gorodenkoff/iStock via Getty Images

Investment Thesis

Management for Intuitive Surgical (NASDAQ:ISRG) recently participated in Bank of America’s Healthcare conference last week. I found some of the commentary and forward-looking perspectives laid out by management particularly intriguing as they relate to my long-term outlook related to Intuitive Surgical.

Some of the comments that management laid out in the healthcare conference last week allowed me to set some more reasonable expectations around this robotic surgery-focused company, particularly around the company’s operating margins that have always been robust pre-pandemic. In addition, the company also reported the first quarter earnings report for FY24, which I will also incorporate into my revised valuation model.

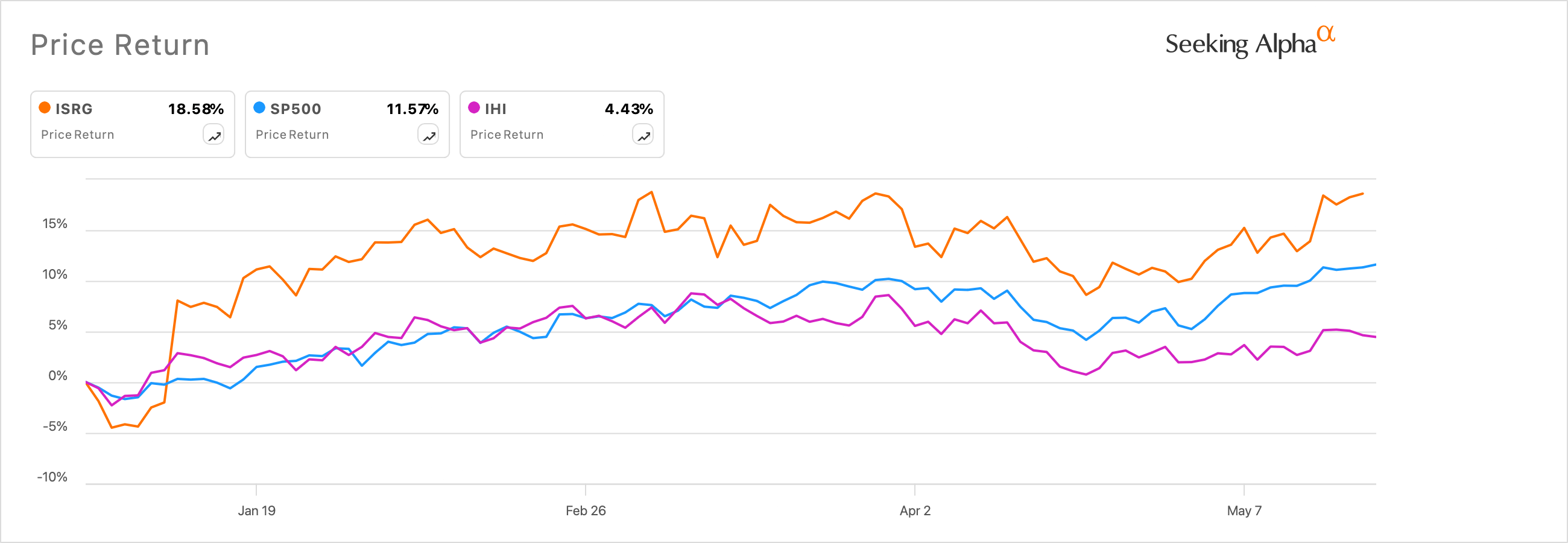

For the year, Intuitive Surgical has beaten the broader market indices, such as the S&P 500 Index, as well as its peer group, as seen in Exhibit A below. In the following exhibit, I have used the iShares U.S. Medical Devices ETF (IHI) to round up most of Intuitive Surgical’s peers into one bucket.

Exhibit A: Intuitive Surgical’s stock beats markets and its peer group (SA)

Based on the recent commentary from management and its forward-looking perspectives, I continue to maintain my Hold rating on the company, but I’m lowering my target price.

