JHVEPhoto

Investment thesis

My previous bearish thesis about Advanced Micro Devices (NASDAQ:AMD) aged decently since the stock notably underperformed the broader market since January. The company's Q1 earnings release is approaching, and I am cautious about it. Intel's (INTC) fresh earnings release did not add optimism to me as the CPU giant's Q2 guidance has been much weaker than expected by Wall Street analysts. Apart from Intel's weak Q2 guidance, AMD also has its big company-specific problem of sky-high inventory. I expect this factor to weigh on the company's profitability expansion in the next couple of quarters, and there is even a risk of impairing these inventories given the rapid pace of advancement in the chipmaking industry. AMD's generous valuation appears to be underserved, given the two big red flags I have mentioned above. All in all, I reiterate "Sell" rating for AMD.

Recent developments

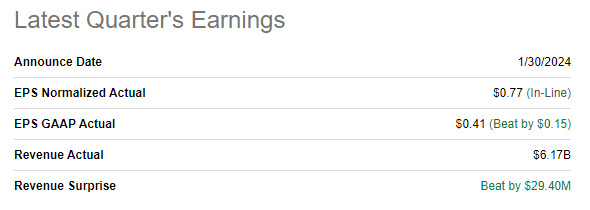

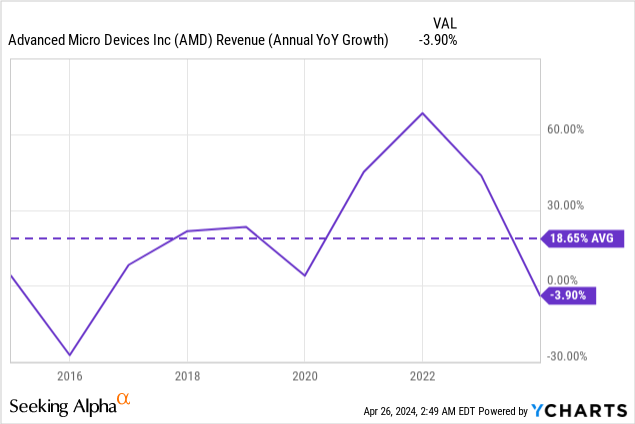

AMD released its latest quarterly earnings on January 30, when the company surpassed consensus expectations. In Q4, AMD's revenue increased by 10% YoY and the adjusted EPS expanded from $0.69 to $0.77. For the full fiscal 2023, AMD's revenue declined by 3.9%.

