Yagi Studio/DigitalVision via Getty Images

Investment Thesis

Roblox (NYSE:RBLX) recently launched their own in-game ad solutions, which are based on placing interactive ads within games. Per the release, the current ad formats offered are Image Ads and Portal Ads within games.

While both of these ad formats are a great start for the company’s industry-first ad solution in gaming, I believe it is the Portal Ads that hold more value with scope for better monetization rates and engagement because brands that already have virtual worlds in Roblox games would be incentivized to spend on portal ads inviting virtual users into their virtual worlds. This tracker shows the number of brands opening virtual worlds in Roblox, which include brands such as Nike, Walmart, Chipotle, Crocs, etc.

Meta’s (NASDAQ:META) earnings call showed that better ad monetization led to higher ad revenue boosts in their Q1 earnings, which I view as a positive sign for Roblox’s ad product.

However, Roblox appears to be mostly priced in at the moment with minimal upside. In addition, the seasonal volatility gives me confidence to remain neutral on the company at the moment.

Meta’s Ad commentary is a boost to the macro overview boosting Roblox’s prospects

On Meta’s Q1 earnings call, their management noted some key perspectives that I believe are very conducive to long-term growth for Roblox.

Meta’s management noted that the company saw better monetization efficiency for its ads due to improved levels of understanding user preferences. The company expects monetization and ad placement efficiency to improve even further as they roll out improved ad formats on top of their Reels video platforms.

With Roblox’s ad solutions and their existing gaming product platform, I believe the company is already well placed to benefit from ads because Roblox’s gaming platform itself is interactive enough. The company is in a strong position to place interactive ads based on user preferences and a stronger call-to-action, which I think should lead to higher monetization for Roblox.

In addition, Meta continues to have a positive outlook on ads, which is echoed by the 13.2% ad spending growth expected in the digital space in 2024. In contrast to that, in-game ad growth is expected to be marginally higher this year, with 13.4% projected growth for 2024. This is also an emerging area for digital ads, as noted in the research, so as we move through the quarter, I expect these growth rates to improve if overall monetization gets better. This presents a robust outlook for Roblox.