Procedure growth was stronger than expected

In my previous coverage of Intuitive Surgical, I mentioned the company “continues to impress me with an impressive show of strength in its earnings report for FY23.” Part of my marginal level of skepticism about the valuation stemmed from the ~20% run-up in the stock at the time I first published my previous coverage. But based on trends I saw at the time, I was still optimistic about Intuitive Surgical because “macrotrends in hospitalization and inpatient care are [were] turning into tailwinds.” At the time of my last coverage, I said that I was “confident that the company is positioned to significantly beat their FY24 procedure growth.”

Most of that optimism played out as I expected based on the results published by Intuitive Surgical’s management in Q1 FY24.

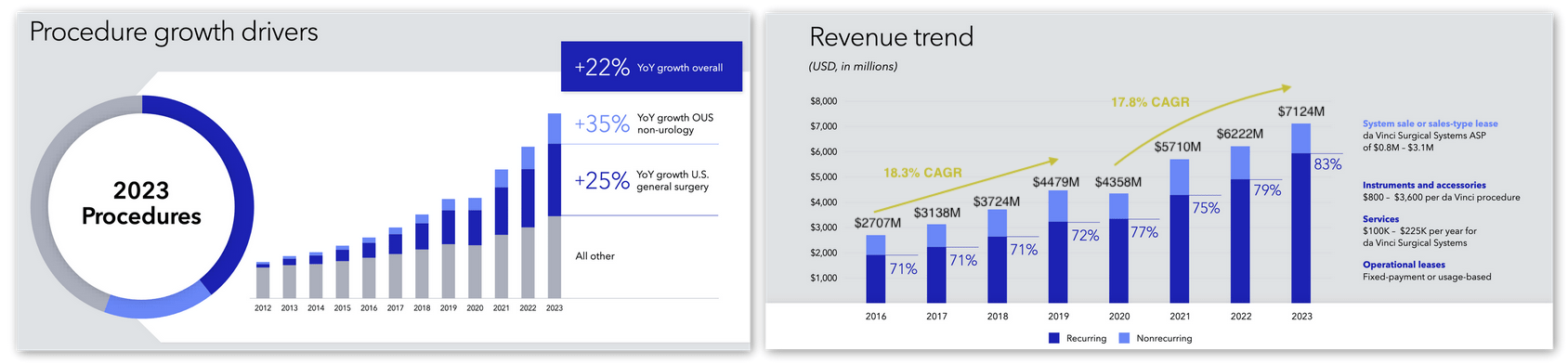

In Q1 FY24, the company reported that surgical procedure volume, a measure to track the number of surgical procedures conducted on the company’s robotic surgical systems such as the da Vinci, grew 16% y/y. This was at the higher end of their 13–16% projection range for FY24 procedures laid out in the previous Q4 FY23 quarter’s earnings call. I was pleased to see these results, and I agree with the general consensus that the procedure growth the company posted was quite strong. To top the results off, management revised their procedure growth for FY24 higher, now expecting 14–17% procedure growth in FY24.

This resulted in a strong performance in the company’s top line, with management reporting revenues grew 11.8% y/y to $1.89 billion, beating expectations by $20 million.

These were strong numbers posted by management, especially given that the company outperformed expectations in FY23 and was able to post robust double-digit growth in procedures and revenue, as seen in Exhibit B below.

Exhibit B: Intuitive Surgical’s revenue and procedure annual growth (Q1 FY24 Investor Presentation, Intuitive Surgical)

Looking for a reversal in operating leverage

There is no doubt that the company has been able to experience a strong reversal in growth after facing headwinds during the pandemic. As seen in Exhibit B above, revenue has grown at a 17.8% CAGR after the pandemic, almost catching up to the pre-pandemic revenue growth rate of 18.3% CAGR.