Seeking Alpha

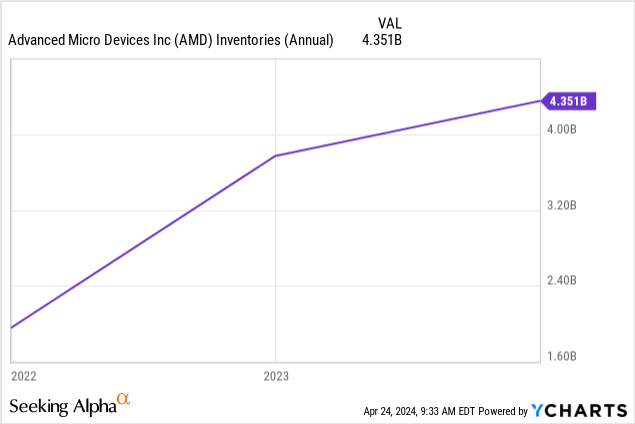

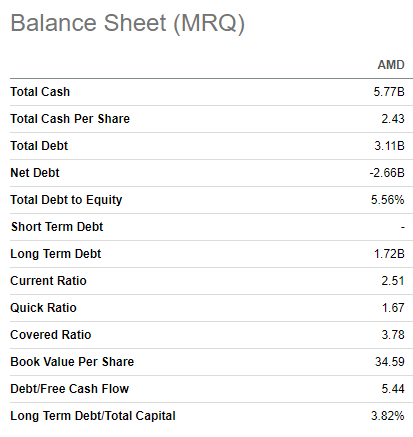

AMD's balance sheet is solid with $5.7 billion in cash and prudent leverage ratios. This positions the company well in terms of financial flexibility to invest in R&D and new investment opportunities. However, inventory levels almost tripled between 2021 and 2023 while revenue grew by 38% over the same period. Mounting inventory might pose several challenges to AMD. Apart from apparent obsolescence and impairment risks, increasing inventory levels ties up cash that could potentially be reinvested in profitable growth. Having high inventory levels for longer also may force AMD to resort to discounting, which will adversely affect profitability. This is a red flag, in my opinion.

Despite sky-high inflation, AMD's balance sheet is still robust. There was $5.77 billion in cash as of the 2023 year-end and almost no leverage. Liquidity ratios are also decent, which means that AMD has a solid potential to exercise notable financial flexibility.

Seeking Alpha

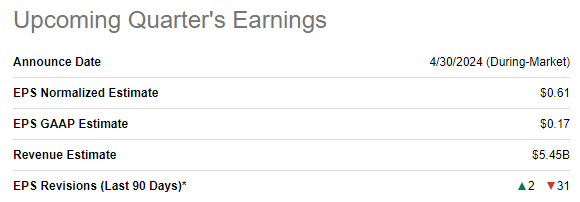

The upcoming earnings release is scheduled for April 30. Q1 revenue is expected by consensus to be $5.45 billion, signaling a 1.8% YoY growth. The adjusted EPS is expected to be about flat. An important factor underscoring weak Wall Street sentiment around AMD's upcoming earnings release is that there were 31 EPS downgrades over the last 90 days.

Seeking Alpha

A notable warning sign regarding AMD's upcoming earnings release is yesterday's quarterly earnings release by Intel (INTC). INTC plunged by more than 7% after-hours despite beating consensus estimates. The reason for investor's pessimism is the weak next quarter's guidance. Intel's management expect Q2 revenue to be between $12.5 billion and $13.5 billion, while Wall Street analysts expected $13.6 billion in Q2. Apart from disappointing revenue guidance, INTC's Q2 adjusted EPS guidance of $0.1 per share is way lower than analysts' expectation of $0.25.

Intel's earnings are likely to correlate notably with AMD's because both companies are dominating in the CPU industry and are lagging behind NVIDIA (NVDA) in GPUs. That said, even a solid rebound in global PC shipments in Q1 is not enough for INTC to have a strong guidance for Q2. This appears to be in line with what Christopher Danely from Citi forecasted before the earnings season. That said, I am very cautious about AMD's upcoming earnings release. The company might deliver above-the-consensus Q1 results, but it is unlikely to expect guidance boost considering Intel's weak guidance.

AMD's latest 10-K report

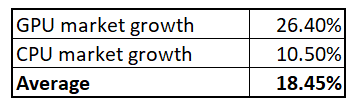

From the longer-term perspective, I think that AMD's prospects are bright. It is impossible to figure out from the company's 10-K report the share of GPU's and CPU's it sells. The company disaggregates revenue by end markets, but not by product types. Given AMD's quite diversified revenue mix, I think that a fifty-fifty mix would be fair for my estimations. It is crucial to understand shares of CPUs and GPUs in the company's revenue mix because these products have very different growth prospects for the next decade. For example, GPUs are projected to compound with a 26.4% CAGR over the long term. On the other hand, CPUs are expected to demonstrate much more modest growth with a 10.5% CAGR.

Seeking Alpha

Assuming that GPUs and CPUs are evenly split in the company's revenue mix, an 18.5% CAGR projection for AMD's revenue over the long run looks reasonable. This estimate appears to be approximately in line with the last decade's average YoY revenue growth, according to the below chart.