Ad Revenue To Add Boost to Bookings

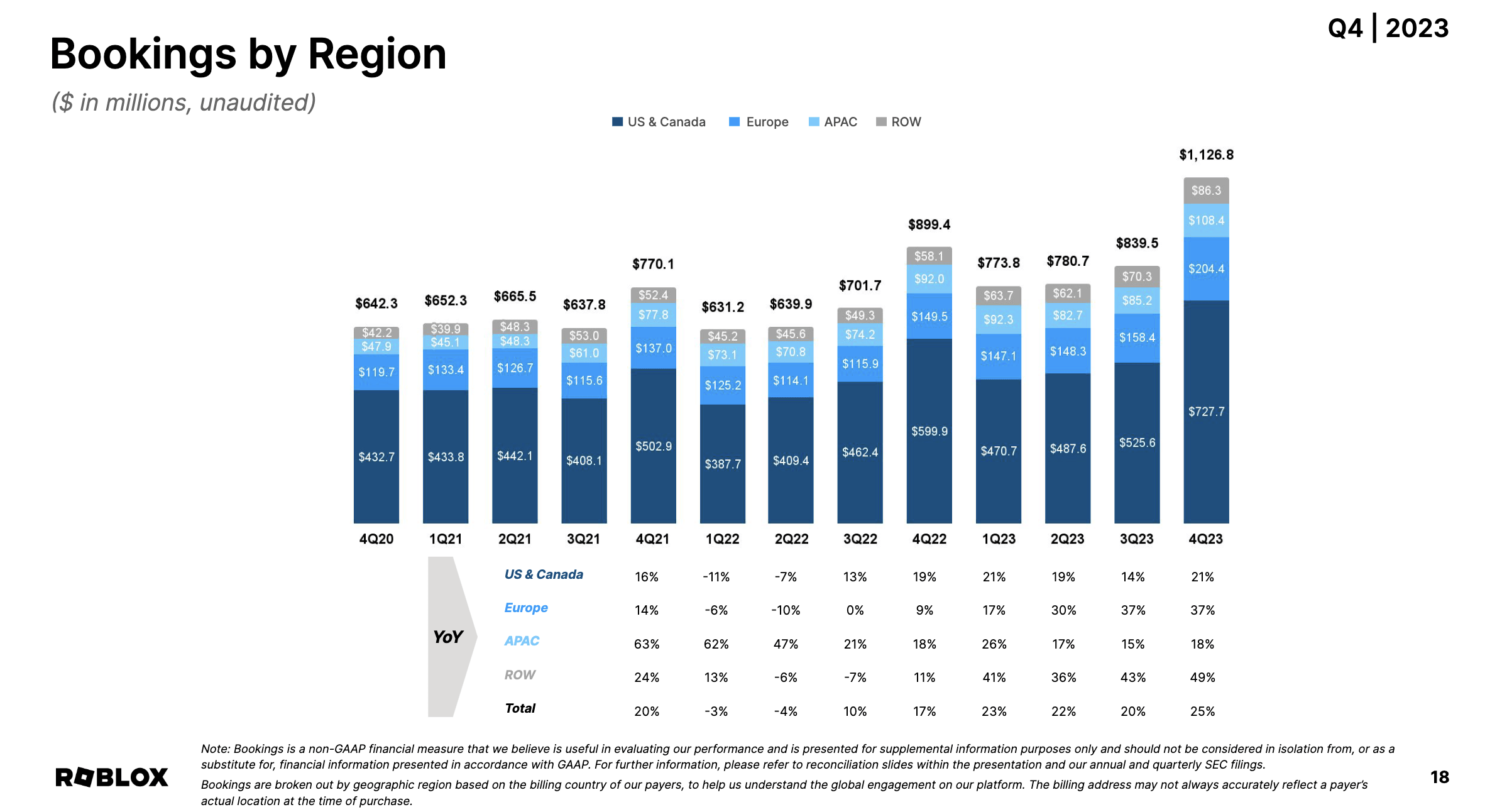

The biggest growth flywheel for Roblox so far has been its bookings metric. Today, the bulk of Roblox’s revenue comes from the sale of its Robux in-game virtual currency as well as premium subscriptions. As can be seen in the chart below, Roblox’s bookings have reported one of the strongest growth rates in the past. It also reached a new high of +$1 billion for the first time in Q4.

Roblox's Quarterly Bookings trends by region (Q4 FY24 Presentation, Roblox)

Most of the growth came from users in the U.S. region, which grew 21% y/y compared to the overall growth in bookings, which grew 25% in Q4. But I was pleased to see the momentum in its Europe region grow by 37% in the same quarter. In the Investor Day presentation last year, management revealed that countries in Western Europe were growing rapidly, led by Germany. I believe these are good signs because users in regions like the U.S. and Western Europe are higher-margin users with the capability of spending more on the platform.

