Robert Way

My Overall Investment Thesis

NIKE, Inc. (NYSE:NKE) has underperformed the market, indicated by the ETF SPDR® S&P 500 ETF Trust (SPY), over the last five years and is currently down almost 25% over the last year. Given their brand value and outlined areas of future growth and investments discussed in their recent earnings call, NKE may be considered a value investment today by some investors. However, the historical fundamentals still point to an overvalued company that should continue to underperform. Based on the fundamentals, I'm giving NKE a sell rating, meaning that I would not buy it at this price. With the recent positive news on the company, and upcoming professional sports events where they are displaying products, we may see a short-term uptick in share price, ultimately brought back down by the poor business fundamentals. I would wait for further price decline before investing in this company.

Company Outlook

NIKE, Inc. is a sports apparel and footwear brand, primarily known for their athletic footwear brands. The company has a robust and growing library of footwear brands such as converse but also has licensing agreements with professional and college sports teams for their athletic apparel. Additionally, with the upcoming 2024 Olympics held in Paris this summer, NIKE Inc. has exclusive agreements to provide athletic apparel to the athletes, and this will include the showcase of innovations in their "Air" line of products.

Over the last few quarters, NIKE, Inc. has continued investing in their business by focusing on product development in key areas such as their retro line of products and women's apparel and footwear. Moreover, NIKE, Inc. continues looking for athletes to serve as product ambassadors that can help support their line of products in new categories. Recently, they have developed products for women in a higher price category than before, such as their Go, Zenvy, and Universa lines of leggings which all exceed the $100 mark. Additionally, through brand ambassadors, NIKE, Inc. is currently in contract discussion with Caitlin Clark who is an American women's basketball player that was recently drafted first overall in the WNBA draft. As the all-time leading scorer in college women's division one basketball, she would be able to provide NKE with a large following for the products they develop together, such as the signature shoe, because of her massive popularity among fans.

Fundamental Analysis

Some quick fundamentals on NKE, they are currently trading at a trailing twelve month non-GAAP price to earnings ratio (P/E) of 26, trading at a forward non-GAAP P/E ratio of 25, and a forward EV/EBITDA ratio of 19.7. Additionally, they are trading over 2 times their trailing and forward price/sales ratio, and 10 times their price to book ratio. NKE has consistently grown their revenue since 2008, but their costs of good have increased significantly while their gross margins are declining overall. As you can see in the chart below with the linear projection model based on their historical data, gross margins should continue to decline even as revenue increases due to rising costs. Costs for the company will continue to increase as they need to pay more for product exposure with new athlete deals and major sporting event product placement. Additionally, product costs were attributed to declining margins back in the September 2023 earnings call. I believe these factors begin to highlight some of the overvaluation of the company, even though these factors are lower than their historic 5-year average. To continue to evaluate this company, I will look at their return on invested capital next.

NKE revenue and cost of goods (in the millions), with gross margins since 2008. Additionally, linear projections for revenue and gross margins over the next two years. (GuruFocus)

Return on Investments

NKE has struggled to provide stock appreciation for investors over the last year with over a 25% decline, and has struggled over the last 5 years with only returning just over 8% in stock appreciation. Since 2008, NKE has provided a large return on invested capital (ROIC) and a large return on capital employed (ROCE), however weighted cost of capital has increased in recent years while both ROIC and ROCE have declined. This was highlighted in their recent 3rd quarter earnings call as they had mentioned multiple areas of their company growing in the low single digits and high single digits on year-over-year basis, but they have invested significantly in product development. Moreover, as you can see in the chart below with the linear projections for the next two years, I believe ROIC and ROCE will continue to decline based on the data I've pulled together. As the company continues investing in product development, spending for restructuring to fuel future growth, and high spending on brand ambassadors, the high investments with single digit growth displayed in key areas of the company will lead to further decline in ROIC and ROCE. This should continue to lead to an overvalued stock that may continue declining over the next few years if they cannot improve investment decisions.

NKE: return on invested capital, weighted cost of capital, and return on capital employed since 2008 with 2 year linear projections. (GuruFocus)

