Monty Rakusen/DigitalVision via Getty Images

Summary

Automation, Robotics, and Artificial Intelligence have converged into a Gigatrend. The race to develop generative AI will or is being implemented in automation and robotics not only as a source of productivity on factory floors or new consumer gadgets but also in defense and ultimately to replace a shrinking workforce as the global population declines in the developed and many emerging economies. The majority of companies developing AI are large, well-known, and funded such as Microsoft (MSFT) in partnership with Open AI, and Nvidia (NVDA) which provides computing power. However, robotics and/or automated robotics that may perform multiple tasks and even improve processes and productivity are still being developed. In September 2023 I reviewed the Global X Robotics & Artificial Intelligence ETF (NASDAQ:BOTZ) and rated it a BUY. I now update this analysis with fresh consensus data to arrive at a new YE24 upside potential of 17%. However, valuations have moved from reasonable in 2024 to 2025 which warrants a downgrade to Hold.

Performance

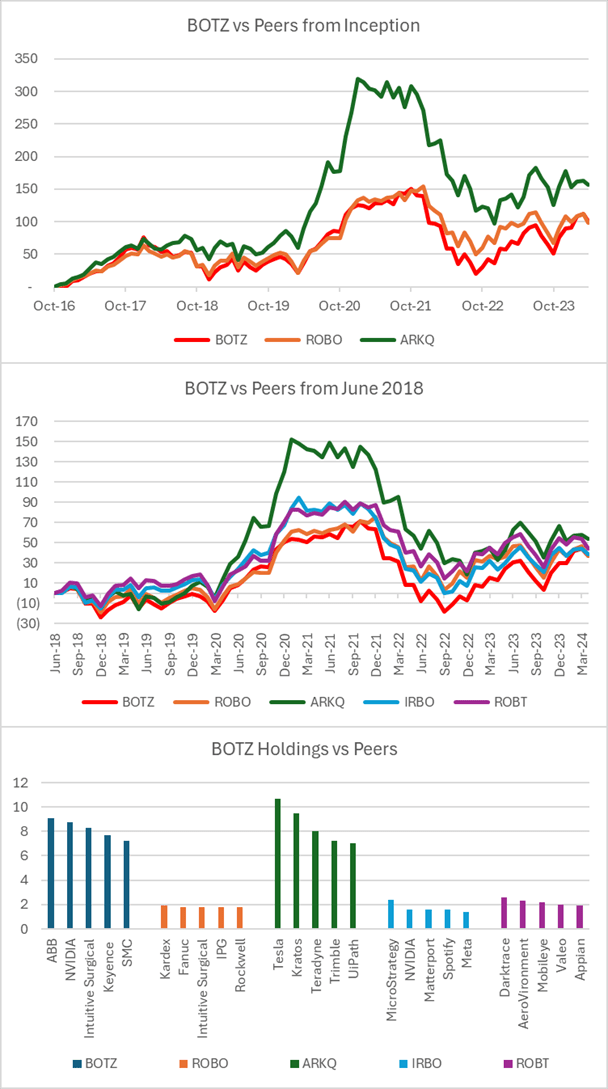

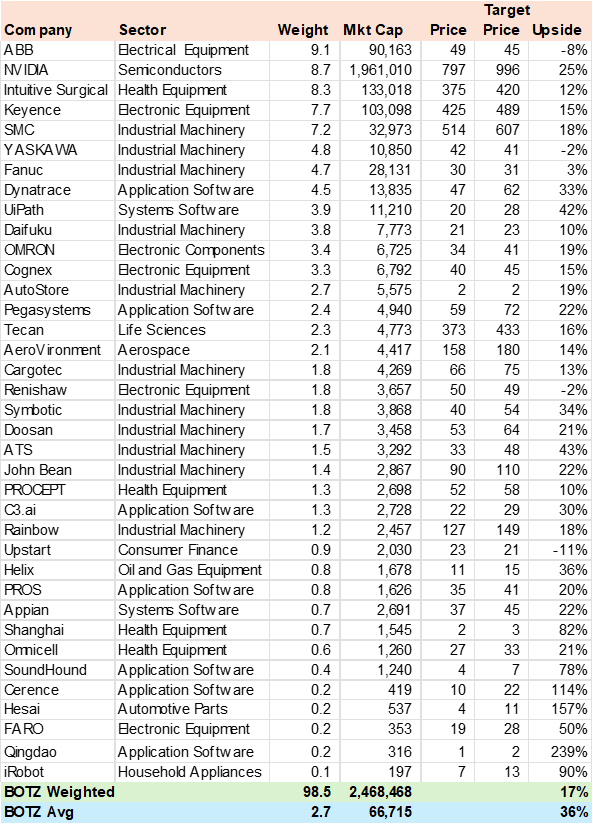

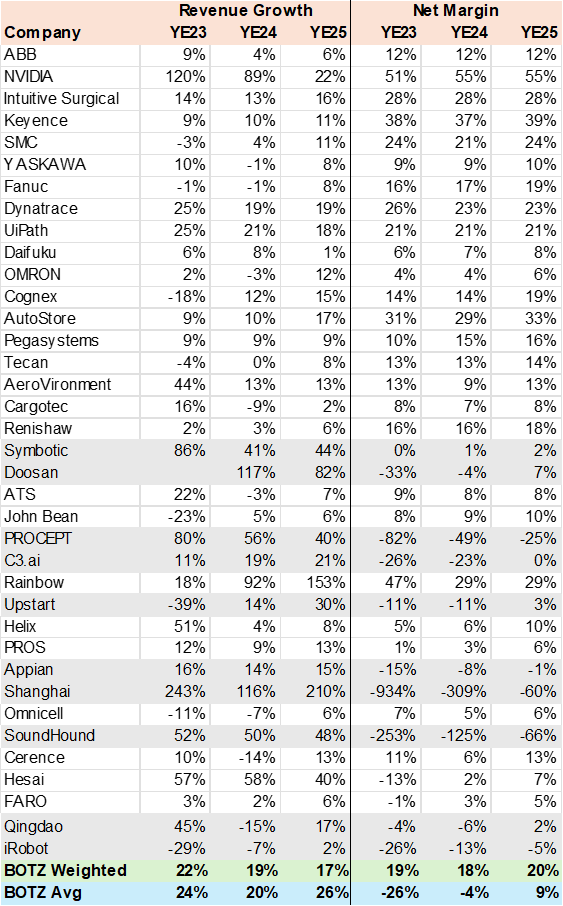

