Prostock-Studio/iStock via Getty Images

Introduction

It's been a wild few days for Hims & Hers (NYSE:HIMS) stock.

Last Friday, CEO Andrew Dudum posted several controversial tweets on X, one of which included his support for university students to protest "against the genocide of the Palestinian people & for your university's divestment from Israel".

This sparked a lot of rage and panic among the investing community, sending HIMS stock 8% lower in a single trading day. Even Shark Tank Co-host Kevin O'Leary and English broadcaster Piers Morgan were disgusted by Dudum's recent comments.

Most people were quick to judge that Dudum might be anti-Israel or pro-Hamas, and that his political views could eventually bring the whole company down.

Fortunately, on Sunday, Dudum followed up with a few clarifying tweets, making it clear that he does not "support acts or threats of violence, antisemitism, or intimidation" and that he was just expressing his "support for peaceful protest".

As a result, HIMS stock rebounded on Monday.

I don't want to get too much into politics but the point is that Dudum said a few things that upset a lot of investors despite exercising his right of free speech as a descendant of Palestinian refugees.

A day later, H&H reported blowout earnings that sent the stock flying more than 15%.

How quickly sentiment can change...

People quickly forget that H&H is a well-run company with strong and improving fundamentals — I'm here to remind you of that.

Political risks could be a major reason to sell HIMS stock.

But here are 10 solid reasons why H&H is still a great buy.

Reason #1: Redefining Healthcare

In a nutshell, H&H is a telehealth platform that provides consumers access to high-quality medical care that is highly convenient, accessible, and affordable. H&H offers a much superior patient experience when compared to legacy healthcare systems where treatments are generally expensive, time-consuming, and complex.

This is especially true with its personalized offerings, which are customized healthcare solutions based on unique individual needs, such as dosage levels, form factors, and multiple conditions. Traditional healthcare systems often prescribe patients with one-size-fits-all solutions, which may not produce the results that patients are looking for — H&H is changing that.

By offering personalized solutions, H&H patients get more results and satisfaction. This is why consumers are flocking to H&H, as seen by the rapid increase in the number of Subscribers opting for personalized subscriptions, which was over 602K as of Q1, up 176% YoY and up nearly 6x since Q2 of 2022.

Author's Analysis

In addition, H&H has always marketed itself as an easy-going, innovative brand that people can trust. This branding strategy and focus on innovation provide a healthcare experience unlike any other, which is why H&H has resonated with so many people.

Reason #2: High-quality Business Model

H&H operates a predominantly subscription-based business model. Moreover, I think H&H is recession-resistant given that people always put health as their top priority. This allows H&H to generate consistent, predictable Revenue.

Furthermore, management also said that the company is seeing stronger retention levels when customers sign up for personalized offerings relative to generic alternatives. This further improves Revenue quality.

Not only that but H&H also has a high Gross Margin of 82%, which expanded by 200bps YoY, demonstrating economies of scale within the business. Gross Margin improvement was due to increased volume at Affiliated Pharmacies.

Author's Analysis

A high Gross Margin profile means strong earnings potential. It also means more flexibility in terms of pricing. Given its high-quality business model, H&H has the luxury of providing high-quality healthcare at mass-market prices, without sacrificing quality or inflicting considerable damage to its bottom line.

