BalkansCat

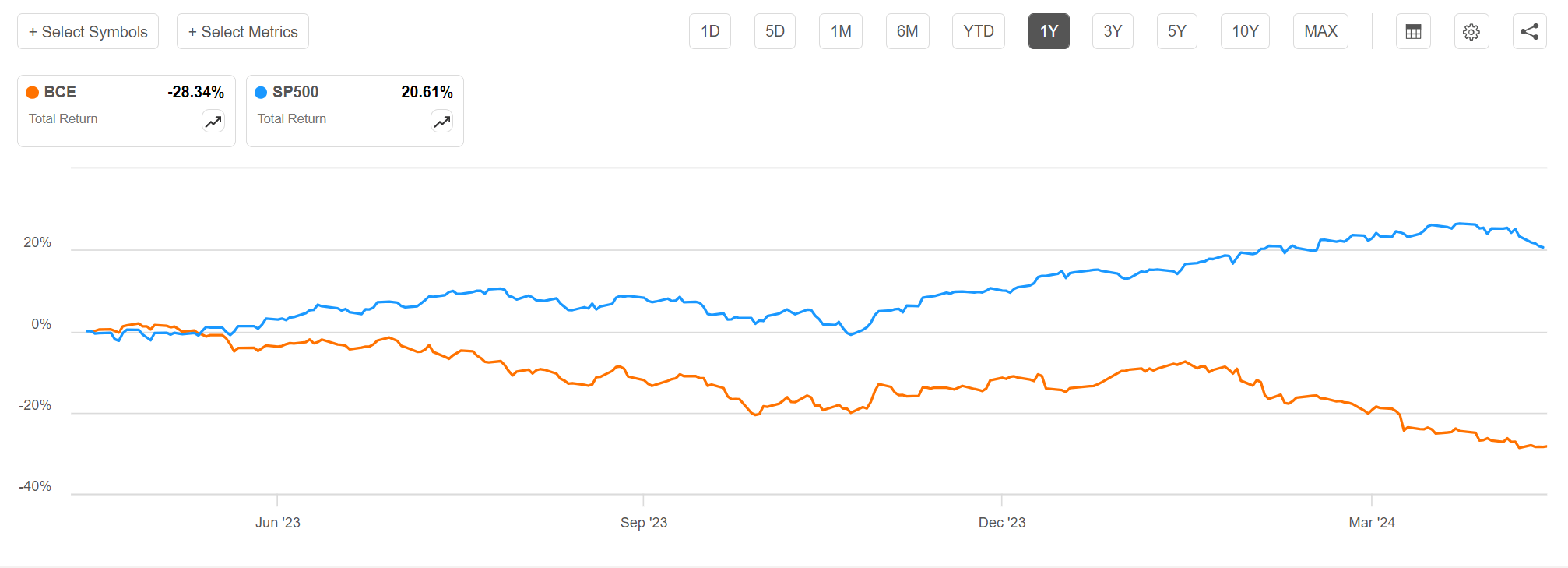

There is an old investment axiom to be greedy when others are fearful, and fearful when others are greedy. In the case of BCE Inc. (NYSE:BCE), it appears investors are certainly fearful, as the stock has lost an incredible 28% in the past year when the rest of the markets have been powering higher (Figure 1).

Figure 1 - BCE has massively underperformed the market (Seeking Alpha)

Are investors right to be fearful about BCE Inc., or does this selloff represent a good opportunity to snap up shares on the cheap?

I, personally, believe BCE shares present good value at current levels and have added some to my retirement accounts. Earning a relatively safe 8.9% dividend yield does not hurt either.

Brief Company Overview

BCE, also known as Bell Canada Enterprises, is a leading telecommunications provider in Canada, offering wireless, broadband, television, and landline phone services. With over 10 million customers, BCE commands approximately 1/3 of the Canadian national wireless market in competition with Rogers Communications (RCI) and TELUS Corp (TU). BCE is also the primary legacy telephone ("wireline voice") provider in eastern Canada and has a large share of the broadband internet market.

In addition to telecommunications, BCE also operates a sprawling media business including television and radio stations, the leading Canadian sports network TSN, as well as the Canadian broadcast rights for popular American channels like HBO, Showtime, and Starz.

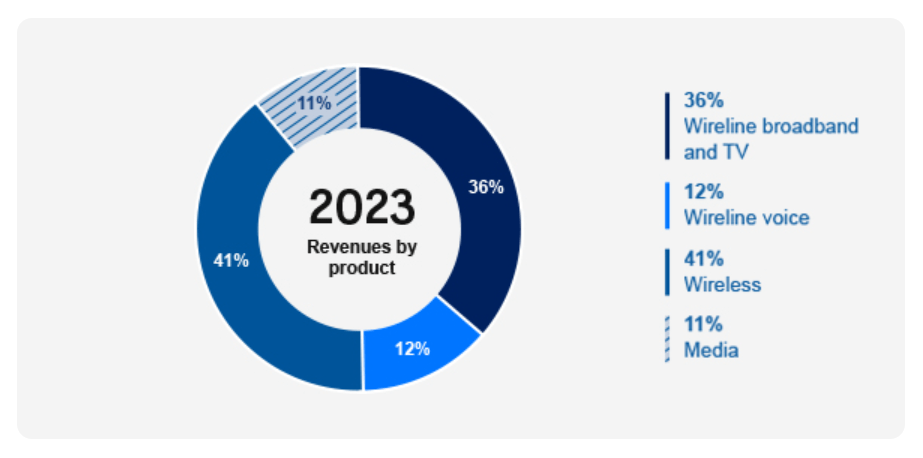

By segment, wireless contributed 41% of BCE's 2023 revenues, while wireline broadband and TV contributed 36%. Legacy wireline voice was 12% of revenues and the Media segment was 11% (Figure 2).

Figure 2 - BCE revenue by segment (BCE investor presentation)

Troubles With Wireless Competition

Recently, the CEOs of BCE, Rogers, and Telus were summoned to testify before a House of Commons committee on rising costs of wireless services and job layoffs.