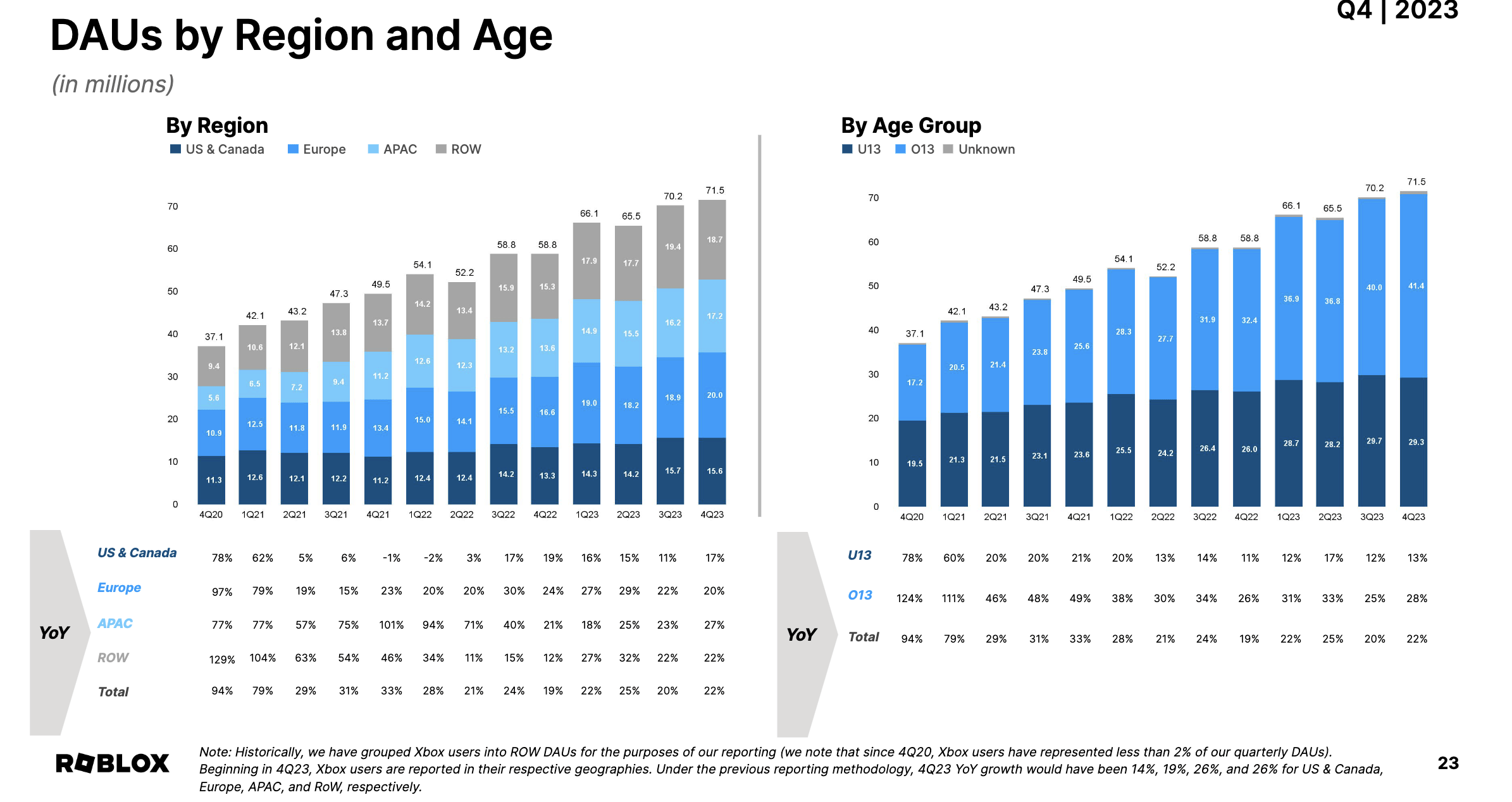

Roblox's Quarterly DAU's by Region and Age (Q4 FY24 Presentation, Roblox)

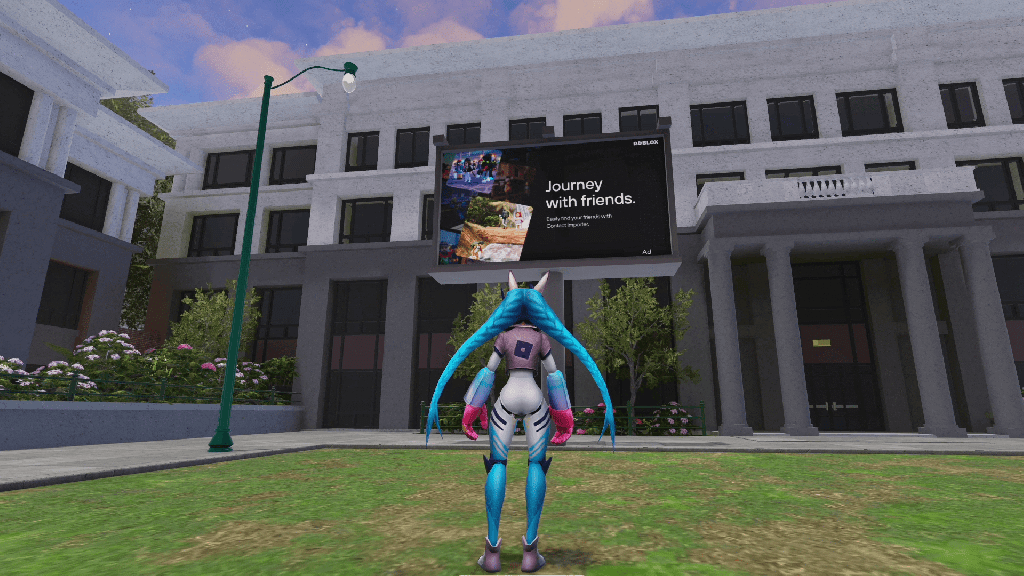

Plus, user growth continued on the platform, growing 22% in Q4, supported by stronger growth in its over-13-year-old users, who now account for almost 60% of Roblox’s user base. I believe the company continues to position itself to benefit from this healthy mix of its users, especially older users over 13 years old, as Roblox is expected to widen the launch of its ad products this year. Here is an example of how Roblox's interactive ads will work as users move through virtual spaces on the platform.

An example of how Roblox's ad would look like on the platform (Company sources)

I believe ad revenue will be an immediate way for the company to recognize more high-margin revenue upfront versus its bookings, part of which includes deferred revenue that is usually spread out over time.