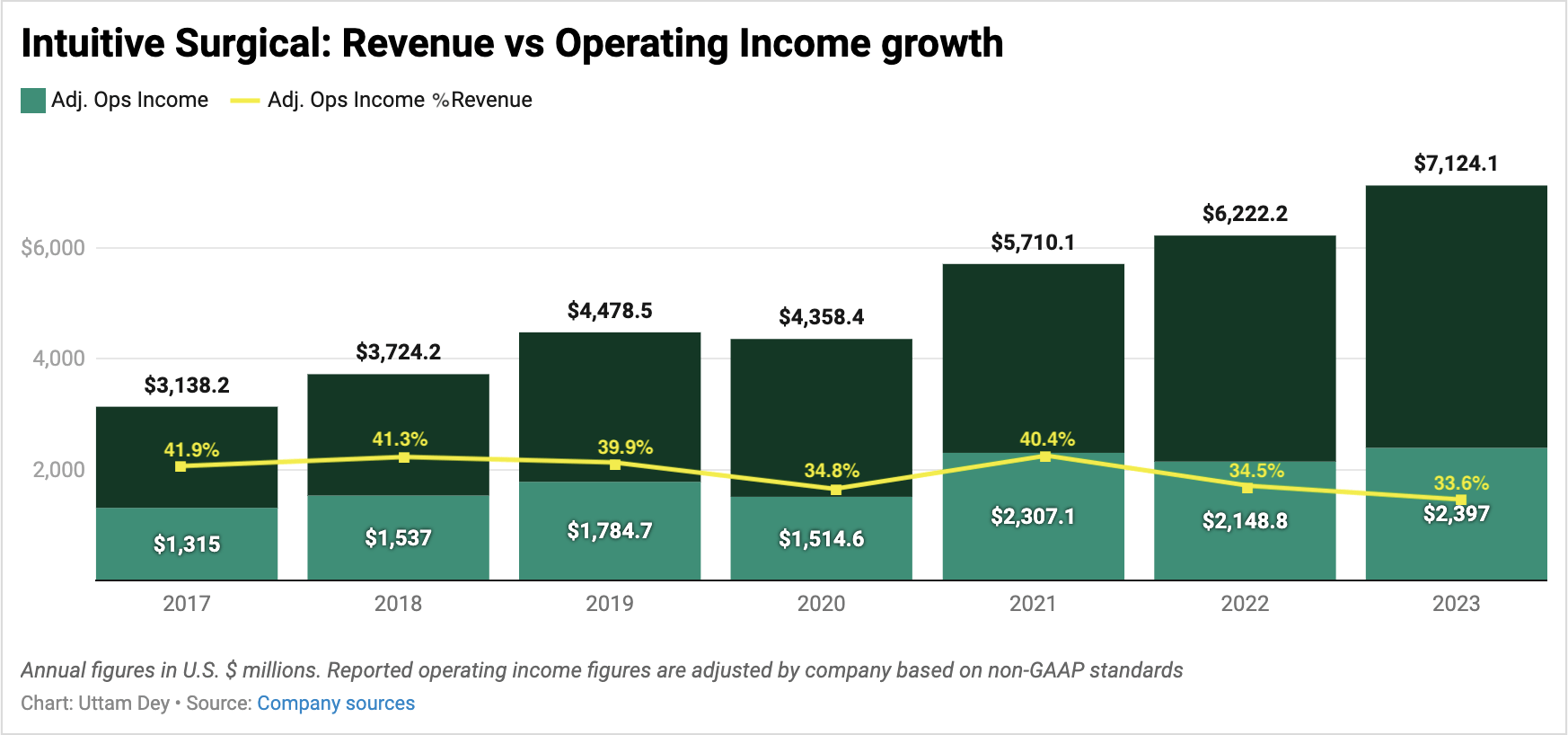

However, the company’s operating margin profile still needs to participate in that post-pandemic growth phase. As seen in Exhibit C below, the company’s adjusted operating income has grown ~16% on a compounded basis, lagging behind the ~18% CAGR growth rates posted at the top of the company’s books.

Exhibit C: Intuitive Surgical’s Operating Income on an adjusted basis is still to participate in its post pandemic growth phase. (Company sources)

At the Bank of America Healthcare conference last week, management mentioned that they are working towards alleviating the margin compression seen, especially in their operating income. What could also be further impacting the margins in the near term is the rollout of the company’s da Vinci 5 robotic surgery system. Management has previously mentioned that they expect to eventually “improve these margins over a multiyear period.”