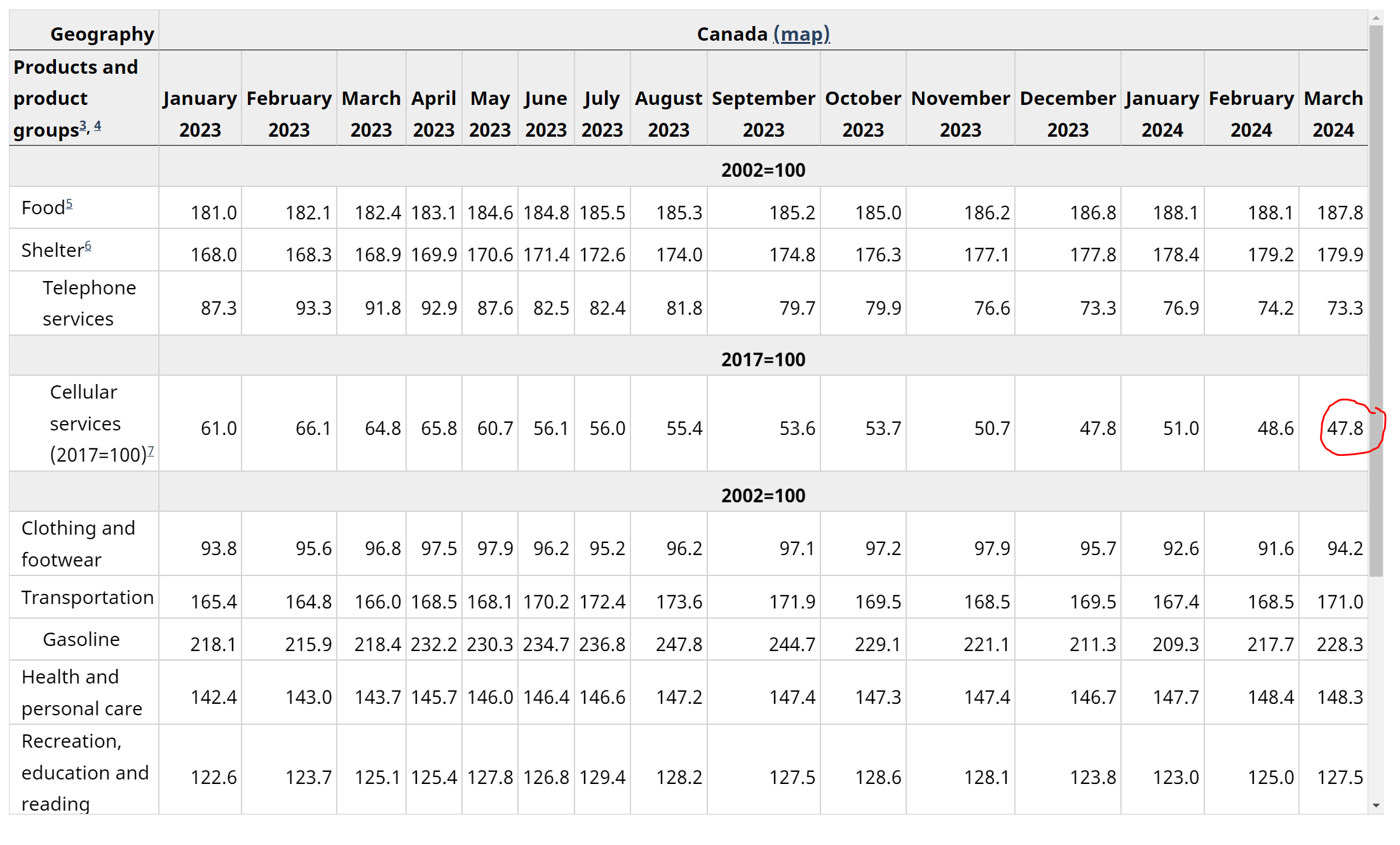

While vilifying telecom companies may be a popular Canadian pastime and consumers undoubtedly want lower prices, the truth of the matter is that wireless prices have been on the decline in Canada in the past few years due to the entry of Quebecor/Freedom Mobile. According to Statistics Canada, the cost of Cellular Services is roughly half of what it was in 2017 (Figure 3).

Figure 3 - Cellular services is one of the few areas where consumers are seeing price relief (Stats Can)