Profitability is still a question mark, for now

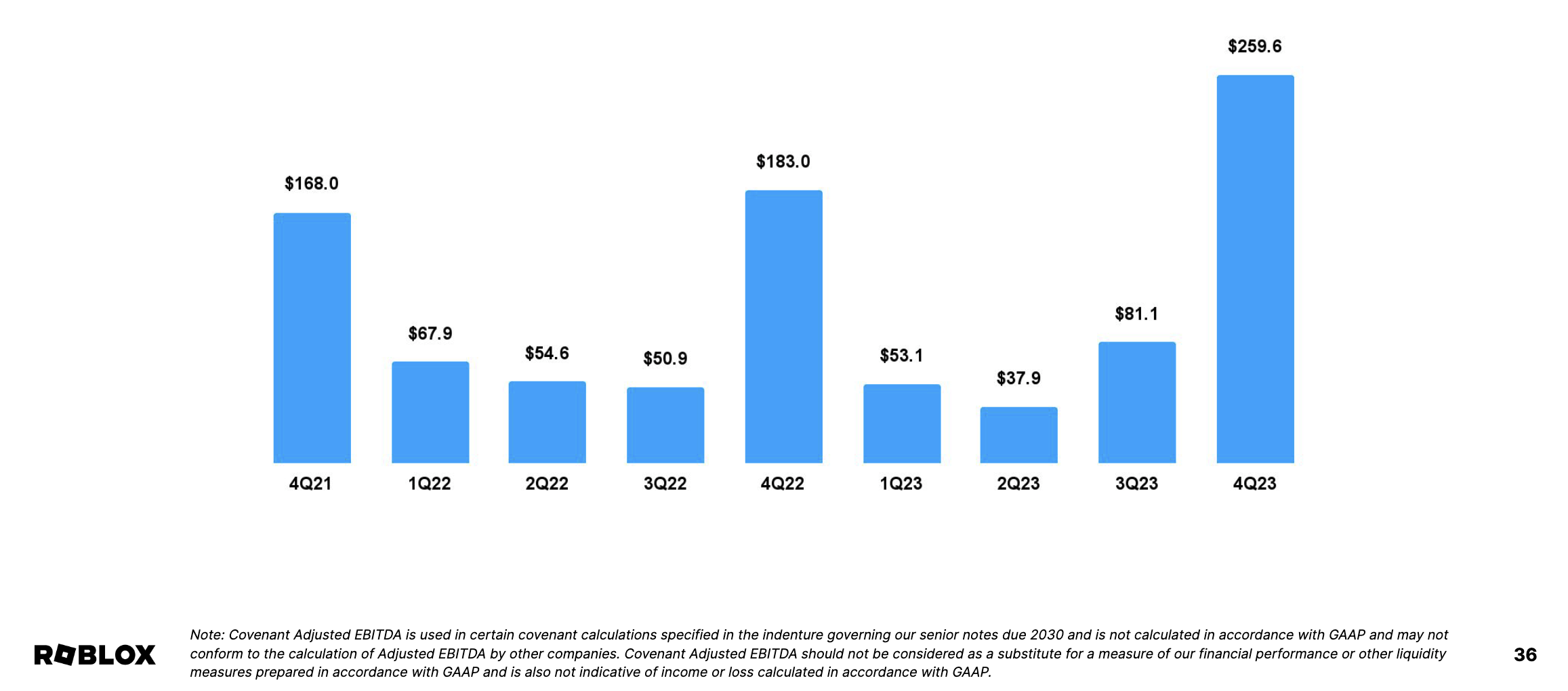

I believe I need to be very clear when I say that Roblox is a pure-play growth company. Management has mentioned some focus on being profitable, but this is on the Covenant Adjusted EBITDA profitability metric, which does show that they are profitable using this metric.

Roblox's Covenant-adjusted EBITDA - includes deferred revenue (Q4 FY24 Presentation, Roblox)

When perusing through slide 37 of their Q4 results’ supplemental materials, I noticed that the company adds back its deferred revenue to its adjusted EBITDA numbers, which eventually shows Roblox’s positive profitable metric. I understand management’s rationale for using Covenant Adjusted EBITDA, but with deferred revenue being spread out over many months, it does not make sense at the moment to assume this metric in my calculations for its target price. The company has revised the tenure under which it spreads out its deferred revenue, essentially the sale of its Robux tokens, to 28 months, up from 25 months in Q3 FY22 and 23 months in Q1 FY22.

