Richard Drury

Overview

I previously assigned Golub Capital (NASDAQ:GBDC) two separate buy ratings: the first one in November of 2023 and the most recent being in February of 2024. My last coverage leaned heavily on the idea more investors would flock to higher yielding assets such as BDCs to offset a higher interest rate environment. At the time, the Fed seemed to be dragging their feet on implementing interest rate cuts. Now it seems that rate cuts aren't expected this quarter and will likely continue to get pushed back as inflation remains high, and the labor market is strong.

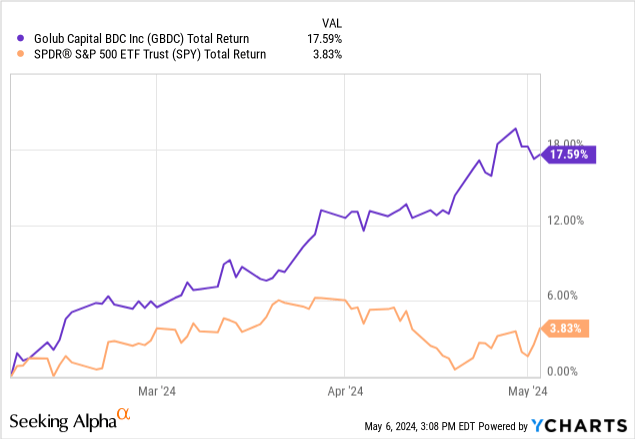

Well, my thoughts played out as expected and now the price of GBDC has run up even more. GBDC delivered superior growth since then by growing NII (net investment income), improving financials and liquidity, and growing their portfolio by making new investments. Since my last coverage, GBDC has outperformed the S&P 500 (SPY) in total return by a large margin. Unfortunately, this recent price run makes GBDC less attractive than previously, and now the price sits at a much higher premium to NAV than its averaged in the past.

Golub Capital operates as a business development company that focuses on senior and junior debt as well as equity investments for companies looking for capital. GBDC's focus is primarily within middle market companies that are screened and rated internally to gauge quality. GBDC invests anywhere between $10M - $80M of capital into these middle market companies. Golub Capital is also externally managed by GC Advisors.

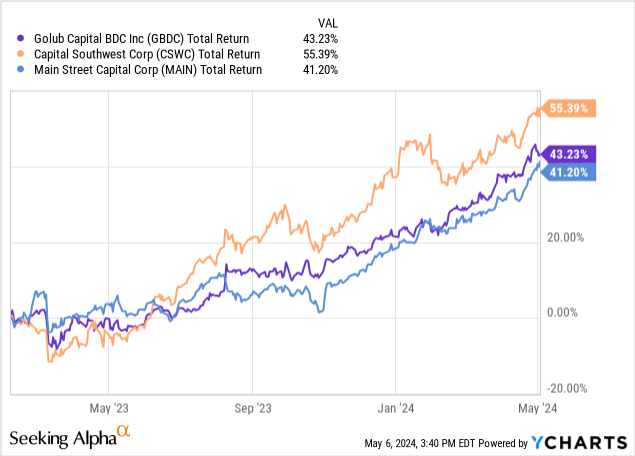

I admittedly missed out on lots of gains here because I was busy piling cash into peer BDCs that are internally managed, such as Main Street Capital (MAIN) and Capital Southwest (CSWC). Internally managed BDCs typically pass along more of the net investment income growth to shareholders in the form of dividend raises or supplementals.

To my surprise, though, GBDC has provided several supplemental dividends and continues to deliver excellent returns that are on par with these internally managed peers. GBDC's current dividend yield sits at 9.2% following the price run. For reference, at the time of my last coverage, the dividend yield was over 10%. I point this out because the recent price run no longer makes GBDC as attractive in my opinion, as it current trades at a premium to NAV that is higher than it's ever been over the last four years.