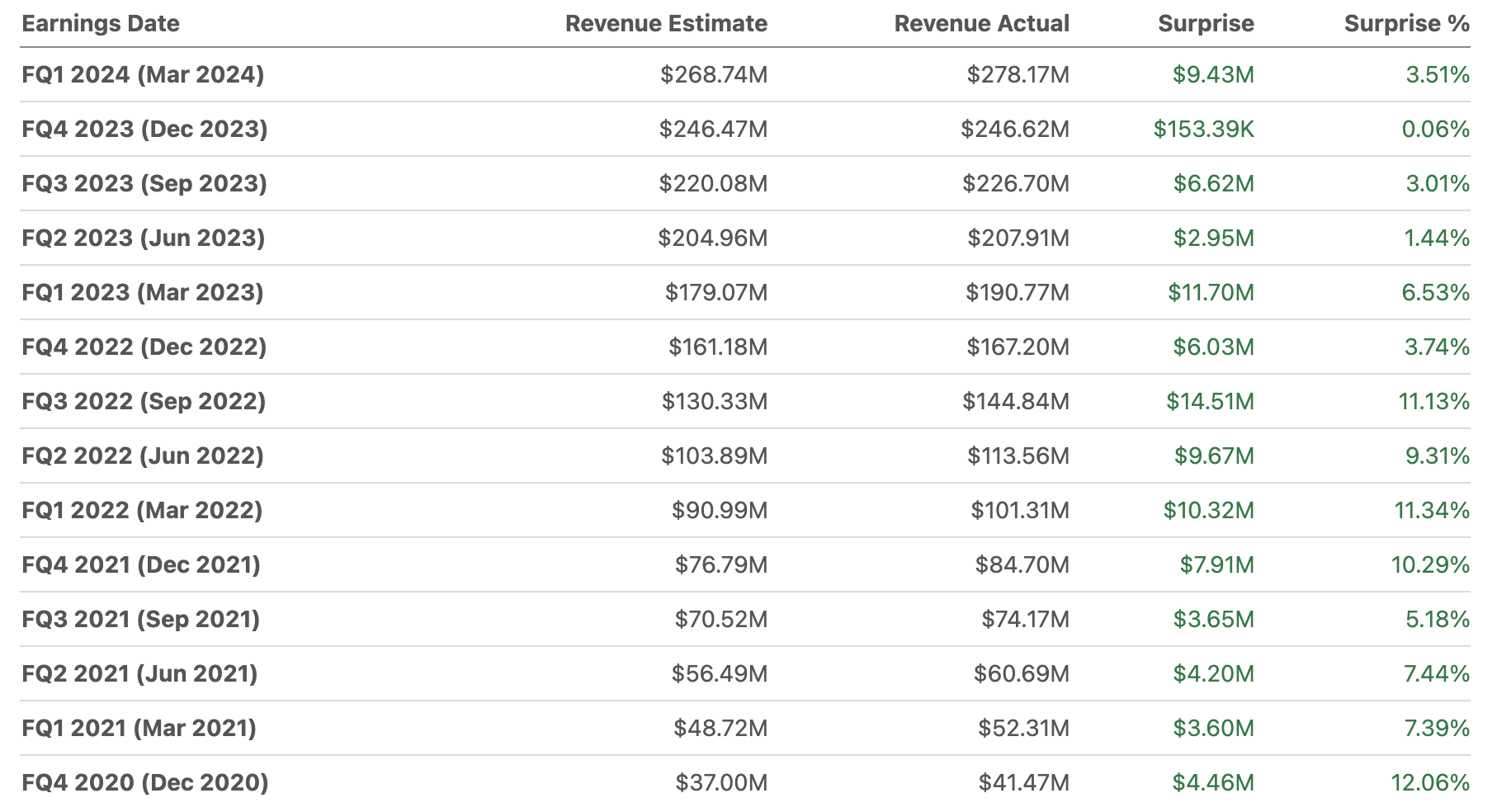

Reason #3: Blistering Growth

In Q1, Revenue was $278M, up 46% YoY, which beat analyst estimates by $9M and the high-end of management's guidance by $6M.

Growth has been phenomenal, and as you can see, H&H has been growing at high double-digits consistently over the last few years.

Author's Analysis

Growth was primarily driven by the company's expanding Subscriber base, which was 1.7M as of Q1, up 41% YoY, with particular strength from personalized solutions, which I talked about earlier.

Of important note, H&H added a record 172K Net New Subscribers in Q1, showing strong demand and brand awareness. Subscriber growth is a leading indicator of future Revenue growth so it's great to see the company grow its Subscriber base like this.

In short, there's no denying H&H's blistering growth.

Author's Analysis

Reason #4: Self-sufficiency

And it's not like H&H is issuing loads of equity or debt to supercharge its growth. Yes, it did have a capital boost a few years ago from its SPAC merger with Oaktree Acquisition Corp. But other than that, H&H has maintained a pristine balance sheet with virtually zero debt. At quarter end, the company has a Net Cash position of $192M.

You may have noticed that Net Cash dropped slightly QoQ. Well, that is due to the company buying back $28M worth of its common stock in Q1, which helps minimize shareholder dilution. As of Q1, $20M remains under its buyback program — at its current buyback rate, I expect a new buyback program to be announced as early as Q2, which should be a catalyst for the stock.