From my last update, the ETF gained 22%, beating all the peers by a wide margin, which is due to a large stake in NVDA. The peer group has very different holdings and strategies with active ARK Autonomous Technology & Robotics ETF (ARKQ) the worst-performing due to its 10% stake in Tesla (TSLA). However, from inception, BOTZ has performed at the bottom of the peer group which may be due to its more industrial sector focus. Below are several charts that highlight this performance and the difference in the top 5 holdings for each ETF. The other ETFs have near equal weightings and focus on somewhat more developing companies, which strategy is ultimately better remains to be seen.

Created by author with data from Capital IQ

Portfolio Upside Potential of 17%

The ETF is primarily focused on the industrial side of robotics, the companies that make robots or the equipment and components, while a smaller portion is in software that runs autonomous robots that in the future will learn i.e. artificial intelligence.

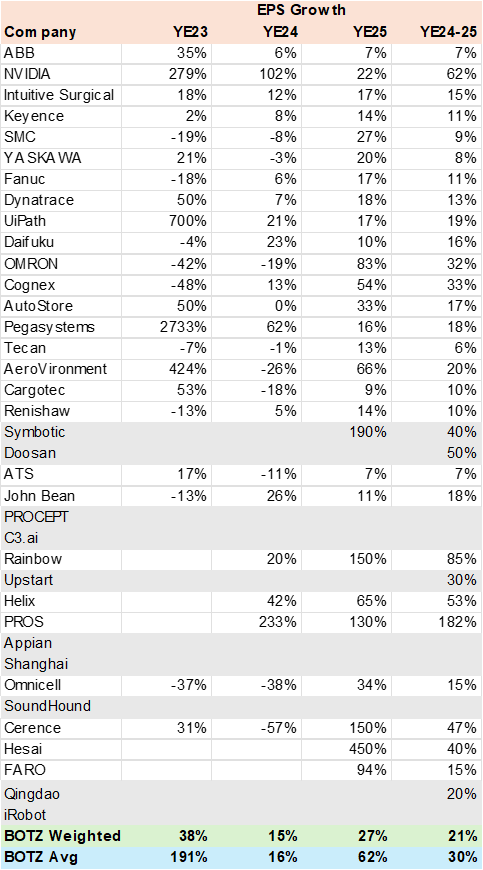

I gathered consensus data for 98% of the AUM and calculated a potential upside of 17% to YE24 based on analyst price targets. The ETF appears to be somewhat handicapped by downside risk in the largest weight ABB Ltd (OTCPK:ABBNY) which has been up nearly 40% in the last 12 months. As can be expected the small caps have the greatest potential albeit without any positive earnings. Much of the holdings are foreign stock that many investors may have difficulty accessing given the poor liquidity in the pink sheet market.

