Richard Drury

Old National's (NASDAQ:ONB) Q1 2024 results were recently released:

- Non-GAAP EPS of $0.45 beat by $0.02.

- Revenue of $433.98M (-4.0% Y/Y) misses by $6.02M.

At first glance, these do not seem exciting, but actually the quarterly report was positive. The bank maintained its competitive advantage on deposits, in fact their cost remained quite low; net interest income may have hit its bottom and is expected to rise in the coming quarters.

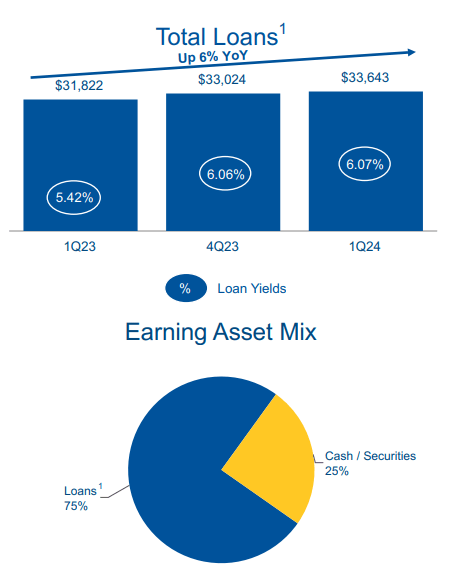

Loans and securities portfolio

Old National Bancorp (ONB) Q1 2024 Earnings Call

Total loans reached $33.64 billion, up 6% from the same quarter last year. Much of this growth was due to the C&I loans segment rather than CRE loans, and the motivation is purely economic. Demand for C&I loans is still stable and is likely to remain the main growth driver for this bank throughout 2024:

With the rate environment right now, the numbers just don't work at the same level that they used to. So CRE volume across our footprint is down just by market dynamics, not because we've changed our underwriting. We're still selectively adding new clients in CRE as well. But certainly more of the growth is going to come in C&I, where we think we're really well positioned.

As for the average return on total loans, it was 6.07%, an almost flat growth from the previous quarter. In addition, the bank kept its exposure to cash/securities high, now at 25% of total assets.

Old National Bancorp (ONB) Q1 2024 Earnings Call

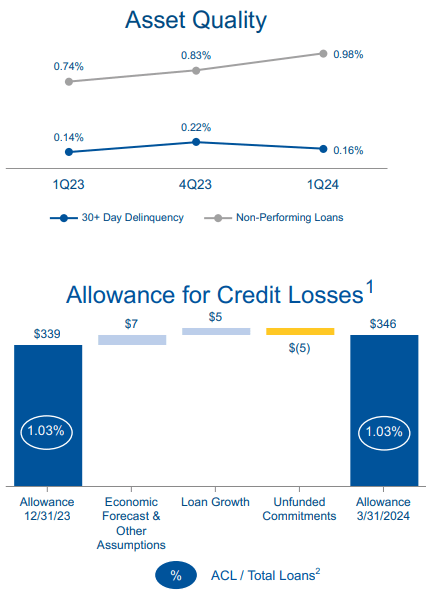

Finally, the credit quality of ONB's loans stays under control. Non-performing loans increased slightly and reached 0.98%, but for the time being there is no concern that this figure will reach worrisome levels in the coming quarters. Based on management's expectations, this is a small deterioration caused by the adverse macroeconomic conditions, but it will not be followed up.

Let us now turn to the securities portfolio, an important component for this bank.

Old National Bancorp (ONB) Q1 2024 Earnings Call

Both AFS and HTM securities have barely changed in size over the past year, but there could be important news in the coming quarters. In fact, over the next 12 months, including interest and principal, the bank will get cash inflows of $1.30 billion. That amount could be reinvested at rates above 5%, which would bring up the current average yield of 3.47%. New bonds yield about 200 basis points more than maturing bonds, and this could be an important growth driver for net interest income/margin.

Reinvestments would always be in high-quality bonds that would not interfere too much with the current asset allocation:

- 76% U.S. treasuries and agency-backed securities.

- 16% highly-rated municipal securities.

- 8% corporate and other.

- All CMBSs are agency-backed.

Be that as it may, even though a good portion of the securities will mature in the next year, the problem of unrealized losses persists since the average duration of the portfolio is 4.3 years. It takes time before they settle down to zero:

- AFS securities are at a loss of $914 million.

- HTM securities are at a loss of $454 million.

The former are already accounted for in the TBV, negatively impacting the AOCI item, the latter are not. In total, we are talking about a figure of $1.36 billion, which is rather high considering that total equity is $5.59 billion.