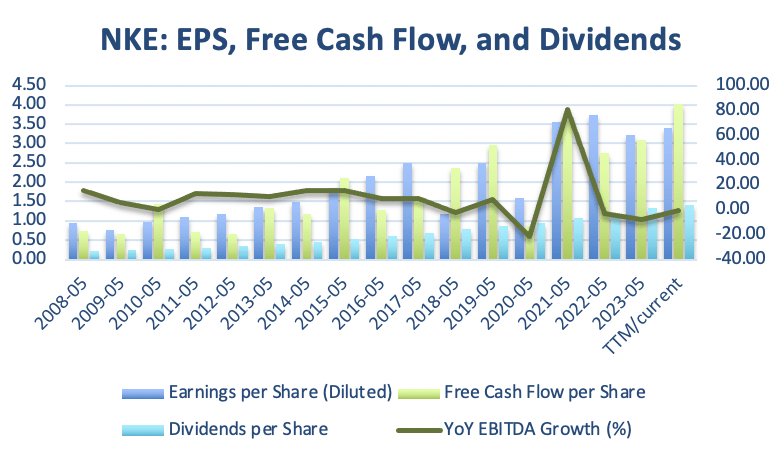

Free Cash Flow and Dividends

Free cash flow is an important area for company valuation. If the company is consistently growing free cash flow per share, it usually indicates a good company. NKE has grown their free cash flow and earnings per share significantly since 2008. Additionally, they have also consistently grown their dividend over this time, currently providing about a 1.57% forward yield. With the current payout ratio of just over 39%, NKE still has room to grow their dividend as they have in the past. However, NKE has had inconsistent EBITDA growth that is currently negative over the last twelve months. The company so far has been able to maintain their margins of around 40%, however, if year over year earnings growth does not improve, I would expect other areas of the company to be affected.

NKE earnings per share, free cash flow, and dividends since 2008. (GuruFocus)

Fair Value

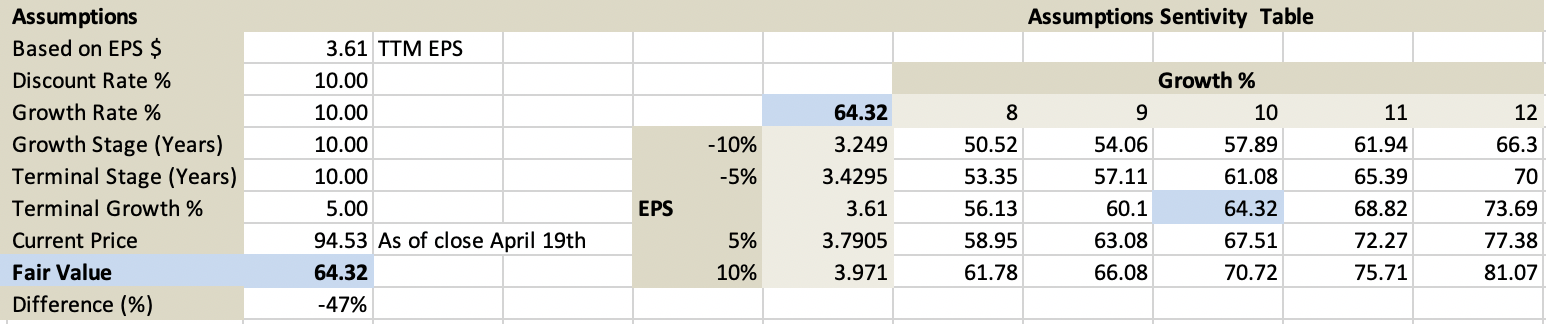

Using a conservative discounted cash flow model based on current earnings per share data and historical growth rates, I believe NKE is currently overvalued and at risk for further decline. Assuming a 10% discount rate, 10% earnings growth rate which is higher than the previous 10-year earnings growth, and assuming 5% terminal growth, NKE is currently trading at a significantly overextended valuation. Please see the chart below for additional assumptions and the outcome based on an earnings per share DCF model. I used earnings instead of free cash flow because NKE's earnings growth over the last 10 years is slightly lower than their free cash flow, and NKE had massive free cash flow generation over the last year, which may have caused an inflated and unsustainable valuation. Essentially, I used EPS data for a more conservative price target.

NKE discounted cash flow model based on trailing twelve month earnings per share fair valuation. (Author's Own Calculations)

Risks To Investment Thesis

NIKE, Inc. has an extraordinary library of products and brand value that helps create deals with professional athletes who covet development of their own signature shoe. This, along with the popularity of these athletes, drives growth for NIKE, Inc. who displays a moat in athletic apparel and footwear in most sports. Given this enormous brand value of NIKE, Inc., it is hard to justify a conservative approach for this company based solely on fundamentals because of the expected valuation of the brand itself; this intangible asset is hard to price. If NIKE, Inc. is able to sign deals with popular athletes like Caitlin Clark, this would drive growth in key areas of company development such as women's apparel and footwear that has otherwise been a slow grower with single digit growth over the last three years. Deals like this, and well-received display of their products, such as with the 2024 Olympics, would likely drive the share price of the company up over the short term. Moreover, there was some recovery in gross margins mentioned in the most recent earnings call, and if margins remain as high as ~44%, NKE should be able to offset increasing costs, which also poses a risk to my sell thesis.

Conclusion

Based on my fundamental analysis above and fair valuation, I believe that NKE is still overvalued, even after the 25% stock price decline the company has already seen over the last twelve months. I anticipate that over the short term, positive news around the company will support positive momentum in the stock; however, this should eventually decline again based on the poor fundamentals. I'm rating this company as a sell, meaning that I would not buy it today, at this price. If the stock decided to decline further and see an improvement in the trend of some core fundamentals like ROIC and ROCE after the events over the next few months/quarters, it would warrant re-evaluation at that point to see if it meets criteria as a good investment (being at or under fair value). As revenue for the company has only grown at an average of ~8% over the last decade, and the company is currently trading at 25 times forward P/E, there are better places for your investment capital that at least have double-digit growth. This article is solely based on my research and my own calculations for fair value.