Q2 Earnings - Updated Financials

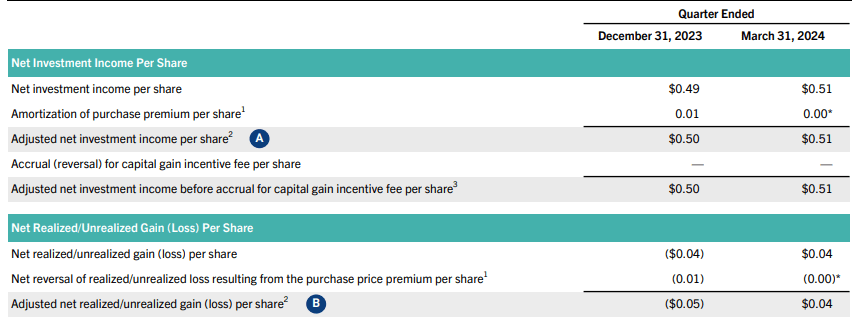

GBDC reported their Q2 earnings on May 6th and the results showed consistent growth. NII came in at $0.51 per share, representing a 21% increase over the $0.42 per share that was reported in Q2 of 2023. We can see that GBDC has been able to consistently grow their NII by capitalizing on this higher interest rate environment. This increased NII can also be attributed to strong credit quality of their portfolio companies as well as base management fee reductions that were implemented. Management reduced their management fee down to just 1%, from the previous fee amount of 1.375%.

GBDC Q2 Presentation

We can see that this reported NII has also come in slightly higher than Q1 of 2024. This growth resulted in a slight NAV (net asset value) bump from $15.03 up to $15.12. For reference, the NAV during Q1 of 2023 was reported in at $14.73. When we see a growing NAV, this indicates that the BDC has been sufficiently out earnings their distribution by a wide enough margin to get some solid footing. This consistent NAV growth is one of the reasons why we've seen the price rise as quick as it has.

This growth can likely be linked back to the consistent growth in new commitments that took place over 2023. In 2023 GBDC had $456.3M going towards new investments and the results are already starting to show. The weighted average yield on these new investments was 11%, and they mostly consisted of senior secured and subordinated debt, classified as "one stop".

GBDC Q2 Presentation

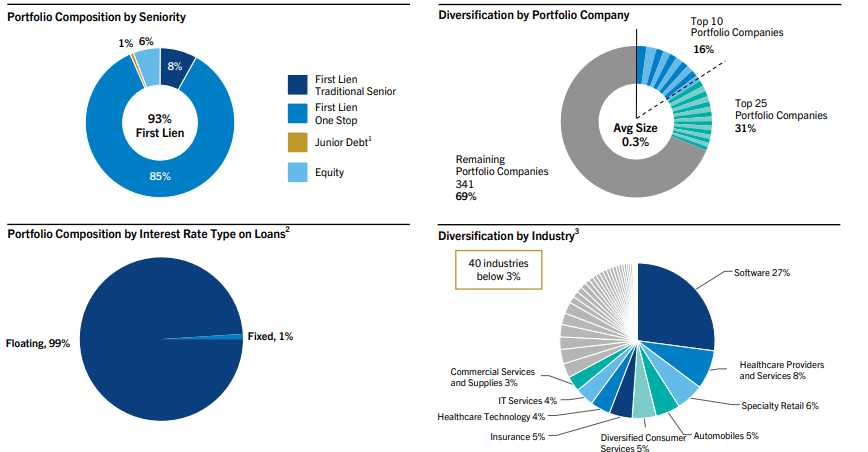

We can see that their portfolio still primarily consists of first lien debt but the equity portfolio slightly increased to 6%. The first lien senior secured debt offers a level of security and risk mitigation since this tier of debt is first of the capital repayment structure. This means that in any cases of default of liquidation of portfolio companies, GBDC's debt is at the top of the priority list for repayment. On the other end of the spectrum, the increased equity exposure increases risk as this tier of financing is on the bottom of the capital structure. However, equity exposure also increases the potential reward that can take place from buyouts or sales.

