Jeremy Poland

Note:

I have discussed Enphase Energy, Inc. (NASDAQ:ENPH) previously, so investors should view this as an update to my earlier coverage of the company.

After the close of Tuesday's session, leading microinverter and battery storage solutions supplier Enphase Energy Inc. or "Enphase" reported another set of disappointing quarterly results with revenues and profitability coming in well below consensus expectations:

Press Releases / Regulatory Filings

While revenues in Europe increased approximately 70% sequentially, sales in the company's core domestic market were down by 34% quarter-over-quarter, which management attributed to seasonality and a further softening in U.S. demand.

That said, reported results were still within the guidance ranges provided in the Q4/2023 earnings release and the company managed to generate $41.8 million in free cash flow, which was essentially allocated to share repurchases:

Press Releases / Regulatory Filings

The company spent an additional $60 million by withholding shares to cover taxes for employee stock vesting and options, which reduced outstanding diluted shares by 480,735 shares.

Enphase ended the first quarter with $1.63 billion in cash, cash equivalents, and marketable securities, down slightly from the $1.70 billion reported at the end of last year.

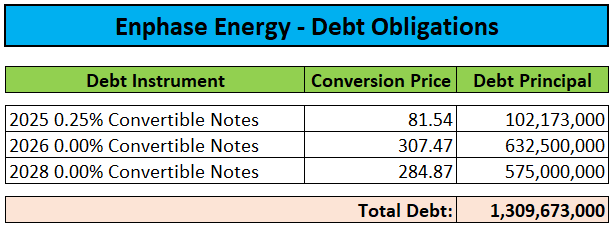

Debt remained unchanged at $1.31 billion:

Regulatory Filings

However, Q2/2024 guidance, while up sequentially, came in well short of consensus expectations again:

Company Press Releases

While disappointing, the weak Q1 performance and slower-than-expected recovery has been predicted by a number of analysts in recent weeks as Enphase's heavy exposure to the flagging U.S. market continues to impact the company's financial performance.

On the conference call, management reiterated previous expectations for channel inventory to normalize by the end of Q2 and remained optimistic about both Europe and the United States.

That said, a number of analysts on the call appeared to be underwhelmed by the mediocre outlook and repeatedly asked management for additional color on the company's expectations for the remainder of the year.

Considering the ongoing weakness in the company's core U.S. market, I would expect analysts to reduce estimates even further, with the consensus 2024 revenue expectation likely to come down to below $1.5 billion from the current $1.59 billion number over the next couple of weeks. In addition, I project the consensus estimate for earnings per share to decrease from $3.22 to approximately $2.50.

At least in my opinion, estimates for 2025 also look overly aggressive with expectations for an almost 50% sales increase difficult to justify, particularly with interest rates in the United States now likely to stay higher for longer.

Bottom Line

Enphase Energy reported another set of weak quarterly results and issued disappointing Q2 guidance well below consensus expectations as the company continues to experience headwinds in its core domestic market.

While management expects the trough to be behind the company, the slower-than-expected industry recovery is likely to result in another round of estimate and price target cuts.

In contrast, the encouraging sales trends on the other side of the Atlantic bode well for competitor SolarEdge (SEDG) which derives more than 60% of its sales from Europe.

Given the mediocre outlook, I do not see any reason to initiate or add to existing positions at this point. Consequently, I am reiterating my "Hold" rating on Enphase Energy's shares.

Massively Outperform in Any Market

Value Investor's Edge provides the world's best energy, shipping, and offshore market research. Even during turbulent market conditions, our long-only models have outperformed the S&P 500 by more than 30% YTD.

We also offer income-focused coverage geared towards investors who prefer lower-risk firms with steady dividend payouts. Our 8-year track record proves the ability of our analyst team to outperform across all market conditions. Join VIE now to access our latest top picks and model portfolios.