FreshSplash/E+ via Getty Images

The LMP Capital and Income Fund Inc (NYSE:SCD) has been successfully delivering a strong performance over the past years, outperforming the benchmark and the peer group.

SCD's portfolio composition seems well positioned to navigate this current macroeconomic environment. The fund trades at somewhat more reasonable valuations compared to the broader index and its sector exposure are a positive now. Its overweight exposure to energy can work as an inflation hedge, and its allocation to the real estate sector is supposed to deliver good returns when interest rates start to drop.

On the flip side, current discount to NAV is near top levels seen in the past, which makes share prices more vulnerable for the time being, since the duration of the current market pullback is unclear. That said, while investors may be cautious about this fund in the short term, I see SCD as a fund that is worth keeping in the watchlist.

Fund Description & Highlights

The objective of the fund is to deliver total return, with emphasis on generating a stream of income. Broadly speaking, SCD is expected to invest in a number of securities, including stocks, MLPs, REITs and fixed income. However, the fund has maintained just a marginal exposure to fixed income, with the vast majority of the portfolio invested in stocks, MLPs and REITs.

As of March 31st, 2024, the fund was 64.8% invested in stocks, 16.1% in energy MLPs, 11.0% in equity REITs, 5.0% in convertible preferred stocks and only 4.2% in bonds, while 3.1% remained in cash.

We have also seen some rotation in the portfolio since the end of 2022, as the fund has decreased its allocation to MLPs from 24% to 16%. Meanwhile, the exposure to REITs increased from 6% to 11% over the same period, as this sector is viewed with a better risk/reward ratio after the underperformance compared to the overall S&P 500, dragged down by the rate-hike cycle.

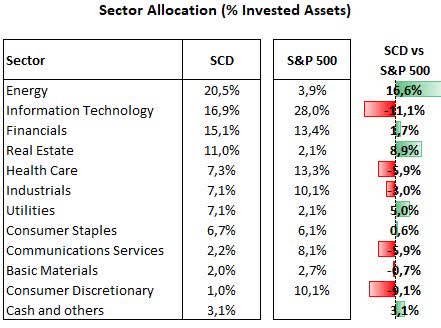

Putting together all equities held by the fund, including MLPs and REITs, SCD's largest allocation overall is in the energy sector, as expected, with 20.5% of total equities (16.1% from MLPs and 4.4% from other companies in the energy group). The second largest exposure is to the information technology sector with 16.9%, followed by financials with 15.1%, real estate 11.0%, health care 7.3%, industrials and utilities 7.1% each, consumer staples 6.7%, communications services 2.2%, basic materials 2.0%, and consumer discretionary 1.0%.

Overall, SCD is somewhat a value-oriented portfolio, as its average price to earnings ratio at 17.3 is well below the S&P 500 of nearly 21.9. That is influenced by certain distinctions with regards to the sector exposure. As we can see below, SCD has overweight allocations on lower multiples sectors, such as energy (+16.6%) and utilities (+5.0%), but also an underweight position in typically higher multiples sectors, such as information technology (-11.1%) and health care (-5.9%).

Franklintempleton, morningstar's websites, consolidated by the author

SCD has a relatively concentrated portfolio with only 72 companies. Of those, the top ten constituents account for nearly 32% of the total portfolio, and are a mix of MLPs, such as Energy Transfer Equity LP (ET) and Enterprise Products Partners LP (EPD), big techs (Microsoft (MSFT), Apple (AAPL) and Broadcom (AVGO)), and financials such as Blackstone (BX) and Apollo Global Management (APO).

As we can see, despite the underweight exposure to the information technology sector, the fund remains with core positions in big players in this sector, which might allow the fund to benefit from a continuation of the tech rally seen for much of the past years

Likewise, the fund's investment in MLPs is also concentrated, with nearly 80% allocated to a selection of 5 big players (Energy Transfer Equity LP, Enterprise Products Partners LP. MPLX LP (MPLX), Oneok (OKE) and Plains GP Holdings LP (PAGP)). This allocation to large-cap energy companies provides relatively better earnings predictability, suggesting lower volatility for the portfolio.

In summary, the fund has a heavy allocation of nearly 88% to equities. While that makes the fund more exposed to stock market volatility, its allocation to MLPs and REITs offers diversification to investors and still upside potential from different spots of the market.

SCD's Solid Returns Over Time

SCD is a special type of allocation fund. While many funds in this category employ a broad allocation strategy, the bulk of SCD exposure is in equities, such as common stocks, MLPs and REITs.

In spite of that, SCD has defined a blended benchmark composed of 65% S&P 500 and 35% Bloomberg U.S. Aggregate Bond Index as a reference to measure its relative performance.

As we can see below, despite the recent pullback, the performance of SCD has been solid over time, outpacing the blended benchmark in most timeframes, except the 10-year period, as the strong bull market in stocks boosted S&P 500 up more than 200% over the period. It is fair to say, though, that the poor return of the U.S. aggregate bond has also contributed to SCD's outperformance over the period.

We can see as well that SCD has delivered much better results compared to other closed-end funds. Here we use roughly 20 funds adopting allocation and equity strategies in the U.S. market as a reference, and in both cases SCD has largely outperformed the peer group. As a remark, we have also used equity funds for comparison purposes, given SCD's allocation has been skewed to equities.

Seeking Alpha, consolidated by the author

Looking ahead, my view is that SCD's outperformance can continue, as the fund's value-oriented approach is likely to be an advantage as the broader market is still trading at high multiples, despite the recent pullback.