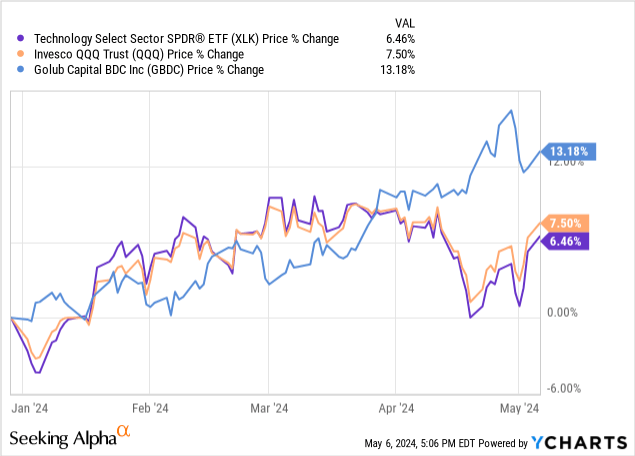

In addition, 99% of their investments are in floating rate debt. This is how GBDC has been able to efficiently capitalize on the higher interest rate environment. Even though the portfolio remains diversified across sectors, the majority exposure is to software companies that are likely tech based. We've seen the technology sector (XLK) and the Invesco QQQ (QQQ) perform well YTD. In fact, it looks like this majority tech exposure may actually contribute to the fact that GBDC's price movement closely mirrors QQQ.

Dividend

As of the latest declared quarterly dividend of $0.39 per share, the current starting dividend yield is 9.2%. As mentioned, NII was reported in at $0.51 per share, which represents a dividend coverage of over 130%. Knowing that the high yield income is highly sustainable in this environment makes it very appealing for income focused investors. This is especially true for those at or nearing retirement that may depend on the income generated from their portfolio.

Not only is the dividend coverage in a comfortable place, but the growth over time has been surprising. For a BDC that's already yielding near double digits, I wouldn't really have much of an expectation around growth. However, GBDC has outperformed here by providing a high dividend growth. The dividend increased at a CAGR (compound annual growth rate) of 16.83% over the last 3 year period. This can be attributed to the higher interest rate environment that we are in, starting with the rapid increasing of interest rates in 2022. Even over a longer time of 10 years, the dividend increased at a CAGR of 3.75%.

Not to mention, the growth of the dividend doesn't even include the special distributions that were issues over the last year and a half. GBDC issued a special dividend in the first quarter of 2024 at $0.07 per share, as well as two different special dividends over the course of 2023. This growth demonstrates how well GBDC has been able to capitalize on this higher rate environment and reinforce its spot as a top BDC in the sector.

Portfolio Visualizer

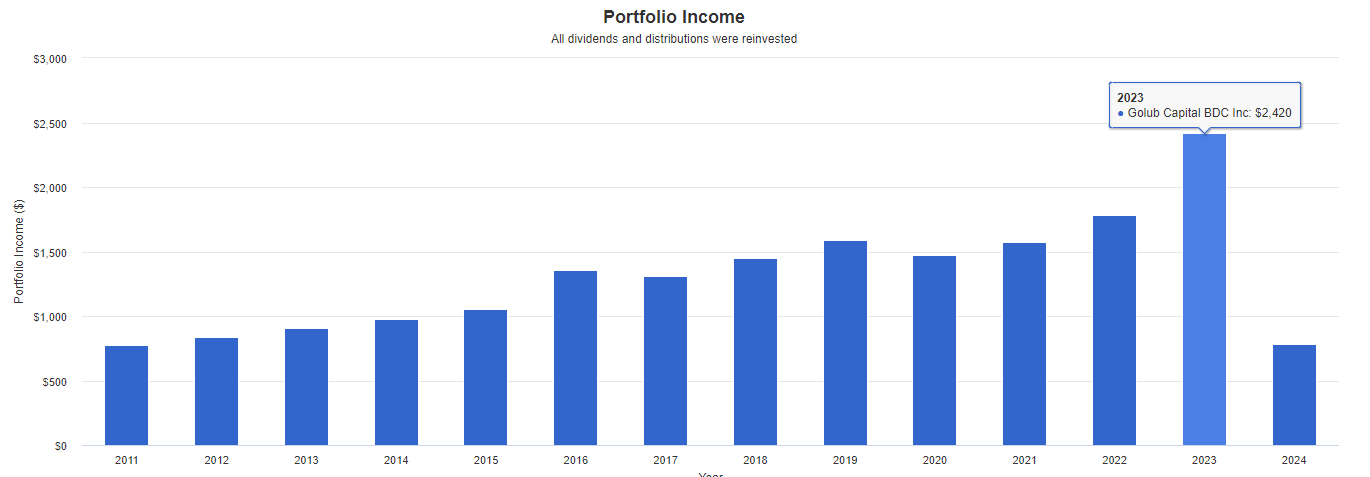

Using Portfolio Visualizer, we can see what kind of results an investment of $10,000 would have. This calculation assumes an initial investment in 2011 with no additional capital ever deployed during the holding period. However, it does include the reinvestment of dividends for every single quarter. In 2011, your investment would have net you $711 in annual dividend income. Fast forward to 2023 and we can see that you would now be receiving $2,420 in annual dividend income and you position value would now be over $30,000.

