mohd izzuan/iStock via Getty Images

Novartis (NYSE:NVS) is off to a strong start in 2024 with a $0.12 EPS beat and a $330 million revenue beat. The year-over-year comparisons by Seeking Alpha note an 8.6% decline in revenues compared to the same quarter last year, but this comparison includes the divested Sandoz division and the existing business that excludes Sandoz generated a 10% Y/Y increase in total revenues in the first quarter of the year along with a 22% Y/Y increase in operating income thanks to the exclusion of the lower margin Sandoz business.

The share price of Novartis is up modestly since I upgraded the stock from neutral in late October 2023 and the new and improved Novartis, as I labeled it after the spinoff of Sandoz, is in good shape and on track to deliver shareholder value in the following years.

Strong first quarter performance driven by core growth products

Back in October 2023, I argued that the spinoff of Sandoz was a great decision as it was a drag on margins and that a clean branded pharma business can have both better growth, higher margins and increased long-term profits. Generics are also a much lower barrier to entry business where price erosion is part of the value proposition versus branded drugs, but that makes it a business where it is tough to create shareholder value as competition with other generics result in a price race to the bottom.

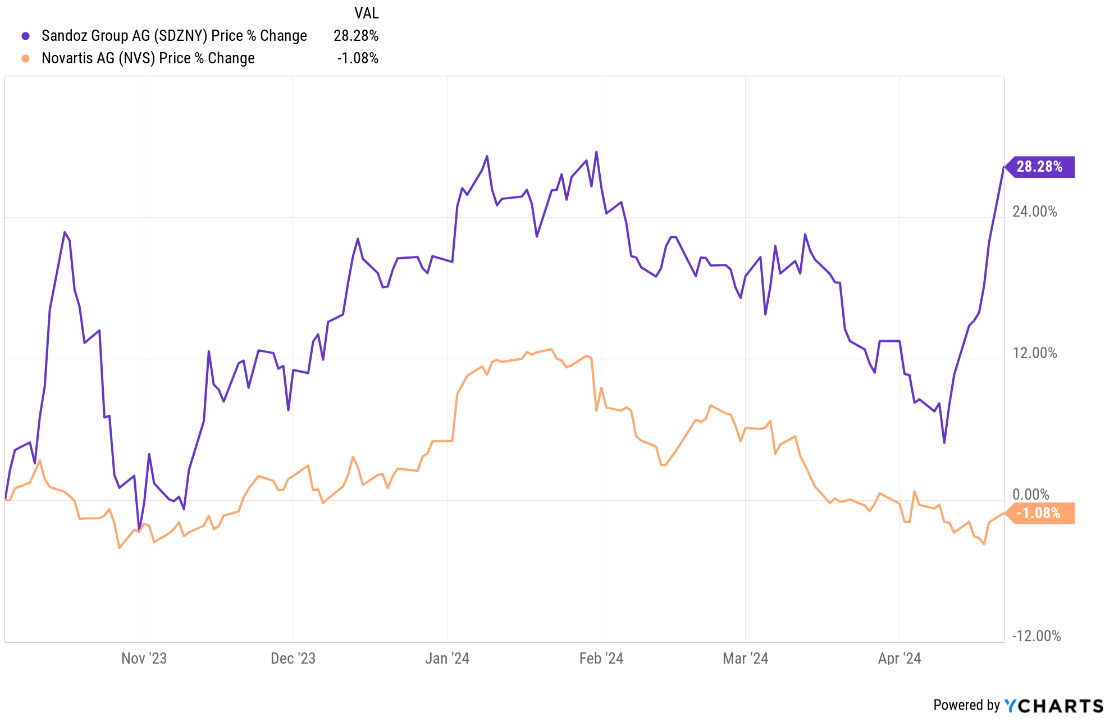

However, the share price performance of Sandoz since the spinoff is proving me wrong so far - it has significantly outperformed the share price of Novartis since the spinoff.

YCharts

Novartis delivered 10% Y/Y revenue growth in the first quarter of 2024, outperforming Street expectations. The growth was driven by the strong performance of all important growth products.

Entresto was very strong with 36% Y/Y growth and nearly $1.9 billion in quarterly sales. Entresto's growth accelerated from 27% in Q4 2023 and 30% in FY2023, and the growth was driven by continued strong demand following adoption of new guidelines for heart failure, but also by increased penetration in the hypertension market in China.

Cosentyx delivered another quarter of accelerating growth as sales grew 25% Y/Y to $1.28 billion, up from 21% growth in Q4 2023 and only 4% in FY2023. The majority of the growth was driven by the recent launches, including the new hidradenitis suppurativa indication, but also by volume growth in core indications.

Kesimpta, Kisqali, and Pluvicto remain in high growth mode with 66%, 54%, and 47% Y/Y net sales growth, respectively.