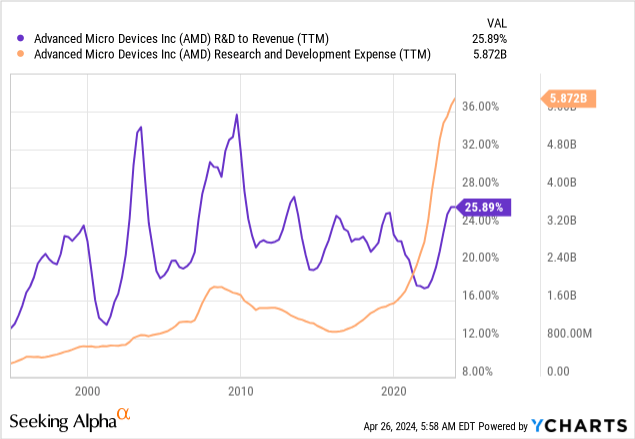

All in all, I recognize AMD's long-term potential. I believe in AMD's long-term strength because it has a solid 33% market share in x86 CPUs, which increased from 20% within just recent few years. The company significantly lags behind NVDA in terms of the GPU market share. However, according to tomshardware.com, AMD's market share in GPU expanded from 17% to 19% between Q3 and Q4 of 2023. On a YoY basis, AMD's market share dynamic was even better in Q4 with an expansion from 12% to 19%. Moreover, just ten days ago, AMD unveiled its upgraded version of RYZEN chips, which are suitable for sophisticated large language models. Lisa Su is a well-known innovator and I see this strong commitment in AMD's R&D to revenue ratio, which is also impressive in absolute terms. The company allocates around a quarter of its revenue to R&D, which is more than $5 billion in absolute terms.

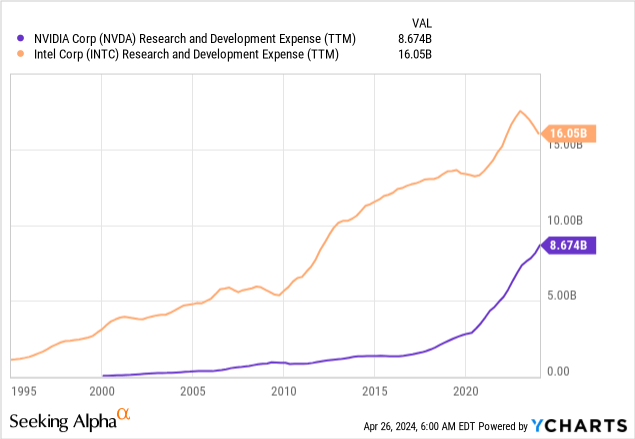

On the other hand, AMD competes with such giants as Nvidia and Intel in the GPU field. Both of these companies invest in R&D even more and NVIDIA holds an 80% market share in GPUs. Intel is lagging behind significantly in the GPU race, but is set to receive up to $8.5 billion in direct funding and $11 billion in loans for commercial semiconductor projects under the CHIPS and Science Act, according to Tech Monitor.

That said, the competition is fierce, and I do not expect AMD to become a GPU leader in foreseeable future. However, the industry is emerging to the rapid adoption of AI capabilities across the business world, and I think that AMD's commitment to innovation and solid footprint in data center business will help the company to successfully absorb industry tailwinds.

Therefore, I think that AMD has solid positioning in both CPU and GPU segments. However, I believe that near-term stock price movements will depend more on current headwinds, which we saw in Intel's weak guidance for Q2 2024. Apart from this factor, I also consider sky-high inventory levels to be a dragging down factor for the company's profitability in foreseeable future. Also, let us not forget that AMD outsources its manufacturing to Taiwan Semiconductor (TSM), a company with foundries located in Taiwan and across neighbor countries, including China. That said, AMD's operations and supply-chain are under the risk of a potential escalation of historical geopolitical tensions between China and Taiwan. However, NVDA faces the same risk.