At the BofA Healthcare conference, when asked whether investors should model for operating margins either in line with or slightly below procedure growth, management said:

That is the intent. So, with operating margins, they are lower than they have been historically. It's not our -- or it's not a management objective to get back up to 40%. I would say our expectation is to be at the upper end of our peer set.

Based on these comments, I will now expect management to target the 35–37% operating margin range over the next few years on an adjusted basis instead of the higher margin range I was initially anticipating.

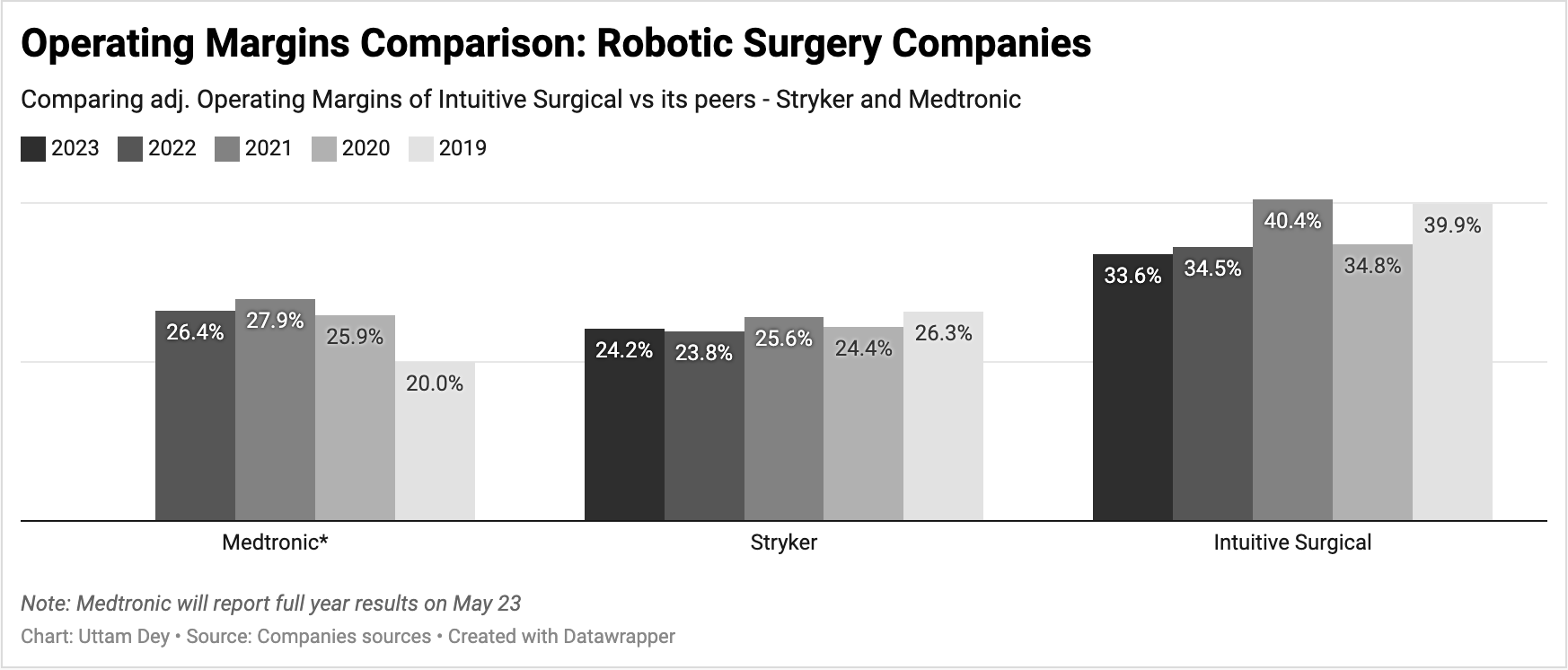

Also, I do note that if I compare Intuitive Surgical’s operating leverage to its peer set, Medtronic (NYSE:MDT) and Stryker (NYSE:SYK), as company management alluded to in the healthcare conference, Intuitive Surgical does operate its business with superior operating leverage as compared to its peers.