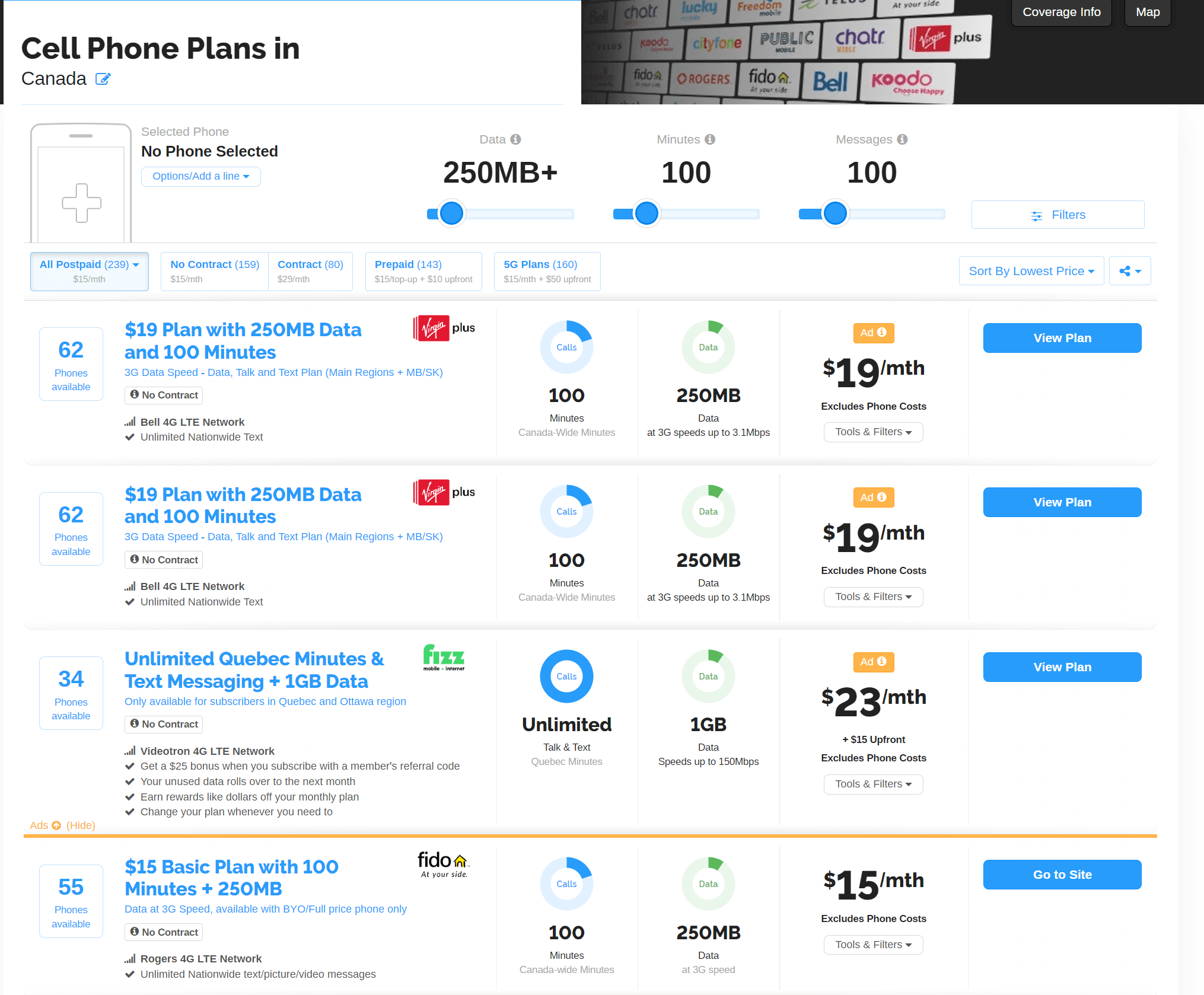

This is confirmed by my personal experience (as I reside in Canada), as simple, no-frills, value wireless plans can often be obtained for ~C$20 / month (Figure 4).

Figure 4 - Illustrative price of no-frills wireless plans (whistleout.ca)

Instead of competing on price, BCE and the other major telecom providers try to bundle multiple services (i.e. wireless and internet) and features (i.e. caller ID and USA calling) to maintain their premium average revenue per user ("ARPU").

Given the already intense competition in the wireless space, I do not expect major regulatory changes to come out of the recent bout of political scrutiny.

Three Reasons I am Buying BCE Now

Instead, I believe BCE's shares present an interesting opportunity at the moment for those willing to go against the crowd.

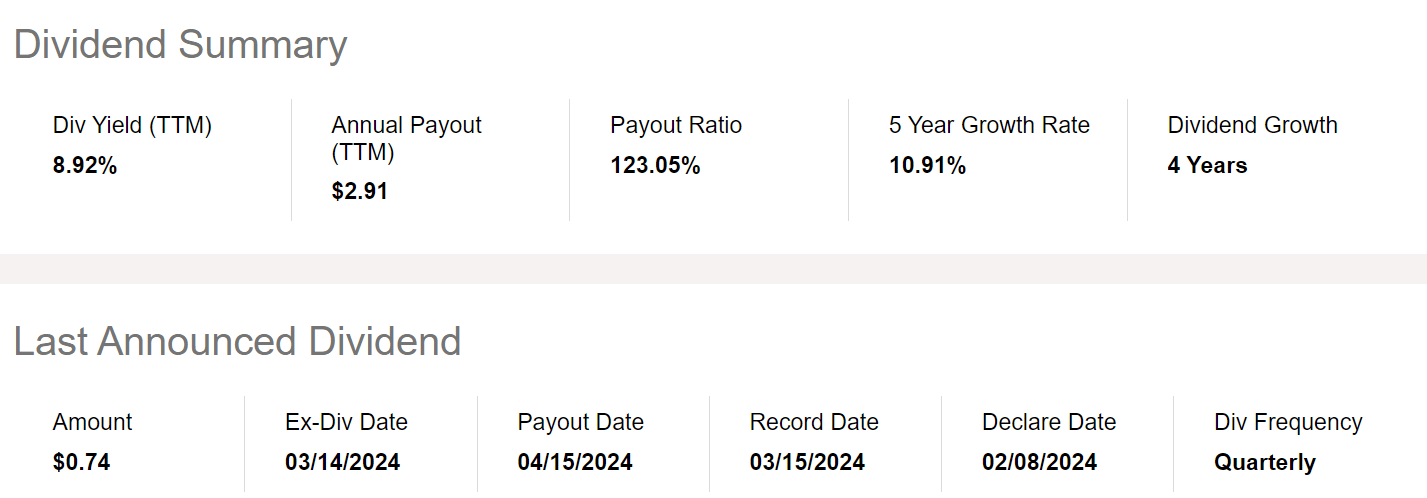

First, BCE is known for paying hefty dividends, and due to its recent stock price declines, BCE's shares are now yielding a juicy 8.9% dividend (Figure 5).