Consensus Price Target (Created by author with data from Capital IQ)

Revenue Growth and Net Margins

Using consensus data, I arrived at an estimated 19% revenue growth rate in 2024 that decelerates to 17% in 2025 due to more normalized growth at NVDA while ABB and several of the top holdings are more mature companies with under 15% revenue growth and steady margins. This provides the ETF portfolio with a solid core and less overall risk in my view. About 9% (in grey) of the portfolio holds smaller developing companies, many without earnings in the forecast period. This provides the ETF with a boost to its risk/reward profile.

Consensus Revenue Growth (Created by author with data from Capital IQ)

EPS Growth

The ETF's portfolio has a consensus EPS growth rate of 15% and 27% for YE24 & YE25 respectively, down from over 38% in 2023 as NVDA slows its exceptional growth. Nonetheless, the ETF has a normalized 21% EPS growth rate in the YE24-25 period that I later used to calculate valuation metrics. As can be seen, there are some very high growth rates in the small-cap companies and others have no earnings in the forecast period. I adjusted the weighted EPS growth for these very high numbers that are not representative of normalized run rates and may distort valuations.

Consensus EPS Growth (Created by author with data from Capital IQ)

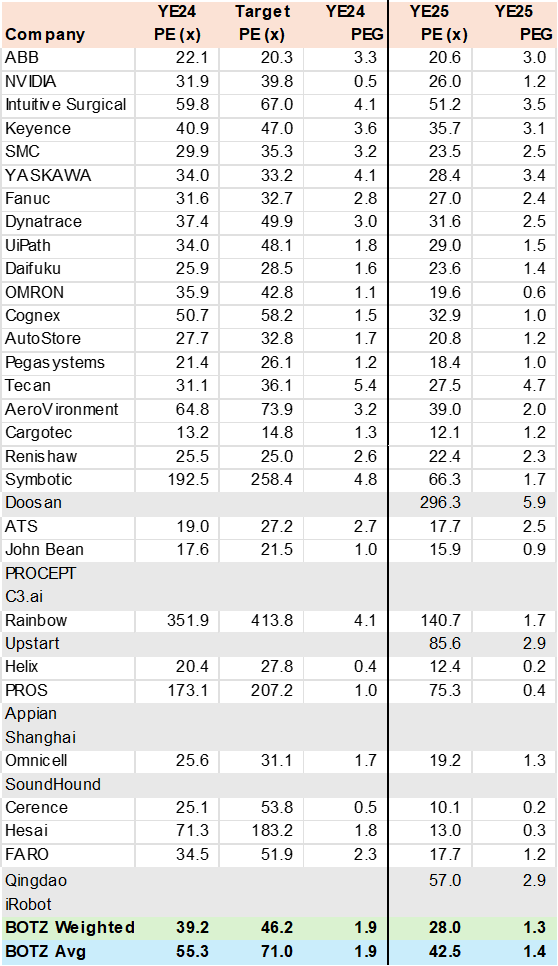

Valuation: Not Outrages

At first view, the market valuation seems unreasonable for many stocks from large to small such as a PE target of 67x for Intuitive Surgical (ISRG) or 50x PE for Dynatrace (DT) while many small caps that barely have earnings have PE targets over 200x, which are not the analyst's intention and most likely their valuations are based on a revenue multiple or some other metric that captures the companies potential long term. However, stripping out the distortions I arrive at a PE of 39x for ETF on YE24 results, which on a relative PEG (PE to EPS growth) valuation metric is not outrageous at 1.9x but clearly at a premium to the SP500 (SPX) or NASDAQ (NDX). On 2025 estimates the PEG declines to 1.3x which is reasonable for the more patient investors.

Consensus Valuation (Created by author with data from Capital IQ)

Conclusion

I rate BOTZ a Hold. The ETF has a balanced portfolio of large-cap growth and small-cap developing companies that should meet or exceed consensus forecast in this dynamic and high-growth sector. However, the valuation has been stretched and investors should be patient as results need to catch up to prices in my view.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.