Valuation update

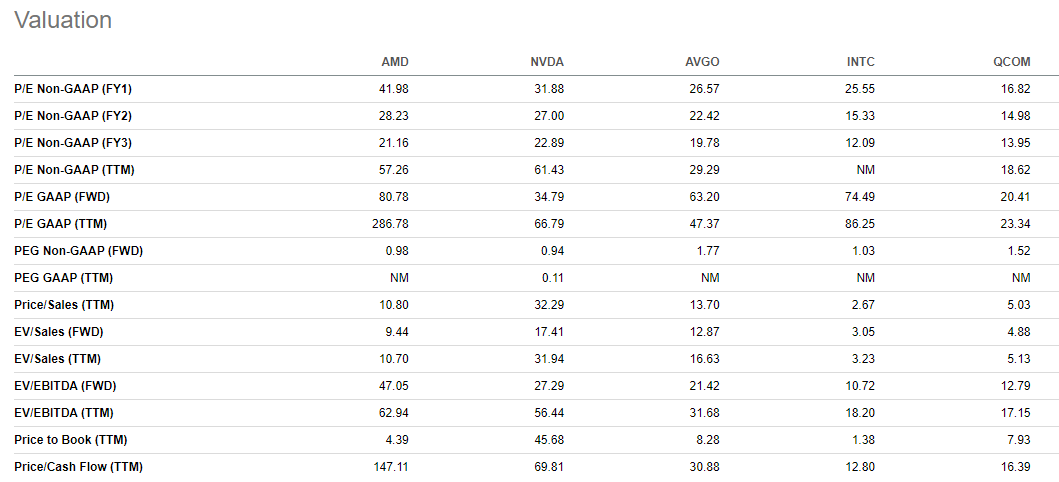

AMD delivered a solid 83% rally over the last 12 months and had a decent start in 2024 with a 4.3% YTD share price growth. AMD looks overvalued from the valuation ratios perspective because its current multiples are mostly higher than historical averages. Indeed an 81 forward P/E and 87 forward P/FCF ratios look very high. If we bring other prominent semiconductor players' valuation ratios to our discussion, AMD is the most expensive among all of them across the board. Even NVIDIA's forward valuation ratios look modest compared to AMD's.

Seeking Alpha

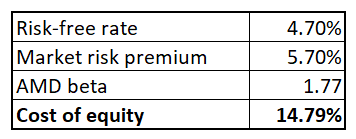

Now I want to simulate the discounted cash flow [DCF] model. While usually I refer to external sources to figure out WACC, today I want to calculate it by myself using CAPM. I ignore the cost of debt for AMD because its total debt is quite insignificant compared to the company's market cap. The current 10-year treasuries yield is at 4.7%, which is the risk-free rate for my calculations. I take the last year's 5.7% U.S. market risk premium, and Seeking Alpha suggests that AMD's 24-months beta is 1.77.