Figure 5 - BCE dividend yield is 9% (Seeking Alpha)

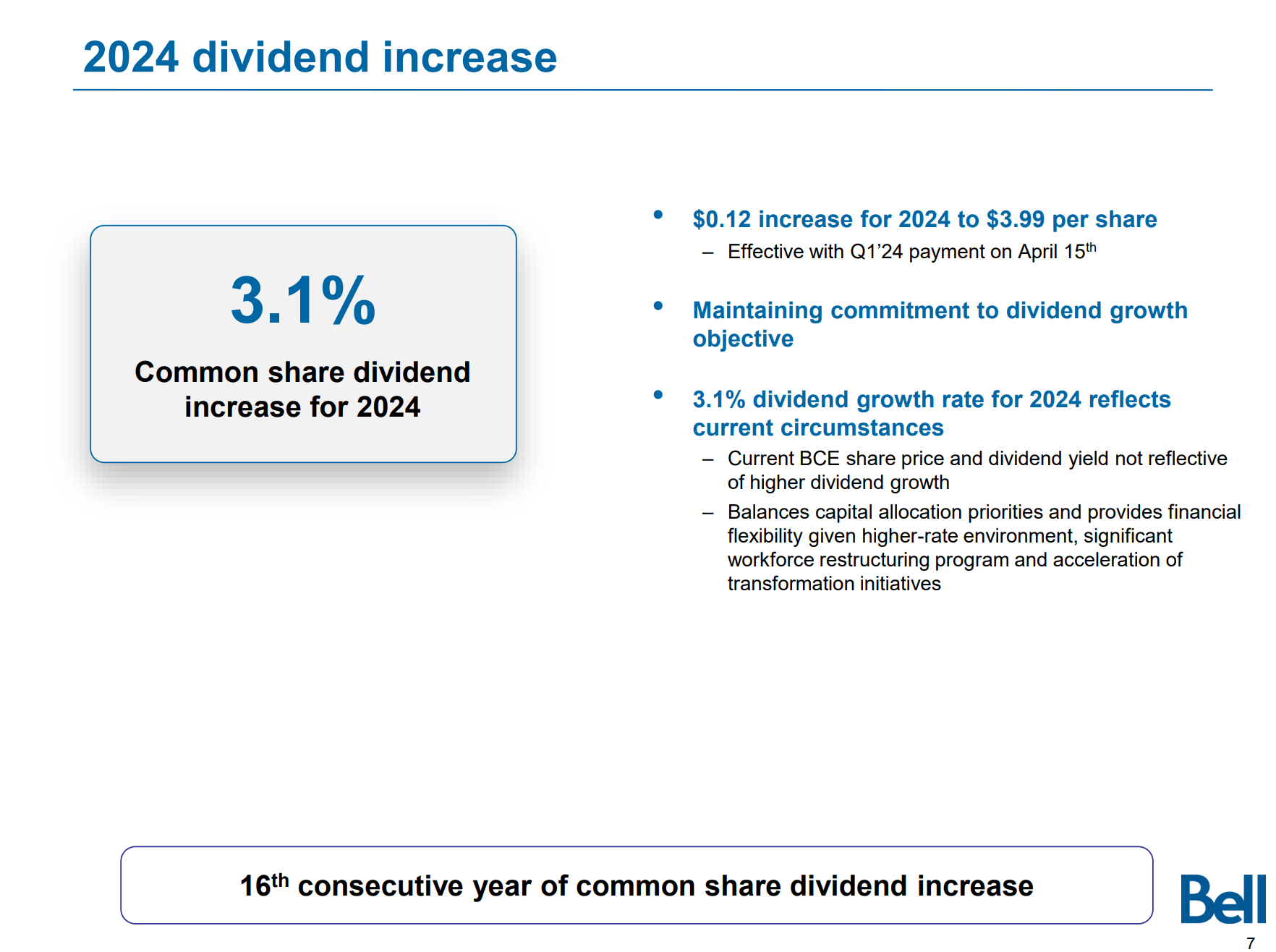

Normally, a high dividend yield could be a sign of a potential dividend cut. However, BCE recently increased its dividend by 3.1% to C$3.99 / share for 2024, so the dividend appears safe for the near term (Figure 6).

Figure 6 - BCE increased dividend 3.9% in 2024 (BCE investor presentation)