Moreover, SCD's significant allocation to the energy sector can be a positive, as oil prices have historically shown a positive correlation with inflation, which could benefit SCD's returns if inflationary pressures persist.

Distributions Underscored By Gains From Investments

SCD's current distribution rate is roughly 9.2%, which is competitive compared to the average of the peer group in the range of 8 to 9% and significantly higher than treasury yields (4.9% for 2 years and 4.6% for 10 years).

That has been a major contributor to the fund's income. As we can see from the annual report ended on Nov 30, 2023, the fund's portfolio generated $6.8 million from dividends, taking advantage of an invested portfolio that yields 4.3%. This is considerably higher than S&P 500's yield of nearly 1.3%, thanks to the fund's large exposure to MLPs, that typically yield above 7%, and also REITs and utilities to a lower extent.

In addition, the fund also generated a modest $0.3 million from interest. After netting out foreign taxes, total investment income was $7.03 million. But the fund also had total expenses reaching as high as $6.48 million, as a reflection of interest expenses of $3.47 million during the period, driven by interest rates averaging 5.6% over the loan balance.

This resulted in a net investment income of only $0.55 million, compared to $6.47 million accumulated in the previous year of 2022.

Fortunately, consistent with the fund's strong total return in 2023, there was $26.37 million in realized gains from investments plus $4.39 million in unrealized appreciation during this timeframe. That was enough to produce an increase in net assets from operations of $25.31 million and cover distributions of $23.15 million over the period.

Nearly 53% of total distributions, or $12.08 million, was considered as distributed earnings, while the remaining $11.07 million recorded as return of capital. As a result, total net assets decreased just 0.4% to $255.43 million, as opposed to a large decrease of roughly 10% seen in 2022.

From a historical perspective, the fund already had a steep drop of above 10% in net asset back in 2020, driven by a negative total return of roughly 6% in NAV.

As mentioned earlier, gross expenses was the main detractor in 2023, given the weighted average interest rate on loan of 5.60% well above previous years (2.03% in 2022, 0.79% in 2021 and 1.44% in 2020) that led net expenses to net assets ratio up to 2.62, compared to 1.67 in 2022, 1.33 in 2021 and 1.65 in 2020, and slashed the net investment income to net assets ratio to 0.22, compared to 2.45 in 2022, 3.35 in 2021 and 4.40 in 2020.

A point of concern here is to which extent the 'higher for longer' interest rates scenario that we live now is going to maintain net expenses under pressure. If rates are kept unchanged for much of 2023, ending the year with just 50 base points of rate cuts from current levels, we are likely to see the weighted interest rate on loan near the 5% mark again and total expenses around $6 million, absent any mitigation measures taken by the fund management.

Nonetheless, higher expenses are expected to be transitory and should not become a major issue as long as the fund can generate enough gains from investments to cover distributions. That said, the ability of the fund to manage this mixed scenario is certainly something to watch as the year progresses and the rate trajectory may finally converge to the downside.

SCD Price/NAV Discount Not Compelling For Now

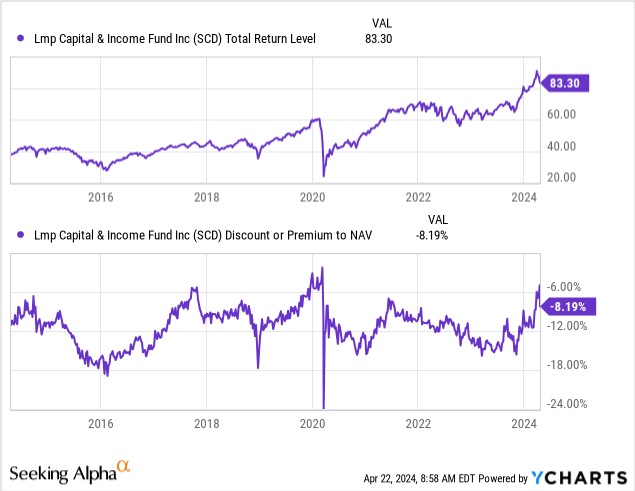

Following the rally in the stock over the recent months, the discount in shares of SCD versus its NAV has narrowed somewhat from double-digit to 6%. Although the recent market pullback prompted the discount back to 8%, it seems to me that current discount is still near historical tops seen in 2017 or 2022 and, therefore, it is not offering the best entry point for potential investors, which, in my view, should be closer to -11%, the midpoint of the 6% to 15% discount range at which it has traded at recently.

Overall, while SCD seems not compelling now from the discount perspective, I see the fund well-positioned going forward, as its valuation is lower than the benchmark and its portfolio composition is likely to outperform, given the current economic backdrop, since SCD's oversized allocation in the energy sector is expected to work as an inflation hedge, as oil prices play an important role in the current inflationary backdrop. On the other hand, the fund's exposure to sectors battered by higher rates, such as Real Estate, is expected to perform well when the FED finally starts to reduce rates.

This portfolio's overweight allocation to MLPs and REITs sets the fund apart from its peers, in my view, as many tend to be overly allocated to big tech stocks or exposed to high-yield fixed income vehicles.

In any case, my view is that SCD is an interesting fund, but I am reluctant to rate it as a buy now, given short-term pressures on the expenses side and an occasional impact on distributions. Adding to my cautious stance, the current discount is not appealing on a historical basis.