Author's Analysis

Management is comfortable buying back the stock since the company is already cash flow positive. In Q1, Cash Flow from Operations was $26M, which was the highest it has ever been for the company.

Free Cash Flow was $12M, representing a FCF Margin of 4%. As you can see, FCF was not as high as it was back in Q3. That's because H&H has been ramping up CapEx to expand and improve its Affiliated Pharmacies.

That being said, it's great to see the company allocate excess capital for share buybacks and further growth. And this is only possible because the company has no debt and is cash flow positive, making H&H, by definition, self-sufficient.

Author's Analysis

Reason #5: GAAP Profitability

H&H's improving profitability has also contributed to its self-sufficiency.

In Q1, GAAP Net Income was $11M, representing a 4% Net Margin, which expanded 900bps YoY and 300bps QoQ.

For the most part, H&H was unprofitable — but now, they have recorded their second consecutive quarter of GAAP Net Income profitability, eliminating one of the biggest bear arguments against the stock: H&H can't turn a profit.

Author's Analysis

Here, we can see the same trend as Adjusted EBITDA, which was $32M in Q1. Adjusted EBITDA Margin was 12%, up 900bps YoY and 400bps QoQ. Considering the company's growth and profitability momentum, it won't be long before H&H reaches its long-term Adjusted EBITDA Margin target of 20% to 30%.

Author's Analysis

Margin expansion was due to operating leverage as H&H continues to scale.

Of important note, H&H drove strong marketing leverage with Marketing Expenses as a % of Revenue dropping 400bps YoY to 47%. Management expects this ratio to drop to "high 30s to low 40s by the end of the decade" — I expect H&H to hit this target within two to three years.

Hims & Hers FY2024 Q1 Shareholder Letter

Customer Acquisition Costs (CAC) per New Subscriber was $658, an improvement from $965 in Q4. Payback Period was 0.49 years, an improvement from 0.52 in Q4. In other words, H&H's marketing is getting more efficient with the company getting back their money faster. This eliminates another bear argument against the stock: H&H's CAC is unsustainably high.

Author's Analysis

The main point here is that H&H has turned GAAP profitable with margins set to improve further over the next few years. The flip to profitability is definitely a surefire statement that H&H has a scalable business model capable of generating strong earnings for investors.

We are pleased to see this amount of leverage during a time of robust growth and record level additions of net new subscribers because it serves as a proof point of our ability to maintain strong growth while driving leverage.

(CFO Yemi Okupe — Hims & Hers FY2024 Q1 Earnings Call)

Finding fast-growing, profitable companies is incredibly difficult — H&H is a rare find.

Reason #6: Skin in the Game

This one is a double-edged sword.

The positive: H&H is a founder-led company with a visionary CEO at the helm. In addition, CEO Andrew Dudum holds about a 9% stake in the company, so he has a lot of skin in the game.

Simply Wall St

The negative: As we've seen recently, the CEO could be reckless at times. Moreover, due to the dual-class common stock structure, Dudum holds approximately 90% of the outstanding voting power, which means that Dudum has the final say. Even if they wish to, the board has no power to remove Dudum from office.

Whichever camp you choose is entirely up to you. As for me, I prefer to focus on the positive.

I believe it is Dudum's best interest to continue leading and building the company that he founded 7 years ago. He has come too far to put H&H at great risk solely to fulfill his political interests.

Reason #7: Perfect Execution

As a public company, H&H has a 100% track record of beating analyst Revenue estimates. As you can see below, there's no red ink in sight. That speaks volumes about how strong demand is and how well management has executed so far.

Seeking Alpha

And time and time again, management has walked their talk — by a mile too. Here are two examples:

- In their SPAC merger presentation, management projected Revenue of $233M in 2022. How much did they actually do? $527M. More than double what they promised.

- Management also guided for Revenue of $1.2B+ and Adjusted EBITDA of $100M+ in 2025. Guess what? They're on track to achieve these targets a year early.

This level of execution is unheard of.

Reason #8: 10M+ Subscribers

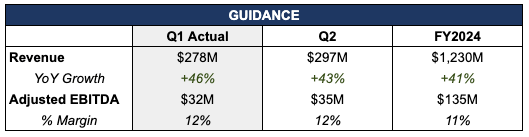

Below, you can see management's guidance for Q2 and FY2024.

In short, the short-term outlook is very strong. Management raised full-year guidance, which happened to beat analyst estimates as well. Nothing new.