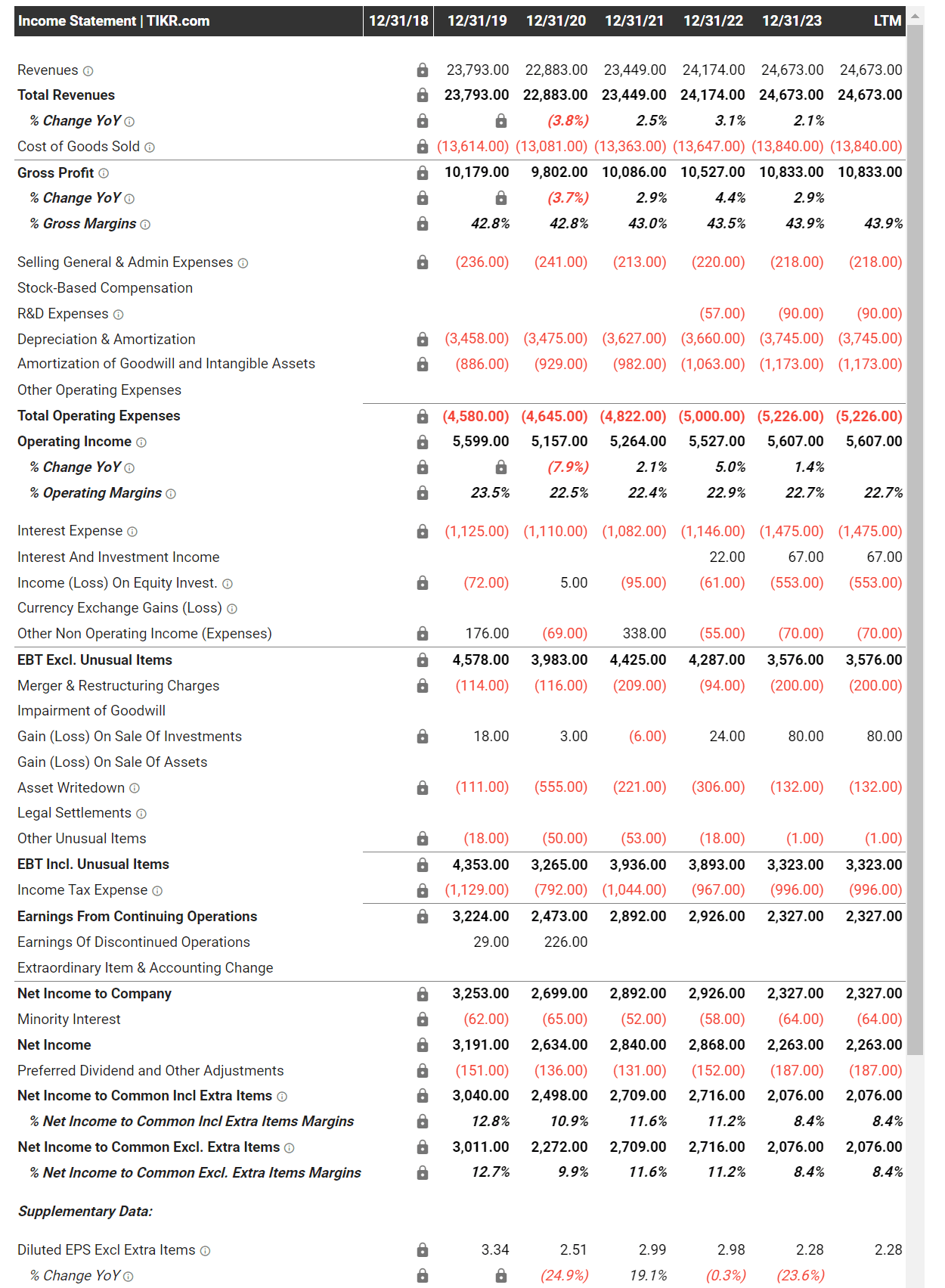

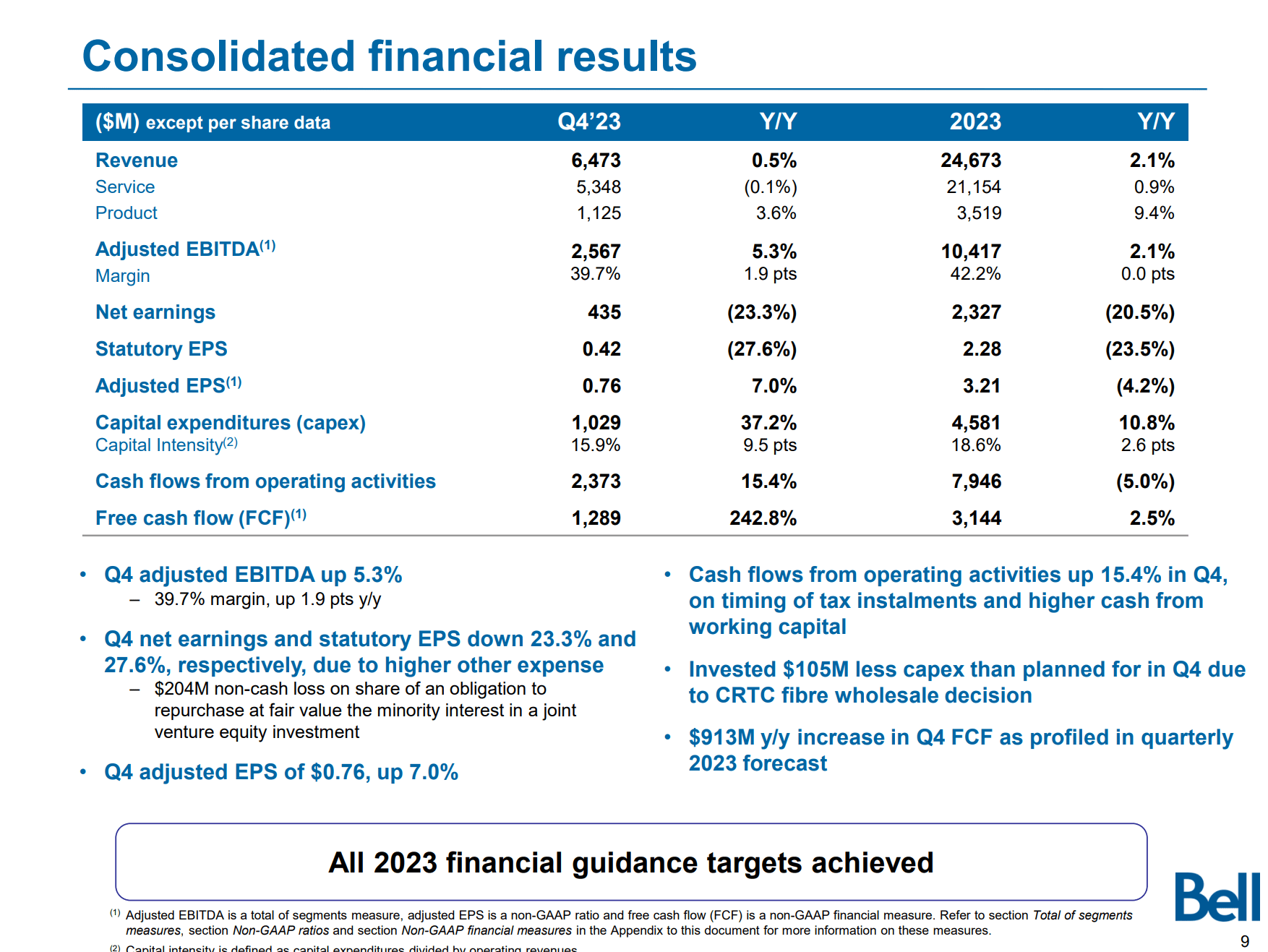

The second reason I am buying BCE for my retirement accounts is because of the company's stability. While BCE's stock price has tumbled by nearly 40% in the past 2 years (including dividends), BCE's financial performance has actually been fairly steady, with revenues growing 2.1% YoY to C$24.7 billion (Figure 7). On a 3-year basis, BCE's revenue CAGR is 2.5%. Operating margins have also been steady at ~22.5-23.0% in the past few years.

Figure 7 - BCE financial summary (tikr.com)

However, higher interest expenses and a string of asset writedowns and restructuring charges have put a dent to the company's net income, with net income falling 21% YoY to C$2.3 billion.