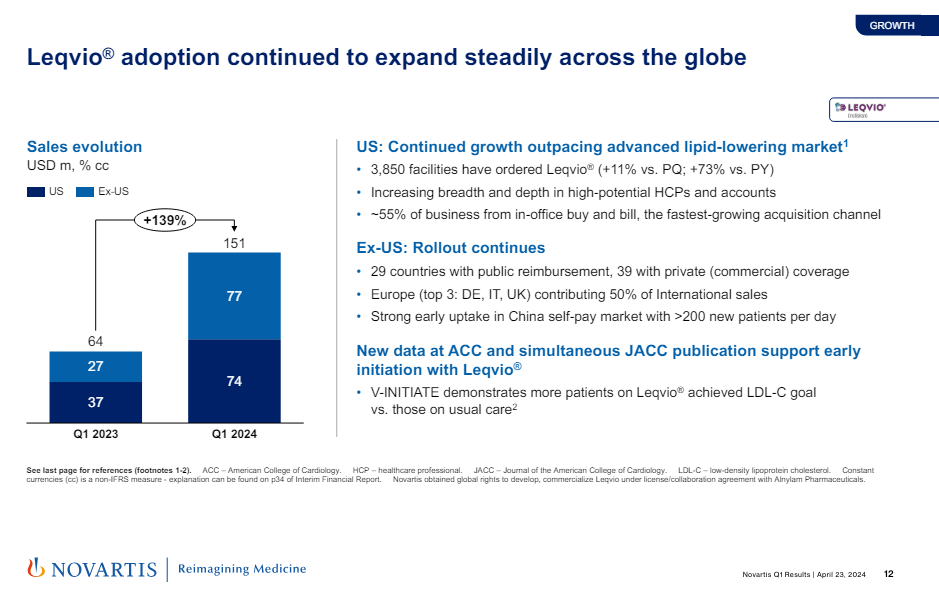

I remain very pleased and pleasantly surprised by the performance of the LDL cholesterol-lowering RNAi drug Leqvio. Quarterly net sales grew 23% sequentially and 136% Y/Y to $151 million, and Novartis is achieving this despite only having an LDL cholesterol-lowering label while competing with PCSK9 antibodies Repatha and Praluent with both having labels that include cardiovascular risk lowering on top of the lowering of LDL cholesterol. I believe Leqvio will become one of Novartis' largest products toward the end of the decade, driven by continued strong growth with the current label, followed by significant acceleration after what I expect to be positive data from the large cardiovascular outcomes trial in 2027.

Novartis investor presentation

I previously wrote about Fabhalta (iptacopan) as one of the more promising products for the second half of the decade, and it was recently launched for the treatment of PNH and generated $6 million in net sales in the first quarter. I expect strong growth going forward, driven by the existing PNH indication, geographic expansion, and by the likely accelerated approval for the treatment of IgA nephropathy and C3 glomerulopathy toward the end of 2024 and in 2025, respectively.

On the negative side, some of the larger products experienced Y/Y declines in net sales - Promacta/Revolade was down 5%, Tasigna 15%, and Lucentis and Gilenya 25%, each, with declines of the latter two driven by increased generic competition.

Full year revenue and operating income growth guidance increased, balance sheet leaves room for M&A

The strong revenue growth in the first quarter has driven the increase of the full-year net sales and operating margin guidance. Novartis now expects 2024 net sales to grow in high single-digits, up from mid-single digits, and core operating income to grow in low double-digits to mid-teens, up from the previous high-single digit growth guidance.

Net debt increased sequentially from $10.2 billion to $15.8 billion, but this was mainly due to the $5.2 billion annual dividend payment in March and the company's balance sheet leaves quite a bit of room for business development considering Novartis' significant cash flow generation along with continued dividend payments and share repurchases.

And although the company is generally focused on smaller tuck-in acquisitions, I would not exclude the possibility of mid-sized deals.

Conclusion

Novartis is off to a strong start in 2024 with a beat-and-raise quarter and with strong performance of nearly all key growth products. I continue to see the company as well-positioned to deliver long-term shareholder value, especially after the spinoff of Sandoz that made the company a pure-play, high-margin pharma company with a strong pipeline and a healthy balance sheet which it can utilize to give capital back to shareholders through dividends and buybacks and to enhance its product portfolio and pipeline through M&A.

The key risk in the medium term is Entresto going generic, and this would represent a sizable hit to overall company growth profile in the next few years. There are no new updates on the appeal to reverse the negative US District Court decision on the combination patent of Entresto that expires in July 2025.

I publish my best ideas and top coverage on the Growth Stock Forum. If you're interested in finding great growth stocks, with a focus on biotech, consider signing up. We focus on attractive risk/reward situations and track each of our portfolio and watchlist stocks closely. To receive e-mail notifications for my public articles and blogs, please click the follow button. And to go deeper, sign up for a free trial to Growth Stock Forum.