For my valuation purposes, I don’t believe this is the right metric, so I have used their forward sales to estimate my target price in the next section.

On a purely adjusted basis, Roblox continues to expect EBITDA losses of between $115 million and $150 million for FY24. This is quite a wide guidance range for adjusted EBITDA losses, in my opinion. Still, after eyeballing the guidance, I suspect management expects its profitability to improve in the better half of the year since approximately a fourth of its adjusted EBITDA losses are expected in Q1 alone.

In addition, the company still carries ~$1 billion worth of debt on its balance sheets, mostly in the form of senior notes due in 2030. Debt issuance costs for Roblox’s 2030 notes currently stand at 3.875%. According to the company’s 10-K, this leads to yearly contractual obligations of ~$39 million in the form of principal and interest cash payments until it carries the debt. Hence, in my opinion, it would be in the best interest for the company to quickly generate meaningful, profitable streams of revenue. In-game ads would be one way to do that, but these are early days.

Roblox is a Hold

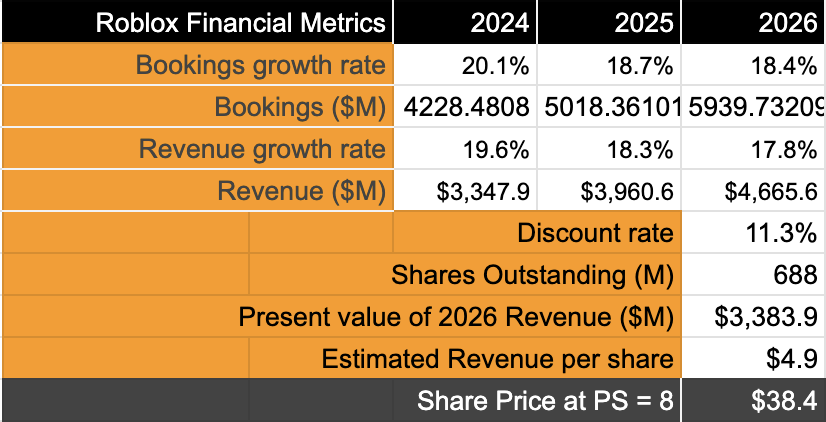

As stated earlier, I will be using forward sales to arrive at the correct target price. Here are my assumptions:

The primary top-line metric I have used to forecast Roblox’s growth is bookings. This is because Bookings contain revenue and deferred revenue that, at the moment, is spread across 28 months. Per Roblox’s 10-K, they recognized their FY22 deferred revenue in their FY23 books last year. This is also in line with consensus estimates that are higher than the company’s own projections, given the strong ad landscape that I noted earlier.

I have not added potential gains from ad revenue yet. I expect to see quantitative results published by management for me to include this in my forecasts moving forward. I believe management should be detailing their ad product performance in the next few quarters.

Discount rate of >11% due to a higher debt load implies some level of risk. Calculations can be seen here.

- Assumed shares are diluted by a range of 3-4% per year based on commentary made during Investor Day and previous earnings calls.

Roblox's valuation model shows minimal upside (Author)

This shows that Roblox is estimated to grow in the high teens, between 18 and 19%. Given these projected growth rates, Roblox should warrant a forward sales valuation multiple of 8, which implies an upside of ~8% from current levels.

Considering some of the risks, lack of inherent profits, and seasonal volatility during this time of the year, I am not confident enough to buy this stock here, thus leaving a Hold rating.

I also wanted to mention a few risks to the outlook here. Multiple projections from research firms and corporate commentary suggest the ad outlook remains strong for the year. Meta’s strong ad performance is another example I had highlighted earlier.

However, were these conditions to deteriorate, it would impact the company’s growth rates severely. Geopolitical tensions, economic slowdowns, and higher-than-expected interest rate environments are potential headwinds.

Note: Roblox is expected to report their Q1 FY24 earnings on May 9th, next month. At the very least, I expect management to provide some anecdotal evidence about their view on Roblox's ad product's launch. Any revenue contributions from them will be further appreciated if they are in a position to explain how much incremental revenue came from ads.

Takeaways

Roblox has all the signs for a great year ahead. The momentum in its bookings should continue as demand for its virtual games and Robux coins continues to propel the company ahead. I expect the new additions to its in-game ad solutions to further boost its growth over the next few years and reduce its dependency on bookings.

But, with the stock’s current valuation baking into most of my growth expectations, I will recommend a neutral view on Roblox at the moment.