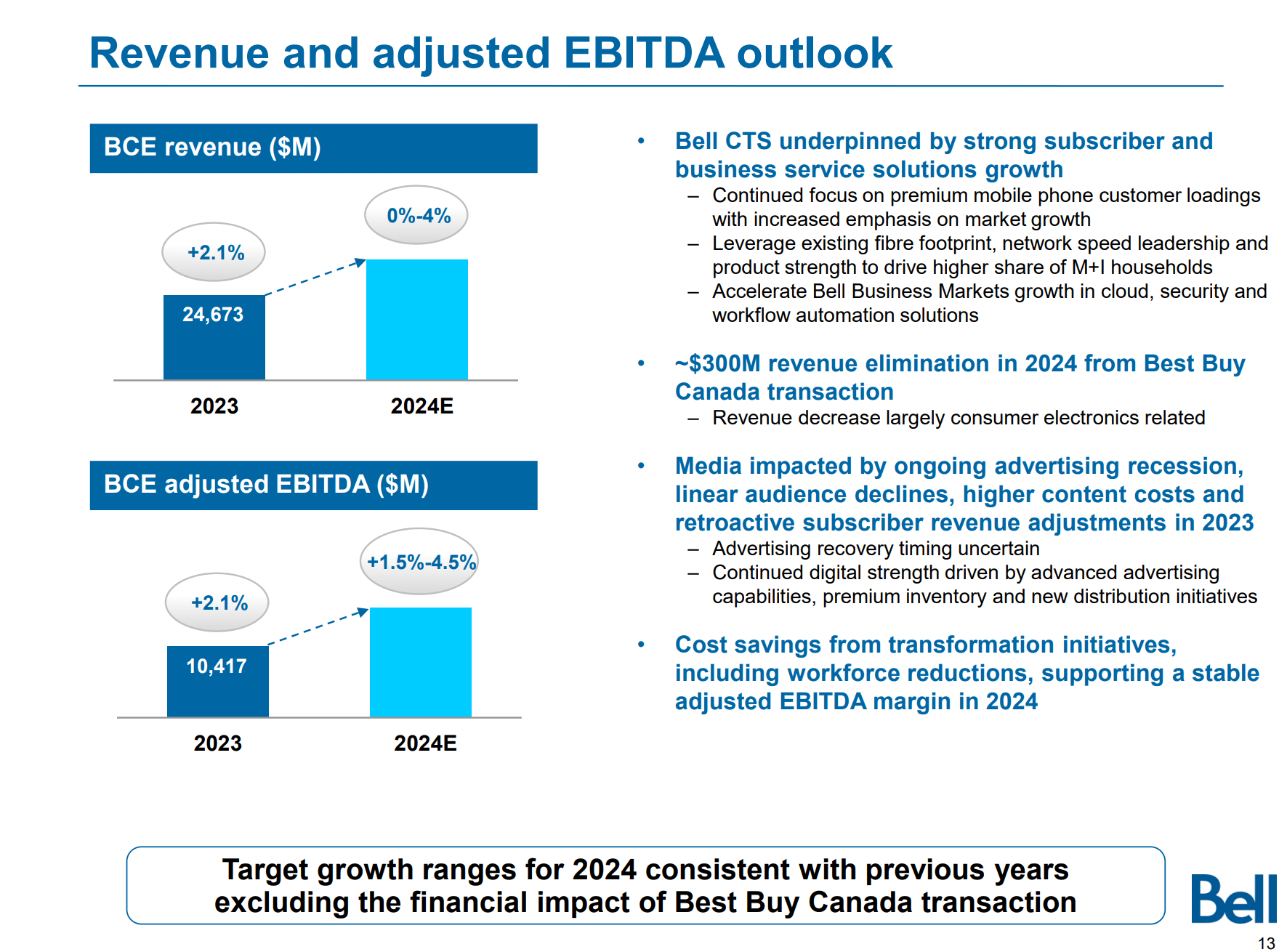

Looking forward, BCE expects continued steady modest growth in revenues and adjusted EBITDA, although ultimately, earnings may come in significantly lower due to additional restructuring charges and/or writedowns (Figure 8).

Figure 8 - BCE is projecting steady growth in 2024 (BCE investor presentation)

Valuation Appears 'Cheap'

Finally, and perhaps most importantly, BCE is now screening 'cheap'. With the bulk of its fiber network overhaul now completed, BCE's free cash flow profile should be expanding in the coming years as the company reaps the benefits of connecting millions of Canadian households with fiber-to-the-home ("FTTH").