Different Outlook & Valuation

At the time of my original coverage of GBDC, the Fed was estimated to cut rates on three separate occasions. Since then, the outlook has changed and there have been no cuts so far in 2024. Even if rates are eventually cut at this point, I expect the cuts to be light. I anticipate light cuts in the future based on their uncertainty. Lighter rate cuts could allow them to test the waters and see how the economy reacts.

The Fed is expected to hold rates unchanged in June. Due to a consistently higher than expected level of inflation in combination with a solid job market, the Fed stays cautious of raising rates too soon. As a result, they've opted to wait and let more economic data roll in month by month. Bank of America analysts estimate that there's a possibility we won't see rate cuts until 2025.

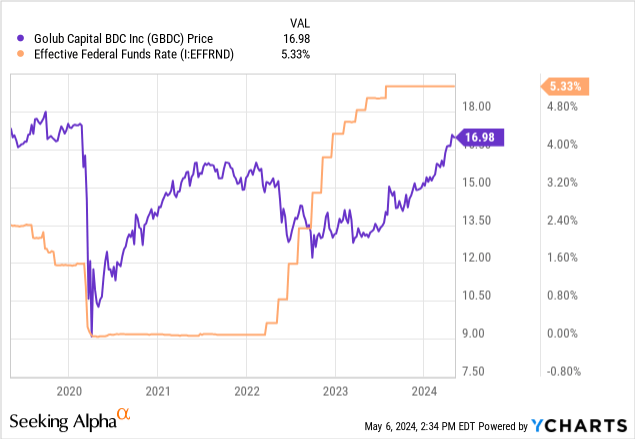

GBDC is now nearing its pre-pandemic levels of $17 per share and above. When rates started to rapidly rise in 2022, the price initially reacted to the downside and lost its momentum from 2021. However, I believe the high quality portfolio, management, and NII growth led to the price still climbing even while rates were high. As the portfolio value grew from additional investments and NII rose, the valuation of GBDC increased as well.

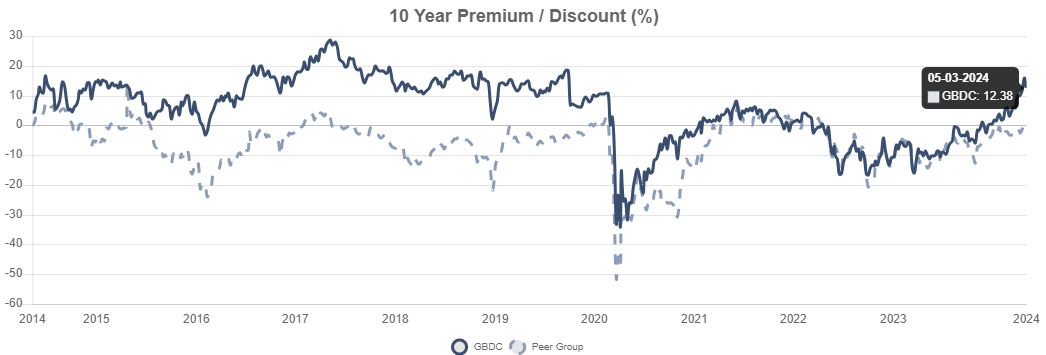

We can see this increase in valuation even when looking at the current premium to NAV (net asset value) that GBDC trades at. The current price sits at a premium to NAV above 12%. For reference, the price traded at an average discount to NAV of -2.78% over the last 3 year period. When I last covered GBDC, the premium sat at a very modest 2% level where I was comfortable adding.