Old National Bancorp (ONB) Q1 2024 Earnings Call

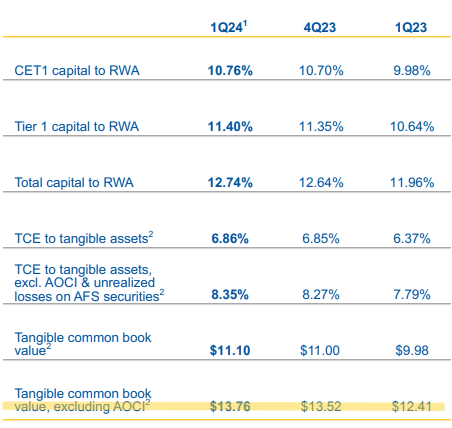

As you can see from this image, excluding AOIC, the TBV per share would be significantly higher than it is today: $13.76 vs $11.10.

The weight of unrealized losses is putting pressure on the TBV, and consequently on the price per share. With the market discounting fewer and fewer cuts and stickier-than-expected inflation, this situation could last much longer. Mainly, it will depend on when the Fed decides to cut rates.

Deposits and net interest margin

Old National Bancorp (ONB) Q1 2024 Earnings Call

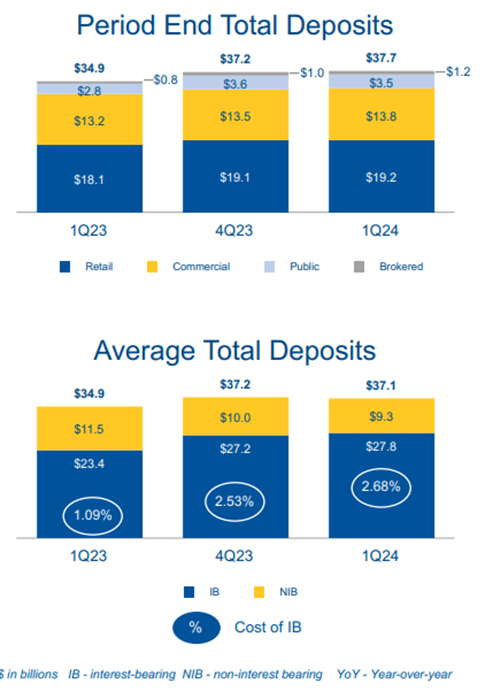

Total deposits (period end) reached $37.70 billion, an increase of $500 million over the previous quarter and $2.80 billion over last year. The current figure largely covers loans; in fact, the Loan to Deposit ratio is only 89%. So, ONB does not need to issue expensive certificates of deposit in order to obtain capital: its deposits meet its financial needs.

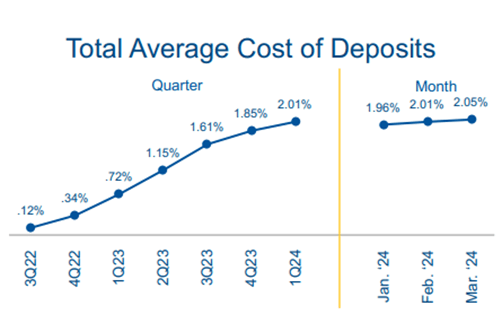

The most positive aspect concerns their cost, in fact, it averages 2.68%, which is quite low compared to peers. Moreover, when the $9.30 billion of non-interest-bearing deposits (25% of total deposits) is also taken into account, the overall average cost is reduced to only 2.01%.

Old National Bancorp (ONB) Q1 2024 Earnings Call

This is probably the greatest advantage of this bank and is due to the reliability it has conveyed to its customers over the years.

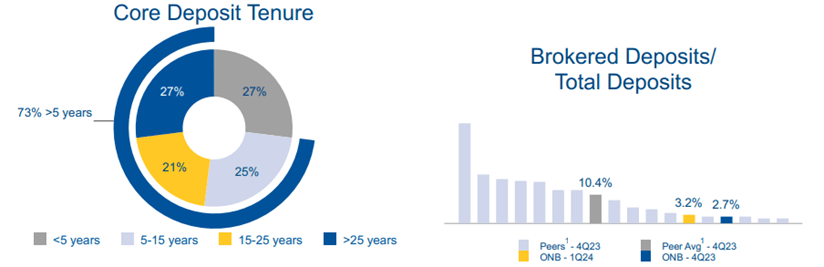

Old National Bancorp (ONB) Q1 2024 Earnings Call

Suffice it to say that 27% of depositors have been choosing ONB for more than 25 years, and more than 73% have been depositing their savings for more than five years. For this reason, this bank is not overexposed to expensive Brokered Deposits.