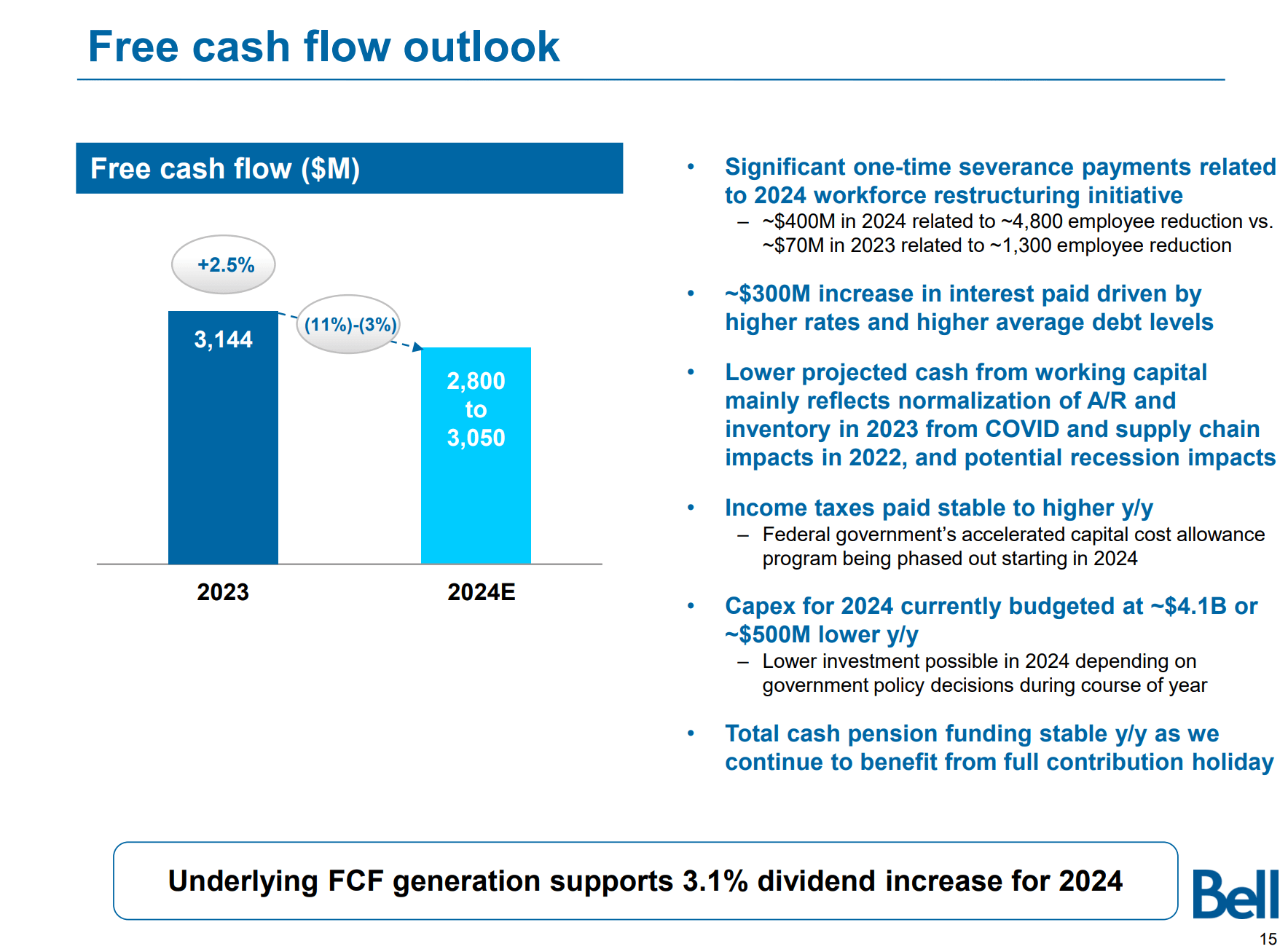

Excluding one-time severance costs of ~$400 million, BCE's 2024 equity free-cash flow outlook should be closer to $3.4 billion compared to $3.1 billion in 2023 (Figure 9).

Figure 9 - BCE FCF outlook (BCE investor presentation)

Compared to BCE's C$41 billion market-cap, this implies a free cash flow yield of 8.3%, which is sufficient to fund the company's generous dividend mentioned above.

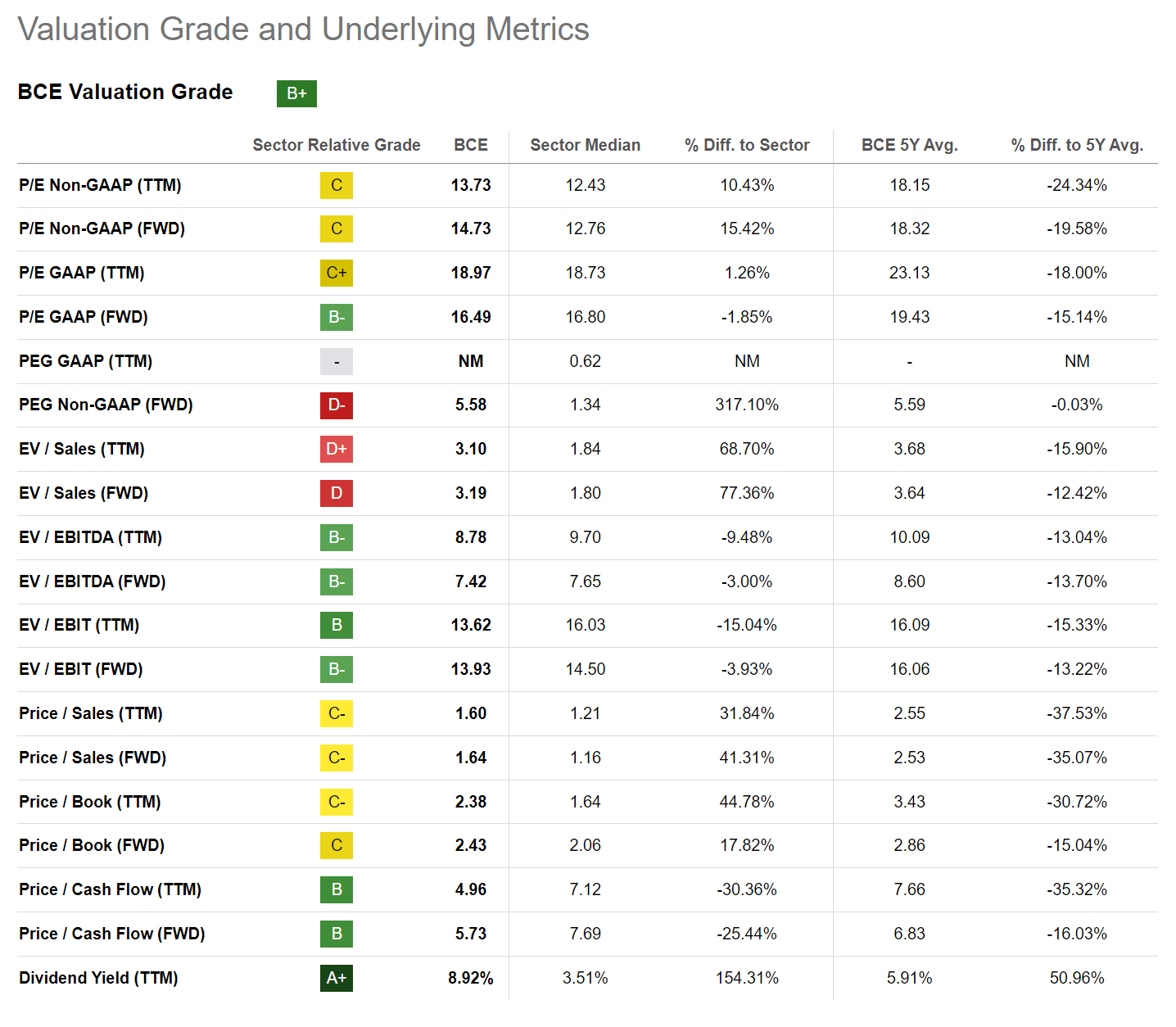

On a trailing basis, BCE is also trading at 8.8x EV/EBITDA, which is a discount to telecom peers at 9.7x (Figure 10). Fwd EV/EBITDA looks even better at only 7.4x.