Author's calculations

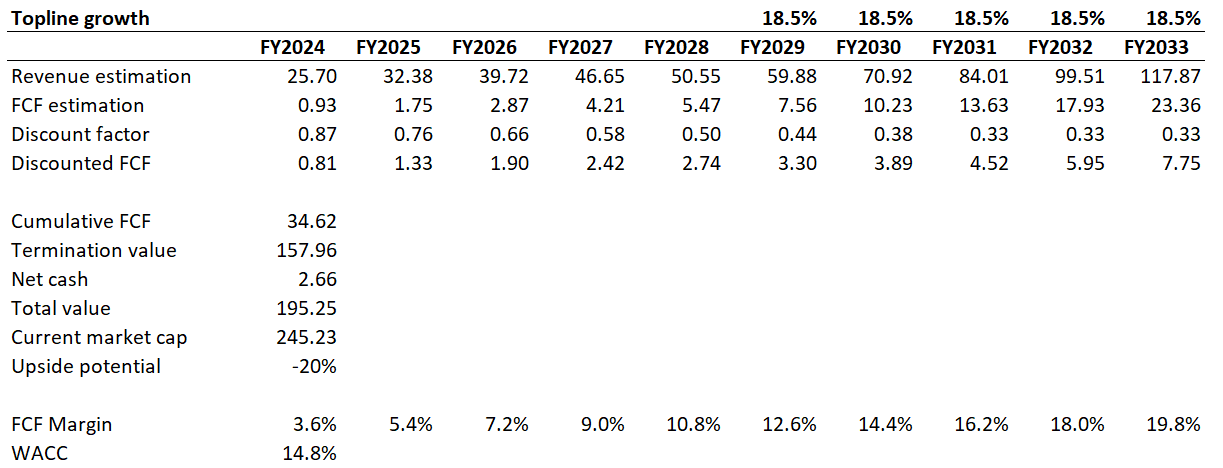

According to my CAPM calculations, AMD's cost of equity is 14.79%. I use this level for discounting of future cash flows. I have revenue consensus estimates available up to FY 2028, which I incorporate into my DCF. For the years beyond I use an 18.5% CAGR which I have figured out in "Recent developments" for AMD's long-term prospects. Considering the mix of consensus projection for 2024-2028 and my assumptions regarding years beyond 2028, the next decade's revenue CAGR is 18%. I use a TTM 3.6% FCF ex-SBC margin for the base year and forecast a 1.8 percentage point yearly expansion, which correlates with the projected revenue growth.

Author's calculations

According to my DCF valuation, the business's fair value is $195 billion. This is around 20% lower than the current market cap. While AMD has the potential to expand its revenue and profitability, I believe that a 20% premium is too generous. That said, the stock looks quite undervalued in my opinion.

Risks to my bearish thesis

The market's reaction on earnings release is difficult to predict. AMD might deliver above the consensus performance, but the market might consider even a slight downgrade in Q2 guidance as a disaster, and this might potentially lead to a sell-off. However, it also works the other way round as well. AMD might deliver relatively weak Q1 performance, but Lisa Su might announce a new jaw-dropping chip release which will be a real threat to NVDA's offerings. That said, there is a risk that earnings release can potentially be a positive catalyst for the stock price, even if financial performance will be nothing special.

AMD is one of the best-performing stocks of the past decade with a 3,600% total return. A lot of people who invested in AMD ten years ago became much wealthier thanks to this investment. Therefore, it is highly likely that the stock has an impressive base of fans who are ready to tolerate volatility and will be willing to buy any dip. This might support the stock price even further, despite the current overvaluation. Should this happen, my thesis is unlikely to age well.

Seeking Alpha

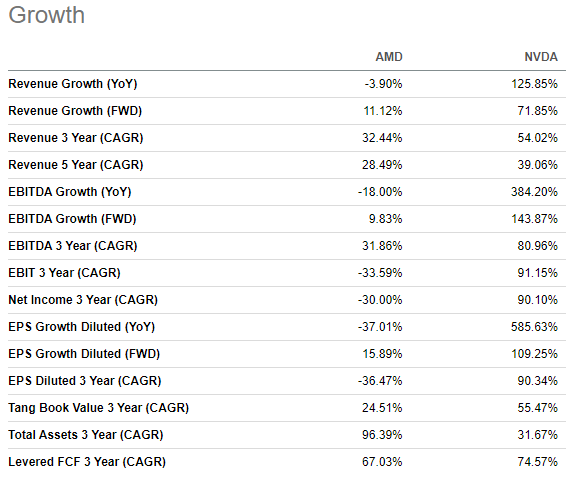

It appears that all notable semiconductor names are likely to be moving in line with NVDA. For example, AMD's revenue and profitability growth is not even close to NVIDIA's. However, AMD rallied by almost two times over the last twelve months, and I believe that the notable portion of AMD's rally related to the big rally in NVDA. That said, a new rally in NVDA might boost AMD's share price higher, even if the company's fundamentals will not improve accordingly.

Bottom line

To conclude, AMD is still a "Sell" in my opinion. The generous 20% premium to the fair value does not appear justified given the elevated inventory problem and Intel's recent weak guidance for Q2.