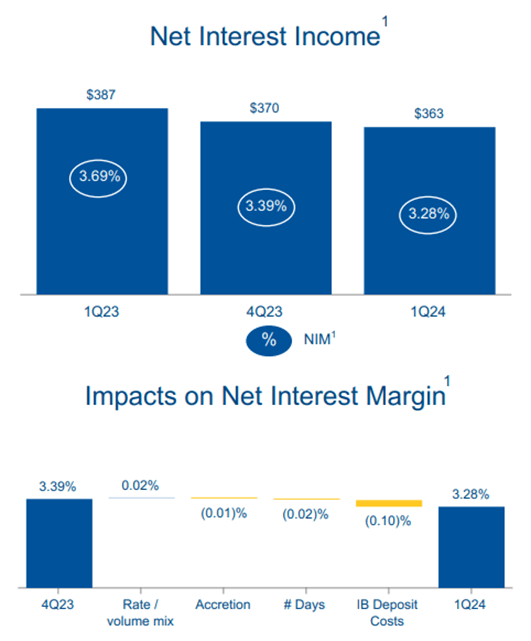

In the face of such efficient liability management, we might expect net interest income/margin to continue to rise, but in reality this has not been the case.

Old National Bancorp (ONB) Q1 2024 Earnings Call

While the cost of deposits has been kept under control, as we saw earlier, the average yield on loans is struggling to increase: compared to the previous quarter, it increased by only one basis point. However, there is positive news; in fact, management expects the bottom to have been reached this quarter:

New loan production rates in the high 7% range and marginal funding costs in the low 4% range support our expectation that net interest income has bottomed out in the first quarter. The investment portfolio increased very modestly in the quarter due to reinvestment of cash flows, partly offset by changes in fair values, and the duration was effectively unchanged. As we've mentioned in past calls, new money yields are running 200 basis points above back book yields, and we have approximately $1.3 billion in cash flows expected over the next 12 months.

John Moran, CFO.

In other words, the cost of deposits will not be able to increase as much, and the spread with new loans will be more profitable for the bank. In addition, the repricing of 200 basis points on maturing securities will generate more interest income. The potential for growth is there, and the low Loan to Deposit ratio allows some flexibility in choices.

Old National Bancorp (ONB) Q1 2024 Earnings Call

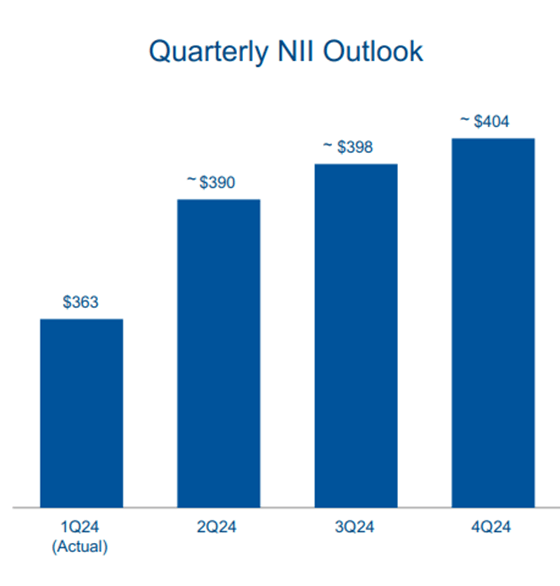

As you can see, net interest income is expected to rise over the next three quarters, but there is a premise to be made. These are management's estimates, and they discount by the end of 2024 a 5-year Treasury at ~4.30%, three rate cuts, and non-interest-bearing deposits of 23% of total deposits. These are assumptions and will not necessarily correspond to reality.

My doubts are mainly about the rate estimates, as they diverge from what the market expects. Right now, three rate cuts are discounted for end-2025, not end-2024.

Conclusion

Old National is a bank with a long history behind it and customers who trust their services. In fact, there is a strong component of non-interest-bearing deposits and the average cost of deposits is lower than that of peers. The problem here lies on the asset side, where loans have stagnant yields and securities have significant unrealized losses.

C&I loans are the ones that management will focus on the most in order to increase interest income; at the same time, maturing securities will be replaced by others with higher yields. It would seem that net interest income has bottomed out, but much will depend on the Fed's monetary policy. In case of no cuts in 2024 (not so unlikely), I think the guidance will be revised downward.