Figure 10 - BCE valuation (Seeking Alpha)

Risks To BCE

While I believe BCE is attractively valued, we must also be cognizant of the risks involved. First, as competition continues to ratchet up in wireless services as Quebecor rolls out its services across Canada, we may see a deterioration in BCE's financial performance in the coming years. BCE's wireline business will also continue to shrink.

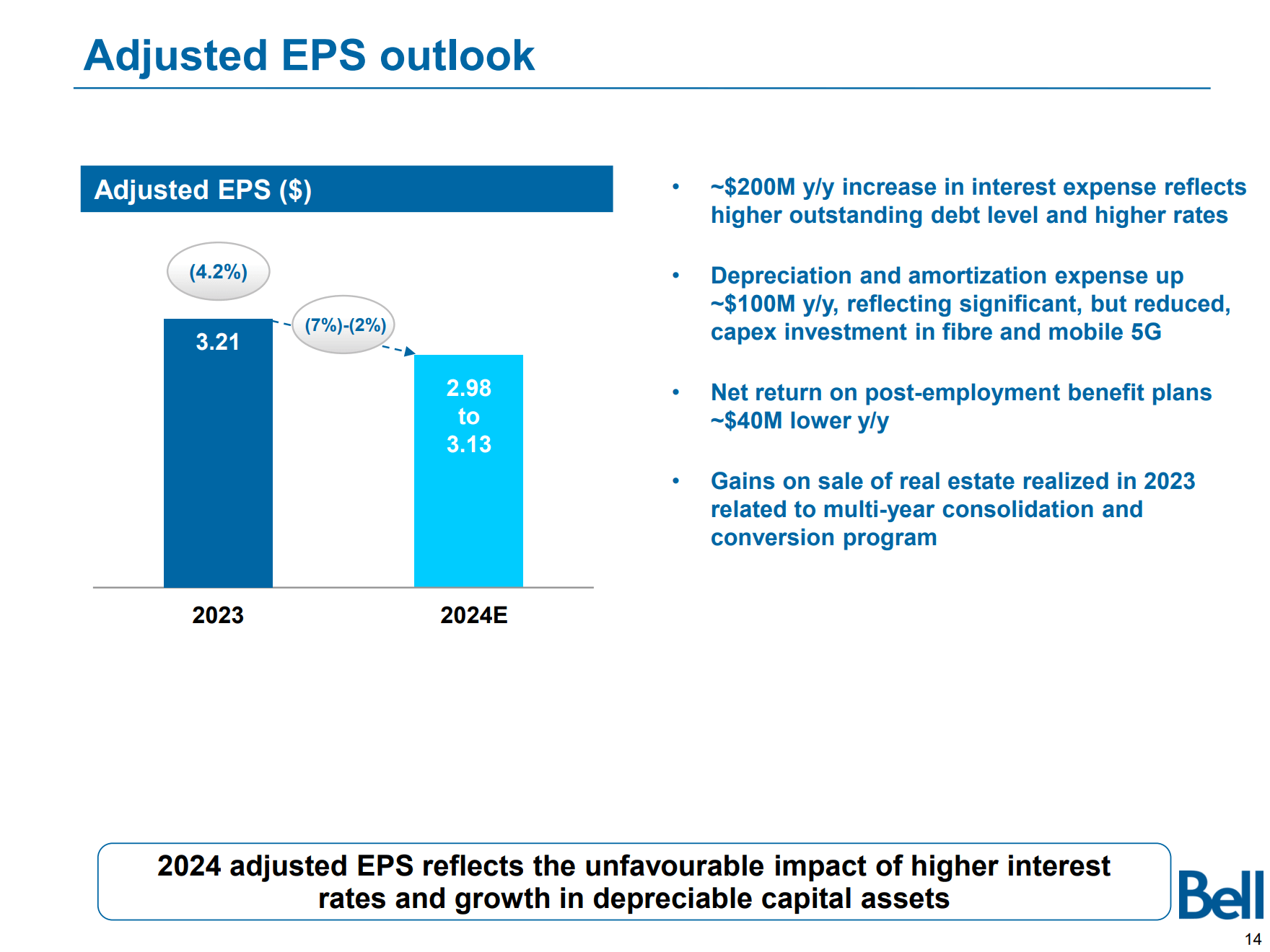

Furthermore, as we mentioned above, BCE has been mired in restructuring costs and asset writedowns for the past few years. For example, in 2023, BCE reported statutory earnings of C$2.28 / share compared to 'adjusted' earnings of C$3.21 (Figure 11).

Figure 11 - BCE has a habit of reporting adjusted earnings (BCE investor presentation)

While investors should overlook the occasional one-off restructuring charge, when it becomes a regular occurrence, are they really one-offs?

Finally, even if we use BCE's adjusted EPS figure of C$3.21 / share in 2023 and an estimated C$2.98 to C$3.13 in 2024, that still implies BCE will be paying more in dividends than it earns in income (Figure 12).

Figure 12 - BCE adj. EPS outlook (BCE investor presentation)

The difference between the two will need to be made up with increased borrowings. While companies can overpay dividends for a short-period of time if the shortfall is due to one-time issues, the situation cannot be maintained indefinitely. In fact, BCE has been paying more in dividends than its earnings for several years in a row, so this is definitely an area of concern.

Conclusion

In summary, I believe BCE is a good investment opportunity at the moment, as the company sports an 8.3% adjusted free cash flow to equity yield. This funds the company's generous 8.9% dividend yield.

While BCE is unlikely to 'shoot the lights out' in any given year, investors should be able to earn a reliable high single digit return at current valuations, with the possibility of excess returns if sentiment improves and BCE's valuation multiple expands. I am initiating on BCE with a buy rating.