Morsa Images

InterCure Ltd. (NASDAQ:INCR) has surprisingly rallied sharply off the post October 7 lows despite not having access to a prime facility in Israel. The cannabis business likely deserves a better stock valuation, but the dust needs to settle in both the Israel cannabis market and the conflict with Hamas. My investment thesis remains Bullish on the cannabis stock, even after the double off the lows already.

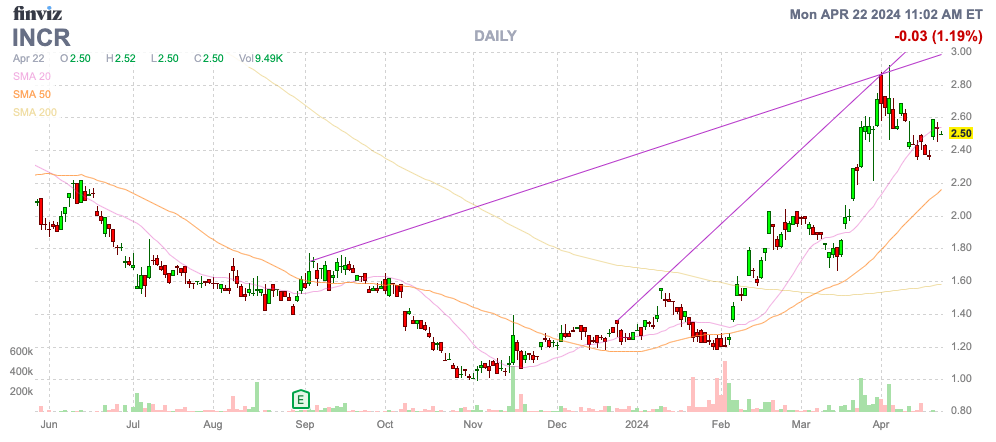

Source: Finviz

Still Waiting

No matter where in the globe, cannabis has constantly been hit by regulators and governments slowly implementing new rules allowing cannabis use. Israel is no different, with InterCure operating under a limited medical cannabis environment with the potential for full recreational sales in the future.

InterCure entered the 2H of 2023 with goals for revenues of at least C$150 million. Israel has approved some new regulations to advance medical cannabis prescriptions, but the country has still made no real steps to approve adult-use cannabis that offers a bigger opportunity.

Source: InterCure 1H'23 earnings release

While business has been decent, InterCure has been hit by unexpected events following the Hamas attack on Israel on October 7. The company has seen the facility in Kibbutz Nir Oz (the "Southern Israel Site") used by the Israel Defense Forces for a medical corps, reducing the company's access to the facility.

InterCure has cut revenues for the 2H of the year to ~C$51 million, but the IDF is expected to reimburse the company for the use of the facility. The company is only facing a short-term impact, with InterCure already working towards restoring the operations of the Southern Israel Site.

In January, Israel's Ministry of Health already eased the path for physicians approving medical cannabis. The move was expected to spur medical cannabis growth, with specialist doctors given more discretion to administer cannabis and changing some of the rules on when patients are eligible for medical cannabis.

Along with these changes in medical cannabis rules, InterCure agreed to buy Leon Pharm. InterCure will pay ~1.8 million shares to acquire the Israel-based pharmacy chain specializing in dispensing medical cannabis, with the company having 24 pharmacies already.

