z1b

Co-authored by Treading Softly

I've always loved the idea of being more environmentally friendly. I have raised animals, grown gardens, and tried to live sustainably on my property, developing it into more of a homestead than a beautiful green lawn. I understand that nature is a balance between many different forces, so I've enjoyed the concept of trying to support that balance instead of just running it over with whatever I might want to stick in my yard at that time.

When it comes to the market, the green I like best is green cash flow. For years, I avoided "green" investments, primarily because they were significantly overpriced relative to the profits they were capable of producing. Many investors seemed to be buying "green" stocks more for that feel-good feeling than making money. In recent years, that has changed.

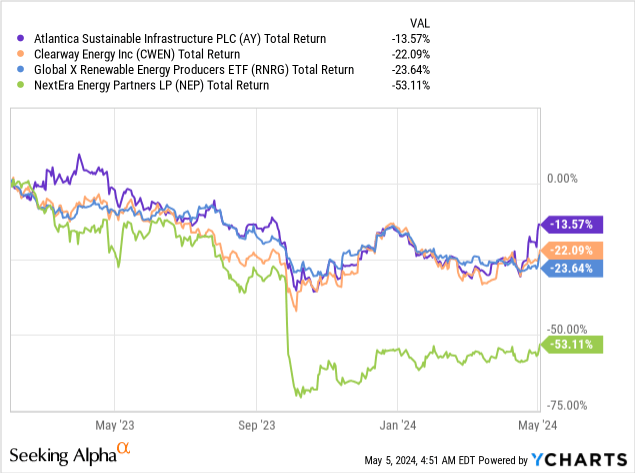

The market has not been kind to most renewable investments. We've seen that many of them have low returns on their investment. With rising interest rates, yieldcos and other renewable energy-focused companies have seen shrinking margins and were squeezed even harder on their return on equity. We have covered renewable investments several times because we enjoy the large yield from them. Others sold out of them in frustration or disgruntlement over how those companies were performing. We bought the dip, and we encouraged others to do so because of the sustainable yield and the expectation of distribution growth.

Today, I want to provide an update on the most recent quarterly results from one of these companies and discuss our investment thesis. The yield is fantastic, the distribution growth is much appreciated, and the renewable investments that they've made aren't going away anytime soon. The market has gone from dramatically overvaluing it to blowing right past fair value. What was once an expensive option is now in the deep-value territory.

Let's dive in!

Bought The Dip, Receiving the Rewards

NextEra Energy Partners (NYSE:NEP), yielding 11.5%, saw its share price tank when management revised guidance. The revision was significant – NEP was guiding for 12-15% growth, and that was slashed to 5-8% with a near-term expectation of 6% growth. It is understandable for investors who expected double-digit growth to be disappointed with single-digit growth.

However, as the market is prone to do, it started with a very reasonable response and went overboard. A company growing at 6% should obviously have a lower valuation than a company growing at 12%. But if I told you I have an investment paying a 12% yield that will have 6% distribution growth over the next three years - are you interested? Of course, you are!

If NEP were a brand-new company that just launched with a 6% growth forecast in the near term and 5-8% growth as the expectation for longer-term growth, it wouldn't be starting with a 12% yield. Perhaps this is because investors feel burned or misled.

Many have criticized management for not reducing guidance earlier. Maybe they could have, but would investors have been any happier about guidance being reduced in March 2023 as they were in September 2023? I doubt it. There simply is no good place or time for management to say, "Hey, remember that 12-15% growth target we've been hitting consistently for the past 10 years? That's over." That is something that is simply never going to be well received. No matter when management broke the news, a large number of investors would have hated them for it.

It is clear that many in the market do not trust NEP's management. They don't believe that NEP can maintain the 5-8% growth rate management is now targeting.

