afford to wait until the price is right. When interest rates pulled back in late 2023, the decision by many net lease REITs to plow ahead with acquisitions looked like a smart move, but investors are again questioning whether these moves will prove costly as rates remain elevated. We're keyed in on commentary regarding cap rate movements in early 2024 and whether the rebound in interest rates has changed the outlook for acquisition and disposition activity in 2024.

Hoya Capital

Key Takeaways: Real Estate Earnings Preview

Real estate earnings season kicked into gear this week, and over the next month, we'll hear results from 175 equity REITs, 40 mortgage REITs, and dozens of housing industry companies. One step forward, one back. Pressured by the rebound in interest rates, REITs again enter earnings season on a skid, with the REIT Index now 12% off recent December highs. While property-level fundamentals remain solid across most property sectors, the latest rate resurgence creates renewed pressure on rate-sensitive sectors and more highly leveraged REITs. For some highly levered private equity portfolios that "kicked the can down the road" with short-term refinancing, the latest rate resurgence will likely prompt more aggressive liquidations, which may create opportunities for public REITs. Notable recent 'green shoots' include a firming in residential rents despite ample multifamily supply, steady positive momentum in retail, a modest rebound in office leasing, some cooling in travel demand, softer leasing trends in goods-oriented property sectors, and an overall slowdown in construction activity.

Hoya Capital

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments, Homebuilders, Manufactured Housing, Student Housing, Single-Family Rentals, Cell Towers, Casinos, Industrial, Data Center, Malls, Healthcare, Net Lease, Shopping Centers, Hotels, Billboards, Office, Farmland, Storage, Timber, Mortgage, and Cannabis.

Disclosure: Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index. Index definitions and a complete list of holdings are available on our website.

Hoya Capital

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Read The Full Report on Hoya Capital Income Builder

Income Builder is the premier income-focused investing service on Seeking Alpha. Our focus is on income-producing asset classes that offer the opportunity for sustainable portfolio income, diversification, and inflation hedging. Get started with a Free Two-Week Trial and take a look at our top ideas across our exclusive income-focused portfolios.

With a focus on REITs, ETFs, Preferreds, and 'Dividend Champions' across asset classes, members gain complete access to our research and our suite of trackers and portfolios targeting premium dividend yields up to 10%.