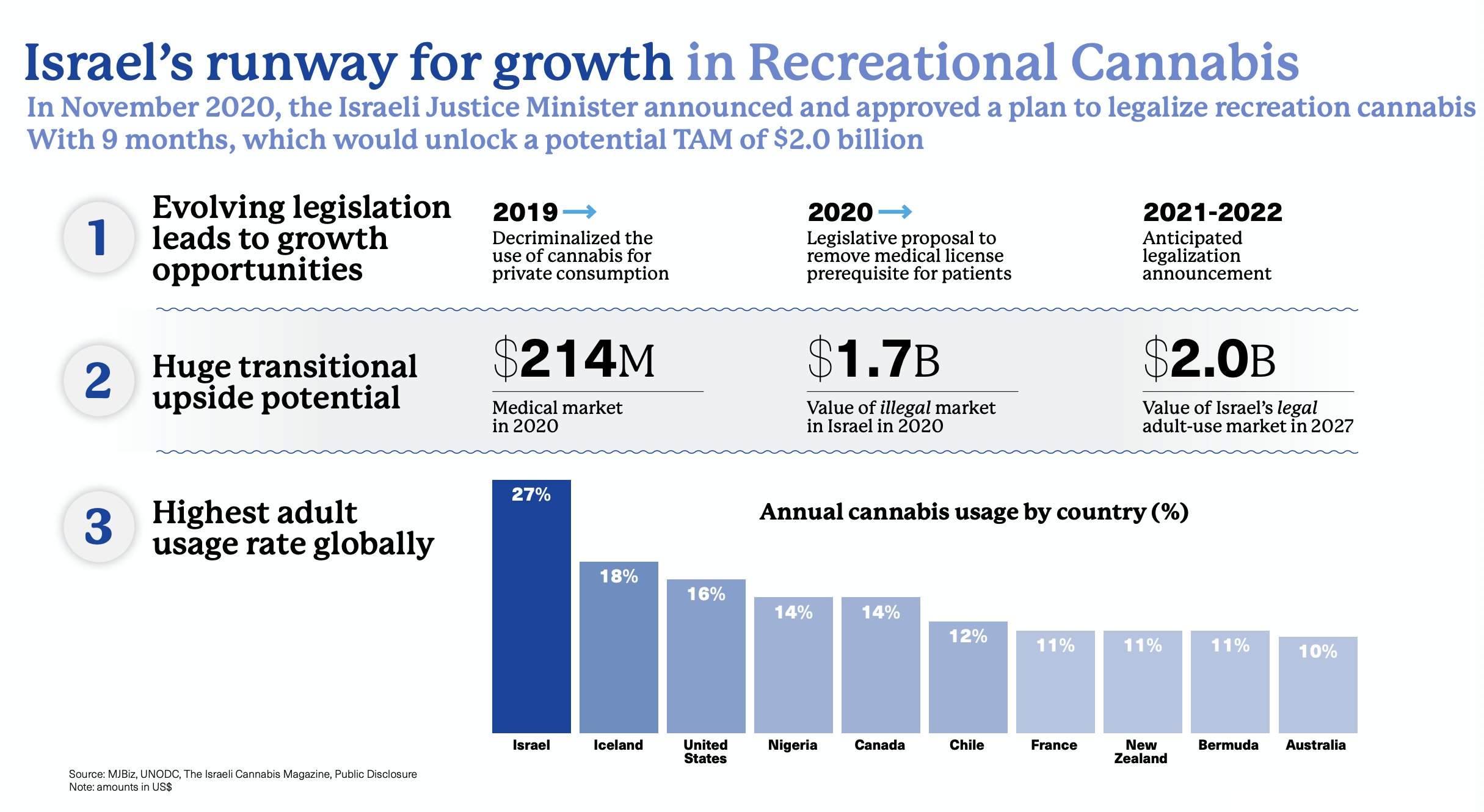

The big question remains when recreational cannabis will gain regulatory approval. The previous guidance had forecast the potential for a $2 billion recreational cannabis market by 2027 due in big part to an illegal market already reaching $1.7 billion back in 2020, but as with most markets, the regulatory approvals haven't occurred in a timely fashion.

Source: InterCure Aug. '21 presentation

Israel has decriminalized cannabis use for citizens over the age of 18 when used in private, but InterCure sales have stalled after the initial bump through 2022. Due to the war with Hamas in Palestine and the impact of the Southern Israel Site, the company hasn't provided a lot of updated financial targets other than forecasting a return to sequential quarterly revenue growth in 2024 with the benefit of entering the German cannabis market.

Dust Settles

InterCure only has a market cap in the $115 million range now, despite the business already being on a path for annual revenues topping C$150 million, or $110 million. The medical cannabis regulations expansion in Israel with forecasts for 70% growth due to the expansion of PTSD patients from the Israel-Hamas war along with the entry into Germany should only fuel growth in 2024, when the business returns to a normalized level as the dust settles in Israel.

The cannabis company is already profitable, with a quarterly EBITDA of ~C$5 million in the 1H '23. The company guided to an estimated 2H '23 EBITDA of C$5 million or 14% of revenues, even with the lower base due to the war.

InterCure had a cash balance of C$42 million at the end of the 1H. The company didn't provide any updated cash position, and reimbursements from the Israeli government will impact the year-end amounts.

The stock trades at just above 1x sales estimates. When the dust settles in Israel, InterCure should be back in growth mode with a thriving medical cannabis business in the country and the opportunity for global expansion into Germany with an already profitable business.

Takeaway

The key investor takeaway is that InterCure Ltd. stock remains a cheap option to play cannabis regulations around the world. The stock is still beaten down at only $2.50, though the ongoing war could lead to lower stock prices in the near term. Investors should use weakness to load up on the leading cannabis player in Israel with a global push.

If you'd like to learn more about how to best position yourself in under valued stocks mispriced by the market to start Q2, consider joining Out Fox The Street.

The service offers a model portfolio, daily updates, trade alerts and real-time chat. Sign up now for a risk-free 2-week trial to started finding the best stocks with potential to double and triple in the next few years.