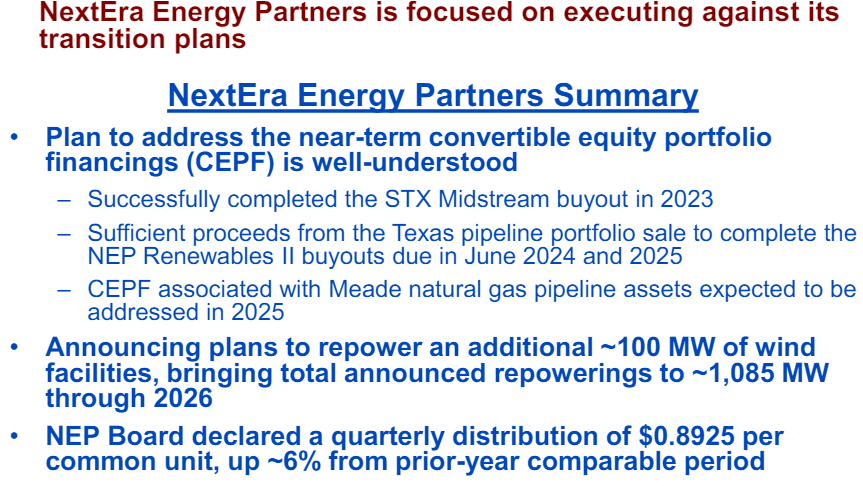

The main focus for NEP today is to pay off its CEPFs (convertible equity portfolio financings). These are obligations that could be paid off with equity if equity prices were higher. However, at current equity prices, that isn't a viable option. NEP raised the capital to pay off CEPFs through the sale of its pipelines. Last year, NEP closed on the sale of its Texas pipeline, which provided enough proceeds to pay off the CEPF maturities in 2024 and 2025. Source

NEP Q1 2024 Presentation

Since issuing equity is not viable, NEP is pursuing growth primarily through "repowerings" - this means upgrading the infrastructure of older wind farms with newer technology that is more efficient. As a result, NEP will be able to produce more power with existing assets. Ultimately, NEP makes money by producing electricity and selling it. Florida Power & Light is NEP's largest customer and is owned by parent NextEra Energy (NEE). If NEP produces more electricity, it makes more money.

The advantage for NEP is that repowering is a lot cheaper than building new windfarms. NEP's plan is that it will not need to issue equity for growth until 2027 at the earliest. This is to provide a runway to manage the CEPF maturities and prove to the market that it can grow at a 5-8% pace. That also buys time for interest rates to come back down, the price of shares to rise, or the price of electricity to rise, to a point where it is profitable for NEP to issue equity.

For Q1, Adjusted EBITDA and CAFD (Cash available for distribution) were up 3.3% and 5.1% respectively year-over-year.

NEP Q1 2024 Presentation

NEP is on track with what management has outlined. Today, we have another distribution hike to $0.8925. We look forward to more distribution hikes as the year goes on. With an 11.5% yield, we don't really need any distribution growth to justify owning it, but we certainly aren't going to turn it down!

Conclusion

Today, we reviewed the Q1 earning release from NEP, one of many potential renewable investments that an investor can make with their portfolio. I like NEP because the market has overreacted to its growth guidance revision. While it was a massive change to digest, the company is continuing to operate as expected and the distribution increases are just smaller than originally guided. Investors are not one to be quick to forgive, nor are they quick to forget. I don't expect that the share price will rise rapidly because of these continued increases, but I do expect that as they continue to perform as expected, the share price will recover over time. In the meantime, I am paid to wait, collecting the strong dividend dollars that are pouring into my account, and enjoying them.

When it comes to retirement, the last thing you want to do is be stressed about every share price change. You have the opportunity to be patient and to be greedy when others are fearful. With renewable investments, there's going to be a lot of turbulence in the water at times. They are affected by interest rates, political winds, or even societal thought, and while all of these facts are true, the well-managed and top-performing companies can also provide you with a strong income. This way, you're able to not only support a greener future, but you're also able to enjoy a wonderful retirement

That's the beauty of my Income Method. That's the beauty of income investing.

If you want full access to our Model Portfolio and our current Top Picks, join us at High Dividend Opportunities for a 2-week free trial.

We are the largest income investor and retiree community on Seeking Alpha with +8000 members actively working together to make amazing retirements happen. With over 45 picks and a +9% overall yield, you can supercharge your retirement portfolio right away.

We are offering a limited-time sale for 17% off your first year. Get started!

Start Your 2-Week Free Trial Today!