Author's Analysis

However, the long-term growth story revolves around one simple idea:

We aim to build a platform where there are tens of millions of customers across Hims & Hers, and believe that the suite of categories and specialties we offer today, as well as the ones we'll continue to expand into, are categories that affect nearly every household in the country.

(CEO Andrew Dudum — Hims & Hers FY2024 Q1 Earnings Call)

As it stands, H&H has amassed 1.7M Subscribers.

The next target is 10M+ Subscribers.

And management has laid out their plan to achieve this big hairy audacious goal:

- Increase Affordability: Management wants to provide high-quality medical care at mass-market prices. Given high Gross Margins and the efficiency gains that they have recently enjoyed, management intends to pass on the savings to consumers, which should lure more Subscribers into the platform.

- Focus on Personalization: There's unprecedented demand for personalized healthcare solutions — management is doubling down on this department. As of Q1, over 35% of its Subscriber base opted for a personalized solution. Management plans to boost this number.

- Maintain High Brand Awareness: As mentioned earlier, management plans to keep Marketing Expenses as a % of Revenue in the mid-30s to low-40s. This should attract new users to the platform.

- Growing the Hers Brand: The CEO mentioned that the Hers brand is one of, if not, "the fastest growing parts of the business". Hers market penetration rate is only 1% to 2%, so management is determined to grow the women's side of their business. This should bring in more female Subscribers.

- New Category/Product Launches: As a result of its expanding network, database, and automation capabilities, H&H will be launching multiple new products in the coming weeks. This should include other categories like "hormonal balance, menopause, testosterone, pain management, insomnia", and even its highly-anticipated GLP-1 product. This should attract new demographics to the platform.

Above all, what 10M+ Subscribers mean is that H&H still has a long growth runway ahead, which also means that...

Reason #9: Earnings Compounder

... H&H has the potential to compound earnings for shareholders.

Earnings growth drives stock returns. Simple as that.

And with the company on the best fundamental footing — from a growth, profitability, and cash flow perspective — in its entire history as a company, I believe H&H will be a serious earnings compounder in the not-so-distant future.

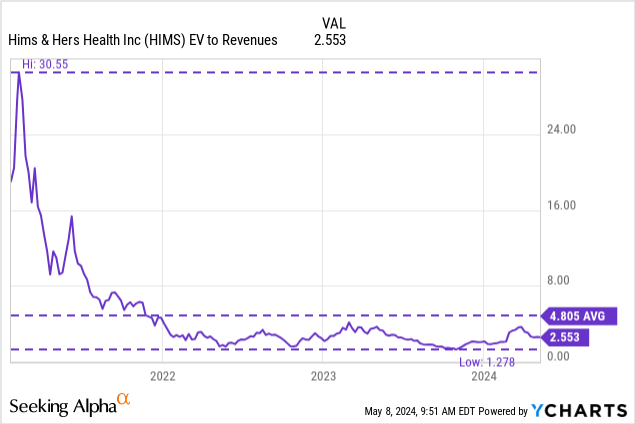

Reason #10: Attractive Valuation

Reasons #1 to #9 don't matter if reason #10 doesn't tick — valuation always matters.

As it stands, HIMS stock trades at an EV to Revenue multiple of just 2.6x, which is extremely cheap considering all the reasons stated above. Compared to its historical multiple, HIMS also trades very attractively.

As for me, I'm keeping my base-case price target relatively unchanged at $28, which represents an upside potential of 139% based on the current price of about $12.

As a reference, analysts have an average price target of $16, which represents an upside potential of 36%.

Author's Analysis

Despite being up more than 100% over the last six months, I believe HIMS stock is still chronically undervalued. I have always argued that there's a divergence between HIMS stock and its fundamentals — as the business continues to grow, the stock continues to struggle.

At some point, the stock will have no choice but to gravitate towards the company's solid fundamentals.

Thesis

Investors have been blindsided by CEO Andrew Dudum's recent political comments. That's why the stock has been struggling lately, despite excellent Q1 results.

I do wish Dudum could stay out of politics — but who am I to stop a man from exercising his freedom of speech? As long as he does not endorse any form of violence and terrorism, I'm alright with him voicing his political opinions.

If he does, then I'm forced to sell.

For now, it's just noise — best to just block it and focus on the 10 solid reasons to own HIMS stock.