Exhibit D below is not an exhaustive comparison since both of these companies include other reportable segments as well in their business, but it still gives investors an idea.

Exhibit D: Intuitive Surgical’s Operating Income on an adjusted basis is still to participate in its post pandemic growth phase. (Companie sources)

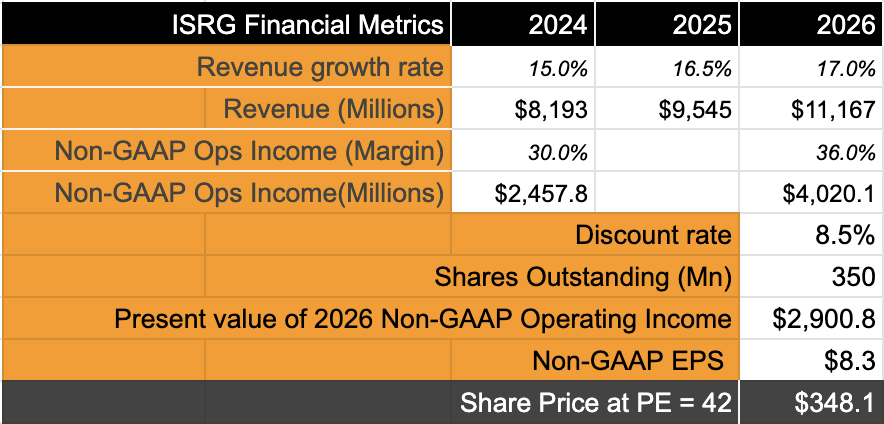

Intuitive Surgical Still a Hold with Price Targets lowered

Here are some of my assumptions factored into my valuation model:

I am raising my revenue outlook from 15% CAGR to 16% as I expect demand to sustain due to the launch of the da Vinci system this year, despite the da Vinci being available for ~15% that of its predecessor, on a like-for-like basis.

My assumptions for adjusted operating margins were laid out in the previous section, where I now assume a margin range of 35–37%.

Discount rates are slightly raised to account for higher beta, calculations here.

Exhibit E: Intuitive Surgical’s valuation model shows downside (Author)

Based on my new outlook, I am using a higher forward valuation multiple despite 19% growth in operating margin as compared to the 8% long-term earnings growth in the S&P 500. I am using this because the company typically displays patterns of beats-and-raises, outperforming its expectations, as seen in the decade-long history below in Exhibit F.

Exhibit F: Intuitive Surgical’s outperformance history (SA)

Despite the downside that I see, I believe the company has solid management and will be able to navigate the company higher, so any deep pullbacks would present investors with buying opportunities. Hence, despite the downside in the stock, I still rate Intuitive Surgical as a Hold.

Risks and other factors to look for

Apart from the usual macroeconomic risks, the da Vinci 5 poses some threats to its growth, in my opinion. I fully expect management to continue as planned with their phased-wise approach to launching and making the da Vinci 5 available to a wider customer base. These plans take the company well into FY25, as per management. That is a large time frame for the company to face sudden headwinds and revise its launch for the da Vinci 5, which would impact its higher-teen growth rates that I have currently baked in. For now, I am not expecting management to miss any steps here.

Note: One of Intuitive Surgical’s peers, Medtronic, will be reporting their own full year FY24 results this week on Thursday, May 23, 2024, before markets open.

Takeaways

Intuitive Surgical still appears to be posting strong growth rates in the teens as management revises their procedure growth based on increasing demand. However, I expect commentary around the company’s margin outlook may weigh on the company until management can revise plans for its operating leverage. This is still a good company that is capable of posting all-round growth.

For those reasons, I believe Intuitive Surgical is a Hold, but any deep pullbacks offer investors a buying opportunity.