CEF Data

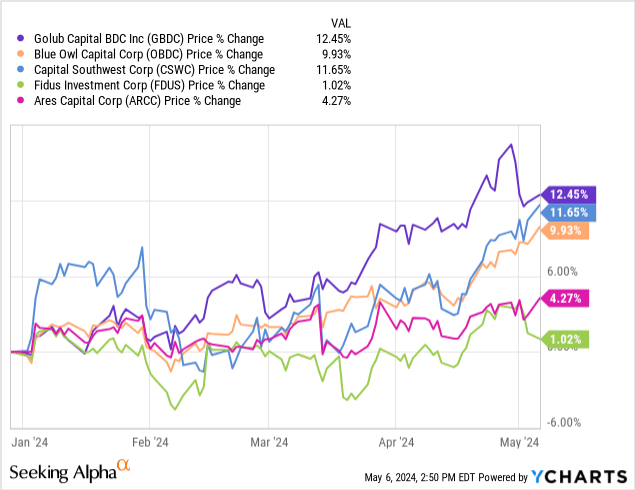

However, now that the premium to NAV sits at one of the highest points over the last 4 year period, I no longer feel comfortable adding here. Despite the high quality performance, portfolio, and improved financial prospects, I believe that it would be best to rate GBDC as a Hold. Just for further reinforcement, we can see that GBDC has outperformed some popular peer BDCs in pure price growth YTD.

Risk Profile

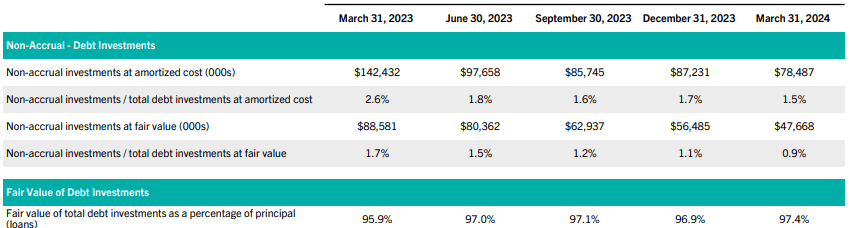

In terms of risk, I wanted to focus on the rate of non-accruals this time around. While the higher interest rates can be a great thing since it pulls in higher levels of interest income and ultimately means a growing NII, it can also be a negative. When interest rates remain elevated for such a prolonged period of time, it can cause strain on some companies that are debt burdened. The higher rates mean that they owe more interest on the capital they've acquired and when the environment stays this way for a longer period of time, it can stifle growth of these borrowers.

GBDC Q2 Presentation

As a result, we tend to see an increase in companies that reach non-accrual status. Non-accrual status is a classification given to portfolio companies that have reached delinquent status with their debts and no longer contribute to GBDC's net investment income. Typically, the debt owed no longer has the expectation of being recovered when it's reached this point. We can see that the non-accrual rate as actually decreased for GBDC from the previous quarter and sits at 1.5% at cost. Therefore, GBDC has actually done a great job at decreasing the risks from this aspect. For reference, here are some relevant BDC non-accrual rates.

- SLR Investment (SLRC): 0.6% non-accrual at cost

- Hercules Capital (HTGC): 1.2% non-accrual at cost.

- BlackRock TCP Capital (TCPC): 3.6% non-accrual at cost.

In terms of liquidity, GBDC has cash and cash equivalents totaling $300M that can help ride out any potential headwinds. In addition, they have solid credit ratings from Fitch, Moody's, and S&P Global. Therefore, I believe GBDC sits in a pretty safe spot and their portfolio is well-managed.

Takeaway

Golub Capital remains a high quality BDC that has outperformed many of its peers. This is likely due to its majority exposure to the tech sector which has seen impressive growth for the year, in combination with a high-quality portfolio with decreasing non-accruals. In addition, NII as increased due to management efficiently capitalizing on this higher interest rate environment as well as cutting their base management fee.

The dividend yield of 9.2% remains extremely well-covered with NII providing a coverage rate of over 130%. However, GBDC has become expensive as the price now sits at a high premium to NAV. This premium is the highest it has been over the last four year period. As a result, I am downgrading GBDC to a Hold and will revisit if the price becomes more attractive for entry.